- Beauty & Personal Care

- U.S. Women Grooming Market

U.S. Women Grooming Market Size, Share, and Growth Forecast 2026 - 2033

U.S. Women Grooming Market by Product Type (Skincare, Haircare, Deodorants & Fragrances, Oral Care, Others), by Category (Mass, Premium), by Ingredient Type (Conventional, Natural & Organic), by Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Pharmacies, Online Retail, Convenience Stores), by Regional Analysis, 2026 - 2033

U.S. Women Grooming Market Size and Trend Analysis

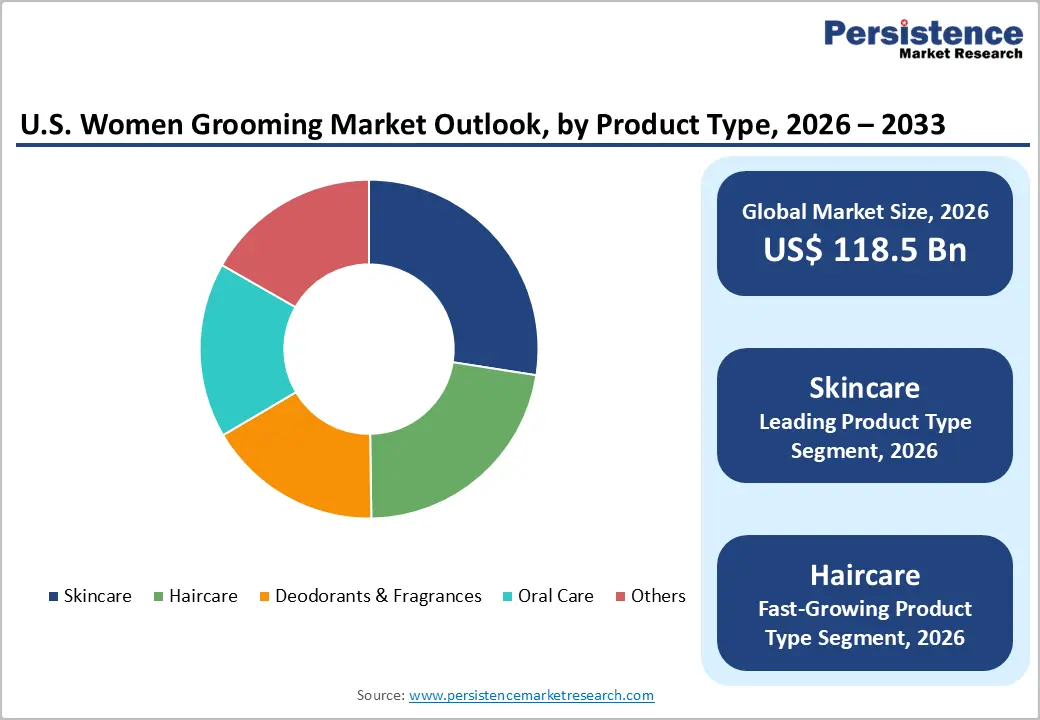

The U.S. women grooming market size is expected to be valued at US$ 118.5 billion in 2026 and projected to reach US$ 174.7 billion by 2033, growing at a CAGR of 5.7% between 2026 and 2033.

Sustained expansion is being driven by rising female workforce participation, an entrenched self-care culture, and accelerating demand for clean, dermatologically tested formulations. According to U.S. Bureau of Labor Statistics data, women accounted for nearly 47% of the total U.S. labor force in 2024, supporting consistent discretionary spending on skincare, haircare, and personal hygiene. Concurrently, social commerce, dermatologist-led influencers, and a heightened focus on preventive wellness continue to push category innovation and premiumization.

Key Market Highlights

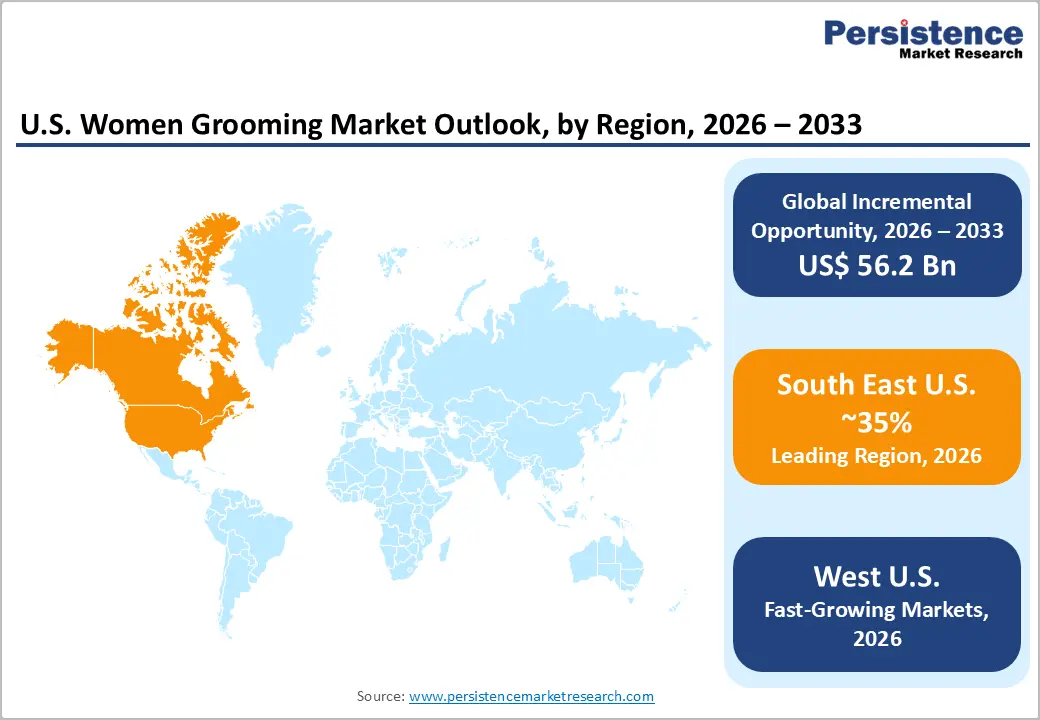

- Leading Region: The West region leads the U.S. women grooming market with an estimated 28% value share in 2025, driven by California's beauty innovation hubs, high disposable income, and concentration of indie clean-beauty brands.

- Fastest Growing Region: The Southwest is the fastest-growing region through 2032, supported by Hispanic population expansion, climate-driven sun-care demand, and beauty manufacturing investments across Texas and Arizona.

- Dominant Segment: Skincare dominates the U.S. women grooming market with an estimated 35% value share in 2025, anchored by daily routines spanning cleansers, moisturizers, sunscreens, serums, and clinically validated anti-aging formulations.

- Fastest Growing Segment: Haircare is the fastest-growing product type through 2032, propelled by scalp-health awareness, bond-repair innovation, sulfate-free formulations, and the surge of texture-specific products for diverse hair types.

- Key Market Opportunity: Growth of natural, organic, and microbiome-friendly formulations represents a major opportunity, supported by USDA organic certifications, MoCRA transparency mandates, and rapidly scaling DTC and social-commerce channels.

Market Dynamics

Market Growth Drivers

Rising Women's Workforce Participation and Disposable Income Fueling Premium Grooming Demand

Strong income growth among American women is translating into materially higher per-capita spending on grooming products. The U.S. Bureau of Labor Statistics reported that women's median weekly earnings reached US$ 1,055 in 2024, up nearly 4.2% year-over-year, while the U.S. Census Bureau noted that real median household income rose to US$ 80,610 in 2023, supporting consistent discretionary outlays on personal care, skincare, fragrances, and premium haircare formats.

Reinforcing this trend, the U.S. Bureau of Economic Analysis confirmed that personal consumption expenditure on personal care products has grown consistently above 5% annually since 2022. This income strength is fueling trade-up to premium serums, vitamin-C ampoules, scalp treatments, and luxury fragrances, anchoring durable, long-term demand momentum across the U.S. women grooming spectrum and accelerating premiumization.

Clean-Beauty Movement and Dermatologist-Led Skincare Adoption Wave

The U.S. Food and Drug Administration (FDA) enacted the Modernization of Cosmetics Regulation Act (MoCRA) in late 2022, mandating facility registration, ingredient safety substantiation, and adverse-event reporting from December 2023. This regulatory tightening has accelerated industry-wide reformulation toward transparent, clinically validated, and dermatologically tested products, reshaping innovation roadmaps and elevating consumer expectations for ingredient integrity across the U.S. cosmetics market and adjacent grooming subcategories.

Reinforcing this momentum, a 2024 American Academy of Dermatology survey reported that 63% of U.S. women now consult dermatologists or use dermatologist-recommended products, up from 48% in 2019. Demand for sulfate-free shampoos, retinol alternatives, and microbiome-friendly formats is rising sharply, prompting category leaders to expand SKUs, license patented actives, and structurally enlarge addressable grooming demand.

Market Restraints

Ingredient Inflation and Persistent Global Supply-Chain Volatility Pressure

The U.S. Bureau of Labor Statistics Producer Price Index for personal care manufacturing rose 6.8% cumulatively between 2022 and 2024, reflecting elevated costs of glycerin, hyaluronic acid, palm derivatives, and packaging resins. U.S. Customs and Border Protection data shows a 9% increase in cosmetic ingredient import duties since 2023, materially raising the landed cost base for both mass and premium grooming brands operating across the U.S. market.

Compounding these cost pressures, shipping disruptions through the Red Sea inflated freight rates by nearly 30% in 2024 according to the U.S. Department of Transportation Maritime Administration. These pressures are squeezing margins of mass-market women grooming brands, forcing price hikes that risk eroding volumes among value-conscious shoppers, especially in deodorants and oral care segments where price elasticity remains high.

Tightening Regulatory Scrutiny on Chemical Ingredients and Reformulation Costs

Under MoCRA, the U.S. Food and Drug Administration (FDA) has expanded its oversight of fragrance allergens, talc, formaldehyde releasers, and PFAS compounds. The Environmental Working Group flagged that more than 2,000 personal care products in the U.S. still contain restricted substances, intensifying compliance scrutiny and forcing brands to undertake costly ingredient swaps, supplier audits, and re-validation programs across legacy product portfolios.

Adding further complexity, state-level laws such as California Assembly Bill 2762 and Washington's Toxic-Free Cosmetics Act of 2023 ban over 20 chemicals from cosmetics sold from 2025 onward. Compliance requires costly reformulation and stability re-testing, which slows innovation pipelines and disproportionately burdens smaller indie brands competing within the broader U.S. personal care market, creating near-term drag.

Market Opportunities

Surge in Natural, Organic, and Microbiome-Friendly Grooming Formulations

Consumer pivot toward clean, plant-derived, and biome-balancing chemistry is opening a high-margin runway for incumbents and new entrants across the U.S. women grooming landscape. The U.S. Department of Agriculture (USDA) National Organic Program certified more than 2,800 personal care SKUs by 2024, a 35% rise from 2021, while NSF International reported that natural personal care certifications grew 18% year-over-year in 2024.

Capitalizing on this shift, brands such as The Honest Company, Inc., Burt's Bees (a subsidiary of The Clorox Company), and Drunk Elephant (owned by Shiseido Company, Limited) are scaling biome-friendly shampoos, prebiotic deodorants, and waterless concentrates. This momentum is also unlocking incremental traction within the U.S. natural cosmetics and organic personal care markets, both expected to outpace conventional grooming through 2033.

Rapid Growth of Direct-to-Consumer and Social-Commerce Distribution Channels

U.S. Census Bureau data shows that e-commerce penetration of health and personal care reached 22.4% in Q4 2024, up from 15.1% in 2020, reshaping how American women discover, evaluate, and purchase grooming products. Social-commerce gross merchandise value on TikTok Shop crossed US$ 9 billion in 2024 per company disclosures, with beauty as the leading category and women grooming products driving disproportionate engagement.

Reinforcing channel scale, Sephora's loyalty program crossed 34 million members in 2024, while Ulta Beauty, Inc. reported 44.6 million active loyalty members. These platforms enable faster product launches, micro-influencer-led conversion, AR try-on, and AI-personalized routines, positioning brands integrating first-party data, subscription replenishment, and live-shopping formats best to capture U.S. beauty market share.

Category-wise Insights

Product Type Analysis

Skincare leads the U.S. women grooming market with an estimated 35% value share in 2025, anchored by entrenched daily routines spanning cleansers, moisturizers, sunscreens, serums, and anti-aging formats. American Academy of Dermatology guidance recommending broad-spectrum SPF use has translated into rising sunscreen penetration, with U.S. Food and Drug Administration (FDA) monograph-compliant SKUs expanding sharply post-MoCRA, sustaining segment leadership.

Haircare is emerging as the fastest-growing product type, propelled by surging scalp-health awareness and a structural shift to bond-repair, sulfate-free, and texture-specific formulations. American Academy of Dermatology data highlights that nearly 50% of U.S. women experience hair-thinning concerns, while Olaplex Holdings, Inc. and L'Oréal USA, Inc. are scaling clinically validated launches across the U.S. haircare market, accelerating premiumization and innovation pipelines.

Category Analysis

The Premium category leads the U.S. women grooming market with an estimated 55% value share in 2025, reflecting entrenched consumer willingness to pay for clinically validated actives, luxury experience, and trusted heritage brands. U.S. Bureau of Economic Analysis data on personal consumption expenditure shows premium beauty outpacing mass beauty by nearly 300 basis points in annual growth since 2022, anchoring durable category leadership.

Premium is simultaneously the fastest-growing category, driven by accelerating consumer demand for ingredient transparency, sustainable packaging, and clinically substantiated efficacy claims. Retailers such as Sephora and Ulta Beauty, Inc. report prestige skincare and fragrance baskets carrying materially higher average ticket sizes versus mass equivalents. Affluent millennials and Gen-Z consumers, supported by social-commerce discovery and dermatologist endorsements, continue justifying steady price elevation.

Ingredient Type Analysis

Conventional formulations retain leadership with an estimated 68% value share of the U.S. women grooming market in 2025, reflecting decades of consumer trust, broad price accessibility, and entrenched mass-retail distribution. U.S. Food and Drug Administration (FDA) monograph-compliant actives such as benzoyl peroxide, salicylic acid, and avobenzone underpin top-selling skincare and haircare SKUs across pharmacy, grocery, and mass-merchant beauty aisles nationwide.

Natural & Organic is the fastest-growing ingredient category, supported by USDA organic-certified launches, NSF/ANSI 305 compliance, and consumer scrutiny of endocrine disruptors and synthetic preservatives. The Environmental Working Group Skin Deep database now lists over 88,000 assessed products, fueling clean-label switching. Momentum aligns with parallel acceleration in the U.S. natural cosmetics market, where plant-based actives and biome-friendly chemistry reshape reformulation roadmaps.

Distribution Channel Analysis

Specialty Stores lead the U.S. women grooming market with an estimated 32% value share in 2025, anchored by experiential retail, expert assistance, and curated assortments at chains such as Sephora, Ulta Beauty, Inc., and Bluemercury. Ulta Beauty, Inc. reported net sales of US$ 11.3 billion in fiscal 2024 across more than 1,400 stores, sustaining strong omnichannel preference among American women.

Online Retail is the fastest-growing distribution channel, propelled by accelerating digital adoption, subscription replenishment, and DTC brand proliferation across the U.S. women grooming landscape. U.S. Census Bureau retail e-commerce data shows health and personal care penetration exceeding 22% in Q4 2024, while Amazon.com, Inc. Premium Beauty store and TikTok Shop are unlocking discovery, AR try-on, and AI-personalized routine recommendations at unprecedented scale and speed.

Regional Insights

U.S. Women Grooming Market Size

The U.S. women grooming market remains the world's most lucrative single-country opportunity, anchored by approximately 170 million women across the country per U.S. Census Bureau estimates and per-capita beauty spending exceeding US$ 350 annually. The West region leads with an estimated 28% national share in 2025, supported by California's beauty innovation hubs and high disposable income.

- Southwest U.S. Women Grooming Market Trends and Insights

The Southwest is being shaped by rapid Hispanic population growth, climate-driven demand for sun protection, and expansion of beauty supply chains in Texas. U.S. Census Bureau projections show the Hispanic population exceeding 30% of the regional base. Trends include bilingual digital marketing, multicultural haircare growth, and Texas-based logistics investments by L'Oréal USA, Inc. and The Procter & Gamble Company.

- West U.S. Women Grooming Market Size

The West holds an estimated 28% share of the U.S. women grooming market in 2025, with California alone contributing the bulk of regional revenues. U.S. Census Bureau data places California's female population at over 19 million, while the state hosts headquarters of The Clorox Company, Olaplex Holdings, Inc., and indie clean-beauty leaders driving premiumization and clean-formulation leadership.

- Southeast U.S. Women Grooming Market Size

The Southeast contributes approximately 22% of U.S. women grooming revenues in 2025, supported by Florida and Georgia's expanding population base per U.S. Census Bureau counts of over 52 million women regionally. Humidity-driven haircare, fragrance, and sun-care demand, combined with Atlanta-based logistics hubs operated by The Home Depot, Inc. and The Coca-Cola Company networks, accelerate omnichannel grooming consumption.

Competitive Landscape

The U.S. women grooming market is moderately consolidated, with a handful of multinational personal care conglomerates anchoring the top tier while a rapidly expanding long tail of indie, dermatologist-founded, and DTC brands fuels category innovation. Established leaders compete on R&D scale, dermatologist partnerships, clinical efficacy substantiation, and global supply networks, leveraging deep distribution relationships across mass, premium, and specialty retail channels.

Strategic priorities include acquisitions of clean-beauty brands, investments in AI-driven personalization, sustainable and refillable packaging commitments, and the scaling of subscription replenishment models. Indie players differentiate through ingredient transparency, social-led storytelling, and category-specific authority spanning scalp health, microbiome care, and biome-balancing formulations.

Key Market Developments

- In March 2024, The Estée Lauder Companies Inc. announced a multi-year strategic restructuring plan, 'Profit Recovery and Growth Plan', focused on reinvigorating prestige beauty growth and rebalancing its U.S. portfolio across skincare and fragrance.

- In September 2024, L'Oréal USA, Inc. expanded its Cary, North Carolina manufacturing facility with a US$ 140 million investment to scale skincare and haircare production for the U.S. women grooming market.

- In January 2025, The Procter & Gamble Company launched a new clean haircare line under Pantene with sulfate-free, biome-friendly formulations, targeting the rapidly growing premium-mass segment of the U.S. women grooming market.

Companies Covered in U.S. Women Grooming Market

- The Procter & Gamble Company

- L'Oréal USA, Inc.

- The Estée Lauder Companies Inc.

- Unilever PLC

- Johnson & Johnson Services, Inc.

- Coty Inc.

- Shiseido Company, Limited

- Kao Corporation

- Beiersdorf AG

- Revlon, Inc.

- The Clorox Company (Burt's Bees)

- Olaplex Holdings, Inc.

- Edgewell Personal Care Company

- Church & Dwight Co., Inc.

- The Honest Company, Inc.

Frequently Asked Questions

The U.S. women grooming market is projected to be valued at US$ 118.5 billion in 2026 and is expected to reach US$ 174.7 billion by 2033, growing at a CAGR of 5.7%.

Rising women's workforce participation, higher disposable income, the clean-beauty movement, and dermatologist-led skincare adoption supported by the FDA's MoCRA regulation are the primary demand drivers.

The West region leads with an estimated 28% share in 2025, anchored by California's beauty innovation hubs, indie clean-beauty leaders, and high per-capita personal care spending.

The fastest-emerging opportunity lies in natural, organic, and microbiome-friendly formulations, supported by USDA organic certifications, NSF International standards, and rapid DTC and social-commerce growth.

Leading players include The Procter & Gamble Company, L'Oréal USA, Inc., The Estée Lauder Companies Inc., Unilever PLC, and Johnson & Johnson Services, Inc.