Industry: Chemicals and Materials

Published Date: December-2024

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 180

Report ID: PMRREP5201

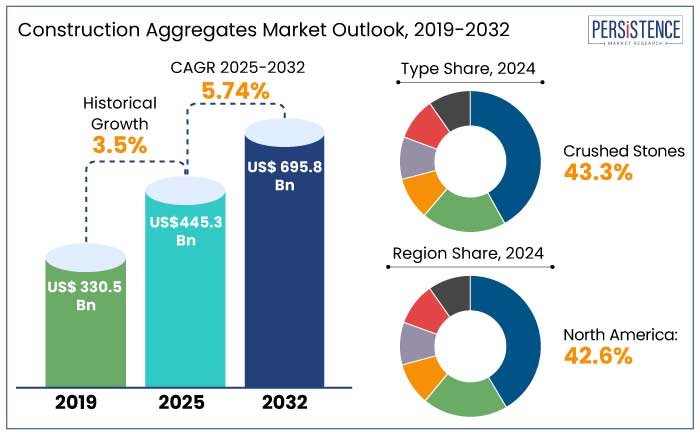

The global construction aggregates market is estimated to reach a size of US$ 445.3 Bn in 2025. It is predicted to rise at a CAGR of 5.7% through the assessment period to reach a value of US$ 695.8 Bn by 2032.

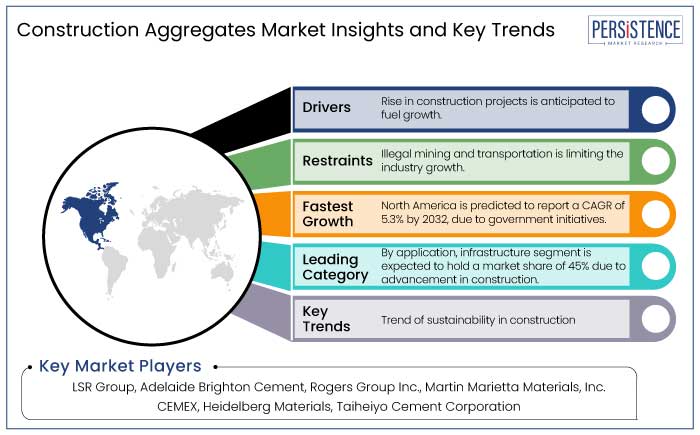

The fast expansion of residential projects, increased tourism, and improvements in building technology are contributing to the substantial construction component market growth. In 2024, the demand for construction aggregates like limestone and granite cultivated significantly due to their use in infrastructure projects like airports, roads, and urban developments. For instance,

Building Information Modelling (BIM) has greatly increased project efficiency and aided in market development by improving timeliness, cutting waste, and improving cost planning. The growth of infrastructure developments connected to tourism, such as hotels and recreation facilities, has led to a notable increase in overall utilization.

Problems like growing fuel prices, which affect production costs, might limit expansion. Government incentives and sustainable practices are anticipated to lessen these difficulties and maintain market momentum.

Key Highlights of the Market

|

Market Attributes |

Key Insights |

|

Construction Aggregates Market Size (2025E) |

US$ 445.3 Bn |

|

Projected Market Value (2032F) |

US$ 695.8 Bn |

|

Global Market Growth Rate (CAGR 2025 to 2032) |

5.7% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

3.5% |

North America holds a market share of 42.6% in 2024, with the US expected to experience significant growth due to government infrastructure investments. In July 2021, the U.S. Department of Transportation announced that it granted US$ 905.25 Mn to 24 projects under the Infrastructure for Rebuilding America program.

Post-pandemic recovery has accelerated, supported by advancements in construction technologies such as AI-based design. The regional market is projected to exhibit a CAGR of 5.3% from 2025 to 2032.

Asia Pacific accounts for a 23% share of the global construction aggregates market in 2024. This growth is driven by the ongoing urbanization of rural areas, particularly in emerging economies like India and China. As these regions rapidly transform into cosmopolitan urban centers, the demand for construction aggregates continues to rise.

China's "New Urbanization Plan" seeks to achieve over 65% urbanization, necessitating more infrastructure and building supplies by 2030. As urban development projects advance, aggregate demand is predicted to stay strong.

Crushed stones are expected to hold a 43.3% market share in 2024, solidifying their significance in a variety of sectors. Because of their strength and durability, these materials are frequently used in road building, coastal protection, and landscaping projects for their aesthetic appeal.

One of the most recent developments is their function in strengthening cement and concrete mixes, which is essential for infrastructure projects. Crushed stones have been highlighted as a key component in large-scale coastline protection projects started in 2023, especially in Asia, to prevent erosion. Their adaptability assures demand in a variety of industries, highlighting their status as a vital resource for environmental preservation and building.

The infrastructure segment is predicted to dominate the market, accounting for 45% in 2024 due to construction projects like metro stations, airports, and urban townships, providing opportunity for the market players. Rapid industrialization in emerging economies, including India, Brazil, and South Africa, is driving demand. For instance,

Companies like Vulcan Materials and Martin Marietta Materials continue to expand their offerings to meet rising global demand.

The global construction aggregates market is expanding because of industry developments, rising tourism, and fast residential development. The market further enhances structural strength and reduces cracks, while the tourism industry's growth is fueled by competitive investments in projects.

The most plentiful resource is construction aggregates, which are used for filtration, water purification, and preventing soil erosion as well as for highways, airports, runways, parking lots, and railroads. Also, the demand for construction aggregates is driven by the need for offices, homes, and shopping centers owing to rapid urbanization.

Government investments in transport and energy networks have boosted aggregate demand, but increased fuel prices could negatively impact aggregate production and industry growth.

The global construction aggregates market recorded a CAGR of 3.5% in the historical period from 2019 to 2023. The market for construction aggregates was impacted by supply chain disruptions in 2020, but the sector has recovered well because of significant government investment in residential and commercial infrastructure projects.

Major contributors include countries such as the U.S., France, and Malaysia, while companies like LafargeHolcim and CEMEX lead global production. The market is bolstered by growing infrastructure needs and sustainable practices. Demand for construction aggregates is estimated to record a considerable CAGR of 5.7% during the forecast period between 2024 and 2032.

Rising Government Initiatives to Support the Development in Emerging Countries

Developing countries like India, Brazil, and Mexico are experiencing significant economic growth by improving infrastructure and liberalizing regulations to attract new investments.

Developing nations have strengthened regional trade agreements in response to the global trend toward trade liberalization, which has created beneficial conditions for suppliers of construction aggregates, notwithstanding protectionist policies in the U.S. and Europe.

Trend of Sustainability in Construction Sector Promotes Innovation

There is a rising need for recycled and sustainable aggregates as the building industry adopted environmental rules and the circular economy, which lessens dependency on virgin resources. For instance, In October 2023, Heidelberg Materials introduced ReCirc, a brand of sustainable aggregate products that emphasizes recycled building waste.

European countries, particularly Germany and the U.K., have implemented policies incentivizing the use of recycled materials in public infrastructure. Global adoption is expected to grow, with sustainable aggregates projected to constitute 25% of all construction aggregates in 2025.

Illegal Transport and Mining Operations Curbs the Industry

Transportation expenses impact the construction aggregates market due to their weight and bulk, which lead to high logistical costs. Global reserves of essential materials like sand and gravel are rapidly depleting, creating supply chain pressures. Illegal mining is estimated to exacerbate such issues, particularly in countries like India, which faces stringent regulatory crackdowns to curb unregulated operations.

Introduction of Cutting-edge Materials and Methods in Construction Sector

In order to improve the longevity and functionality of structures, especially in high-performance and sustainable concrete applications, the construction industry is employing cutting-edge methods and materials, especially premium aggregates. For instance, in September 2023, LafargeHolcim unveiled their ECOPact line, which uses premium aggregates for enhanced durability and environmental performance.

Quality and long-term market efficiency are being prioritized by smart infrastructure projects in the U.S. and Japan, which are increasing demand for premium aggregates.

Adoption of Advanced Construction Techniques Presents Growth Avenues

Advanced construction techniques are driving a rise in demand for high-quality aggregates due to their enhanced durability and performance. Premium aggregates are necessary for long-lasting composites and high-strength concrete to improve structural integrity and infrastructure longevity. Long-lasting structures are the outcome of using these materials in commercial buildings, bridges, and roadways.

According to the World Economic Forum (2023), technological innovations like recycled aggregates are crucial for improving material efficiency and lowering environmental impact. It is important in complicated building projects, particularly in metropolitan areas and megaprojects.

The global construction aggregates market is dominated by leading players who are strategically building long-term supply chain relationships to improve product quality and service delivery. Partnering with vendors allows them to outsource noncritical activities, reducing internal workloads and boosting operational efficiency.

Manufacturers are prioritizing sustainability by investing in eco-friendly products like recycled aggregates and manufactured sand. This not only addresses environmental concerns but also allows them to enter emerging markets that prioritize green building materials. By innovating and adapting to market demands, manufacturers are positioning themselves for future growth and competitiveness.

Recent Industry Developments

|

Attributes |

Details |

|

Forecast Period |

2025 to 2032 |

|

Historical Data Available for |

2019 to 2023 |

|

Market Analysis |

US$ Billion for Value |

|

Key Regions Covered |

|

|

Key Market Segments Covered |

|

|

Key Companies Profiled in the Report |

|

|

Report Coverage |

|

|

Customization and Pricing |

Available upon request |

By Type

By Application

By Region

To know more about delivery timeline for this report Contact Sales

The market size is set to reach US$ 695.8 Bn by 2032.

Crushed stone is a popular and durable aggregate used in residential and commercial construction projects to provide a strong foundation for concrete slabs.

North America is projected to attain a market share of 42.6% in 2024.

The market is estimated to showcase a CAGR of 5.7% through 2032.

Some of the leading key players in the market are LSR Group, Adelaide Brighton Cement, Rogers Group Inc., and Martin Marietta Materials, Inc.