- Beauty & Personal Care

- Hair Care Market

Hair Care Market Size, Share and Growth Forecast, 2026 - 2033

Hair Care Market by Product Type (Cleansing, Conditioning, Scalp care, Hair growth, Repair, Styling, Hair Color), End User (Women, Men, Children, Professional users), Ingredient Type (Natural, Clinical actives, Protein, Synthetic functional ingredients), and Regional Analysis for 2026 - 2033

Hair Care Market Share and Trends Analysis

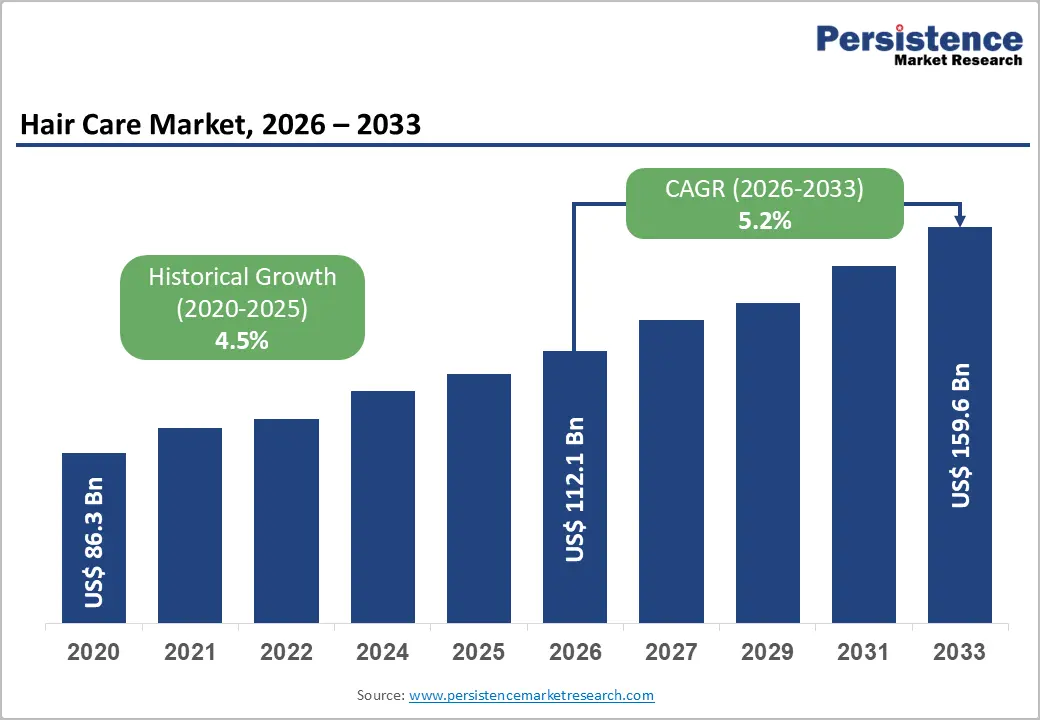

The global hair care market size is likely to be valued at US$ 112.1 billion in 2026 and is projected to reach US$ 159.6 billion by 2033, growing at a CAGR of 5.2% during the forecast period of 2026-2033.

The market demonstrates steady and sustained expansion driven by increasing consumer awareness regarding scalp health, rising demand for natural, clean-label, and clinically effective formulations, and growing personal grooming expenditure across both developed and emerging economies. Consumers are progressively shifting from basic cleansing products toward multi-functional hair care solutions, including repair, scalp nourishment, anti-hair fall, and hair growth treatments, which are significantly enhancing product value per unit.

Key Industry Highlights

- Dominant Product Segments: Cleansing products are expected to lead with 35% share in 2026, while scalp care and hair growth products are likely to grow fastest, driven by rising scalp health concerns and preventive hair treatment demand.

- Leading End-User Segments: Women are projected to dominate with 60% share in 2026, while the men’s segment is the fastest growing, supported by increasing grooming awareness and anti-hair fall product adoption.

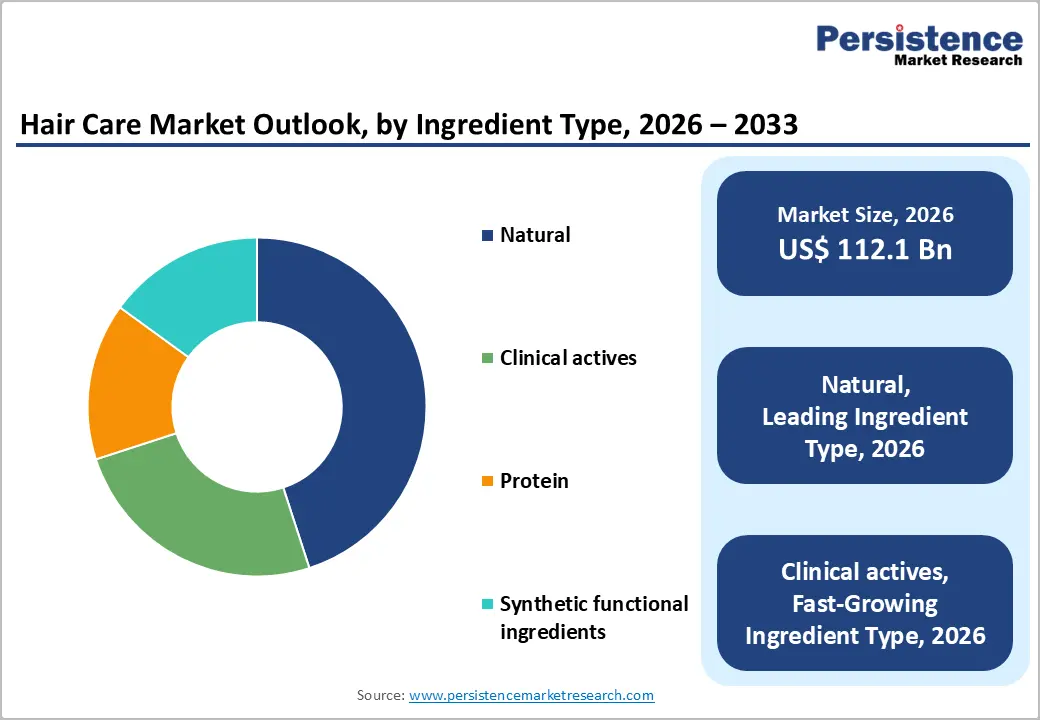

- Ingredient Innovation Landscape: Natural ingredients are expected to drive innovation with over 45% combined share in 2026, while clinical actives are the fastest-growing category due to demand for clean-label and dermatology-backed solutions.

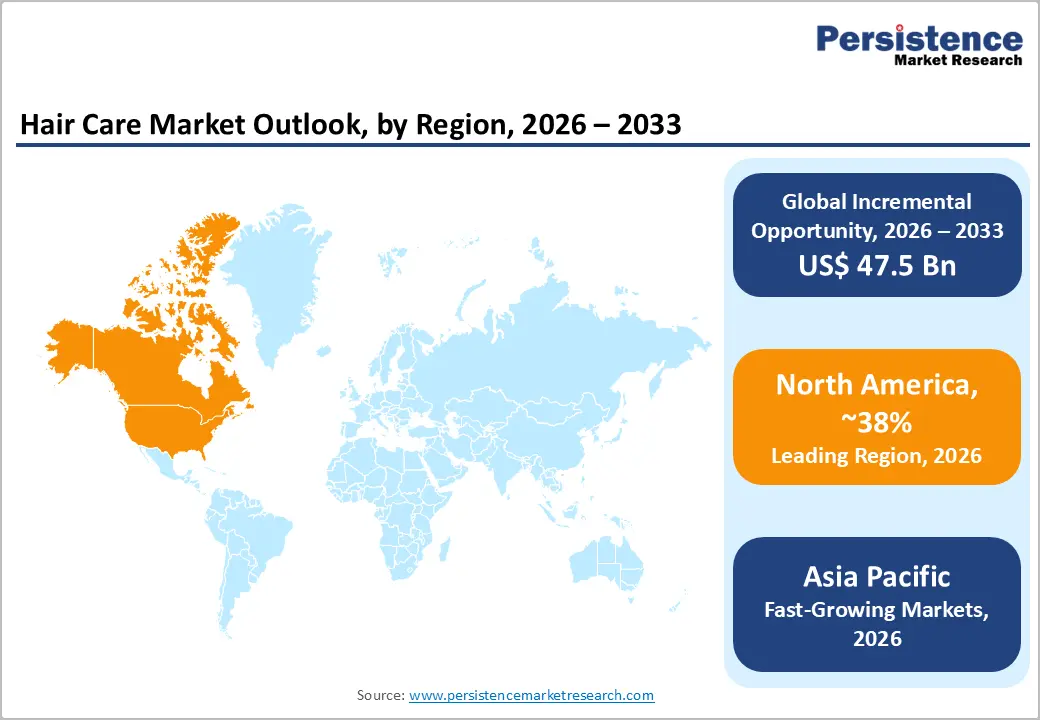

- Regional Leadership: North America currently holds the largest market share of about 38% in 2026, driven by high disposable incomes, premiumization, and strong established brands, while Asia Pacific is the fastest-growing region, led by rising demand in India and China for premium, anti-hair fall, and natural hair care products.

- Competitive Environment: Market competition is shaped by AI-driven personalization, sustainable packaging, and dermatology-backed formulations, with strong expansion into high-growth emerging markets and D2C channels.

| Key Insights | Details |

|---|---|

|

Hair Care Market Size (2026E) |

US$ 112.1 Bn |

|

Market Value Forecast (2033F) |

US$ 159.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.5% |

DRO Analysis

Driver - Rising Consumer Focus on Scalp Health and Preventive Hair Care

The shift from cosmetic-only hair care to scalp-centric preventive care is a major growth driver. According to dermatology and cosmetic science associations, nearly 40–50% of adults globally experience scalp-related issues such as dandruff, dryness, or hair thinning, increasing demand for specialized scalp care formulations. Rising urban pollution levels and environmental stressors have further intensified scalp damage concerns. This is driving adoption of medicated shampoos, exfoliating scalp scrubs, and microbiome-balancing products across global markets. Manufacturers are increasingly integrating actives such as salicylic acid, niacinamide, and probiotic-based ingredients. As a result, scalp care is shifting from a niche dermatology category to a mainstream preventive care segment.

This trend is further supported by regulatory tightening in major global markets, especially around cosmetic safety and ingredient transparency. Updated European regulatory frameworks have strengthened restrictions on sensitizing and high-risk chemical substances used in personal care formulations. At the same time, environmental policies targeting microplastics in rinse-off products like shampoos are pushing brands toward biodegradable alternatives. These changes are forcing large manufacturers to reformulate scalp care portfolios to meet compliance standards. The impact is visible in faster adoption of dermatology-backed scalp solutions and clinically tested formulations. This regulatory push is reinforcing preventive scalp care as a core growth pillar of the hair care market.

Growing Demand for Natural and Clean-Label Ingredients

Global consumers are increasingly shifting toward natural, organic, and chemical-free formulations due to rising concerns over synthetic additives and long-term scalp sensitivity. This demand is strongly supported by increasing regulatory emphasis on ingredient transparency and product safety across major markets. Authorities in developed regions are expanding safety evaluations for preservatives, allergens, and chemical compounds used in cosmetics. This is encouraging brands to adopt clearer labeling practices and safer formulation standards. Consumers are also actively preferring sulfate-free, paraben-free, and silicone-free products. As a result, natural and clean-label positioning has become a key competitive requirement in the hair care industry.

The regulatory developments over the years are accelerating this transition at a global level. Strengthened cosmetic compliance frameworks are pushing manufacturers to reformulate products using safer botanical and bio-based ingredients. Restrictions and tighter scrutiny on certain synthetic compounds are further encouraging innovation in plant-derived surfactants and essential oil-based formulations. Leading brands have already begun large-scale reformulation of shampoos and conditioners to align with these standards. This shift is also improving brand trust and strengthening long-term consumer loyalty. Consequently, clean-label and natural formulations are becoming a structural growth driver across both premium and mass-market hair care segments.

Restraints - High Product Premiumization and Affordability Constraints

One of the key restraints is the increasing premiumization of hair care products, which limits adoption in price-sensitive markets. Advanced formulations involving clinical actives, peptides, and organic certifications significantly increase production costs. In developing economies, where per capita spending on personal care remains relatively low, premium products face affordability challenges. For instance, rural penetration in several South Asian and African markets remains limited due to pricing gaps of 2–3x between mass-market and premium products. This restricts volume growth and creates a segmentation imbalance between urban and rural markets. This affordability challenge is further reinforced by real-world cost pressures observed in 2025 across the FMCG sector, particularly from ingredient inflation in categories such as sodium lauryl sulfate alternatives, argan oil, and shea butter used in premium formulations.

Companies such as Unilever and Procter & Gamble reported cost headwinds in their 2025 earnings communications, citing higher raw material and packaging expenses impacting personal care margins. At the same time, retailers such as Walmart and Carrefour noted a visible shift in consumer purchasing patterns toward private-label shampoos and conditioners due to household budget constraints. This trading-down behavior is slowing the adoption of salon-grade and treatment-based hair care products, directly limiting premium market expansion.

Regulatory Complexity and Ingredient Compliance Barriers

Hair care manufacturers face growing regulatory scrutiny regarding chemical safety, labeling, and environmental compliance. The European Union’s stringent cosmetic ingredient regulations and increasing restrictions on sulfates, parabens, and silicones require continuous reformulation. Compliance with evolving frameworks such as REACH adds operational burden. In 2025, several brands faced delays in product approvals due to updated allergen disclosure requirements in Europe and North America. This increases time-to-market and raises R&D expenditure, particularly for small and mid-sized companies lacking regulatory infrastructure.

This challenge is further intensified by specific regulatory actions implemented in 2025–2026, including the European Union’s REACH restriction on intentionally added microplastics in rinse-off cosmetic products such as shampoos and scrubs, which is forcing large-scale reformulation across brands such as L’Oréal and Henkel.

In addition, the United States Food and Drug Administration’s enforcement of MoCRA (Modernization of Cosmetics Regulation Act of 2022) during 2025 has introduced mandatory product listing, facility registration, and adverse event reporting requirements for companies such as Procter & Gamble and Estée Lauder Companies. These regulations are increasing compliance complexity, delaying product approvals, and raising operational costs, particularly for companies managing large, multi-brand hair care portfolios across regions.

Opportunities - Expansion of Clinical and Dermatology-Based Hair Care

A major opportunity lies in the rapid expansion of dermatology-backed hair care solutions, particularly for hair loss and scalp disorders. The global hair loss treatment segment is witnessing strong demand due to the increasing prevalence of alopecia and stress-induced hair thinning. According to clinical dermatology associations, nearly 1 in 3 adults experiences noticeable hair thinning by age 35. This is creating opportunities for clinically tested formulations, including minoxidil-based over-the-counter products and peptide-infused serums. Pharmaceutical-cosmetic convergence (“cosmeceuticals”) is expected to contribute significantly to incremental market value, particularly in North America and Europe.

This opportunity is further reinforced by real-world clinical product expansion in 2025 within regulated pharmacy channels, where dermatology-led hair treatments are increasingly being positioned as first-line consumer solutions for early-stage hair thinning. A key example is the wider retail availability of OTC minoxidil formulations in pharmacy chains such as Walgreens and Boots, improving accessibility of clinically validated hair regrowth solutions.

In parallel, Kenvue (formerly Johnson & Johnson Consumer Health) has expanded dermatology-focused scalp care lines in 2025, integrating clinically tested ingredients such as peptides and scalp-soothing actives into everyday hair care routines. These developments are strengthening consumer trust in science-backed solutions and accelerating the shift from cosmetic care to treatment-oriented hair care globally.

Growth of Personalized and AI-Driven Hair Care Solutions

Personalization is emerging as a transformative opportunity, with brands increasingly leveraging AI-based scalp diagnostics and customized formulations. In 2025, several global brands introduced mobile app-based hair analysis tools that recommend ingredient-specific regimens. This trend aligns with rising consumer demand for individualized solutions. The personalized hair care market is expected to account for a growing share of premium product sales, particularly among Gen Z consumers. The opportunity lies in subscription-based models, direct-to-consumer customization, and data-driven product recommendations.

This trend is strongly supported by real-world digital beauty technology deployments in 2025, where companies are integrating AI-driven imaging and scalp assessment tools into consumer ecosystems. A notable example is the launch of Dyson’s AI-enabled hair analysis feature within its connected beauty devices ecosystem, which assesses hair health parameters and recommends tailored styling and care routines. Additionally, Shiseido has expanded its digital beauty diagnostic tools in Asian and global markets, using AI-based scalp imaging to guide personalized product selection and skincare-like hair regimens. These innovations are enabling a shift from mass-market hair care to precision-based solutions, increasing consumer engagement and supporting long-term subscription-driven business models.

Category-wise Analysis

Product Type Insights

Cleansing products dominate the product type segment, projected to capture about 35% of the market share in 2026. Cleansing products such as shampoos serve as the core entry point in daily hair care routines and maintain universal adoption across all age and income groups. Modern formulations now extend beyond basic cleansing to include anti-dandruff, hydration, and scalp-friendly systems, increasing their functional value. The segment benefits from high purchase frequency and strong retail penetration across both offline and online channels. In 2025–2026, brands such as CLEAR (Unilever) expanded scalp-focused shampoo ranges in Asia, strengthening functional cleansing demand. Despite rising competition from treatment categories, cleansing remains structurally resilient due to its essential usage nature.

Scalp care products are expected to represent the fastest-growing product type segment, driven by increasing concerns around hair thinning, stress-related hair loss, and pollution-induced scalp damage. This segment includes serums, exfoliating scalp treatments, and targeted growth solutions incorporating actives such as niacinamide and peptide complexes. Growth is supported by rising consumer willingness to adopt preventive and dermatology-inspired routines. In 2025, brands such as Rene Furterer expanded scalp stimulation treatment lines in Europe, focusing on plant-based dermo-cosmetic solutions. Additionally, salon-to-home treatment migration is accelerating demand for high-performance scalp therapies, making this segment a key driver of premiumization and product innovation.

Ingredient Type Insights

Synthetic functional ingredients seem to dominate the ingredient type segment, accounting for about 45% of total market share in 2026. These ingredients are widely used in mass-market shampoos and conditioners due to their cost efficiency, stability, and scalability in large-volume production. They provide consistent cleansing, foaming, and conditioning performance, making them essential for affordable hair care offerings. In 2025–2026, large-scale retailers such as Tesco expanded private-label hair care ranges using optimized synthetic surfactant systems to maintain affordability amid inflation pressures. The segment remains critical for global accessibility, especially in price-sensitive markets where cost control is a primary purchasing factor.

Natural ingredients are anticipated to be the fastest-growing segment, driven by rising demand for clean-label, safe, and dermatologically validated formulations. This includes botanical extracts, essential oils, and scientifically tested actives used in scalp repair and hair strengthening products. The segment is witnessing strong adoption in premium and mid-premium categories, supported by increasing consumer awareness of ingredient safety. In 2025, Weleda expanded its plant-based hair care portfolio across European markets, emphasizing biodynamic botanical formulations. Additionally, Natura &Co enhanced its Amazonian bioactive ingredient sourcing strategy to strengthen sustainable hair care offerings. This shift is accelerating hybrid formulations that combine natural origin ingredients with clinically proven performance benefits.

Regional Analysis

North America Hair Care Market Trends

North America is expected to hold currently holds the largest share of the global hair care market, accounting for approximately 38% in 2026, driven by high disposable incomes, strong premiumization trends, and the presence of well-established global brands. The region shows strong demand for premium scalp care, anti-hair loss treatments, and clean-label formulations, supported by highly developed retail and e-commerce ecosystems. The United States remains the core contributor, with consumers increasingly prioritizing performance-based and clinically tested hair care solutions.

This leadership is further strengthened by regulatory and retail developments that reinforce product safety and premium positioning. The U.S. Food and Drug Administration’s continued enforcement of MoCRA compliance requirements in 2025 has increased transparency and safety standards for cosmetic manufacturers, strengthening consumer trust in regulated products. In addition, CVS Health expanded its dermatology-focused hair care assortments in 2025, increasing the availability of scalp health and OTC hair treatment solutions across pharmacy channels. Furthermore, Amazon Beauty’s enhancement of AI-driven hair diagnostic tools in 2025 has accelerated personalized product recommendations and strengthened digital adoption. These developments collectively reinforce the region’s leadership in innovation-led and science-backed hair care consumption.

Europe Hair Care Market Trends

Europe holds a significant share of the global hair care market, with strong performance from Germany, the U.K., France, and Spain. The region is characterized by mature consumer markets with high demand for organic, sustainable, and dermatologically tested hair care products, supported by strong environmental and ethical consumption trends. Consumers increasingly prefer vegan, eco-certified, and refillable product formats, making sustainability a core purchasing driver across the region.

This market structure is shaped by regulatory tightening and sustainability-led retail transformation across the European Union, which is reinforcing Europe’s leadership in clean-label beauty. The EU’s continued enforcement of REACH restrictions on rinse-off cosmetic formulations is accelerating the phase-out of non-biodegradable and certain synthetic ingredients, driving reformulation across shampoo and conditioner categories. In addition, Germany’s leading retail chains expanded refillable personal care stations in 2025, reflecting rising consumer demand for low-waste beauty solutions. Furthermore, France’s national health regulatory authority (ANSM) strengthened cosmetic safety monitoring in 2025, increasing oversight of ingredient compliance and product safety standards. These developments are reinforcing Europe’s position as a global hub for sustainable and regulation-driven hair care innovation.

Asia Pacific Hair Care Market Trends

Asia Pacific is projected to be the fastest-growing regional market, led by China, India, Japan, and ASEAN countries. The region is experiencing strong growth driven by rapid urbanization, rising disposable incomes, and increasing consumer focus on scalp health, anti-hair fall solutions, and natural hair care products. While mass-market demand remains strong, premium and treatment-based segments are expanding rapidly, particularly in urban populations. Japan leads in advanced formulation innovation, while China and Southeast Asia drive large-scale consumption and digital retail growth.

This expansion is strongly supported by digital commerce and policy-driven industry developments across the region, which are accelerating both accessibility and premiumization. The Chinese government’s continued expansion of cross-border e-commerce pilot zones in 2025 has strengthened international brand penetration through platforms such as Tmall Global, boosting premium hair care imports. In Southeast Asia, Shopee and Lazada expanded livestream beauty commerce formats in 2025, significantly improving product discovery and conversion rates among younger consumers.

Additionally, Japan’s Ministry of Economy, Trade and Industry (METI) advanced cosmetic innovation initiatives in 2025 focused on scalp microbiome research and bioactive formulation development, reinforcing the country’s leadership in high-end hair care innovation. These developments collectively position Asia Pacific as the most dynamic and fastest-expanding regional market globally.

Competitive Landscape

The global hair care market is moderately consolidated, with leading players such as L’Oréal, Procter & Gamble, Unilever, and Estée Lauder Companies holding strong positions across mass and premium segments. Their dominance is supported by extensive distribution networks, strong brand equity, and continuous investment in product innovation across scalp care, repair, and styling categories. These companies also leverage large-scale marketing capabilities and retailer partnerships to maintain shelf dominance. Innovation remains centered on premiumization and science-backed formulations.

Competitive strategies are increasingly focused on dermatology-led products, sustainability, and digital-first engagement models. In 2025, Unilever expanded its scalp-focused hair care lines across multiple regions, while Procter & Gamble strengthened its bond-repair and salon-grade treatment portfolio in premium channels. The players, such as Kao Corporation and Amorepacific, are expanding in Asia through botanical and scalp microbiome-focused formulations, targeting regional preferences. The market is becoming more dynamic due to e-commerce growth and the rising influence of indie and digital-first brands.

Key Developments:

- In January 2026, Henkel acquired Olaplex for approximately US$ 1.4 billion to strengthen its premium bond-repair and science-led hair care portfolio. The deal enhances Henkel’s position in high-growth treatment and repair-focused hair care segments, expanding its premium salon-grade capabilities globally.

- In June 2025, L’Oréal acquired Color Wow to reinforce its professional hair care division and expand high-performance styling capabilities. This acquisition strengthens L’Oréal’s presence in salon-grade frizz control and premium styling solutions across global markets.

- In March 2025, e.l.f. Beauty acquired Rhode in March 2025 for approximately US$ 1 billion to expand its direct-to-consumer beauty ecosystem and strengthen digital-first brand engagement. The acquisition accelerates growth in youth-driven beauty platforms and enhances reach across beauty and hair-care-adjacent categories.

Companies Covered in Hair Care Market

- L’Oréal S.A.

- Procter & Gamble Co.

- Unilever PLC

- Estée Lauder Companies

- Henkel AG & Co. KGaA

- Shiseido Company Ltd.

- Kao Corporation

- Amorepacific Corporation

- Johnson & Johnson

- Dabur India Ltd. Marico Ltd.

- Coty Inc.

- Revlon Inc.

- Natura & Co

- Beiersdorf AG

Frequently Asked Questions

The global hair care market is projected to reach approximately US$ 112.1 billion in 2026.

Rising consumer focus on scalp health, premiumization, and demand for natural and clinically effective formulations are driving the market.

The market is expected to grow at a moderate, steady growth rate through 2033, driven by treatment-based and premium product adoption.

Expansion of scalp care, clinical hair treatments, and personalized AI-driven hair care solutions are key opportunities.

Major players include L’Oréal, Unilever, Procter & Gamble, Estée Lauder Companies, and Kao Corporation.