- Home Appliances

- U.S. Bedroom Furniture Market

U.S. Bedroom Furniture Market Size, Share, and Growth Forecast 2026 - 2033

U.S. Bedroom Furniture Market by Product Type (Beds & Mattresses, Wardrobe and Storage, Dressers, Nightstands, Headboards, Others), Price Range (Less than US$ 500, US$ 500 to US$ 999, Above US$ 1,000), Distribution Channel (Offline, Online), and Regional Analysis for 2026 - 2033

U.S. Bedroom Furniture Market Size and Trend Analysis

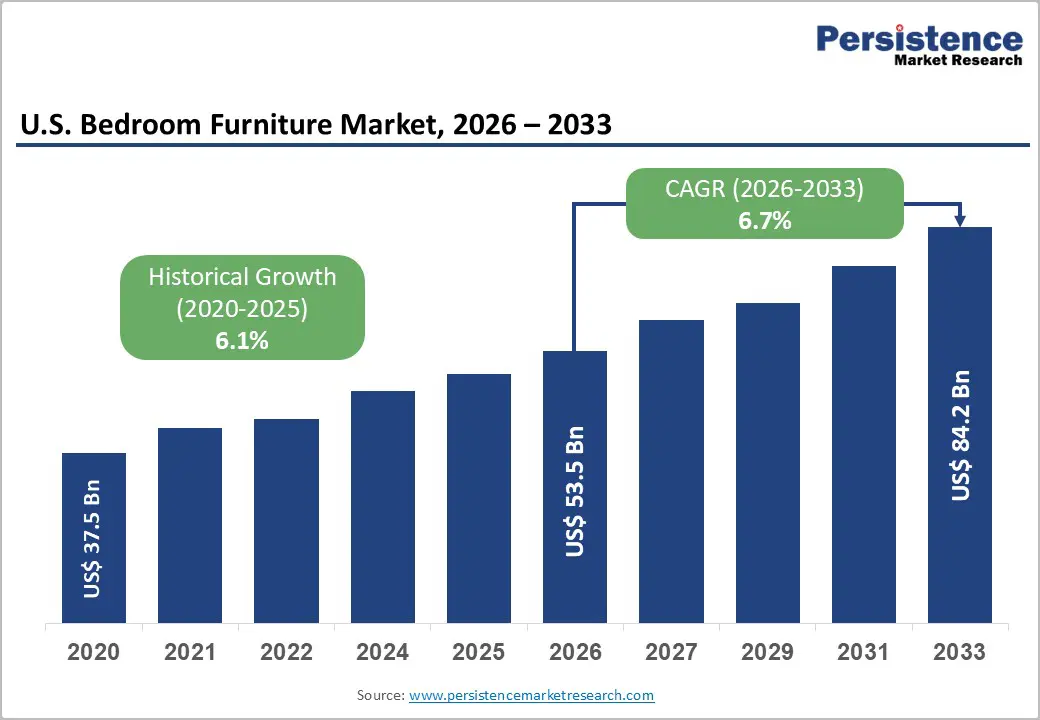

The U.S. bedroom furniture market size is valued at US$ 53.5 Bn in 2026 and is projected to reach US$ 84.2 Bn by 2033, growing at a CAGR of 6.7% between 2026 and 2033.

Growth is primarily driven by sustained housing construction activity, rising household incomes, and a pronounced consumer shift toward premium and smart bedroom furniture solutions. According to the U.S. Census Bureau, approximately 1.42 million housing units were started in 2024, reinforcing furniture demand across all price tiers. The growing influence of millennials as homebuyers, coupled with increasing home renovation expenditure and the rapid adoption of e-commerce platforms with augmented reality features, continues to expand the addressable market. Historically, the market grew at a CAGR of 6.1% between 2020 and 2025, reflecting sustained consumer confidence and structural demand fundamentals.

Key Market Highlights

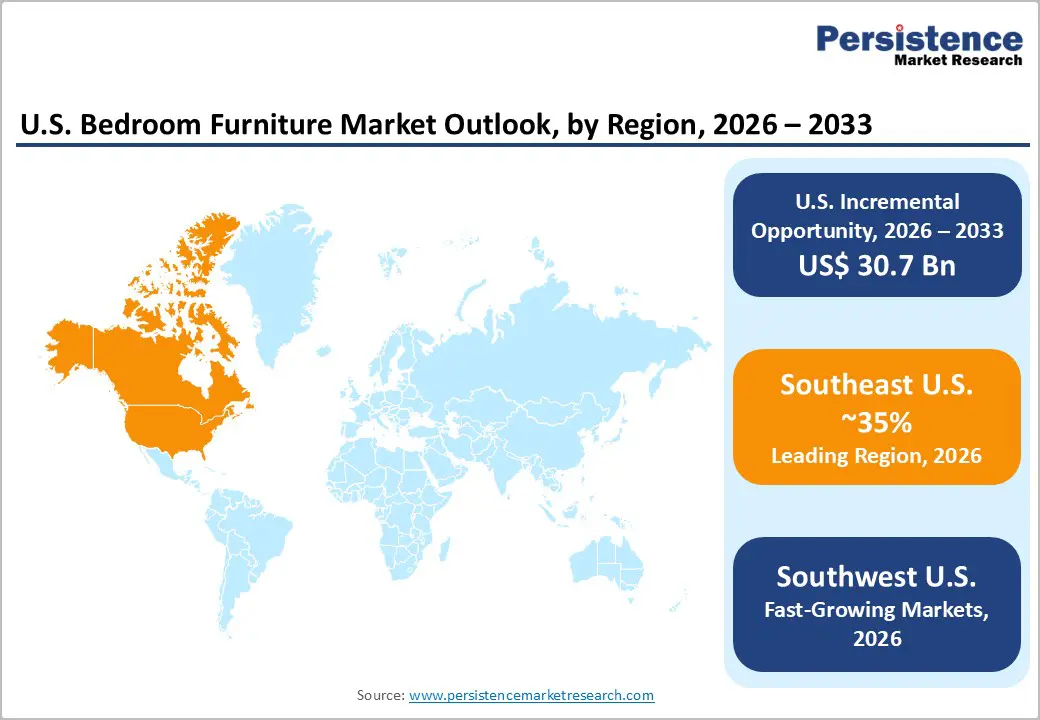

- Regional Leader: The Southeast U.S. is the dominant regional market, accounting for approximately 35% of national new single-family housing starts; robust population in-migration to Texas, Florida, and Georgia sustains consistently strong bedroom furniture demand.

- Fastest Growing Region: The Southwest U.S. is the fastest-growing region, with cities such as Phoenix, Las Vegas, and Austin growing at over 2-3% annually per U.S. Census Bureau data, driving elevated mid-range and premium bedroom furniture demand through 2033.

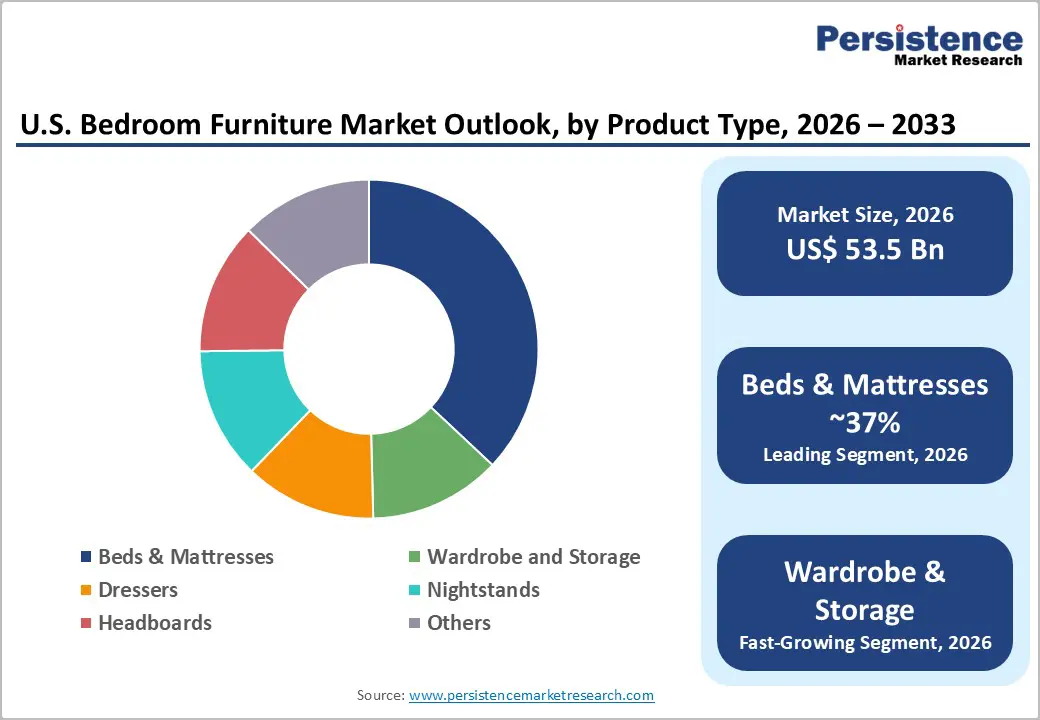

- Leading Segment: Beds & Mattresses is the dominant product segment with approximately 37% market share, underpinned by the National Sleep Foundation's recommended 7-10 year mattress replacement cycle and rising consumer investment in sleep wellness technology.

- Fastest Growing Segment: The online distribution channel is the fastest-growing segment with a projected CAGR of over 6.4%, driven by Wayfair LLC's digital marketplace, IKEA's AR-powered planning tools, and accelerating consumer adoption of immersive e-commerce experiences.

- Key Opportunity: Key market opportunities lie in AR/AI-powered e-commerce platforms and growing demand for FSC-certified, low-VOC bedroom furniture, as sustainability increasingly shapes purchase decisions among millennial and Gen Z consumers in the US$ 500-999 price tier.

| Key Insights | Details |

|---|---|

| U.S. Bedroom Furniture Market Size (2026E) | US$ 53.5 Bn |

| Market Value Forecast (2033F) | US$ 84.2 Bn |

| Projected Growth CAGR (2026 - 2033) | 6.7% |

| Historical Market Growth (2020 - 2025) | 6.1% |

Market Dynamics

Market Growth Drivers

Rising Housing Activity and Home Renovation Expenditure

The U.S. residential construction sector continues to serve as a fundamental driver of demand within the bedroom furniture industry. In 2024, more than 1.4 million housing starts were recorded, with single-family units comprising nearly 70% of total completions. Newly purchased homes typically generate substantial furnishing needs, as homebuyers are estimated to spend between US$ 5,000 and US$ 10,000 on furniture within the first year.

Annual home improvement expenditures exceed US$ 450 billion, a considerable portion of which is directed toward bedroom upgrades. Moreover, the emergence of approximately 73 million millennials entering prime homebuying years is expected to reinforce this momentum through 2033. Collectively, these demographic and macroeconomic factors underpin a durable and consistently expanding demand environment.

Premiumization and Growing Demand for Smart and Tech-Integrated Bedroom Furniture

Consumer preferences in the U.S. are rapidly evolving from purely functional furniture toward premium, technologically integrated bedroom products. The Consumer Electronics Show (CES) 2024 highlighted smart bedroom solutions, including beds with integrated sleep monitoring, adjustable firmness, and ambient lighting systems, as a significant emerging product category. Sleep Number Corporation, a publicly listed smart bed manufacturer, reported net revenue of approximately US$ 1.8 billion in its FY2023 Annual Report, underscoring the robust commercial viability of tech-enabled bedroom furniture.

The U.S. Bureau of Labor Statistics (BLS) Consumer Expenditure Survey further indicates that household spending on furniture and bedding rises proportionately with disposable income, which expanded by 4.2% in 2024 according to the Bureau of Economic Analysis (BEA). This confluence of improving affordability and aspirational consumption is reinforcing the premiumization trend across beds, mattresses, and premium storage systems, significantly elevating average selling prices and overall market revenues.

Market Restraints

Volatility in Raw Material Costs and Supply Chain Disruptions

Wood and engineered wood products are the primary raw materials used in bedroom furniture manufacturing, accounting for approximately 60-65% of total production costs. The U.S. Bureau of Labor Statistics' Producer Price Index (PPI) for lumber and wood products demonstrated price volatility of more than 40% between 2022 and 2024, directly compressing manufacturer margins. Upholstery materials, metal hardware, and foam components have seen additional cost escalations driven by energy price inflation and logistics bottlenecks.

The National Retail Federation (NRF) reported that supply chain disruptions continued to affect furniture on-time delivery rates in 2023-2024, leading to elevated order cancellations. Such cost unpredictability disproportionately impacts small-to-mid-size furniture manufacturers, constraining their capacity to compete at scale.

Impact of Import Tariffs and Trade Policy Uncertainty on the Furniture Sector

Approximately 50% of furniture sold in the U.S. is imported, according to the American Home Furnishings Alliance (AHFA), with China historically accounting for the largest share. The continuation of Section 301 tariffs, imposing 25% levies on furniture imported from China, has significantly elevated landed costs for retailers and importers.

In 2025, the U.S. Trade Representative (USTR) announced expanded trade measures affecting furniture components and finished goods from multiple sourcing nations. These policy changes have forced manufacturers to restructure supply chains, including near-shoring to Vietnam, Mexico, and Eastern Europe, adding cost and operational complexity that weighs on margins and retail pricing competitiveness across the mid-range segment.

Market Opportunities

Accelerating E-Commerce Adoption and Augmented Reality-Powered Shopping Experiences

The digitization of the U.S. furniture retail landscape presents a significant and sustained growth opportunity for market participants. According to the U.S. Census Bureau's Quarterly Retail E-Commerce Sales data, e-commerce as a share of total U.S. retail sales has grown consistently, with furniture and home furnishings among the fastest-adopting categories. Wayfair LLC reported 21 million active customers and US$ 10.5 billion in U.S. net revenue in 2024, validating the commercial scale of online furniture retail.

Particularly transformative is the integration of Augmented Reality (AR) tools, such as IKEA's AI-powered room planning application and Wayfair's 'View in Room' feature, which allow consumers to virtually place furniture in their living spaces, significantly reducing return rates and increasing purchase confidence. Brands investing in immersive digital shopping experiences are expected to capture disproportionate online market share through 2033, making digital infrastructure investment a key strategic imperative.

Growing Consumer Preference for Sustainable and Eco-Certified Bedroom Furniture

Heightened environmental awareness among U.S. consumers is creating a compelling opportunity for furniture manufacturers to differentiate through sustainability credentials. The Forest Stewardship Council (FSC) reports that certified wood products are experiencing growing demand in North American retail channels, with FSC-certified furniture generating higher consumer preference scores, particularly among millennials and Gen Z buyers.

Inter IKEA Systems B.V. confirmed in its FY2024 Sustainability Report that 97% of the wood used in its products is either FSC-certified or sourced from recycled materials. The U.S. Environmental Protection Agency (EPA) increasingly promotes low-VOC (volatile organic compound) material standards, creating regulatory tailwinds for eco-friendly manufacturers. Companies that align product portfolios with sustainability benchmarks and third-party certification programs are well-positioned to tap into this rapidly growing, premium-priced consumer cohort through the forecast period.

Category-wise Insights

Product Type Analysis

The Beds & Mattresses segment is the dominant product category within the U.S. Bedroom Furniture market, accounting for an estimated 37% revenue share. This leadership is primarily attributed to the non-discretionary replacement cycle of mattresses. The National Sleep Foundation recommends mattress replacement every 7 to 10 years, ensuring consistent baseline demand irrespective of macroeconomic conditions. The American Academy of Sleep Medicine (AASM) notes that sleep disorders affect over 70 million Americans, driving demand for ergonomically designed beds and high-performance mattresses.

The segment has further benefited from the rapid growth of the direct-to-consumer (DTC) mattress-in-a-box industry, with brands such as Nectar and DreamCloud expanding access to the premium mattress segment. Smart bed adoption featuring adjustable firmness, sleep tracking, and temperature regulation further elevates average selling prices, reinforcing the category's sustained revenue dominance.

Price Range Analysis

The US$ 500 to US$ 999 price bracket is the leading segment within the price range category, commanding approximately 48% of total market revenue. This tier aligns with the median consumer budget for bedroom furniture purchases, reflecting an optimal balance between quality expectations and affordability constraints. The U.S. Bureau of Labor Statistics (BLS) Consumer Expenditure Survey indicates that the average American household spends approximately US$ 600-US$ 700 annually on furniture, with bedroom furnishings constituting the largest share.

Products in this segment, including platform beds, mid-range dressers, and storage wardrobes from brands such as Ashley Furniture Industries, LLC, Rooms to Go, and Wayfair LLC, offer durable construction and contemporary styling at accessible price points. The widespread availability of Buy Now, Pay Later (BNPL) financing solutions through retailers further reduces the upfront purchase barrier and stimulates conversion rates across mid-tier channels, helping maintain this segment's market leadership.

Distribution Channel Analysis

Offline channels remain the dominant distribution mode in the U.S. Bedroom Furniture market, accounting for approximately 75% of total revenues. The primacy of in-store retail is fundamentally driven by the tactile and sensory nature of furniture purchasing. Consumers prefer to physically test mattress firmness, evaluate material quality, assess dimensional fit, and visualize color coordination before committing to a purchase. Specialty furniture retailers, including Ashley Furniture Industries, LLC, with over 1,100 stores globally, La-Z-Boy Inc., and Ethan Allen Interiors Inc., operate extensive national and regional showroom networks that provide curated in-person experiences.

The Furniture, Home Furnishings, and Equipment Stores sub-sector, tracked by the U.S. Census Bureau, consistently reports higher average transaction values in physical retail compared to online channels, underscoring the role of in-store consultation and trial in driving premium purchases. Despite strong online channel growth, offline retail's dominance is expected to persist through the forecast period, supported by ongoing investments in experiential retail formats.

Regional Insights

Southeast U.S. Bedroom Furniture Market Trends

The Southeast United States remains the leading regional market for bedroom furniture, supported by the nation’s highest levels of new residential construction. The region accounts for approximately 35% of all new single-family housing starts, driven by strong population in-migration to states such as Texas, Florida, Georgia, and North Carolina. This demographic expansion, coupled with consistently high home sales in metropolitan areas like Dallas-Fort Worth, Houston, Atlanta, and Orlando, sustains a steady base of first-time and move-up buyers requiring comprehensive bedroom furnishings.

The South also benefits from a robust manufacturing presence, including major production facilities operated by Ashley Furniture and Williams-Sonoma, Inc., which offers partial insulation from tariff-related volatility. Strong consumer spending power, lower living costs, and expanding suburban development collectively reinforce the region’s long-term market leadership through 2033.

Southwest U.S. Bedroom Furniture Market Trends

The Southwestern United States represents the fastest-growing regional market for bedroom furniture, supported by strong population expansion, vigorous housing development, and rising household incomes across major metropolitan areas. Cities such as Phoenix, Las Vegas, and Austin rank among the nation’s fastest-growing urban centers, with annual population increases exceeding the national average, thereby driving sustained demand for mid-range and premium bedroom furniture.

Although the 2025 tariff framework has introduced notable pricing pressures by increasing landed costs for import-reliant retailers, the region benefits from its strategic proximity to Mexico, an increasingly important manufacturing alternative as supply chains shift away from China. Expanding retailer showroom footprints in key cities, combined with high homeownership aspirations among younger residents, positions the Southwest as a compelling long-term growth corridor through 2033.

West U.S. Bedroom Furniture Market Trends

The Western United States constitutes the second-largest regional market for bedroom furniture, anchored by California, the nation’s most populous state and its highest-revenue furniture market. With more than 14.1 million households, the region offers a substantial consumer base across all product categories. Pacific Coast states display strong preferences for design-focused, sustainable, and eco-certified furniture, supporting demand for premium and FSC-certified offerings from brands such as Inter IKEA Systems B.V. and Williams-Sonoma, Inc.

Market dynamics are further shaped by federal trade policies and California’s stringent environmental regulations, including CARB Phase 2 standards, which have elevated statewide quality requirements. These policies incentivize manufacturers to adopt cleaner production methods while raising barriers for low-cost producers. High disposable incomes, established retail hubs, and refined aesthetic preferences continue to drive sustained demand for contemporary and luxury furniture.

Competitive Landscape

The U.S. Bedroom Furniture market is highly fragmented, with the top five players collectively accounting for less than 10% of total market revenue. This fragmentation reflects the market's vast geographic spread, diverse consumer preferences across price tiers, and the continued relevance of regional and independent retailers. Market leaders are differentiating through vertical integration, digital transformation, and strategic portfolio expansion. Ashley Furniture Industries, LLC leads through manufacturing scale and retail network breadth, while Wayfair LLC dominates e-commerce via technology-driven personalization. Key strategic trends include direct-to-consumer (DTC) model adoption, FSC-certified sustainable product integration, and smart furniture innovation. Strategic acquisitions, such as Ashley's purchase of Resident Home in 2024, signal intensifying consolidation activity, particularly within the premium beds and mattress sub-segments.

Key Market Developments

- March 2026: Ashley Furniture Industries announced the cessation of manufacturing operations at its Mesquite, Texas, facility, resulting in the layoff of 266 employees. The move, effective May 7, 2026, follows a WARN notice filed with the Texas Workforce Commission. This decision is part of Ashley Furniture’s broader strategy to consolidate production across other facilities, optimize its manufacturing footprint, and enhance vertical integration and long-term operational efficiency.

- October 2025: Inter IKEA acquired U.S.-based logistics technology firm Locus to strengthen its home delivery capabilities. The acquisition enables IKEA to bring advanced logistics functions, such as AI-driven route optimization, real-time tracking, and fulfillment automation, in-house, enhancing last-mile delivery efficiency and customer experience.

- May 2024: Wayfair Inc. opened its first large-format physical store in Wilmette, Illinois, a 150,000 sq ft flagship with a restaurant, marking a landmark shift from its 20-year online-only model to omnichannel retail.

Top Companies in the U.S. Bedroom Furniture Market

- Ashley Furniture Industries, LLC (Arcadia, U.S.) is the largest furniture manufacturer and retailer in North America. Ashley operates 1,100+ stores globally and generates approximately US$ 6 billion in U.S. retail revenue. Its vertically integrated manufacturing model, extensive bedroom portfolio, and the 2024 acquisition of Resident Home (including Nectar and DreamCloud brands) reinforce its market leadership across value, mid-range, and premium price tiers, making it the most influential single player in the U.S. Bedroom Furniture market.

- Inter IKEA Systems B.V. (Delft, Netherlands) operates 52 U.S. stores alongside a rapidly growing e-commerce platform, primarily serving budget and mid-range consumers with flat-pack, design-conscious bedroom furniture. In FY2024, IKEA reported that 97% of its wood was FSC-certified or from recycled sources. Its AI-powered room planning tool and AR visualization application are redefining the digital furniture purchase journey and driving strong omnichannel engagement among younger consumer demographics.

- Wayfair LLC (Boston, U.S.) recorded US$ 10.5 billion in net revenue in 2024 with 21 million active customers. Operating brands including Joss & Main, AllModern, Birch Lane, and Perigold, it serves all price segments. The 2024 launch of its first large-format physical store signals a decisive omnichannel strategy to complement its dominant digital presence and deepen consumer engagement across the full bedroom furniture purchase journey.

Companies Covered in U.S. Bedroom Furniture Market

- Inter IKEA Systems B.V.

- Wayfair LLC

- Ashley Furniture Industries, LLC

- Williams-Sonoma, Inc.

- Restoration Hardware, Inc. (RH)

- La-Z-Boy Inc.

- Crate and Barrel

- Rooms to Go

- Raymour & Flanigan

- Ethan Allen Interiors Inc.

- Herman Miller Inc.

- Sauder Woodworking

- THUMA Inc.

Frequently Asked Questions

The U.S. Bedroom Furniture market is valued at US$ 53.5 Bn in 2026 and is expected to reach US$ 84.2 Bn by 2033, growing at a CAGR of 6.7% during the forecast period, supported by steady housing construction, premiumization trends, and rising consumer spending on home interiors.

Key drivers include sustained residential construction activity, with over 1.4 million housing starts in 2024 per the U.S. Census Bureau, rising disposable incomes, the premiumization trend, and the growing adoption of smart, tech-integrated bedroom furniture solutions showcased at events such as CES 2024.

The Beds & Mattresses segment leads with approximately 37% revenue share, driven by the National Sleep Foundation's recommended 7-10 year mattress replacement cycle, growing sleep health awareness highlighted by the American Academy of Sleep Medicine (AASM), and the expanding smart bed market led by Sleep Number Corporation.

The Southeast U.S. is the leading region, contributing approximately 35% of all new single-family housing starts nationally per the U.S. Census Bureau, underpinned by strong population in-migration to Texas, Florida, Georgia, and North Carolina, and consistently high consumer spending on home furnishings.

Key opportunities include the rapid expansion of e-commerce platforms with AR and AI visualization tools, and the growing demand for FSC-certified, low-VOC, sustainably sourced bedroom furniture, particularly among millennial and Gen Z consumers across the mid-to-premium price tiers.

Key market players include Inter IKEA Systems B.V., Wayfair LLC, Ashley Furniture Industries, LLC, Williams-Sonoma, Inc., Restoration Hardware, Inc. (RH), La-Z-Boy Inc., Crate and Barrel, Rooms to Go, Raymour & Flanigan, Ethan Allen Interiors Inc., Herman Miller Inc., Sauder Woodworking, and THUMA Inc.