- Medical Devices

- Medical Imaging Equipment Market

Medical Imaging Equipment Market Size, Share, and Growth Forecast 2026 - 2033

Medical Imaging Equipment Market by Product Type (X-ray Imaging Systems, Computed Tomography (CT) Scanners, Magnetic Resonance Imaging (MRI) Systems, Ultrasound Imaging Systems, Others), Portability (Fixed/Stationary Systems, Mobile Systems, Portable Systems, Handheld Systems), Application, End-user, and Regional Analysis, 2026 - 2033

Medical Imaging Equipment Market Size and Trend Analysis

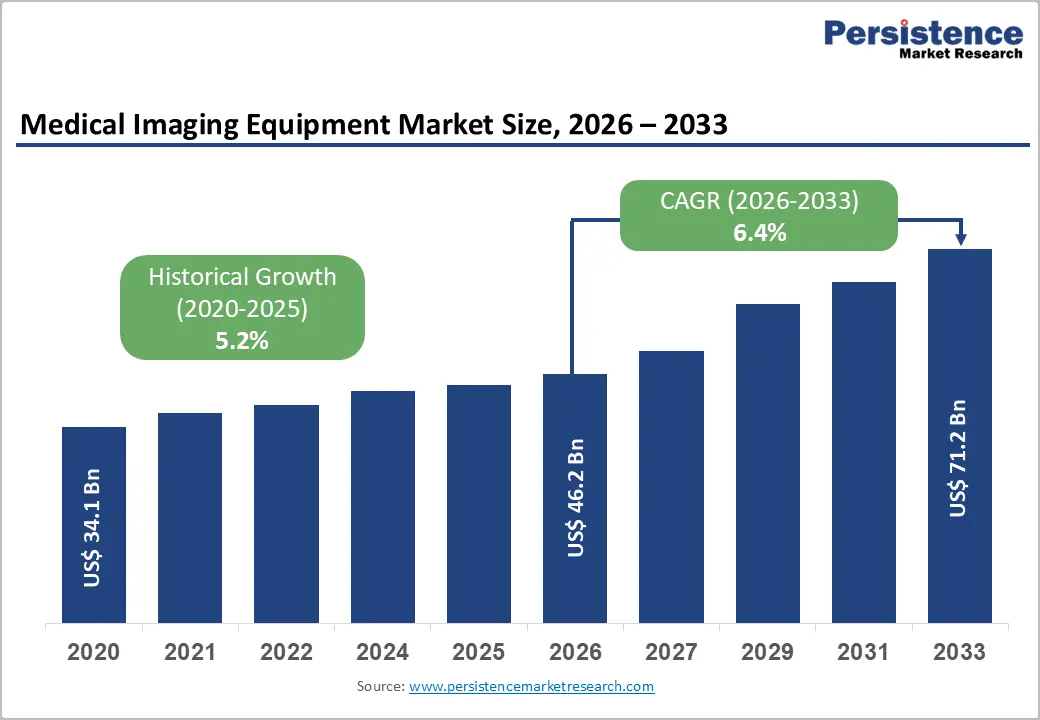

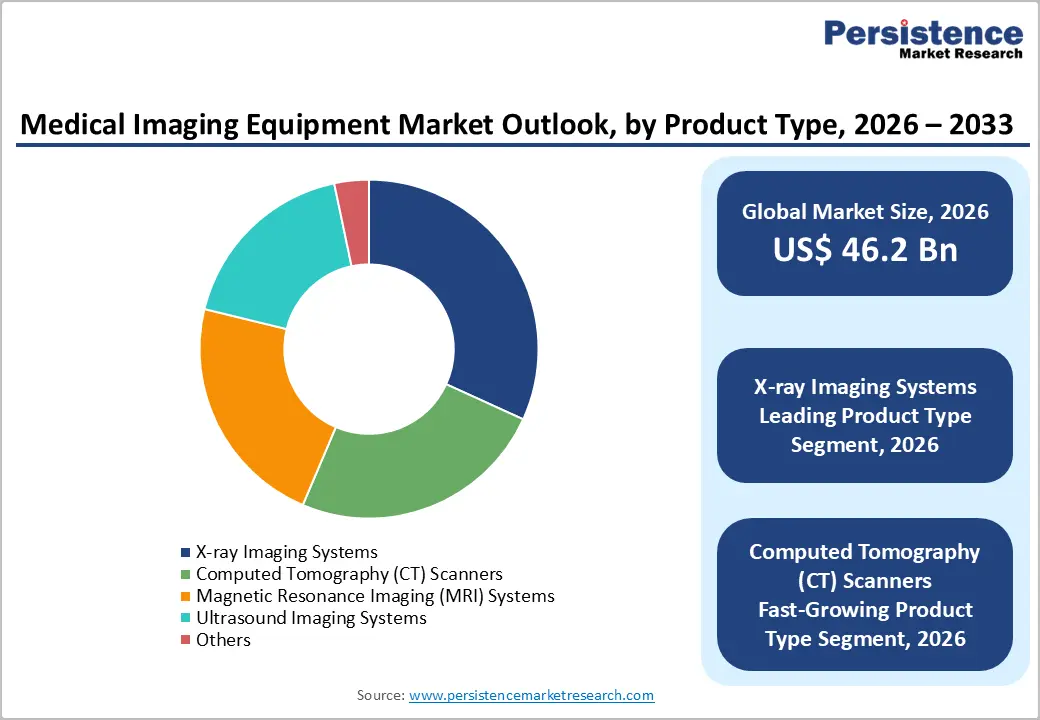

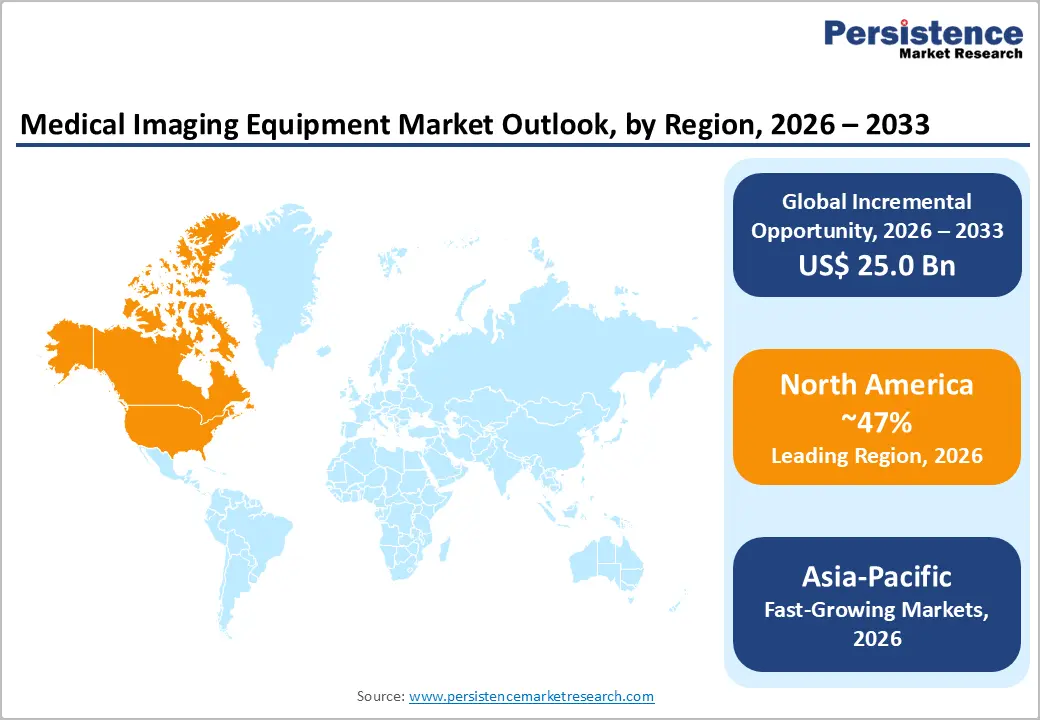

The global Medical Imaging Equipment market size is expected to be valued at US$ 46.2 billion in 2026 and projected to reach US$ 71.2 billion by 2033, growing at a CAGR of 6.4% between 2026 and 2033. Market growth is fundamentally driven by the rise in global burden of chronic and non-communicable diseases, the aging world population requiring advanced diagnostic imaging, and the integration of artificial intelligence into imaging platforms, which is dramatically improving diagnostic accuracy and workflow efficiency.

The World Health Organization (WHO) estimates that non-communicable diseases including cardiovascular diseases, cancer, and neurological disorders, account for 74% of global deaths annually, creating sustained and growing demand for high-resolution diagnostic imaging across all major modalities. Concurrently, expanding healthcare infrastructure investment in the Asia Pacific and the Middle East, favorable reimbursement frameworks in developed markets, and rapid adoption of portable and AI-enabled imaging systems in point-of-care settings are collectively sustaining above-baseline market growth through the forecast horizon.

Key Industry Highlights:

- Regional Leadership: North America holds 47% of global medical imaging equipment market share in 2026, driven by the world's highest CT/MRI density per OECD data, comprehensive Medicare reimbursement, FDA innovation support, and active AI-driven equipment upgrade cycles.

- Fast-Growing Market: Asia Pacific is forecast to register the highest CAGR, driven by China's 14th Five-Year healthcare investment plan, India's Ayushman Bharat infrastructure expansion, and rapidly growing domestic imaging OEMs including United Imaging Healthcare and Mindray.

- X-ray Imaging Systems Dominate Product Type: X-ray Imaging Systems hold 32% product type market share in 2026, underpinned by the broadest global installed base, lowest total cost of ownership, widest clinical versatility, and ongoing digital detector and AI-integrated workflow innovations.

- CT Scanners are the Fastest Growing Product Segment: CT Scanners are forecast to register the highest product CAGR, driven by photon-counting CT commercialization by Siemens Healthineers and GE HealthCare, AI-enhanced reconstruction technology, and oncology and cardiovascular screening volume growth.

- Key Opportunity: Portable and handheld imaging systems, particularly AI-enabled ultrasound represent the highest-growth commercial opportunity, expanding point-of-care diagnostics in emergency medicine, rural healthcare, and resource-limited emerging market settings globally.

Market Dynamics

Drivers - Rising Global Burden of Chronic Diseases and Aging Demographics Fuelling Imaging Demand

The dramatic increase in chronic disease prevalence, particularly cardiovascular diseases, cancer, and musculoskeletal disorders is the primary demand driver for medical imaging equipment. The increase in new cancer cases every year, imaging plays an indispensable role in cancer screening, staging, treatment planning, and response monitoring.

Additionally, the WHO projects that the global population aged 60 and over will reach 2.1 billion by 2050, significantly amplifying demand for neurology, orthopedics, and cardiovascular imaging. The American College of Radiology (ACR) reports that over 900 million imaging procedures are performed annually in the U.S. alone, underscoring the scale of imaging infrastructure demand and the continuous replacement and upgrade cycle that sustains equipment procurement volumes.

AI Integration and Digital Transformation Accelerating Adoption of Next-Generation Imaging Systems

The integration of artificial intelligence and deep learning algorithms into medical imaging systems is fundamentally transforming diagnostic capabilities and driving equipment upgrade cycles. The FDA had authorized over 700 AI/ML-enabled medical devices by 2023, with radiology and medical imaging representing the largest single category. AI-powered features, including automated lesion detection, image noise reduction, workflow triage, and radiology reporting assistance, are now embedded in flagship systems from Siemens Healthineers (AI-Rad Companion), GE HealthCare (Edison platform), and Philips (IntelliSite Pathology Solution). These AI capabilities are accelerating technology refresh demand as existing installed-base equipment becomes functionally obsolete, generating significant incremental capital equipment investment across hospital systems globally.

Restraints - High Capital Equipment Costs and Budget Constraints in Public Healthcare Systems

Advanced medical imaging systems represent among the highest capital expenditure items in hospital procurement budgets. A state-of-the-art 3 Tesla MRI system can cost between US$ 1.5 million and US$ 3 million, while high-end CT and PET-CT systems similarly command million-dollar price points. In public healthcare systems across Europe and emerging markets, constrained capital budgets, lengthy government procurement cycles, and austerity-driven healthcare spending cuts regularly delay equipment replacement and new installations. The OECD notes persistent inequalities in imaging equipment density between high-income and lower-income nations, limiting global adoption rates and constraining market volume growth.

Radiation Safety Concerns and Regulatory Compliance Burden

Ionizing radiation exposure from X-ray and CT imaging remains a significant regulatory and clinical concern, influencing utilization patterns and procurement decisions. The International Commission on Radiological Protection (ICRP) and U.S. Nuclear Regulatory Commission (NRC) impose strict radiation dose management requirements on imaging facilities. Growing clinical emphasis on ALARA (As Low As Reasonably Achievable) principles and the ACR Dose Index Registry compliance requirements create ongoing investment obligations in dose monitoring and management infrastructure, adding operational cost burden and influencing physician referral patterns away from high-dose imaging modalities in some clinical scenarios.

Opportunities - CT Scanner Innovation Driving Fastest Product Segment Growth

Computed Tomography (CT) scanners are the fastest-growing product segment in the medical imaging equipment market, driven by continuous technological innovation in photon-counting CT, spectral CT, and low-dose acquisition protocols. The introduction of photon-counting CT commercialized by Siemens Healthineers with the NAEOTOM Alpha in 2021 and subsequently by GE HealthCare represents a generational leap in CT resolution, enabling unprecedented tissue contrast without increased radiation dose. The Radiological Society of North America (RSNA) annual meeting consistently features photon-counting and AI-enhanced CT as the most-attended innovation categories. Healthcare systems globally are accelerating CT fleet modernization programs to access these clinical advantages, creating substantial capital equipment replacement demand that vendors are well-positioned to capitalize on through the forecast period.

Portable and Handheld Imaging Systems Expanding Point-of-Care and Emerging Market Penetration

The rapid advancement of portable and handheld medical imaging technology particularly ultrasound is creating a transformative growth opportunity by extending diagnostic imaging to point-of-care, emergency, and resource-limited settings. Handheld ultrasound devices such as Butterfly Network's iQ+ and GE HealthCare's Vscan Air have demonstrated clinical utility across emergency medicine, cardiology bedside assessment, and rural healthcare delivery. The World Health Organization (WHO)'s Essential Diagnostics List and programs targeting imaging access in low-resource settings are expanding the addressable market for affordable portable systems. In emerging economies, handheld and portable imaging platforms offer an entry point for healthcare infrastructure development without the capital requirements of fixed system installations, representing a high-volume, high-growth commercial opportunity for imaging equipment manufacturers with competitively priced portable portfolios.

Category-wise Analysis

Product Type Insights

X-ray imaging systems lead the medical imaging equipment product market with approximately 32% market share in 2026. X-ray's dominant position reflects its status as the most widely deployed, cost-accessible, and clinically versatile diagnostic imaging technology globally. The modality is used across virtually all clinical specialties, from chest radiography in pulmonology to orthopedic trauma assessment, and operates with lower installation, maintenance, and operational costs compared to MRI or CT. According to the WHO, X-ray is the imaging modality with the widest global installed base and the primary first-line diagnostic tool in both developed and emerging health systems. Continuous innovation in digital detector flat-panel X-ray, wireless mobile DR systems, and AI-powered automated reading is sustaining demand in both hardware replacement and new installation segments.

Portability Insights

Fixed/Stationary Systems constitute the dominant portability segment, accounting for approximately 58% of the medical imaging equipment market in 2025. Fixed systems installed in dedicated radiology suites, MRI rooms, and CT scanning bays deliver the highest image resolution, broadest clinical functionality, and maximum patient throughput of any imaging configuration. Hospitals and dedicated diagnostic imaging centers continue to invest in fixed system upgrades to benefit from the latest detector technologies, magnet field strengths, and AI-integrated software platforms. High-acuity clinical workflows in oncology, neurology, and cardiovascular imaging require the consistency and clinical performance that only fixed, fully configured imaging suites can deliver, sustaining the segment's dominant revenue contribution across all major geographies.

Application Insights

Oncology is the leading application segment, representing approximately 28% of the medical imaging equipment market in 2025. The extraordinary clinical centrality of imaging in cancer management from screening mammography and lung cancer CT screening to PET-CT staging, MRI treatment planning, and therapy response assessment, makes oncology the highest-value and highest-volume application for virtually every imaging modality. The IARC projects global cancer incidence to rise to 28.4 million new cases per year by 2040, representing a massive secular demand driver. Leading imaging vendors are heavily investing in oncology-specific AI applications, dedicated oncology CT and MRI protocols, and molecular imaging (PET-CT) capabilities to capture the disproportionate imaging demand generated by this indication.

End-user Insights

Hospitals are the dominant end-user segment, commanding approximately 52% of medical imaging equipment revenue in 2026. Hospitals, particularly large academic medical centers and multi-specialty regional hospitals, procure the broadest array of imaging equipment, including MRI, CT, PET-CT, digital X-ray, and interventional imaging systems. The American Hospital Association (AHA) reports over 6,100 registered hospitals in the U.S., each operating multi-modality imaging suites with active equipment replacement cycles. Capital equipment procurement decisions within hospitals are supported by DRG reimbursement structures, with imaging studies representing one of the highest-volume and most reimbursed clinical service lines. Hospitals' scale procurement volumes, multi-system vendor relationships, and ongoing fleet modernization requirements make them the primary revenue-generating end-user segment for equipment manufacturers.

Regional Insights

North America Medical Imaging Equipment Market Trends and Insights

North America accounted for approximately 47.0% of the global medical imaging equipment market in 2025, supported by the world’s largest installed base of MRI, CT, and digital radiography systems, comprehensive reimbursement through Medicare, Medicaid, and private insurers, and rapid adoption of AI-enabled diagnostic imaging. The region is home to leading manufacturers such as GE HealthCare and Hologic, Inc., which continue to drive innovation in photon-counting CT, high-field MRI, and portable ultrasound. Ongoing replacement of aging imaging systems and expansion of outpatient diagnostic networks are sustaining robust equipment demand across hospitals and aging centers.

U.S. Medical Imaging Equipment Market Trends and Insights

The U.S. represented nearly 85.6% of the North American medical imaging equipment market in 2025. High diagnostic imaging utilization, favorable reimbursement, and strong capital spending by integrated delivery networks support continued adoption of advanced CT, MRI, mammography, and digital X-ray systems. Domestic innovation led by GE HealthCare and Hologic, Inc. further strengthens market leadership.

Canada Medical Imaging Equipment Market Trends and Insights

Canada accounted for approximately 9.8% of the regional market in 2025. Provincial investments to reduce imaging wait times, replacement of aging MRI and CT scanners, and expansion of community-based diagnostic services in Ontario, Quebec, and British Columbia are driving steady demand for advanced medical imaging equipment. Europe Medical Imaging Equipment Market Trends and Insights\

Europe Medical Imaging Equipment Market Trends and Insights

Europe accounted for approximately 28.4% of the global medical imaging equipment market in 2025, supported by universal healthcare systems, mature diagnostic infrastructure, and strong local manufacturing capabilities. The region benefits from the presence of Siemens Healthineers and Philips, both of which play central roles in MRI, CT, ultrasound, and molecular imaging innovation. Continued replacement of aging scanners, expansion of outpatient diagnostic centers, and adoption of AI-assisted imaging workflows are driving steady market growth across major European healthcare systems.

Germany Medical Imaging Equipment Market Trends and Insights

Germany represented approximately 24.7% of the European medical imaging equipment market in 2025. Strong hospital capital budgets, broad statutory health insurance coverage, and the headquarters of Siemens Healthineers support sustained demand for premium MRI, CT, and hybrid imaging systems in university and tertiary care hospitals.

UK Medical Imaging Equipment Market Trends and Insights

UK accounted for nearly 16.3% of the regional market in 2025. Expansion of NHS Community Diagnostic Centres and targeted investments to reduce imaging backlogs are generating substantial procurement demand for MRI, CT, and digital radiography systems across the country.

Asia Pacific Medical Imaging Equipment Market Trends and Insights

Asia Pacific accounted for approximately 19.6% of the global medical imaging equipment market in 2025 and is the fastest-growing regional market, projected to expand at a CAGR of around 8.7% through 2032. Growth is driven by rapid hospital construction, increasing healthcare expenditure, broader insurance coverage, and rising demand for advanced diagnostic imaging. Regional manufacturers such as United Imaging Healthcare Co., Ltd. and Shenzhen Mindray Bio-Medical Electronics Co., Ltd. are strengthening local production and accelerating adoption of cost-competitive CT, MRI, ultrasound, and digital X-ray systems across emerging and developed healthcare markets.

China Medical Imaging Equipment Market Trends and Insights

China represented nearly 42.8% of the Asia Pacific medical imaging equipment market in 2025. Strong government investment in hospital infrastructure, domestic procurement preferences, and rising adoption of premium CT and MRI systems are driving sustained demand. Local manufacturers led by United Imaging Healthcare Co., Ltd. continue to gain share in both public and private hospital tenders.

India Medical Imaging Equipment Market Trends and Insights

India accounted for approximately 12.7% of the regional market in 2025 and is projected to grow at a CAGR of around 10.4% through 2032. Expansion of private hospital chains, Ayushman Bharat-supported diagnostic access, and increasing installation of CT, MRI, and ultrasound systems in tier-2 and tier-3 cities are significantly expanding the country's imaging equipment market.

Competitive Landscape

The global medical imaging equipment market is moderately consolidated, with four major players Siemens Healthineers AG, GE HealthCare Technologies Inc., Koninklijke Philips N.V., and Canon Medical Systems Corporation, collectively commanding over 55% of global revenue.

Key competitive strategies include AI platform differentiation, portfolio expansion into portable and handheld segments, value-based healthcare service models (equipment-as-a-service), and geographic penetration of Asia Pacific through localized product development. Emerging Chinese manufacturers including United Imaging Healthcare and Mindray are intensifying competition in the mid-market and emerging markets segment through aggressive pricing and NMPA-accelerated product launches.

Key Developments

- In May 2026, Philips introduced Titanion MR, an ultra-high-gradient 3.0T MRI system, at the ISMRM 2026. The platform combines advanced gradient performance with AI-enabled workflows to support quantitative imaging and biomarker development, expanding MRI capabilities beyond conventional anatomical and functional imaging.

- In May 2026, HKSH Medical Group and Siemens Healthineers partnered to establish Asia’s first Photon-Counting CT Simulator (PCCT-Sim) Reference Site in Hong Kong, advancing photon-counting technology for precision radiotherapy planning, clinical research, and industry training.

Companies Covered in Medical Imaging Equipment Market

- Siemens Healthineers AG

- GE HealthCare Technologies Inc.

- Koninklijke Philips N.V.

- Canon Medical Systems Corporation

- FUJIFILM Holdings Corporation

- Shimadzu Corporation

- Hologic, Inc.

- Samsung Medison Co., Ltd.

- Carestream Health, Inc.

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

- Esaote S.p.A.

- Konica Minolta Healthcare Americas, Inc.

- Planmeca Oy

- FONAR Corporation

- United Imaging Healthcare Co., Ltd.

- Others

Frequently Asked Questions

The global Medical Imaging Equipment market is expected to be valued at US$ 46.2 billion in 2026, growing from US$ 34.1 billion in 2020 at a historical CAGR of 5.2%. It is projected to reach US$ 71.2 billion by 2033, driven by rising chronic disease burden, AI-integrated imaging system adoption, and expanding healthcare infrastructure investment across Asia Pacific.

Rising prevalence of cancer, cardiovascular and neurological disorders, expanding aging populations, and increasing demand for early and accurate diagnostic imaging are driving adoption of advanced medical imaging equipment.

North America is the leading region with approximately 47% global market share in 2025, anchored by the world's highest MRI and CT density per OECD data, comprehensive Medicare reimbursement for diagnostic imaging procedures, the FDA innovation ecosystem, and the U.S. headquarters of major imaging OEMs including GE HealthCare and Hologic, Inc.

Significant opportunities lie in AI-enabled imaging systems, handheld and portable devices, emerging market healthcare expansion, and replacement of aging diagnostic equipment with high-resolution digital platforms.

Leading companies include Siemens Healthineers AG, GE HealthCare Technologies Inc., Koninklijke Philips N.V., Canon Medical Systems Corporation, FUJIFILM Holdings Corporation, United Imaging Healthcare Co., Ltd., Shenzhen Mindray, Hologic, Inc., Samsung Medison, and Butterfly Network, Inc., competing through AI platform differentiation, photon-counting CT innovation, portable imaging expansion, and emerging market penetration strategies.