- Off-Road Equipment & Machinery

- Global Construction Mining Equipment Market

Global Construction Mining Equipment Market Size, Share, and Growth Forecast 2026 - 2033

Construction Mining Equipment Market by Product Type (Excavators, Loaders, Dozers, Crushing, Pulverizing & Screening Equipment, Dump Trucks/Haul Trucks, Motor Graders, Cranes & Lifting Equipment, Drilling & Mining Equipment), Application (Construction Applications (Residential, Commercial, Infrastructure, Industrial), Mining Applications (Coal Mining, Metal Mining, Quarrying & Minerals)), Sales Type, and Regional Analysis, 2026-2033

Global Construction Mining Equipment Market Size and Trend Analysis

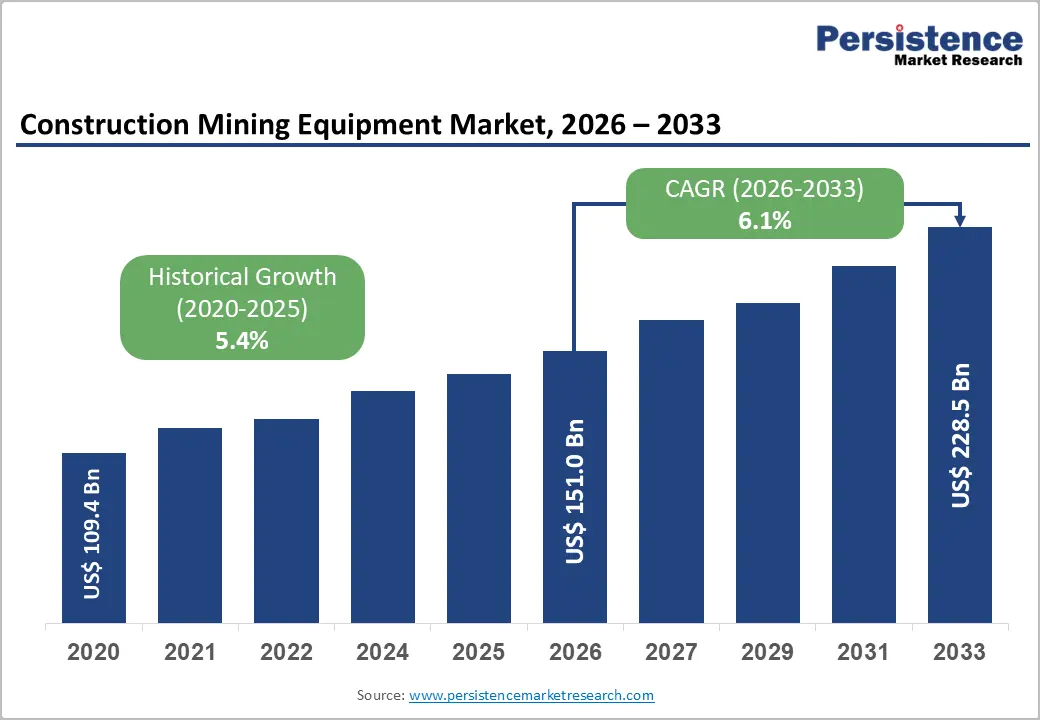

The global construction mining equipment market size is expected to reach US$151 billion in 2026 and is projected to reach US$228.6 billion by 2033, growing at a CAGR of 6.1% between 2026 and 2033. The market expansion is anchored in a multi-trillion-dollar global infrastructure pipeline and accelerating mineral demand for the energy transition.

According to the G20 Global Infrastructure Hub, the world needs roughly US$94 trillion in infrastructure investment by 2040, while the International Energy Agency (IEA) projects that demand for critical minerals such as copper, lithium, and nickel will more than double by 2030 under stated policy scenarios. These twin pillars, combined with rapid fleet electrification and OEM deployment of autonomous machinery by Caterpillar, Komatsu, and SANY, are sustaining double-digit capex commitments across construction and mining contractors.

Key Industry Highlights:

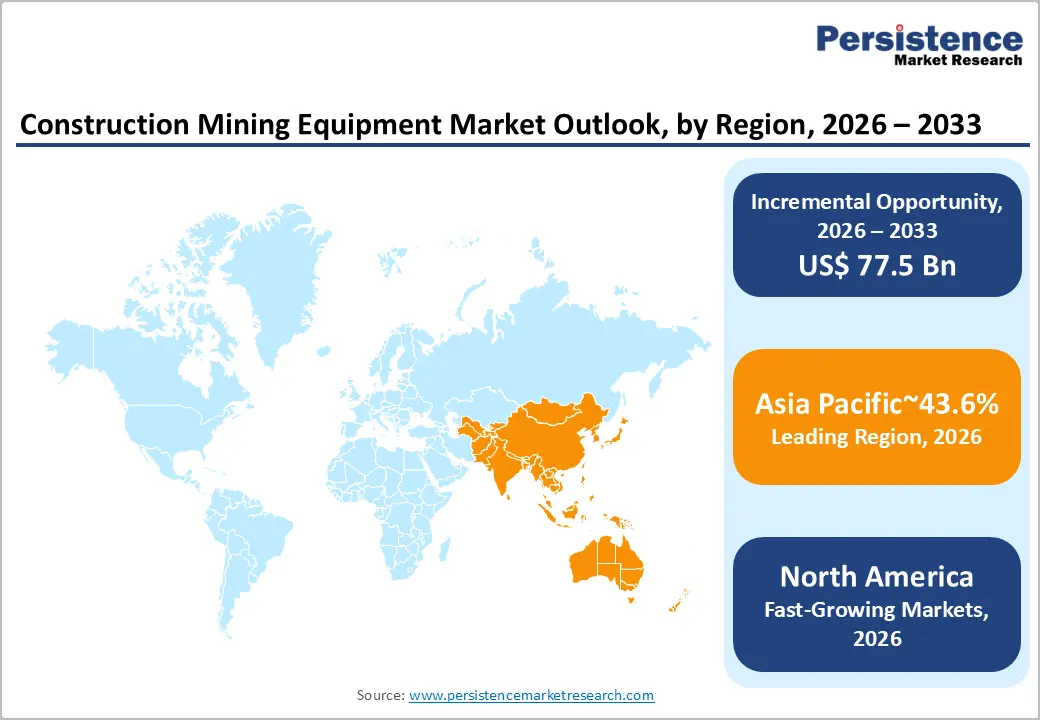

- Leading Region: Asia Pacific dominates with a 43.6% share in 2026, supported by China’s US$15.1 billion market, India’s capex surge, and Southeast Asia’s nickel and infrastructure-driven equipment demand.

- Fast-Growing Region: Asia Pacific is also the fast-growing region with a forecast CAGR above 7% in the forecast period, propelled by Indian Bharatmala projects and Southeast Asia’s critical-mineral mining expansion.

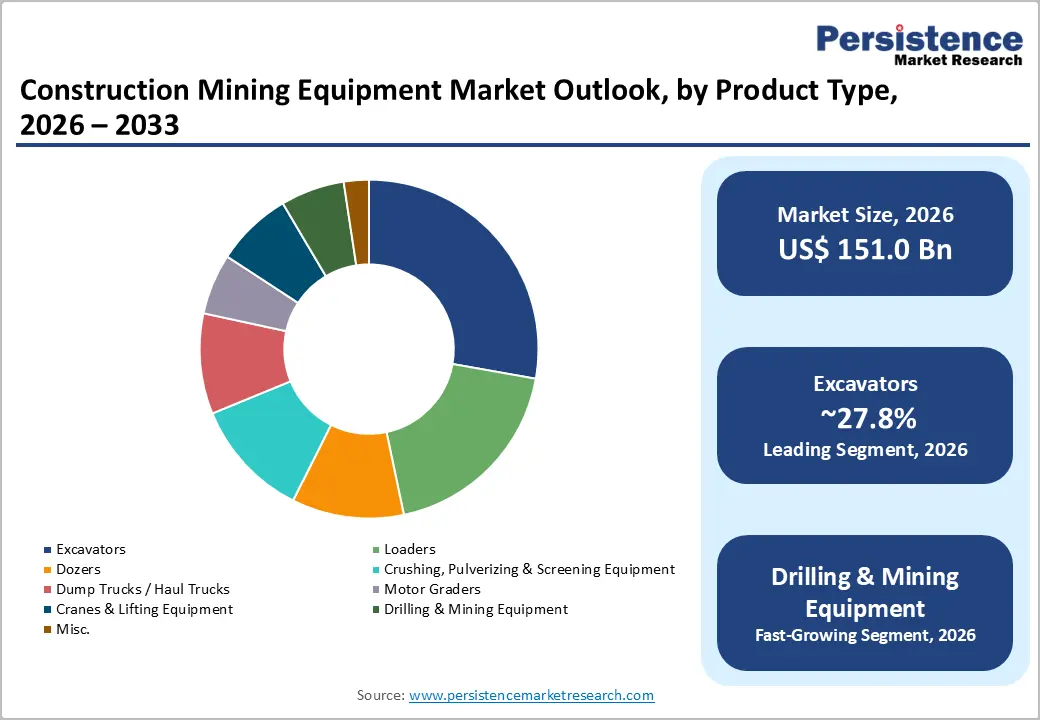

- Dominant Product: Excavators lead the product-type category with a 28% share in 2026, owing to versatility across construction, mining, demolition, and infrastructure applications across all major regional markets globally.

- Fastest Growing Segment: Drilling & Mining Equipment is the fastest-growing product category between 2026 and 2033, fueled by IEA forecasts of doubling critical-mineral demand and ultra-class capex by BHP and Rio Tinto.

- Key Opportunity: Autonomous and electric equipment plus aftermarket service contracts represent the highest-margin opportunity, with parts margins of 25-30% and rapid OEM rollouts by Caterpillar, Komatsu, and SANY.

DRO Analysis

Drivers - Infrastructure Mega-Projects and Public Capex Programs Anchor Equipment Demand

Governments worldwide are channelling unprecedented public capital into roads, rail, ports, and energy grids, translating directly into excavator, loader, and haul-truck procurement. The U.S. Bipartisan Infrastructure Law allocates US$1.2 trillion through 2026, while India’s Ministry of Finance raised capital expenditure by 11.1% to US$133 billion in FY 2024-25 (equivalent to 3.4% of GDP).

China’s National Bureau of Statistics reported fixed-asset investment in infrastructure construction grew 4.4% year-on-year in 2024. These commitments, supported by the European Investment Bank mobilising EUR 88 billion of financing in 2024, ensure a deep multi-year backlog for heavy equipment OEMs.

Critical Mineral Demand for Energy Transition Lifts Mining Fleet Renewal

The electrification of transport and renewable build-out is reshaping mine plans and equipment specifications. The International Energy Agency (IEA) estimates that copper demand will reach roughly 33 million tonnes by 2040 under the Announced Pledges Scenario, with lithium demand multiplying nearly 9-fold by 2040.

The U.S. Geological Survey (USGS) recorded global mine production of copper at 23 million tonnes in 2024, while Rio Tinto and BHP sanctioned over US$30 billion in combined growth capex for copper and iron ore in 2024. Such investments translate into orders for ultra-class haul trucks, hydraulic shovels, and autonomous drills.

Restraints - Volatile Raw Material and Component Costs Compress OEM Margins

Heavy equipment manufacturers face persistent input-cost pressure from steel, copper, semiconductors, and hydraulic components. According to the World Steel Association, global crude steel prices remained elevated through 2024, with hot-rolled coil averaging US$ 720-780 per tonne in key markets.

The Semiconductor Industry Association (SIA) noted that automotive- and industrial-grade chip lead times stretched to 26 weeks in late 2024. These constraints elevate sticker prices for excavators and dozers, deferring purchases by smaller contractors and lengthening fleet replacement cycles in price-sensitive regions.

Stringent Emission Norms Elevate Compliance Burden for Diesel Fleets

Tightening exhaust regulations, such as the U.S. EPA Tier 4 Final, EU Stage V, and China Stage IV standards, require costly aftertreatment retrofits and engineering redesign. The European Environment Agency reported that non-road mobile machinery contributed nearly 15% of NOx emissions in the EU transport sector in 2023. Compliance adds an estimated US$ 8,000-12,000 per unit to mid-size machine costs, slowing replacement in cost-sensitive end-markets and pressuring OEM working capital.

Opportunities - Autonomous and Electric Equipment Open New Revenue Pockets

OEM investment in zero-emission and autonomous machinery is opening premium-priced product categories. Caterpillar recorded over 680 million tonnes of material moved by its autonomous truck fleet by the end of 2024, while Komatsu reached over 750 cumulative autonomous haul truck deployments globally. In April 2026, Komatsu launched the PC9000-12, available in diesel Tier 4, unregulated diesel, and electric drive configurations. SANY Group rolled out its 1,000th electric excavator in May 2026. These shifts allow OEMs to capture aftermarket recurring revenue through fleet-management software, telematics subscriptions, and battery service contracts.

Aftermarket Services and Equipment Rental Generate High-Margin Streams

Total cost-of-ownership models and contractor preference for asset-light operations are channelling demand into rental fleets and parts-and-services contracts. The American Rental Association (ARA) projected U.S. equipment rental revenue at US$78.2 billion in 2024, with double-digit growth forecast for the construction segment.

United Rentals reported revenue of US$15.3 billion in 2024, while Ashtead Group (Sunbelt) delivered US$10.9 billion in revenue. Aftermarket parts typically deliver 25-30% gross margins versus 15-18% on new equipment, making service contracts a strategic priority for OEMs such as Caterpillar and Volvo Construction Equipment.

Category-wise Analysis

Product Type Insights

Excavators lead the global construction and mining equipment market with approximately 28% share in 2026. Their dominance stems from unmatched versatility across earthmoving, trenching, demolition, mining, and forestry tasks.

According to data from the Japan Construction Equipment Manufacturers Association (CEMA), hydraulic excavator shipments accounted for the single largest equipment category by unit volume in 2024. Caterpillar, Komatsu, Hitachi Construction Machinery, SANY, and XCMG collectively produced more than 280,000 excavator units in 2024. India’s Indian Construction Equipment Manufacturers Association (ICEMA) reported 33% growth in crawler excavator sales in FY 2023-24, underscoring sustained demand from highway and metro projects.

Application Insights

The construction application segment dominates with approximately 68% share in 2026, driven by housing, urban infrastructure, and commercial development. The Oxford Economics Global Construction 2030 study indicated that worldwide construction output exceeded US$12 trillion in 2024, with infrastructure and residential construction together accounting for over 60% of activity.

India’s Pradhan Mantri Awas Yojana - Urban (PMAY-U) sanctioned 1.18 crore houses, with 86.6 lakh completed by 2024. Within mining, World Coal Association data shows global coal production held above 8.7 billion tonnes in 2024, while copper, iron ore, and lithium mining capex underpinned demand for haul trucks and shovels. Construction applications absorb a higher diversity of equipment categories, securing their leading position.

Regional Insights

North America Construction Mining Equipment Market Trends and Insights

North America holds a share of 24.1% in 2026, supported by federal infrastructure stimulus under the Bipartisan Infrastructure Law and Inflation Reduction Act, the reshoring of semiconductor and EV battery plants, and a record pipeline of LNG and data-center construction. Demand is concentrated in compact excavators, large mining trucks for copper and gold operations, and electrified urban fleets. Penetration of telematics-enabled and Tier 4 Final-compliant machinery is among the highest globally.

U.S. Construction Mining Equipment Market Size

The U.S. Construction Mining Equipment market is valued at US$29.8 billion in 2026, driven by US$2.2 trillion in total construction spending as per the U.S. Census Bureau, 1.6 million new housing starts in 2024, and 8.2 million construction workers as per the Bureau of Labour Statistics. Mining capex from Freeport-McMoRan and Newmont, plus chip-fab and EV-plant ground-up builds, anchor heavy-equipment orders.

Europe Construction Mining Equipment Market Trends and Insights

Europe accounts for a share of 20.3% in 2026. According to Eurostat, EU construction output rose 0.4% month-on-month in December 2024, with Spain (+11.2%), Czechia (+9.7%), and Slovakia (+5.8%) leading annual growth. The EU Green Deal and REPowerEU initiatives are channelling investment into grid, wind, and renovation projects, lifting demand for compact and electrified equipment compliant with Stage V emission norms.

Germany Construction Mining Equipment Market Size

Germany’s Construction Mining Equipment market reached US$ 7 billion in 2026, driven by the EUR 500 billion Special Infrastructure Fund approved by the Bundestag in 2024 and rail-network modernisation led by Deutsche Bahn. OEM presence of Liebherr, Wirtgen Group (John Deere), and Bauer Group reinforces a high-tech, export-oriented production base focused on hybrid and electric crawler excavators.

U.K. Construction Mining Equipment Market Size

The U.K. Construction Mining Equipment market is valued at US$4.5 billion in 2026, supported by HS2 rail works, Hinkley Point C nuclear construction, and the GBP 100 billion capital plan unveiled by HM Treasury. Domestic OEM JCB shipped over 110,000 machines globally in 2024 and is investing GBP 100 million in hydrogen combustion engine development for off-highway equipment.

France Construction Mining Equipment Market Size

France’s construction mining equipment market is estimated at US$3.6 billion in 2026, supported by the Grand Paris Express metro program, the largest transport project in Europe at EUR 42 billion, and post-Olympics urban regeneration. Manitou Group and Mecalac lead domestic production, with strong adoption of compact electric loaders aligned with France’s low-emission urban zones.

Asia Pacific Construction Mining Equipment Market Trends and Insights

Asia Pacific holds a dominant share of 43.6% in 2026, anchored by China’s massive infrastructure stimulus, India’s capex surge, and Southeast Asia’s industrial corridor build-out. China alone produced over 420,000 excavators in 2024, per the China Construction Machinery Association (CCMA). Demand is tilted toward mid-to-large excavators, ultra-class mining trucks for coal and iron ore, and the rapid rollout of electric and intelligent equipment by SANY, XCMG, and Zoomlion.

China Construction Mining Equipment Market Size

China’s Construction Mining Equipment market is valued at US$15.1 billion in 2026, driven by RMB 4.06 trillion of fixed-asset investment in infrastructure (per the National Bureau of Statistics of China), the Belt and Road Initiative export pull, and accelerating coal and rare-earth mining capex. Domestic OEMs SANY, XCMG, and LiuGong together command over 60% of the domestic excavator share.

India Construction Mining Equipment Market Size

India’s construction mining equipment market size is valued at US$24.3 billion in 2026 reflecting the broad construction-allied equipment ecosystem, driven by an 11.1% hike in central capex to US$133 billion in FY 2024-25, the Bharatmala and Sagarmala programs, and Coal India Limited targeting 1 billion tonnes output. ICEMA forecasts the construction equipment industry to triple in size by 2030.

Southeast Asia Construction Mining Equipment Market Size

Southeast Asia’s Construction Mining Equipment market is valued at US$8.9 billion in 2026, with Indonesia, Vietnam, and the Philippines leading demand. Indonesia’s Nusantara new-capital project (estimated US$32 billion) and nickel-mining boom (Indonesia produces over 50% of global nickel per the USGS) underpin sales of large hydraulic excavators, off-highway dump trucks, and crushing plants.

Competitive Landscape

The global construction mining equipment market is moderately consolidated, with the top five OEMs, Caterpillar, Komatsu, SANY, XCMG, and Hitachi Construction Machinery holding approximately 45-50% of global revenue. Leaders are differentiating through autonomy, electrification, and integrated digital fleet platforms such as Caterpillar’s Cat MineStar and Komatsu’s smart construction. R&D intensity averages 3.5-4.5% of sales among top players. Emerging business models include equipment-as-a-service, battery-swap fleets, and OEM-financed rental partnerships, while Chinese OEMs are expanding aggressively across Africa, Latin America, and Southeast Asia.

Key Developments:

- In May 2026, SANY Group rolled out its 1,000th electric excavator and expanded commercial deployment of 5G remote-controlled excavators and unmanned paving-roller fleets, strengthening adoption of smart and sustainable technologies in construction and mining.

- In April 2026, Komatsu Germany Mining Division globally launched the PC9000-12, the largest hydraulic mining excavator in its portfolio, available in diesel Tier 4, unregulated diesel, and electric drive configurations for high-productivity surface mining.

- In March 2026: Caterpillar showcased AI-led autonomy, fleet connectivity, and digital service solutions at CONEXPO-CON/AGG 2026, reinforcing intelligent automation across construction and mining equipment to address productivity and labour-shortage challenges.

Global Construction Mining Equipment Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 110.1 Billion |

|

Current Market Value (2026) |

US$ 151.0 Billion |

|

Projected Market Value (2033) |

US$ 228.6 Billion |

|

CAGR (2026-2033) |

6.1% |

|

Leading Region |

Asia Pacific, 43.6% share in 2026 |

|

Dominant Category-1 (Product Type) |

Excavators, 28% share in 2026 |

|

Top-ranking Category-2 (Application) |

Construction Applications, 68% share in 2026 |

|

Incremental Opportunity (2026-2033) |

US$ 77.6 Billion |

Companies Covered in Global Construction Mining Equipment Market

- Caterpillar Inc.

- Komatsu Ltd.

- Deere & Company (John Deere)

- XCMG (Xuzhou Construction Machinery Group)

- Liebherr Group

- SANY Heavy Industry

- Hitachi Construction Machinery

- Volvo Construction Equipment

- JCB (Joseph Cyril Bamford)

- Sandvik Mining & Rock Technology

- Doosan Bobcat (Hyundai Doosan Infracore)

- Zoomlion Heavy Industry

- Terex Corporation

- Atlas Copco AB

- CNH Industrial (Case Construction Equipment)

Frequently Asked Questions

The Global Construction Mining Equipment Market size is expected to be valued at US$ 151.0 Billion in 2026 and projected to reach US$ 228.6 Billion by 2033, growing at a CAGR of 6.1% between 2026 and 2033.

Massive public infrastructure capex, such as the US$1.2 trillion U.S. Bipartisan Infrastructure Law and India’s 11.1% capex hike to US$133 billion in FY 2024-25, combined with critical-mineral mining capex for the energy transition, is the principal demand driver.

Asia Pacific leads the Global Construction Mining Equipment Market with a 43.6% share in 2026, supported by China’s US$15.1 billion market, India’s rising public capex, and Southeast Asia’s mining and infrastructure boom.

Autonomous, electric, and connected equipment combined with high-margin aftermarket services represent the key opportunity, with parts gross margins of 25-30% and rapid commercialisation led by Caterpillar, Komatsu, and SANY.

Key players include Caterpillar Inc., Komatsu Ltd., SANY Group, XCMG Group, Hitachi Construction Machinery, Volvo Construction Equipment, Liebherr Group, Deere & Company, JCB, Sandvik AB, and Epiroc AB.