- Sensors & Controls

- India CCTV Camera Market

India CCTV Camera Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

India CCTV Camera Market by Camera Type (Box Camera, Dome Camera, PTZ Camera, Fisheye Camera & Others), Connectivity (Wired, Wireless, IP or Network), Functionality (Day/Night, IR/Night Vision, Thermal Imaging, Varifocal, ANPR & LPR), End-user (Commercial, Residential, Industrial, Government, Military & Defense) and Regional Analysis for 2026 - 2033

India CCTV Camera Market Share and Trends Analysis

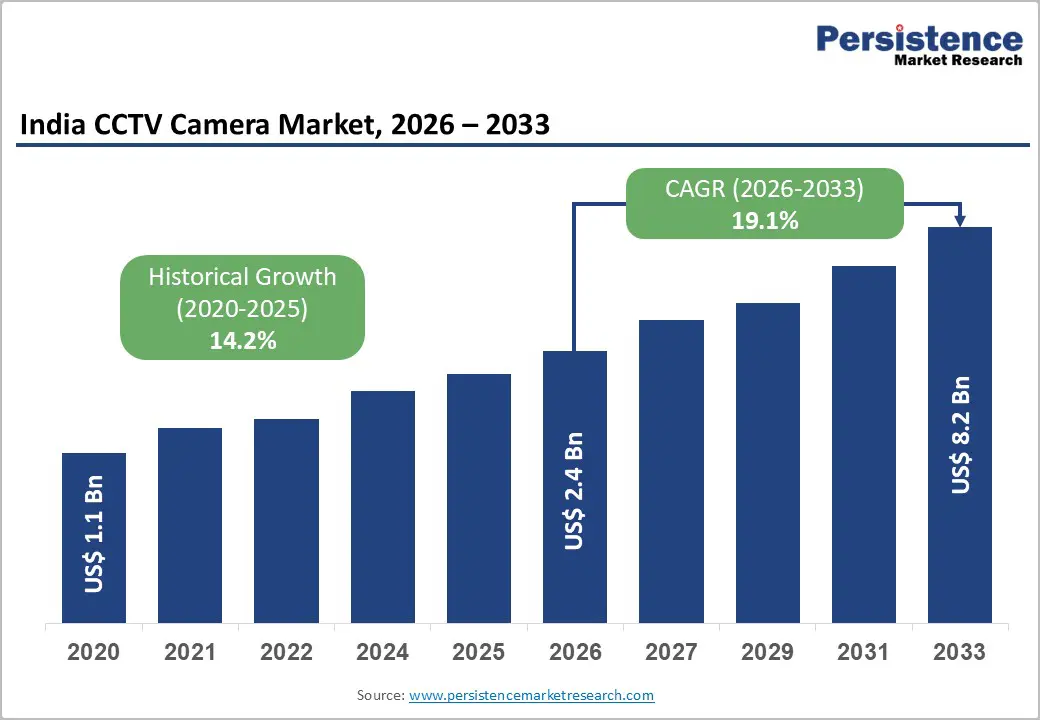

The India CCTV Camera Market size is projected at US$2.4 Bn in 2026 and is projected to reach US$8.2 Bn by 2033, growing at a CAGR of about 19.1% between 2026 and 2033.

Demand is driven by rapid urbanization, smart city investments, and heightened security awareness across commercial, residential, and public infrastructure projects. Government initiatives such as the Smart Cities Mission and state-level surveillance programs are increasing the deployment of video surveillance systems in transport, public spaces, and utilities. Technological shifts toward IP, AI-enabled analytics, and cloud-based storage are further boosting value per installation, expanding addressable revenue beyond hardware into software and services.

Key Industry Highlights:

- The India CCTV camera market is projected at US$2.42 Bn in 2026 and is expected to reach US$8.20 Bn by 2033, implying a CAGR of 19–20% over 2026–2033.

- AI-enabled and IP-based video surveillance revenues, including AI CCTV, are expected to grow at 20%+ CAGR, with AI CCTV alone projected to reach about US$3.7 Bn by 2030.

- Dome cameras lead with about 32.5% share, while fisheye cameras are projected to grow around 21.1% CAGR as 360-degree coverage gains traction in commercial and public-area deployments.

- Wired solutions retain roughly 46.7% share, whereas IP/network cameras are expected to grow at a near 21.9% CAGR, helped by smart-city and enterprise network integration.

- IR/Night Vision leads functionality with around 34.2% share, while ANPR & LPR-enabled solutions are poised for about 22% CAGR on the back of ITS, tolling, and parking projects.

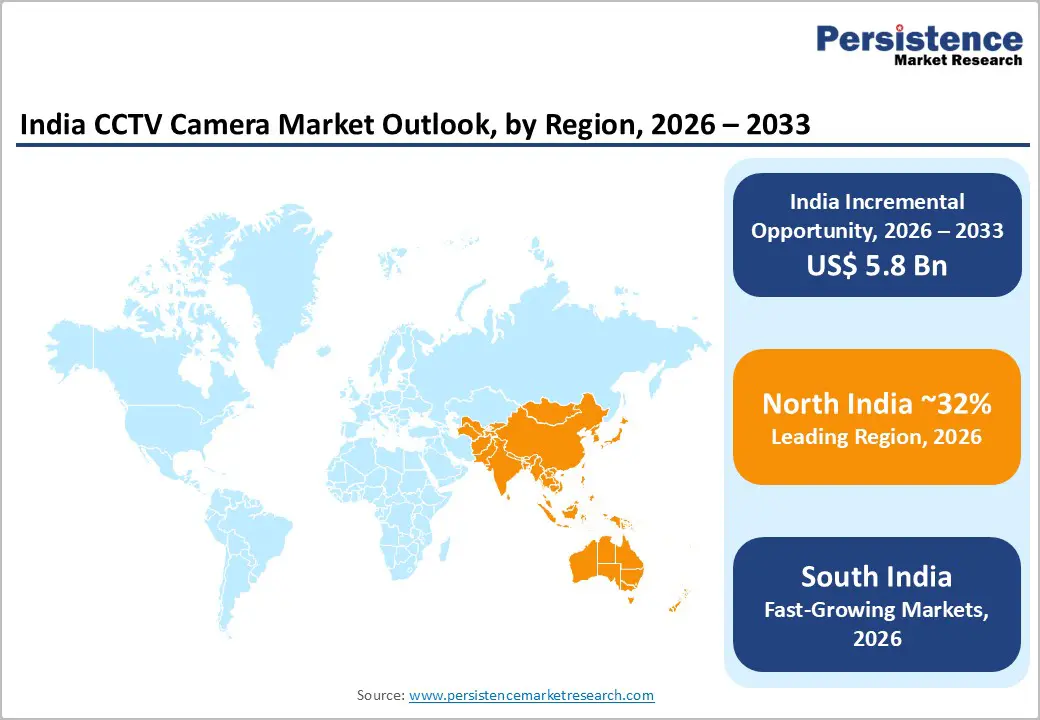

- North India accounts for about 31.8% market share, West India about 27.4% with 18.6% CAGR, and South India is projected to grow at nearly 19.9% CAGR through 2033.

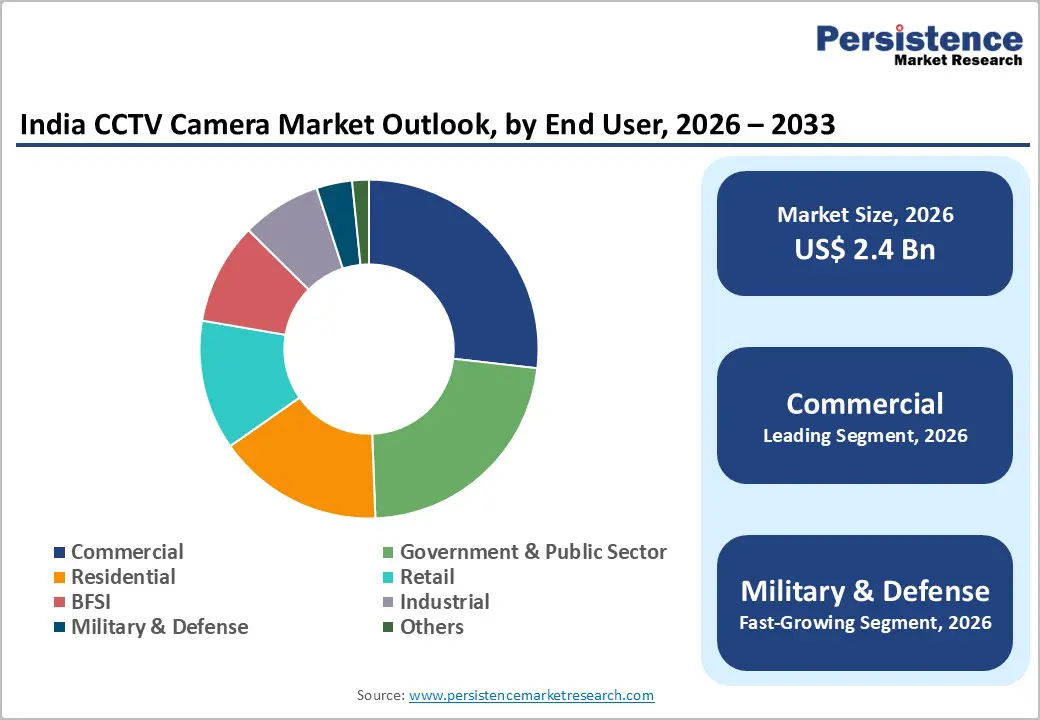

- Commercial end users hold around 26.8% share, whereas military & defense applications are expected to see about 21.3% CAGR, reflecting rising focus on border and critical-infrastructure protection.

| Key Insights | Details |

|---|---|

|

India CCTV Camera Market Size (2026E) |

US$ 2.4 billion |

|

Market Value Forecast (2033F) |

US$ 8.2 billion |

|

Projected Growth CAGR (2026-2033) |

19.1% |

|

Historical Market Growth (2020-2025) |

14.2% |

Market Dynamics Analysis

Drivers - Smart cities, public safety programs, and infrastructure expansion

India’s push for urban safety and smart infrastructure is a primary driver of CCTV camera demand. Under the Smart Cities Mission and state-specific safe-city initiatives, thousands of cameras have been deployed across traffic junctions, metro systems, government buildings, and critical public spaces, with electronic security estimated at about US$1.3 Bn in 2021 and projected to reach near US$4.9 Bn by 2027 at a ~24% CAGR. This sustained pipeline of city-level and transport projects, combined with highway, airport, and rail modernization, is embedding video surveillance as a mandatory layer of infrastructure planning, significantly boosting baseline demand for mid- to high-resolution dome and PTZ cameras.

Transition from analog to IP and AI-enabled surveillance

The India CCTV ecosystem is undergoing a technology transition from legacy analog to IP/network cameras integrated with video management software and analytics. While non-IP (analog/HD) still accounts for around 80% of installed share, IP cameras are growing rapidly due to remote access, PoE support, higher resolutions, and easier integration with IT networks. India’s broader CCTV market is projected to grow at a 18–21% CAGR through 2033, with AI-enabled cameras and analytics-ready endpoints (facial recognition, ANPR/LPR, behavior analytics) expanding at a CAGR above 20%, particularly in commercial, industrial, and smart-city deployments. This transition increases average selling prices and drives recurring revenues for storage, software, and maintenance.

Restraints - Data privacy, regulatory scrutiny, and cybersecurity risks

As deployments scale, concerns regarding data privacy, unauthorized surveillance, and cyber-vulnerable endpoints are intensifying. India’s evolving data-protection and IT security frameworks require enterprises and public agencies to handle video data responsibly, adding compliance complexity and potential legal exposure. Poorly secured IP cameras can serve as attack vectors, while unclear guidelines in certain jurisdictions can delay approvals for large public-area installations, thereby risking project timelines and vendor revenues. These factors may moderate adoption in sensitive environments or raise the cost of compliance-ready solutions.

Supply chain dependence and price competition

The Indian CCTV camera market remains heavily dependent on imported components and finished products, especially from East Asia, exposing it to currency volatility, trade disruptions, and regulatory interventions. High competition from low-cost vendors compresses margins, particularly in analog/HD and entry-level IP segments. Smaller local assemblers can struggle to invest in R&D and certification, potentially limiting domestic value addition and slowing the shift toward higher-spec, cybersecurity-hardened solutions.

Opportunities - Localization, Make-in-India, and cybersecurity-focused offerings

The government's emphasis on domestic electronics manufacturing and on trusted telecom/security equipment creates a strategic opening for local production of CCTV and camera modules. Vendors that invest in Indian manufacturing, secure supply chains, and cybersecurity-certified firmware can target public-sector and critical-infrastructure projects with higher qualification barriers, estimated to represent a sizeable share of the US$8.2 Bn market by 2033. Secure-by-design IP cameras that comply with emerging national standards can command premium pricing and secure long-term service contracts.

Sector-specific solutions for high-growth verticals

Tailored video solutions for retail, logistics, healthcare, education, and defense represent another scalable opportunity. With commercial end users leading adoption (~26–27% share) and defense-related applications projected to grow at a CAGR above 20%, verticalized offerings (POS-integrated retail analytics, yard and warehouse monitoring, hospital compliance, campus safety, and perimeter security) can meaningfully expand revenue per site. These verticals combined can represent several billion dollars of cumulative CCTV and analytics spending over the next decade in India.

Category-wise Analysis

Camera Type Insights

Dome cameras are the leading camera type, holding roughly 32.5% share of the India CCTV camera market by 2026, supported by their discreet aesthetics, vandal-resistance, and versatility across retail, offices, banks, and public buildings. Industry assessments indicate dome formats already account for the largest share of installed CCTV units in India, benefiting from broad availability in analog, HD, and IP variants and a wide range of resolutions. Their ability to blend with ceilings and indoor environments while offering wide-angle coverage underpins continued dominance.

The fastest-growing camera type is fisheye cameras, projected to expand at about 21.1% CAGR between 2026 and 2033, from a relatively small base. Their 360-degree coverage, compatibility with de-warping analytics, and suitability for open layouts such as halls, warehouses, and transport hubs make them attractive for deployments where reducing camera count and blind spots is a priority.

Connectivity Insights

Analog-based solutions, encompassing both wired and wireless analog and HD over coax configurations, account for an estimated 69% share of the Indian CCTV camera market, reflecting the large installed base and cost-effective deployment across legacy surveillance infrastructure. Industry observations indicate analog platforms remain widely adopted due to their operational simplicity, compatibility with existing cabling frameworks, and dependable performance in continuous monitoring environments. Their affordability and ease of installation make them particularly prevalent across residential complexes, small businesses, and established commercial facilities, where upgrading to fully networked architectures is often gradual rather than immediate.

Is the IP or network segment the fastest-growing connectivity type, likely to register around 21.9% CAGR during 2026–2033, as enterprises and city authorities modernize systems to support remote access and AI analytics-IP cameras allow integration with broader IT and IoT ecosystems, simplified scalability, and centralized management, making them the preferred choice for new smart-city phases and greenfield commercial projects.

Functionality Insights

IR/Night Vision cameras lead the functionality segment with approximately 34.2% share, reflecting India’s requirement for round-the-clock monitoring in low-light and outdoor conditions. Most government, transport, and perimeter-security installations specify IR-enabled cameras to maintain visibility during night hours and power-saving regimes. The broad availability of IR features in dome, bullet, and PTZ formats across analog and IP technologies reinforces their central role in deployments.

The ANPR & LPR (Automatic Number Plate / License Plate Recognition) category is the fastest-growing functionality, projected to grow at about 22% CAGR through 2033, driven by traffic enforcement, tolling, parking, and access-control projects. As Indian cities roll out intelligent transport systems and electronic tolling, demand for high-resolution, AI-enabled cameras capable of accurately reading plates under varied conditions is expected to increase sharply.

End-user Insights

The commercial segment (including offices, retail, hospitality, BFSI, logistics, and organized real estate) is the leading end-user group, with an estimated 26.8% share of India’s CCTV camera market in 2026. Rising focus on loss prevention, compliance, and customer analytics is encouraging businesses to deploy higher-resolution cameras integrated with POS and access-control systems. The continued expansion of organized retail, logistics parks, business parks, and co-working spaces ensures robust, recurring demand for scalable surveillance solutions.

The military & defense segment is the fastest-growing end-user category, with an anticipated CAGR of about 21.3% from 2026 to 2033. Border management, critical infrastructure protection, and base security are driving adoption of ruggedized cameras, thermal imaging, and advanced analytics, often integrated with radar and sensor networks to create layered situational awareness.

Regional Market Insights

North India CCTV Camera Market Share and Trends Analysis

North India holds a dominating share of about 31.8% of the Indian CCTV camera market in 2026, driven by dense urban clusters such as Delhi-NCR, Chandigarh tri-city, Lucknow, and Jaipur, and a high concentration of central and state government institutions. Large-scale city surveillance, traffic management, and public-area monitoring projects, supported by Smart Cities Mission funds and state police modernization programs, underpin sustained demand for dome, PTZ, and ANPR-enabled cameras. The region also hosts major corporate headquarters and commercial real estate hubs, further increasing installations.

North India is expected to maintain leadership through 2033 as authorities expand safe-city initiatives, intelligent transport systems, and integrated command-and-control centers. Regulatory focus on women’s safety, crime prevention, and air quality surveillance may widen use cases, while increased scrutiny on data governance and cybersecurity could favor trusted, standards-compliant vendors.

West India CCTV Market Share and Trends Analysis

West India holds about 27.4% share of the India CCTV camera market and is projected to grow at approximately 18.6% CAGR during 2026–2033, supported by strong economic activity in Maharashtra and Gujarat. Metro cities like Mumbai and Pune, along with industrial and port hubs in Gujarat, generate significant demand from commercial complexes, manufacturing plants, warehouses, and transport infrastructure. State-level programs for city surveillance, port and coastal security, and industrial safety further drive camera deployments.

Regulatory harmonization in West India, particularly around building codes, fire and safety norms, and industrial compliance, is expected to encourage standardized CCTV installations across industrial estates and logistics corridors. Investments in smart-port, smart-logistics, and refinery-related monitoring solutions create opportunities for high-spec PTZ, thermal, and explosion-proof cameras.

South India CCTV Camera Market Share and Trends Analysis

South India is witnessing one of the fastest growth trajectories, with the regional CCTV camera market projected to grow at a CAGR of around 19.9% through 2033, driven by a strong existing base. Technology hubs such as Bengaluru, Hyderabad, and Chennai, along with major manufacturing corridors in Tamil Nadu and Karnataka, drive demand for surveillance across IT parks, industrial clusters, and large residential townships. The region’s early adoption of digital and cloud solutions, combined with active state initiatives in urban safety and transport modernization, is accelerating IP camera penetration.

South India’s manufacturing strength in electronics, automotive, and industrial equipment positions it as a potential production and integration hub for CCTV solutions under the Make-in-India initiatives. As states expand smart-city projects and metro rail networks, opportunities for integrated video analytics, ANPR, and platform-screen monitoring systems are expected to grow rapidly.

Competitive Landscape

Leading players in India’s CCTV camera market emphasize innovation-led, IP-centric portfolios, local manufacturing, and close integration with AI analytics and cloud platforms to differentiate beyond price. Key strategies include expanding Make-in-India capacity, tailoring products to smart-city and vertical-specific requirements, and offering full-stack solutions spanning cameras, storage, VMS, and managed services. Emerging models center on recurring revenues from VSaaS, cybersecurity-hardened endpoints, and ecosystem partnerships with telcos, IT integrators, and city authorities.

Strategic Developments

- In January 2024, Hikvision introduced Stealth Edition cameras featuring sleek black housings, integrating ColorVu full color imaging and AcuSense AI for human and vehicle detection. The lineup enhances low-light surveillance accuracy and supports diverse commercial, residential, and infrastructure security applications.

- In June 2025, Honeywell launched its first locally designed and manufactured 50 Series CCTV camera portfolio in India, featuring advanced video analytics, enterprise-grade cybersecurity, and Class 1 Make in India certification, developed in Bengaluru with manufacturing support from VVDN Technologies.

Companies Covered in India CCTV Camera Market

- Hikvision

- Dahua Technology

- CP Plus / Aditya Infotech Ltd

- Honeywell Commercial Security

- Bosch Security Systems

- Panasonic i-PRO / Panasonic Group

- Axis Communications

- Samsung Hanwha Vision

- Godrej Security Solutions

- Sony

- ZICOM Electronic Security Systems

- Infinova

- Pelco

- Matrix Comsec

Frequently Asked Questions

The India CCTV camera market is estimated at about US$2.4 Bn in 2026 and is projected to reach approximately US$8.2 Bn by 2033.

Growth is driven by smart‑city and public‑safety programs, rising commercial and residential security awareness, and the migration from analog to IP and AI‑enabled surveillance solutions.

The India CCTV camera market is expected to grow at around 19.1% CAGR in value between 2026 and 2033.