- Chipsets & Processors

- Processor Market

Processor Market Size, Share, and Growth Forecast 2026 - 2033

Processor Market by Processor Type (Microprocessors (MPU), Graphics Processing Units (GPU), Microcontrollers (MCU), Digital Signal Processors (DSP), Network & Embedded Processors), Architecture Type (CISC Architecture, RISC Architecture, ASIC-Based Processors, Superscalar Processors), Application, End-use, and Regional Analysis, 2026 - 2033

Processor Market Size and Trend Analysis

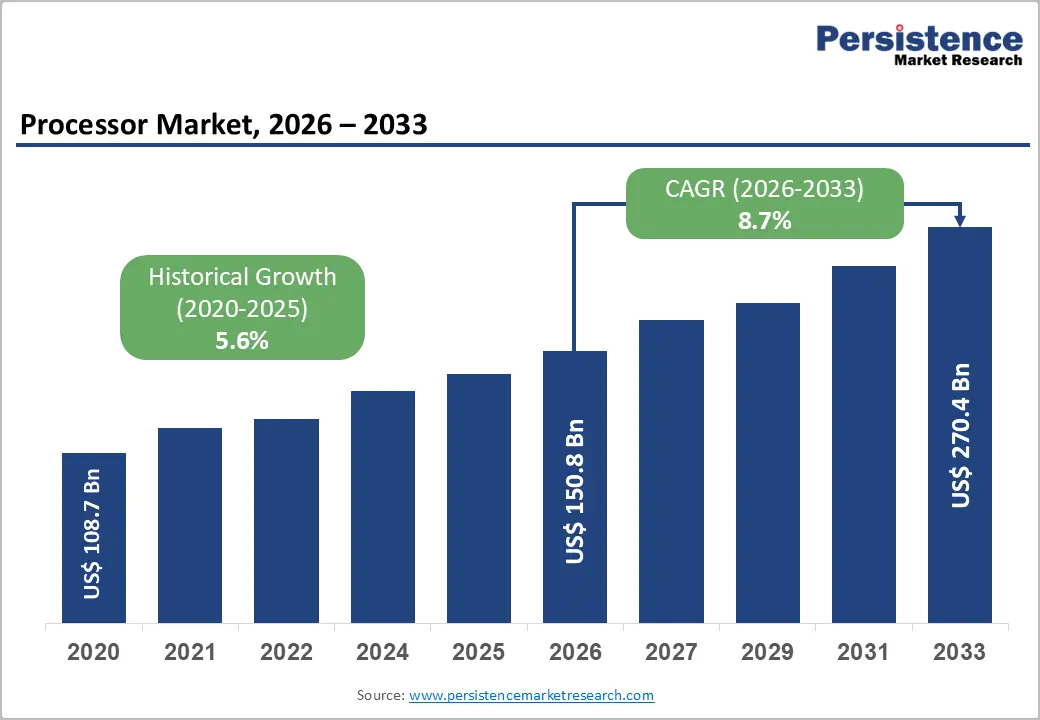

The global processor market is expected to be valued at US$ 150.80 Billion in 2026 and is projected to reach US$ 270.40 Billion by 2033, growing at a CAGR of 8.7% between 2026 and 2033.

Processors are the cornerstone of the digital economy, powering devices ranging from smartphones and personal computers to data centers, automotive systems, and AI infrastructure. Their market growth is driven by rising demand for high-performance computing, cloud services, artificial intelligence, and edge computing applications, alongside continuous advancements in semiconductor manufacturing technologies and processor architectures.

Key Industry Highlights:

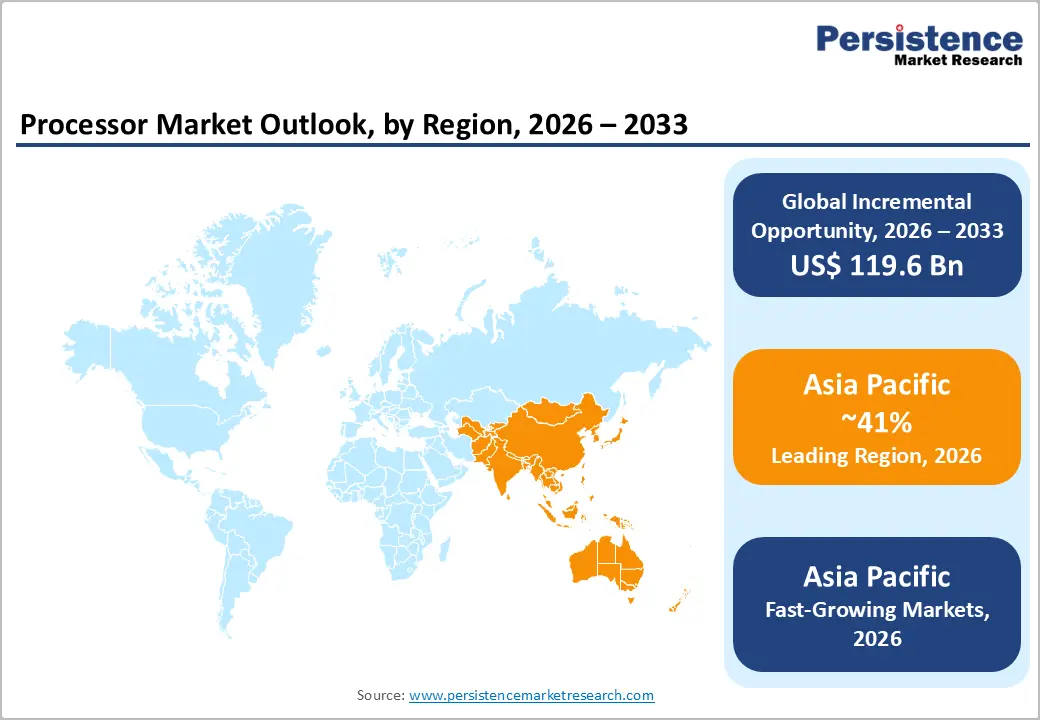

- Leading Region: Asia Pacific accounts for 41% of global processor market revenue in 2026, reaching US$ 61.83 billion. Strong semiconductor investments, including Samsung’s US$ 230 billion fabrication plan and expanding AI and data center infrastructure across China, India, and Southeast Asia, are expected to drive a 9.8% CAGR in the forecast period.

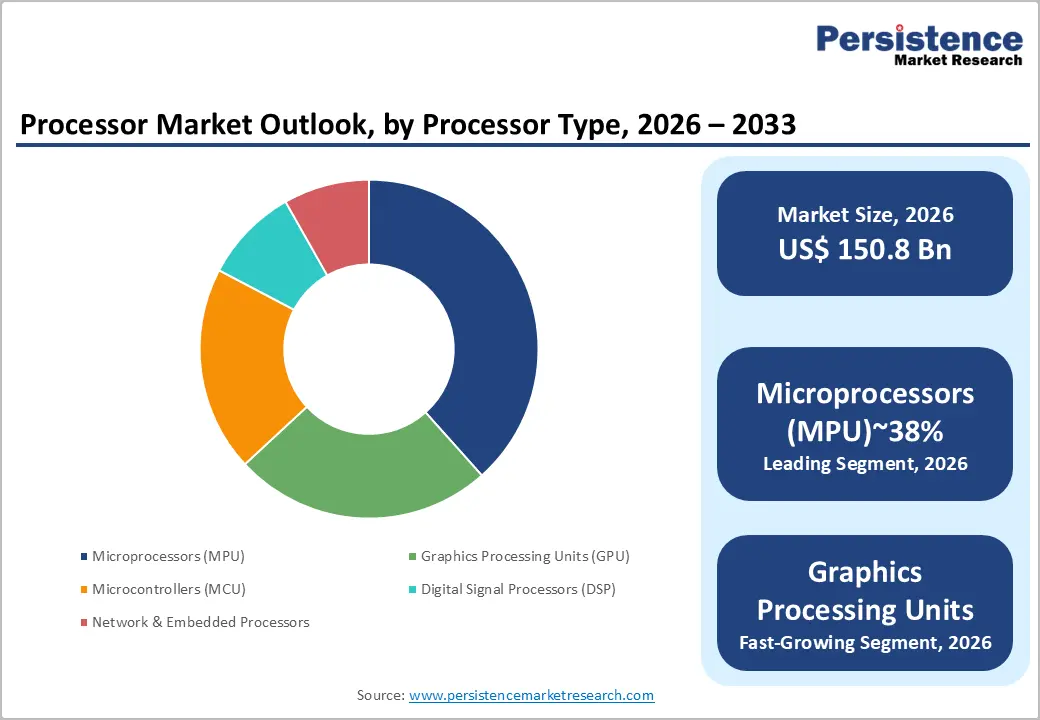

- Leading Segment: Microprocessors (MPUs) hold a 38.0% market share, valued at US$ 57.30 billion in 2026. Their dominance is supported by broad compatibility with existing enterprise software, making migration to alternative architectures costly and reinforcing long-term demand.

- Fastest Growing Segment: RISC architecture is the fastest-growing segment, driven by the success of processors such as Apple’s M4 and Amazon’s Graviton4. Superior performance-per-watt and lower operating costs are encouraging wider adoption in cloud computing and AI workloads.

- Key Opportunity: Government-backed semiconductor initiatives, including India’s INR 76,000 crore Semicon India programme and the European Chips Act, are accelerating investments in domestic chip production and AI infrastructure, creating long-term growth opportunities for processor manufacturers and designers.

Market Dynamics

Drivers - Accelerating AI Infrastructure Build-Out Demanding Specialised Processor Architectures

Hyperscale cloud operators and enterprise IT teams now treat processor procurement as a board-level capital allocation decision, because a single AI training cluster can consume several hundred million dollars in silicon alone. The U.S. Department of Energy's Exascale Computing Project, which achieved full deployment of the Frontier supercomputer at Oak Ridge National Laboratory in 2023, demonstrated that purpose-built processor architectures can deliver more than 1.1 exaFLOPS of performance, setting a benchmark that has triggered analogous national-scale procurement programmes across the European High Performance Computing Joint Undertaking (EuroHPC JU). Over the next two to three years, this dynamic will force incumbent CPU suppliers to either co-design tightly integrated processor-memory packages or cede workload-specific revenue to fabless specialists.

Automotive Electrification and ADAS Mandates Creating Durable Embedded Processor Demand

Automotive OEMs now source an average of US$ 600–900 in semiconductor content per vehicle for battery-electric platforms versus roughly US$ 300–350 for comparable internal combustion equivalents, according to estimates from the Semiconductor Industry Association (SIA).

The European Union's General Safety Regulation (EU) 2019/2144, which mandated advanced driver-assistance systems, including emergency lane-keeping and intelligent speed assistance on all new vehicle types sold in the EU from July 2024, is directly translating into multi-year embedded processor supply agreements between Tier-1 automotive suppliers and semiconductor vendors. Processor suppliers that secure design-win pipelines with automotive OEMs before 2026 will enjoy six-to-eight-year revenue visibility given typical automotive platform lifecycles.

Restraints - Geopolitical Export Controls Creating Supply Chain Fragmentation and Rising Costs

The U.S. Bureau of Industry and Security (BIS) expanded its semiconductor export control framework in October 2023, extending licensing requirements to advanced AI processors, including specific performance thresholds for chips destined for more than 40 countries, which has forced chip designers to develop market-specific product variants that add 12–18 months to development cycles and erode gross margin through duplicated engineering costs. For new entrants without established multi-geography supply chains, clearing these compliance requirements represents a structural barrier that incumbents with dedicated export control legal teams can absorb far more efficiently.

Advanced Node Fabrication Costs Compressing Return on R&D Investment

Tooling and process development costs at the 3nm and 2nm nodes have grown to an estimated US$ 20 Billion or more per new fabrication facility, according to data cited in the Taiwan Semiconductor Manufacturing Company (TSMC) 2023 Annual Report, creating a situation where only a handful of global buyers can anchor a new leading-edge fab economically. Fabless chip designers without guaranteed wafer allocations face both long lead times and spot-pricing volatility that can add 15% to chip bill-of-materials costs during supply-constrained cycles, directly compressing the margins of mid-tier processor vendors.

Opportunities - Edge AI Processor Deployment Across Industrial and IoT Devices

Semiconductor IP licensors and fabless designers should accelerate investment in ultra-low-power AI inference processors optimised for edge deployment, where on-device processing eliminates cloud-round-trip latency and addresses data-sovereignty concerns for industrial operators.

Arm Holdings launched its Cortex-X925 and updated Ethos-U85 neural processing unit IP in 2024, specifically targeting edge AI inference workloads in industrial automation and smart-grid metering, validating commercial timing for this segment. For this opportunity to fully materialise, the ecosystem of edge MLOps toolchains and standardised hardware security frameworks must reach sufficient maturity to satisfy procurement requirements of regulated-sector industrial buyers.

Sovereign AI Chip Programmes Opening New Government-Funded Processor Demand

Government procurement teams and national development banks represent a newly addressable buyer class that did not exist at scale before 2023, offering processor vendors long-cycle, non-cyclical revenue streams anchored by national strategic priorities.

India's Semicon India programme, which allocated 76,000 Crore to semiconductor design, fabrication, and packaging under the Modified Semiconductor and Display Fab Scheme (2023), is driving domestic processor design-house formation and preferential procurement commitments. Specialist fabless AI chip designers and established IDMs with proven domestic-content capabilities are best positioned to capture this opportunity, provided they can demonstrate technology transfer and local employment outcomes that satisfy government co-investment criteria.

Category-wise Analysis

Processor Type Insights

Microprocessors (MPUs) account for 38.0% of the global processor market in 2026, valued at US$57.30 billion, due to their critical role across laptops, desktops, industrial systems, and enterprise servers. PC manufacturers using Intel’s 14th-generation Core Ultra processors and enterprises operating x86-based servers continue to rely heavily on MPUs because of long-standing software compatibility and stable performance.

According to the World Semiconductor Trade Statistics (WSTS) organisation, microprocessors remain the largest category within the logic semiconductor segment, supporting strong demand for both x86 and ARM-based MPU vendors globally.

GPUs are the fastest-growing processor type, driven by rising demand for high-performance parallel computing in AI model training and inference workloads. NVIDIA’s H100 Tensor Core GPU, launched in 2022, became the preferred choice for advanced AI training across hyperscalers such as Microsoft Azure and Google Cloud. This success has encouraged wider GPU adoption by research institutes and enterprises globally. Over the 2026–2033 forecast period, increasing deployment of AI inference at edge locations and telecom infrastructure will further expand GPU demand beyond large hyperscale data centres.

Architecture Type Insights

CISC architecture is likely to account for 41.0% of the global processor market in 2026, reaching US$61.83 billion, supported by the widespread use of x86-compatible systems in enterprise IT, cloud infrastructure, and personal computers. Businesses operating Microsoft Windows Server environments and virtualised cloud clusters continue choosing AMD EPYC and Intel Xeon processors because of their ability to run complex instruction sets efficiently without software redesign. AMD’s growing share in the server CPU market, reaching nearly 24% of x86 server shipments by late 2024, highlights the continued commercial strength of CISC-based processors.

RISC Architecture is the fast-growing segment, mainly driven by the increasing adoption of ARM-based processors in smartphones, tablets, and energy-efficient cloud infrastructure. Apple’s M-series chips, from the M1 to the M4, launched in 2024, proved that RISC processors can deliver excellent performance while consuming less power. This encouraged cloud companies such as Amazon Web Services to expand the deployment of Graviton4 processors in EC2 instances. Growing focus on energy savings and lower operating costs will continue accelerating the shift toward RISC-based architectures during the forecast period.

Application Insights

Smartphones & Tablets account for 31% of the global processor market in 2026, valued at US$46.75 billion, supported by regular smartphone upgrade cycles and growing demand for on-device AI capabilities. Qualcomm’s Snapdragon 8 Gen 3 platform introduced advanced AI processing features, including real-time translation, AI-powered photography, and generative AI applications directly on smartphones. According to the GSM Association (GSMA), global mobile subscribers exceeded 5.6 billion in 2024, creating a large and recurring demand base for mobile processors despite changing economic conditions across different regions.

Servers & Data Centers are the fastest-growing application segment in the processor market, driven by large investments in AI infrastructure from hyperscale cloud providers. Microsoft announced plans to invest US$ 80 Billion in AI-focused data centres during fiscal year 2025, with a major share allocated to advanced processor procurement. Rising AI adoption is increasing demand for high-performance chips across training and inference applications. Additionally, sovereign AI projects in regions such as India, Southeast Asia, and the Middle East will diversify future processor demand beyond U.S.-based hyperscale companies.

End-use Insights

Consumer Electronics account for 39.0% of the global processor market in 2026, reaching US$ 58.81 Billion, supported by the rapid adoption of AI-enabled devices such as gaming consoles, smart TVs, wearables, and home automation systems. Sony’s PlayStation 5, powered by AMD’s custom Zen 2/RDNA 2 processor built by TSMC, demonstrated the growing importance of integrated CPU-GPU designs in consumer devices. The Consumer Technology Association (CTA) projected U.S. consumer technology retail revenue at US$512 billion in 2024, reinforcing the segment’s strong contribution to processor demand worldwide.

IT & Telecommunications is the fastest-growing end-use segment in the processor market, driven by ongoing 5G network expansion and increasing deployment of cloud-based telecom infrastructure. Ericsson’s Cloud RAN deployments in 2024 relied on commercial off-the-shelf processors running virtualised network functions, replacing traditional proprietary hardware systems. This shift is significantly increasing processor usage across telecom networks. Furthermore, ongoing 6G development under the International Telecommunication Union (ITU) IMT-2030 framework is expected to create additional demand for advanced signal processing chips and next-generation telecom processors.

Regional Insights

North America Processor Market Trends and Insights

North America accounts for 27.0% of the global processor market in 2026, representing US$ 40.72 Billion, with its position anchored by the concentration of hyperscale data centre operators, fabless chip designers, and federally funded semiconductor research programmes within the region. The CHIPS and Science Act (2022) has catalysed more than US$ 200 billion in private semiconductor investment commitments across the U.S. through 2025, per the Semiconductor Industry Association, reshaping the domestic processor manufacturing and design ecosystem. North America will increasingly serve as both the primary market for frontier AI processor consumption and the origination point for next-generation chip architectures through the forecast period.

- United States Processor Market Size

The United States commands an estimated 88% share of the North America processor market, approximately US$ 35.83 Billion in 2026, driven by hyperscale cloud capital expenditure from operators including Amazon Web Services, Google, and Meta, each of which has publicly committed multi-year, multi-billion-dollar processor procurement and custom silicon development programmes. The ongoing commercialisation of U.S. Department of Defense edge AI applications requiring radiation-hardened and export-controlled processor designs will provide a durable non-cyclical demand layer in the forecast period.

Europe Processor Market Trends and Insights

Europe accounts for 18.0% of the global processor market in 2026, representing US$ 27.14 Billion, with demand shaped by the European Chips Act (2023), which targets doubling Europe's share of global semiconductor production to 20% by 2030 and has already triggered TSMC's commitment to build a €10 Billion fab in Dresden, Germany. Industrial automation, automotive ADAS, and energy transition applications collectively drive the majority of European processor procurement, distinguishing the region's demand profile from the consumer-electronics-heavy mix seen in Asia Pacific. Regulatory pressure from the EU AI Act (2024) will further accelerate demand for compliant, auditable edge AI processors in critical infrastructure applications.

- Germany Processor Market Size

Germany holds an estimated 28% share of the European processor market, approximately US$ 7.60 Billion in 2026, underpinned by the country's dominant automotive manufacturing sector, where Volkswagen Group's software-defined vehicle platform VW.OS requires deeply integrated automotive processors across powertrain, infotainment, and safety domains. The expected ramp of TSMC's Dresden fab from 2027 will progressively shift Germany from a processor-importing to a processor-producing economy, creating supply chain advantages for locally headquartered automotive and industrial buyers.

- United Kingdom Processor Market Size

The United Kingdom represents approximately 18% of Europe's processor market, roughly US$ 4.89 Billion in 2026, with demand concentrated in financial services data centre infrastructure, aerospace and defence computing, and a growing AI research ecosystem anchored by institutions including the Alan Turing Institute. The UK Semiconductor Strategy (2023), which allocated £200 Million toward chip design capability and supply chain resilience, is nurturing a domestic fabless design community that will generate incremental processor IP licensing and procurement activity over the medium term.

- France Processor Market Size

France accounts for an estimated 14% of the European processor market, approximately US$ 3.80 Billion in 2026, supported by STMicroelectronics' strong position in automotive and industrial microcontroller supply, and by the French government's France 2030 investment plan, which earmarked €5 Billion for electronics and semiconductor-adjacent industries. Expansion of France's nuclear energy infrastructure and smart-grid digitalisation under Électricité de France (EDF) programmes will generate sustained demand for industrial-grade embedded processors through the forecast period.

Asia Pacific Processor Market Trends and Insights

Asia Pacific accounts for 41.0% of the global processor market in 2026, representing US$ 61.83 Billion, and is the fastest-growing region at a projected CAGR of 9.8%, powered by semiconductor manufacturing concentration in Taiwan and South Korea, mass-market consumer electronics production in China, and rapidly scaling data centre investment across India and Southeast Asia. Samsung Electronics' US$ 230 Billion semiconductor investment roadmap through 2042, announced in 2023, anchors the region's fabrication capacity expansion trajectory across leading-edge logic and memory processes. Asia Pacific's dual role as both the world's primary processor manufacturing hub and its largest consumer electronics market creates compounding demand density that no other region can replicate over the forecast horizon.

- China Processor Market Size

China represents an estimated 42% of Asia Pacific's processor market, approximately US$ 25.97 Billion in 2026, driven by domestic smartphone OEM production volumes from Xiaomi, OPPO, and Vivo, and by the Chinese government's "New Infrastructure" initiative directing state capital into data centres, 5G base stations, and AI computing clusters. Export restrictions imposed under the U.S. Entity List have accelerated investment in domestic processor design champions, including HiSilicon and Cambricon, creating a parallel supply ecosystem that will increasingly compete on domestic procurement share in the forecast period.

- India Processor Market Size

India accounts for an estimated 11% of Asia Pacific's processor market, approximately US$6.80 billion in 2026, with demand acceleration tied to smartphone assembly localisation under the Production Linked Incentive (PLI) scheme for Large-Scale Electronics Manufacturing, which attracted Apple's contract manufacturers Foxconn and Tata Electronics to expand Indian assembly operations from 2023 onward. India's rapidly growing data centre sector, forecast by JLL to add more than 1,700 MW of capacity by 2026, will generate proportionally significant processor procurement in the server and networking segment.

- Japan Processor Market Size

Japan holds approximately 17% of Asia Pacific's processor market, roughly US$ 10.51 Billion in 2026, underpinned by Sony Semiconductor Solutions' dominant position in image sensor processors and Renesas Electronics' leadership in automotive microcontrollers supplying Japan's domestic OEM base. The establishment of Rapidus, a government-backed semiconductor venture targeting 2nm logic production by 2027 with IBM process technology partnerships, signals Japan's strategic intent to recapture advanced processor manufacturing capability and will create additional domestic demand anchors through the latter half of the forecast period.

Competitive Landscape

The global processor market operates as a tiered oligopoly at the leading edge, with Intel, NVIDIA, and AMD collectively controlling the majority of high-performance CPU and GPU revenue, while Qualcomm and MediaTek dominate mobile application processor volumes. Competition pivots on three axes: process node access through TSMC and Samsung Foundry, proprietary architecture IP, and software ecosystem lock-in.

Tenstorrent, backed by Hyundai and other strategic investors, represents the most consequential disruptive entrant, deploying open-architecture AI processors that challenge the proprietary software moat strategy of established players. Winners are separating from laggards by internalising full-stack silicon-software co-design capability rather than treating chip and software development as independent workstreams.

Key Developments:

- January, 2025: NVIDIA launched its Blackwell Ultra GB300 architecture, delivering enhanced transformer-engine performance for large-language-model inference workloads, with initial allocations directed to hyperscale customers, including Oracle Cloud Infrastructure.

- March, 2025: Intel completed the organisational separation of its foundry business into a standalone subsidiary structure, a restructuring move designed to attract third-party fabless customers by removing competitive conflict concerns and improving cost transparency.

- November, 2024: Qualcomm unveiled the Snapdragon X Elite platform's enterprise laptop expansion, with Microsoft certifying the ARM-based chip for Copilot+ PC compatibility, accelerating RISC architecture penetration into the commercial PC procurement channel.

Companies Covered in Processor Market

- Intel

- Advanced Micro Devices

- NVIDIA

- Qualcomm

- Samsung Electronics

- Taiwan Semiconductor Manufacturing Company

- Apple

- MediaTek

- Broadcom

- Arm Holdings

- Micron Technology

- SK Hynix

- Texas Instruments

- NXP Semiconductors

- Marvell Technology

- Renesas Electronics

- STMicroelectronics

- HiSilicon

- Cambricon Technologies

- Tenstorrent

- Amazon Web Services

- Rapidus

Frequently Asked Questions

The global processor market is valued at US$ 150.80 Billion in 2026 and is projected to reach US$ 270.40 Billion by 2033, advancing at a CAGR of 8.7%. The primary growth catalyst is the intersection of generative AI infrastructure build-out and sovereign semiconductor policy programmes, which are simultaneously expanding processor demand volumes and diversifying the geographic base of fabrication investment.

Two structural forces dominate: the 5G network densification mandate under the ITU IMT-2020 framework is driving telecom-grade network processor procurement at every radio access node, while the proliferation of edge AI inference applications is pulling demand for ultra-low-power embedded processors into industrial and consumer IoT deployments that did not previously require dedicated processing silicon. Both drivers operate independently of general IT spending cycles, providing durable demand support even during macroeconomic slowdowns.

Microprocessors (MPU) hold the largest segment share at 38.0% in 2026, because decades of enterprise software written for x86-compatible instruction sets make architectural migration economically and operationally prohibitive for the majority of corporate IT buyers. This software compatibility moat provides competitive stability for dominant MPU vendors, though the medium-term risk is gradual workload migration toward RISC-based alternatives for greenfield cloud-native deployments where legacy software dependencies do not apply.

Asia Pacific leads with 41.0% of global processor market revenue in 2026, driven by two structural factors: its concentration of advanced semiconductor fabrication capacity, notably TSMC's leading-edge fabs in Taiwan and Samsung's in South Korea, and its status as the world's largest consumer electronics assembly and consumption geography. Looking forward, the addition of India's semiconductor manufacturing ambitions under the Modified Semiconductor and Display Fab Scheme will deepen Asia Pacific's structural advantages and sustain its fastest-growing regional CAGR of 9.8% in the forecast period.

The largest opportunity lies in purpose-built AI inference processors for sovereign and enterprise edge deployments, where on-device computation requirements are growing faster than centralised cloud capacity can economically serve. Fabless chip designers with proprietary low-power inference architectures and compliance with NIST's AI Risk Management Framework (2023) are best positioned to capture this opportunity, provided they can demonstrate reliable supply chain independence from geopolitically constrained fabrication nodes.

NVIDIA, Intel, AMD, Qualcomm, and MediaTek collectively anchor the competitive landscape, with rivalry intensifying as cloud hyperscalers including Google and Amazon Web Services develop proprietary in-house silicon that displaces third-party procurement at the margin. Competition is primarily fought on performance-per-watt efficiency, software ecosystem depth, and foundry access rather than price alone, a multi-dimensional competitive basis that makes market share displacement a slow process and rewards incumbents with established developer toolchain ecosystems.