- Food Ingredients & Additives

- U.S. High-Intensity Sweeteners Market

U.S. High-Intensity Sweeteners Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

U.S. High-Intensity Sweeteners Market By Product Type (Saccharin, Aspartame, Sucralose, Stevia, Ace-K, Monk Fruit, Neotame, Others), Nature (Artificial, Natural), Application (Food, Beverage, Healthcare & Personal Care, Others), and Regional Analysis, 2026 - 2033

U.S. High-intensity Sweeteners Market Share and Trends Analysis

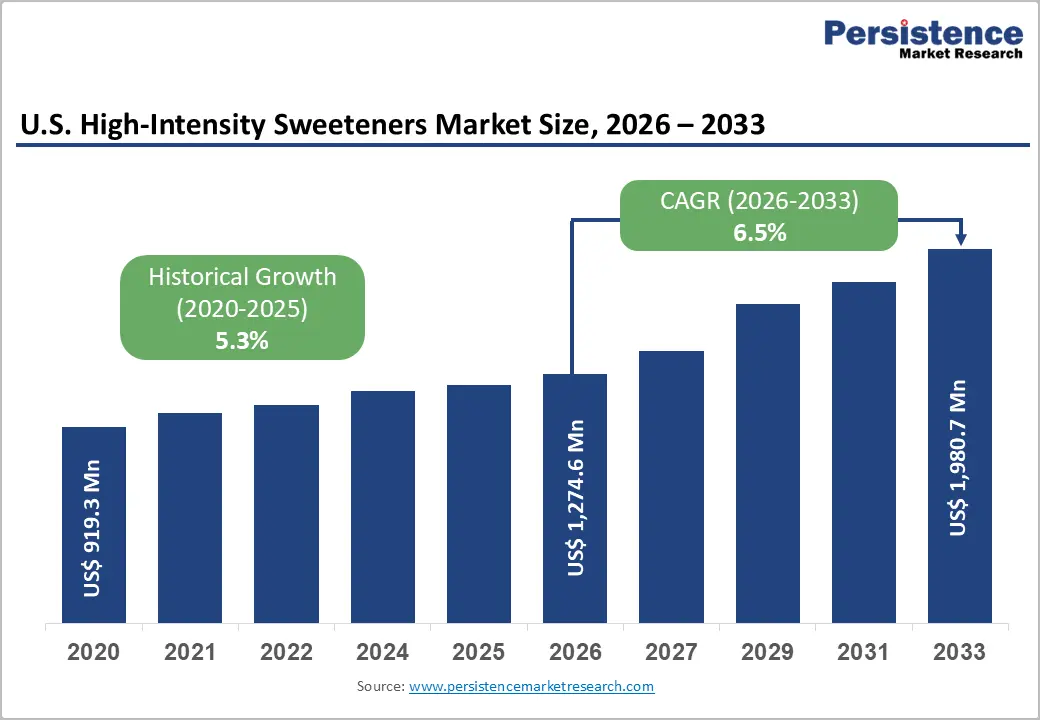

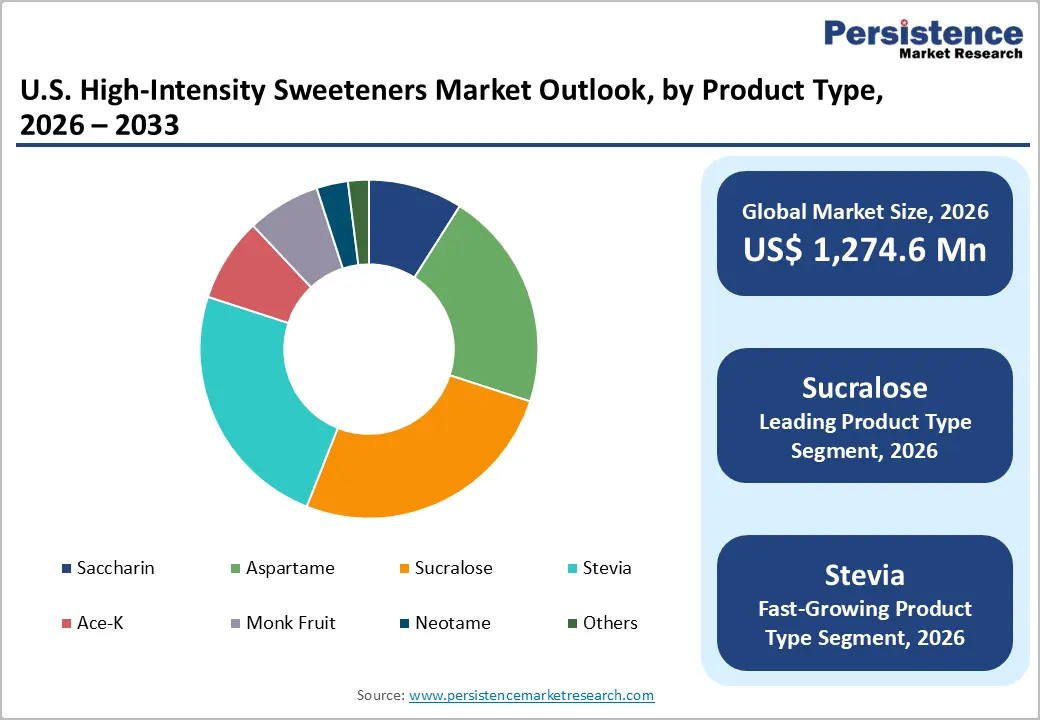

The U.S. High-intensity sweeteners market is estimated to grow from US$ 1,274.6 million in 2026 to US$ 1,980.7 million and is projected to record a CAGR of 6.5% during the forecast period from 2026 to 2033. It is witnessing a strong transformation as consumers increasingly prioritize reduced-sugar diets, calorie control, and clean-label nutrition. Growing awareness regarding obesity, diabetes, and excessive sugar consumption is encouraging food and beverage manufacturers to accelerate the adoption of advanced sweetening technologies.

Demand for plant-based, low-calorie, and diabetic-friendly sweeteners is reshaping product development strategies across beverages, dairy products, nutritional supplements, and processed foods. Technological advancements in fermentation, glycoside extraction, and flavor-masking solutions are significantly improving taste profiles and product acceptance.

Key Industry Highlights:

- Fast-Growing Product Type Segment: Stevia, projected to grow at a CAGR of 8.2% during the forecast period, driven by rising demand for natural, plant-based, low-calorie, and clean-label sweetening solutions.

- Fast-Growing Application Segment: Healthcare & Personal Care, expected to grow at a CAGR of 7.6%, supported by increasing use of sugar-free formulations across nutraceuticals, oral care products, supplements, and wellness applications.

- Growth Indicators: Growing prevalence of obesity and diabetes is accelerating adoption of high-intensity sweeteners as consumers increasingly seek healthier sugar alternatives with lower calorie content and reduced glycemic impact.

- Consumer Trends: Consumers are increasingly preferring natural sweeteners, keto-friendly products, diabetic-safe formulations, clean-label ingredients, and minimally processed food and beverage products aligned with wellness-focused lifestyles.

- Opportunities: Strategic collaborations for co-developing innovative sugar alternatives are emerging as major growth opportunities in the U.S. High-Intensity Sweeteners market.

Market Dynamics

Driver: Rising Health Concerns Linked to Obesity and Diabetes Boost Sweetener Adoption

Escalating rates of diabetes and obesity across the United States are significantly driving demand for high-intensity sweeteners as consumers seek healthier sugar alternatives. According to the Centers for Disease Control and Prevention (CDC), more than 37 million people in the U.S. are living with diabetes, while nearly 100 million individuals are considered prediabetic. Growing public awareness regarding the health risks associated with excessive sugar consumption is encouraging consumers to adopt low-calorie and reduced-sugar dietary choices.

This health-driven shift is increasing the use of high-intensity sweeteners such as stevia, aspartame, and saccharin across beverages, bakery products, dairy items, and dietary supplements. These sweeteners provide sweetness with minimal calories and limited impact on blood glucose levels, making them suitable for diabetic and weight-conscious consumers. Rising healthcare awareness campaigns, preventive nutrition trends, and demand for healthier processed foods are further accelerating growth in the U.S. high-intensity sweeteners market.

Restraint: Bitter Aftertaste Challenges Consumer Acceptance

Although high-intensity sweeteners support sugar reduction and calorie control, consumer dissatisfaction with lingering bitter or artificial aftertastes remains a major market restraint. Sweeteners such as aspartame, saccharin, and sucralose are often associated with taste profiles that differ from traditional sugar, limiting acceptance among some consumers. While these ingredients offer high sweetness intensity with low or zero calories, maintaining sugar-like taste perception continues to be a formulation challenge for manufacturers.

To improve flavor quality, companies are increasingly adopting blended sweetener systems and natural alternatives such as stevia to reduce bitterness and enhance mouthfeel. However, natural sweeteners and advanced formulations can increase production costs and create pricing pressures. Consumer sensitivity toward bitterness also varies significantly, making it difficult for brands to develop universally accepted reduced-sugar products across beverages, dairy, confectionery, and processed food categories.

Opportunity: Collaborative Partnerships to Co-develop Products with Sugar Alternatives

Collaborative partnerships are emerging as a key opportunity in the U.S. high-intensity sweeteners market, allowing companies to develop innovative products using natural sugar substitutes. A notable example is the August 2024 collaboration between Ajinomoto Health & Nutrition North America (AHN) and Shiru, aimed at using AI-powered protein discovery and fermentation to develop sweet proteins for use in beverages and specialty foods. This collaboration aims to produce natural sweeteners from fruits and berries near the equator, responding to the consumer demand for clean-label, minimally processed ingredients.

By combining resources, the two companies can quickly develop healthier alternatives to traditional sugars that align with the preference for natural ingredients and sustainability. These partnerships help expand market reach and introduce unique products that stand out in a competitive landscape. By offering alternatives that mimic sugar's taste and texture, these efforts are well-positioned to meet the rising demand for natural and sustainable products in the sweeteners market.

Category-wise Analysis

By Product Type Insights

Stevia is expected to grow at a CAGR of 8.2% during the forecast period from 2026 to 2033, driven by rising consumer preference for natural and low-calorie sweetening solutions in the United States. Increasing health concerns related to obesity, diabetes, and excessive sugar intake are encouraging consumers to shift toward plant-based sugar alternatives. Derived from the stevia rebaudiana plant, stevia offers sweetness without calories, making it highly attractive among health-conscious consumers.

According to a 2023 study by the International Food Information Council, 73% of U.S.-based consumers expressed interest in natural sweeteners, reflecting growing demand for clean-label and minimally processed ingredients. Food and beverage manufacturers are increasingly reformulating products with stevia to align with evolving wellness trends and vegan-friendly preferences. Advancements in extraction and formulation technologies have also improved stevia’s taste profile, reducing bitterness and increasing acceptance across beverages, dairy, confectionery, and nutritional products.

By Application Insights

Healthcare & personal care is expected to reveal a CAGR 7.6% during the forecast period driven by the growing demand for sugar-free formulations across nutritional, pharmaceutical, and wellness applications. Rising health awareness and growing concerns regarding obesity, diabetes, and calorie intake are encouraging manufacturers to incorporate high-intensity sweeteners into syrups, chewable supplements, protein powders, oral care products, and medicated formulations. These sweeteners help maintain palatable taste profiles while supporting reduced-sugar and low-calorie product positioning.

Growth is further supported by expanding consumer preference for wellness-oriented and clean-label personal care products. Manufacturers are increasingly using plant-based sweeteners such as stevia in toothpaste, mouth fresheners, nutraceuticals, and health supplements targeting diabetic and fitness-conscious consumers. Product innovation, improved sweetener stability, and advancements in flavor-masking technologies are also strengthening adoption across healthcare and personal care applications throughout the U.S.

Competitive Landscape

The U.S. high-intensity sweeteners market is highly competitive, with manufacturers focusing on advanced sugar alternatives that deliver improved taste, stability, and health-focused functionality. Companies are investing in enzymatic refinement, fermentation-based production, and glycoside extraction technologies to enhance the purity, scalability, and flavor performance of plant-based sweeteners. Growing demand across beverages, dairy products, bakery items, and processed foods is accelerating innovation in blended sweetener formulations designed to reduce bitterness and improve sugar-like mouthfeel.

Market participants are increasingly aligning product strategies with clean-label preferences, transparent ingredient labeling, and wellness-oriented dietary trends such as keto-friendly and diabetic-safe formulations. Domestic sourcing initiatives and vertically integrated production models are also gaining traction to improve supply consistency and reduce operational costs. Strategic collaborations, sustainable production practices, and diversified product portfolios are further strengthening competition within the evolving U.S. high-intensity sweeteners market.

Key Industry Developments:

- In March 2026, Arzeda and MANE partnered to commercialize next-generation stevia solutions at scale, supporting cleaner-label and better-tasting sweetening applications for food and beverage manufacturers.

- In February 2026, Tate & Lyle and Manus launched a premium stevia-derived sweetener under the Yume brand, delivering a sugar-like taste profile and marking the first product from The Sweetener Alliance.

- In April 2025, Ingredion became the first company to achieve FSA Silver for 100% of its High-Intensity Sweeteners supply chain, verified by an external audit, the only globally recognized third-party verified supply chain in this category.

U.S. High-Intensity Sweeteners Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 919.3 Mn |

|

Projected Market Value (2026) |

US$ 1,274.6 Mn |

|

Projected Market Value (2033) |

US$ 1,980.7 Mn |

|

CAGR (2026-2033) |

6.5% |

|

Dominant Application |

Beverages, 39% share |

|

Top-ranking Product Type |

Sucralose, 27% share |

|

Incremental Opportunity |

US$ 706.1 Mn |

Companies Covered in U.S. High-Intensity Sweeteners Market

- IFF

- ADM

- Cargill, Inc.

- Ingredion

- Tate & Lyle

- Ajinomoto Co., Inc.

- Roquette

- Sweegen

- GLG Life Tech Corp.

- Pyure Brands LLC

- B&G Foods, Inc.

- Whole Earth Brands

- Heartland Food Products Group

- Others

Frequently Asked Questions

The U.S. High-Intensity Sweeteners market is projected to be valued at US$ 1,274.6 Mn in 2026.

Rising Health Concerns Linked to Obesity and Diabetes Boost Sweetener Adoption is driving the U.S. High-Intensity Sweeteners market.

The U.S. High-Intensity Sweeteners market is poised to witness a CAGR of 6.5% between 2026 and 2033.

Strategic collaborations for co-developing innovative sugar alternatives are emerging as major growth opportunities in the U.S. High-Intensity Sweeteners market.

IFF, ADM, Cargill, Inc., Ingredion, Tate & Lyle, Ajinomoto Co., Inc., and Roquette