- Aerospace & Defense

- U.S. Surveillance Drone Market

U.S. Surveillance Drone Market Size, Share, and Growth Forecast, 2026 - 2033

U.S. Surveillance Drone Market by Platform Type (Fixed Wing, Multi-Rotor, Single-Rotor, Hybrid), Mode of Operation (Remotely Piloted, Semi-Autonomous, Fully Autonomous), Application (Critical Infrastructure & Industrial Inspection, Border & Coastal Surveillance, Law Enforcement & Public Safety, Environmental & Wildlife Monitoring, Disaster Response & Emergency Management, Others) Analysis for 2026 - 2033

U.S. Surveillance Drone Market Size and Trends Analysis

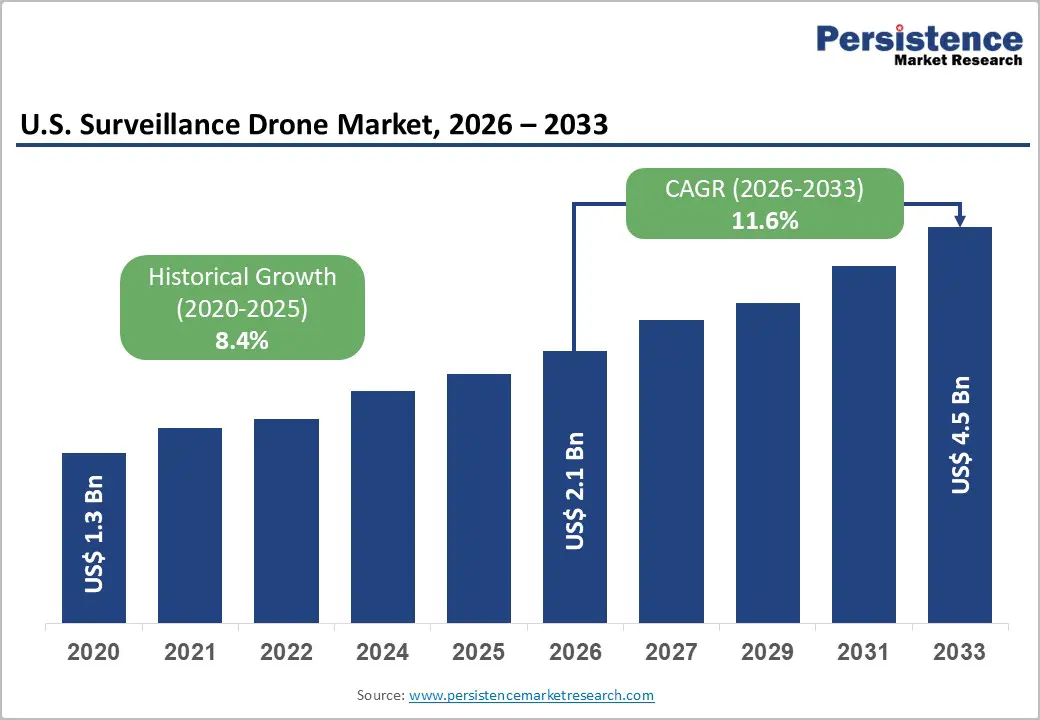

The U.S. Surveillance Drone Market size is projected to rise from US$2.1 billion in 2026 to US$4.5 billion by 2033. It is anticipated to witness a CAGR of 11.6% during the forecast period from 2026 to 2033. The market is being propelled by a confluence of escalating homeland security imperatives, rapid advancements in artificial intelligence-integrated unmanned aerial systems, and expanding public safety and critical infrastructure inspection mandates.

The U.S. Department of Defense directed $9.8 billion toward autonomous and unmanned systems in fiscal year 2026, marking a significant expansion in advanced surveillance and AI-enabled platforms. Total IT spending reached $66 billion, a $1.8 billion increase from 2025, with every service branch boosting AI allocations, including the Navy’s $308 million increase, reflecting the Pentagon’s growing focus on smarter, faster, and more autonomous defense technologies.

Key Industry Highlights:

- Leading Platform Type: Fixed-wing drones capture over 52% market share in 2026, valued at more than US$ 1.1 Bn, driven by the need for long-range monitoring, persistent aerial coverage, and the ability to carry heavier sensors such as LiDAR and high-resolution cameras. Hybrid drones are emerging fast due to their dual power systems and VTOL capability, addressing long-duration surveillance in confined or remote areas.

- Leading Mode of Operation: Remotely piloted drones hold over 55% market share in 2026, valued at more than US$ 1.2 Bn, combining human decision-making with automated systems for critical operations like border surveillance and disaster response. Fully autonomous drones are the fastest-growing segment, expected to rise at a CAGR of 15.4%, driven by demand for continuous monitoring, AI-driven analytics, and reduced operator involvement.

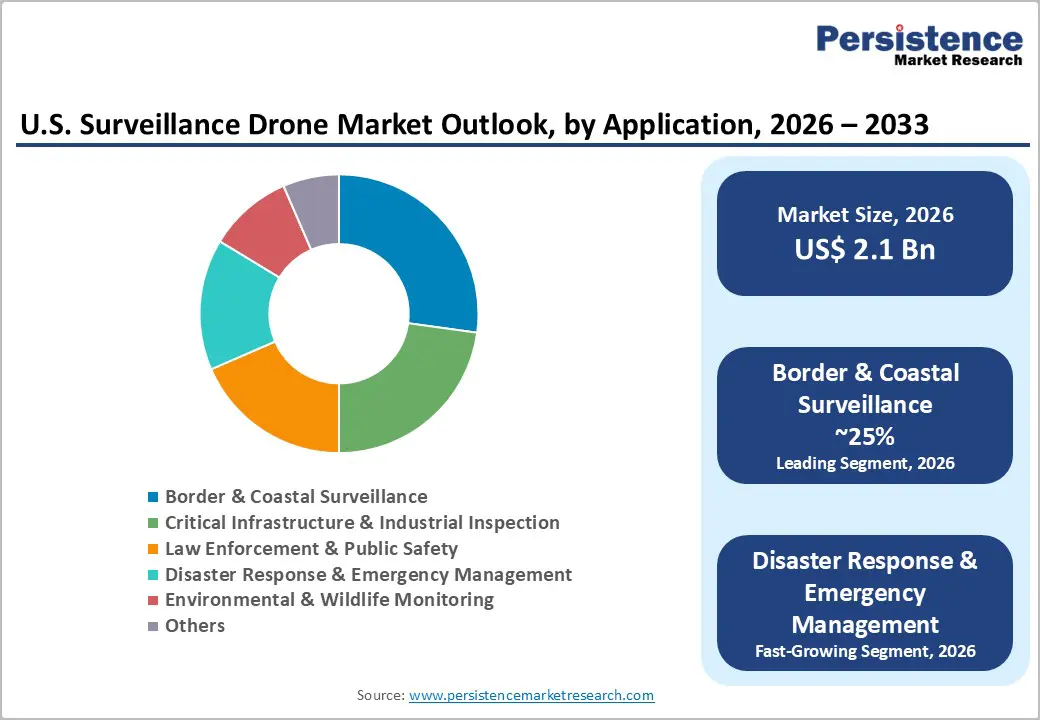

- Leading Application: Border & coastal surveillance commands the largest market share at over 25% in 2026, valued at more than US$ 524 Mn, owing to the need for persistent monitoring of vast and remote areas. Disaster response and emergency management are the fastest-growing, with a CAGR of 14.6%, as drones provide rapid situational awareness and safe access to hazardous zones.

- Market Opportunity: Autonomous AI-integrated drone-in-a-box solutions are driving adoption across industrial, security, and government sectors, supporting persistent surveillance, critical infrastructure monitoring, and operational efficiency. Expanding border security and law enforcement applications, supported by federal contracts such as Skydio’s US$ 74 Mn counternarcotics deal, highlight strong government demand.

| Key Insights | Details |

|---|---|

|

U.S. Surveillance Drone Market Size (2026E) |

US$2.1 Bn |

|

Market Value Forecast (2033F) |

US$4.5 Bn |

|

Projected Growth (CAGR 2026 to 2033 |

11.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

8.4% |

Market Dynamics Analysis

Driver - Accelerating Regulatory Reforms Supporting BVLOS Operations & Airspace Integration

The FAA Reauthorization Act of 2024 emphasized the development of performance-based regulations, including proposed Part 108, specifically designed for Beyond Visual Line of Sight (BVLOS) operations. In line with this, the FAA has been advancing Notice of Proposed Rulemaking (NPRM) initiatives for BVLOS operations, aiming to establish standardized procedures for safe integration of drones into national airspace. In 2024, the FAA authorized multiple operators to conduct BVLOS commercial drone flights concurrently in the same airspace over North Texas, a first-of-its-kind experimental authorization. The gradual normalization of BVLOS rules is expected to significantly expand the operational scope of surveillance drones, enabling persistent monitoring of borders, pipelines, and critical infrastructure at scale, and accelerating adoption across industrial, security, and government applications.

Growing Demand for Industrial Infrastructure Monitoring

Large facilities such as power plants, pipelines, refineries, and transmission networks require continuous monitoring to ensure operational safety and regulatory compliance. Traditional inspection methods involving helicopters or manual field checks are costly and potentially hazardous. Drone-based inspection provides high-resolution imagery, LiDAR mapping, and thermal analysis, enabling faster and safer inspections. Organizations such as the U.S. Department of Energy (DOE) encourage digital inspection technologies to improve infrastructure resilience. Companies managing thousands of miles of pipelines and transmission lines across the U.S. benefit significantly from drone-enabled predictive maintenance. As industrial digitalization expands, drone-based monitoring systems integrated with AI analytics are becoming essential tools for infrastructure security and operational efficiency.

Restraint - Stringent Airspace Regulatory Complexity and Lengthy Approval Processes

Despite regulatory progress, U.S. surveillance drone operators face regulatory complexity and lengthy approval processes for BVLOS flights. Routine BVLOS operations currently depend on case-by-case waivers and authorizations under Part 107, which take months to obtain and increase operational costs. In the FAA’s BEYOND program, most lead participants struggled to meet key performance metrics for BVLOS operations, with only a minority partially meeting certain KPIs for operations without visual observers, highlighting challenges in validating scalable BVLOS readiness. These procedural hurdles increase deployment timelines and deter investment, especially for smaller operators.

Cybersecurity Vulnerabilities and Data Privacy Concerns

UAVs are vulnerable to threats such as GPS spoofing, signal jamming, and unauthorized interception of communications and sensor data, which undermine mission integrity and expose sensitive information to malicious actors. Heightened public scrutiny over mass aerial surveillance by law enforcement has driven an expanding body of state-level privacy protections and warrant requirements. As of 2024, 18 U.S. states have enacted laws requiring law enforcement agencies to obtain a search warrant before using drones for surveillance or searches, and at least 15 states have passed drone-specific privacy protections for private citizens, creating a varied regulatory landscape with divergent requirements across jurisdictions. This patchwork of legislation increases operational complexity and compliance costs for market participants, especially those operating across multiple states.

Opportunity - Autonomous and AI-Integrated Drone-in-a-Box Solutions for Persistent Surveillance

Fully autonomous drone-in-a-box platforms are gaining traction for persistent surveillance, critical infrastructure monitoring, and industrial security applications, driven by advances in edge AI, automated operations, and real-time data analytics. The integration of machine learning-based threat detection and 5G-enabled communications is enhancing mission responsiveness and reducing operator involvement. The U.S. Army has announced plans to vastly expand its drone fleet, including at least one million units over the next few years to support ISR and other missions, reflecting growing military demand. The DoD’s Replicator initiative aims to field thousands of all-domain autonomous systems across multiple service branches, underlining defense interest in scaled autonomous capabilities, though quantities and capability timelines are evolving.

Expanding Border Security and Law Enforcement Surveillance Applications

The U.S. surveillance drone market is poised for significant growth as federal agencies expand aerial monitoring for law enforcement and border security missions. In June 2025, Skydio secured a USD 74 million contract from the U.S. Department of State Bureau of International Narcotics and Law Enforcement Affairs to supply autonomous X10D drones for counternarcotics and law enforcement operations. Federal policy initiatives promoting domestic drone manufacturing and broader UAS deployment underscore strong government intent to scale surveillance capabilities. This creates a robust pipeline of procurement opportunities for drone providers across border monitoring, public safety, and related security applications.

Category-wise Analysis

Platform Type Insights

Fixed wing capturing more than 52% market share in 2026 with a value exceeding US$ 1.1 Bn, due to operational needs for long-range monitoring and persistent aerial coverage. Their aerodynamic wing structure allows them to generate lift efficiently, enabling longer flight endurance and lower energy consumption compared to multi-rotor drones. They cover larger geographic areas per flight and travel at higher speeds, which reduces the number of missions needed to monitor wide territories. Their ability to carry heavier sensors such as high-resolution cameras, LiDAR, and communication systems makes them well-suited for advanced surveillance operations.

Hybrid demonstrate significant growth as they address key operational needs for long-duration monitoring missions. Their dual power systems (fuel + battery) enable significantly longer flight endurance, allowing surveillance over large borders, coastlines, and critical infrastructure without frequent landings. Many hybrid designs combine fixed-wing efficiency with VTOL capability, allowing them to cover large areas while still taking off and landing in confined locations such as urban zones or remote terrains.

Mode of Operation Insights

Remotely Piloted holds over 55% market share in 2026, with a value exceeding US$ 1.2 Bn, as they combine automation with human control for critical decision-making. Human operators analyze live video feeds and adjust missions instantly, which is essential in complex surveillance tasks such as border monitoring, law enforcement, and disaster response. These systems also allow agencies to conduct long-duration monitoring without risking personnel in dangerous areas. Remotely piloted drones provide real-time intelligence and rapid deployment, enabling security teams to respond quickly to evolving situations.

Fully Autonomous is expected to grow at the highest rate, with a CAGR of 15.4%, as agencies increasingly need continuous monitoring with minimal human intervention. Autonomous systems automatically patrol borders, critical infrastructure, and disaster zones, reducing the need for large operational teams. They also enable real-time data processing, automated threat detection, and faster decision-making, which is critical for security and emergency response. The demand for long-duration missions and scalable surveillance operations is pushing organizations toward drones that navigate, analyze, and respond independently.

Application Insights

Border & coastal surveillance commands the largest market share at over 25% in 2026, with a value exceeding US$ 524 Mn, as securing vast land and maritime boundaries requires persistent monitoring over large and often remote areas. Drones patrol long border stretches and coastlines more efficiently than ground patrols or manned aircraft, providing continuous aerial coverage. They also enable real-time detection of illegal crossings, smuggling, and suspicious activities, allowing faster response by security agencies. Advanced sensors such as thermal cameras and high-resolution imaging help monitor difficult terrains and night operations, improving situational awareness for border authorities.

Disaster response & emergency management are expected to grow at a CAGR of 14.6% as emergency agencies increasingly need rapid situational awareness during natural disasters such as hurricanes, wildfires, floods, and earthquakes. Drones provide real-time aerial imagery of damaged infrastructure, blocked roads, and stranded populations, helping responders prioritize rescue operations. They also enable safe assessment of hazardous zones where human access is risky, such as collapsed buildings or chemical spill areas. Drones support search-and-rescue missions with thermal imaging and wide-area monitoring, significantly improving response speed and coordination among emergency teams.

Competitive Landscape

The U.S. surveillance drone market exhibits a moderately consolidated competitive structure, in which a small group of well-established defense contractors coexists with a dynamic cohort of specialized, venture-backed drone technology firms. Established defense primes leverage deep Department of Defense (DoD) relationships and extensive R&D infrastructure, while agile innovators compete through AI-driven autonomy and drone-in-a-box capabilities. The market is increasingly characterized by the integration of edge AI into drone platforms, rising cross-domain autonomy investments, the emergence of subscription-based Drone-as-a-Service (DaaS) models, and a strong emphasis on compliance with the Defense Innovation Unit (DIU) Blue UAS certification, which is essential for accessing DoD procurement pipelines.

Key Industry Developments:

- In January 2026, The U.S. Department of Homeland Security (DHS) launched a new office dedicated to rapidly procuring and deploying drone and counter-drone technologies, aiming to strengthen American airspace security. The Program Executive Office for Unmanned Aircraft Systems and Counter-UAS will oversee strategic investments in advanced surveillance drones, AI-driven monitoring, and autonomous threat detection. This move underscores growing federal focus on leveraging drones for border security, critical infrastructure protection, and public safety.

- In May 2025, Skydio delivered the first Skydio X10D small, unmanned aircraft systems under the United States Army Short Range Reconnaissance (SRR) Tranche 2 program, supplying hundreds of drones to a unit preparing for deployment. The autonomous drones, part of the Blue UAS Cleared List, provide advanced intelligence, surveillance, and reconnaissance (ISR) capabilities, strengthening battlefield situational awareness and operational effectiveness for the U.S. Department of Defense.

Companies Covered in U.S. Surveillance Drone Market

- Aerodyne Group

- Percepto

- Airobotics Ltd.

- Azur Drones

- Cyberhawk Innovations Ltd.

- Avitas Systems

- Sky‑Futures

- Terra Drone Corporation

- MISTRAS Group

- BAE Systems

- Skydio

- AeroVironment

- Teledyne FLIR

- Others

Frequently Asked Questions

The U.S. surveillance drone market is projected to be valued at US$2.1 Bn in 2026.

The rise in investment in autonomous unmanned systems, expanding ISR procurement by all military branches, and regulatory reforms enabling BVLOS drone operations under the FAA Reauthorization Act of 2024 are key drivers of the market.

The market is expected to witness a CAGR of 11.6% from 2026 to 2033.

The deployment of AI-powered, fully autonomous drone-in-a-box surveillance systems for persistent border security, law enforcement, and critical infrastructure monitoring is creating strong growth opportunities.

Aerodyne Group, Percepto, Airobotics Ltd., Azur Drones, Cyberhawk Innovations Ltd., Avitas Systems are among the leading key players.