- Beauty & Personal Care

- U.S. Sexual Wellness Market

U.S. Sexual Wellness Market Size, Share, and Growth Forecast, 2026 - 2033

U.S. Sexual Wellness Market by Product Type (Sex Toys, Condoms, Personal Lubricants, and Others), Distribution Channel (E-commerce, Retailers, Others), Zone (West U.S., Northeast U.S., Midwest U.S., Southeast U.S., and Southwest U.S.), and Zonal Analysis for 2026 - 2033

U.S. Sexual Wellness Market Size and Trends Analysis

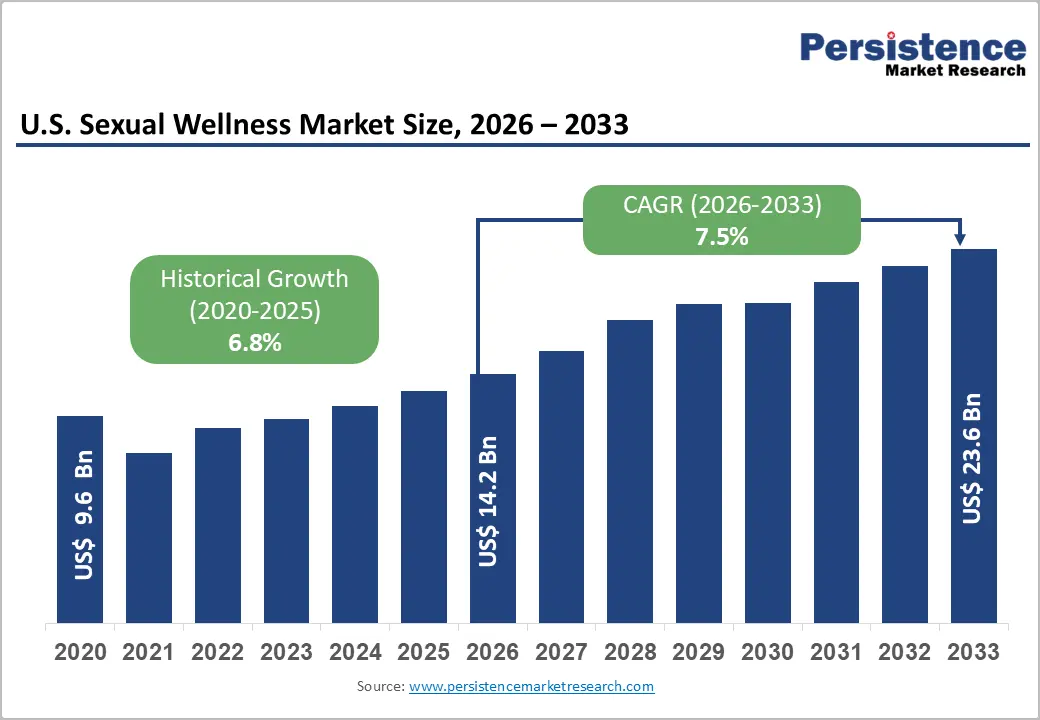

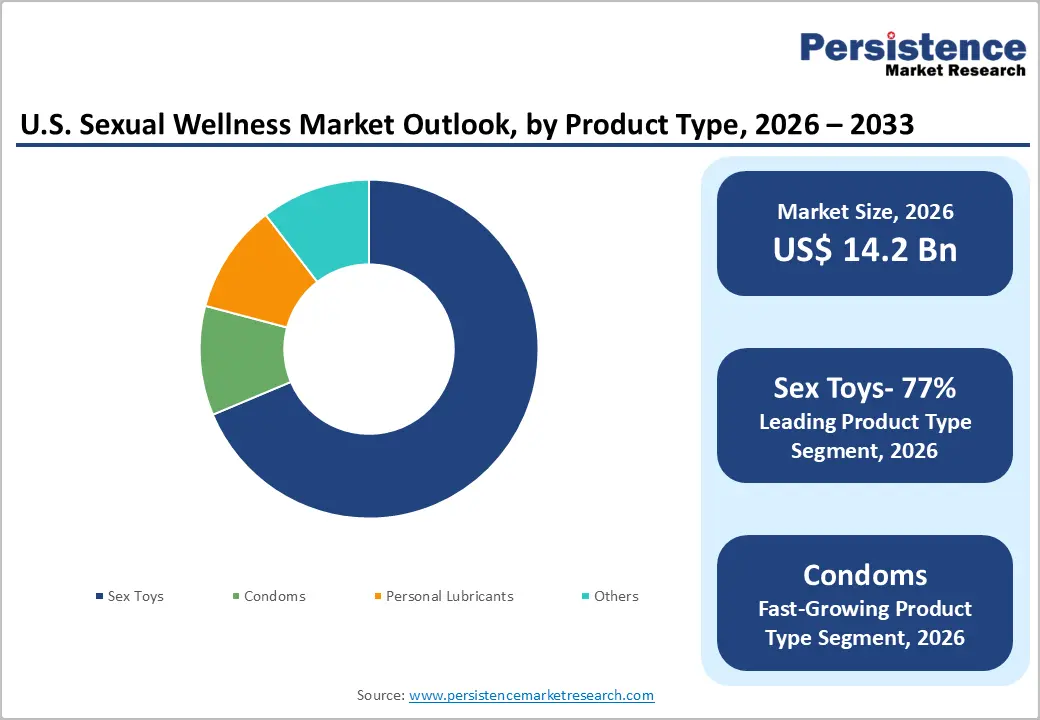

The U.S. sexual wellness market size is likely to be valued at US$ 14.2 billion in 2026 and is projected to reach US$ 23.6 billion by 2033, growing at a CAGR of 7.5% between 2026 and 2033. Based on the provided historical data, the market expanded from US$ 9.6 billion in 2020, reflecting a robust 6.8% historical CAGR driven by rising sexual health awareness, destigmatization of pleasure products, and expanding product portfolios.

Industry analyses of the U.S. sexual wellness sector indicate similar growth trajectories, with value-based CAGRs in the high-single digits underpinned by increased openness to sexual wellness and broadening distribution through both online and mass retail channels. Growth to 2033 will be powered by the dominance of sex toys (over 77% of revenue in 2026), rapid expansion in e-commerce distribution (over 62.6% share in 2026), and rising purchasing power in high-income Zones such as the West and Northeast.

Key Industry-Highlights:

- Demand Dynamics: Growing awareness and social acceptance of sexual health products are expanding demand across diverse age groups in the U.S. Rising recognition of sexual wellness as a key component of overall health and well-being is strengthening market demand.

- Advertising Policy Restrictions: Strict advertising rules on social media and mainstream platforms restrict promotional opportunities for sexual wellness brands, increasing customer acquisition costs and limiting category visibility.

- Smart Device Innovation: Technology-enabled devices with app connectivity, personalized settings, and remote features are creating premium product opportunities and attracting digitally native millennials and Gen Z consumers.

- Sex Toys Dominance: Sex toys account for over 77% of U.S. sexual wellness revenue, driven by product innovation, wider availability, and increasing acceptance across genders and relationship categories.

- Condom Market Growth: Rising STI awareness, contraception demand, and FDA-regulated innovations such as ultra-thin and non-latex products are accelerating condom adoption among younger consumers.

- Online Retail Leadership: E-commerce holds over 62% market share due to anonymity, wider assortments, subscription models, and discreet delivery services supporting the growth of premium devices and wellness kits.

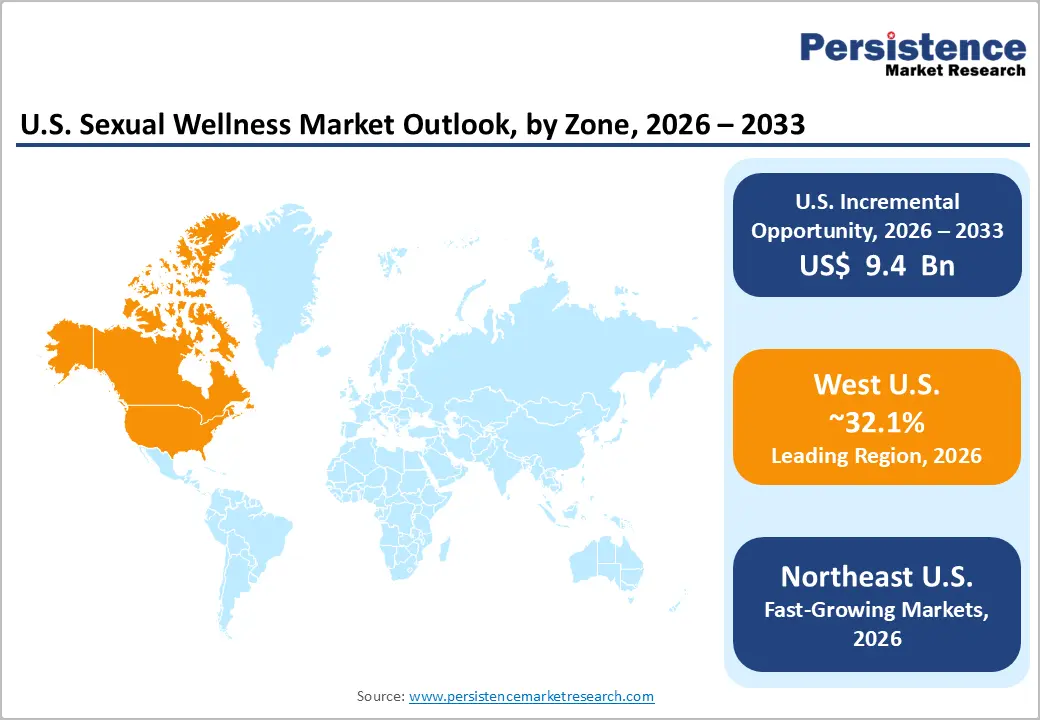

- Western Zone Leadership: High income levels, liberal social norms, and strong technology ecosystems position Western states as the leading Zone for innovation and early adoption of sexual wellness products.

- Northeast Market Expansion: High urban income levels, retail innovation, and comprehensive sex education programs are driving rapid market growth and increasing demand for premium sexual wellness products.

- Competitive Market Landscape: The market features global consumer-health companies and specialized brands competing through innovation, digital marketing, influencer partnerships, and expanded retail distribution strategies.

- Greater societal acceptance of LGBTQ+ communities is increasing demand for inclusive and specialized sexual wellness products.

- Increasing women’s empowerment and focus on female sexual health are accelerating product innovation and market expansion.

Market Dynamics

Key Growth Drivers

Rising Awareness of Sexual Wellness Products to Promote Health Initiatives

As governments and non-governmental organizations encourage the use of contraceptives and disease prevention, the U.S. is developing at a substantial rate due to increased awareness of sexual health products. Organizations like Planned Parenthood and UNAIDS promote safe sexual practices through campaigns, fostering surging adoption of condoms, lubricants, and other sexual wellness products. For instance,

The U.S. government's Ending the HIV Epidemic plan launched in 2019 aims to reduce HIV infections by 90% by 2030, creating high demand for products like PrEP (pre-exposure prophylaxis) and condoms.

In order to improve product accessibility and market growth through digital health platforms for the discreet distribution of sexual wellness goods, Durex and Trojan are collaborating with public health groups.

E-commerce penetration and omnichannel retailization

The U.S. Department of Commerce reports that e-commerce has exceeded one trillion dollars annually and now accounts for more than 15% of total U.S. retail sales, with online penetration reaching record highs in 2024. Analysts of Commerce Department data highlight that e-commerce has grown faster than overall retail for multiple consecutive years, reinforcing the structural shift toward digital purchasing.

In sexual wellness, industry reports show e-commerce already holds the largest channel share and is expected to grow fastest, driven by discreet delivery, broad assortment and subscription models. This infrastructure enables brands to reach underserved demographics and geographies at scale, lowering access barriers for consumers reluctant to buy intimate products instore.

Market Restraining Factors

Persistent stigma and inconsistent sex education

Despite liberalization, sexual wellness products still face cultural and social stigma, particularly in conservative communities and among older demographics. Reporting on U.S. sex-education programs highlights wide variation in state-level curricula and continued reliance on abstinence-focused approaches in some Zones, limiting structured education on condoms, lubricants, and pleasure products. This uneven information environment depresses product uptake in segments where embarrassment, misinformation, or fear of judgment remain high, constraining category conversion outside coastal urban centers.

Advertising restrictions and platform policies

Many mainstream advertising platforms maintain strict limitations on sexual content, especially for devices and erotica-adjacent products, making customer acquisition costlier for emerging brands. Cases such as litigation over transit authority ad bans for female-focused pleasure brands, and ongoing social-media restrictions, illustrate structural barriers to normalized promotion of sexual wellness.

These constraints increase dependence on organic advocacy, influencers, and niche publishers, slowing brand-building relative to adjacent personal-care categories and concentrating marketing scale with large incumbents that can navigate complex compliance requirements.

Sexual Wellness Market Trends and Opportunities

Inclusive and Technology-Driven Product Innovation Expanding Premium Market Potential

The U.S. sexual wellness market is witnessing strong opportunities through inclusive, technology-enabled product innovation. Premium and mid-range brands are increasingly investing in ergonomically designed and app-connected devices that offer personalized user experiences. Products such as dual-ended wands, advanced stimulators, and smart wellness devices now incorporate features including customizable vibration patterns, remote control functionality, and mobile-app integration. These innovations allow users to tailor their experiences while also enabling long-distance intimacy through digital connectivity.

As sexual wellness increasingly overlaps with broader digital self-care and wellness ecosystems, technology-driven devices are gaining acceptance among consumers who value convenience, personalization, and discreet usage.

In addition, advancements in artificial intelligence and smart device integration are opening new avenues for product differentiation in the sexual wellness industry. Companies are experimenting with AI-enabled companionship technologies and highly customizable wellness products that combine emotional interaction with physical functionality. Early launches in international markets have demonstrated strong commercial potential, with high-end models priced between US$1,600 and US$3,000 selling out rapidly in Zones including North America.

As consumer attitudes continue to shift toward more open and technology-integrated sexual health solutions, manufacturers have the opportunity to command premium pricing, increase average revenue per user, and attract digitally native millennial and Gen Z consumers seeking innovative, personalized wellness experiences.

Sexual Wellness Market Insights and Trends

Product Type Insights

U.S. Sexual Wellness Market Dynamics Driven by Transformer Efficiency and EV Motor Demand

The U.S. sexual wellness market is largely driven by the sex toys segment, which includes products such as vibrators, dildos, penis rings, masturbation sleeves, bondage accessories, sex dolls, and other intimate devices. Industry research indicates that sex toys represent the dominant product category, accounting for more than 77% of total market revenue in 2026. Their widespread adoption across genders, age groups, and relationship types reflects the growing normalization of sexual wellness products in mainstream consumer culture.

Increasing availability through online platforms, specialty stores, and large retail chains has further accelerated adoption. In addition, continuous innovation in materials such as body-safe silicone and ABS plastics, along with advanced product formats like air-pulse stimulation and app-connected devices, has encouraged product upgrades and repeat purchases.

While sex toys currently dominate overall market value, condoms are expected to be the fastest-growing segment from 2026 to 2033. Approximately 450 million condoms are sold annually in the United States. This growth is driven by rising awareness of safe sex practices, STI prevention, and contraceptive use, particularly among younger consumers. Strong regulatory oversight from the U.S. FDA, combined with product innovations such as ultra-thin, textured, and non-latex condoms, is improving product safety, comfort, and consumer acceptance, thereby supporting sustained market expansion.

Distribution Channel Insights

E-Commerce Dominates Volume; Retailers Deliver Incremental Reach Upside

E-commerce has emerged as the dominant distribution channel in the U.S. sexual wellness market, accounting for more than 62.6% of total revenue in 2026. The strong performance of online platforms reflects broader retail trends in the United States. According to the U.S. Commerce Department, e-commerce sales have more than doubled since 2019 and now represent over 15% of total retail sales, with penetration approaching one-fifth of non-seasonally adjusted retail transactions in 2024.

Within the sexual wellness category, online channels continue to lead due to factors such as consumer anonymity, wider product assortments, access to user reviews, and discreet delivery services. Digital-first brands are also adopting direct-to-consumer strategies, subscription models, and educational content to reduce stigma and build stronger customer relationships. As mobile commerce and rapid delivery services expand, e-commerce is expected to remain the primary growth channel, particularly for premium devices and curated wellness kits.

Although smaller in revenue share, the retailer channel is the fastest-growing segment, projected to grow at around 8.3% CAGR. Major pharmacy chains, mass retailers, and beauty stores are increasing shelf space for sexual wellness products. Retailers such as Sephora, Target, and Ulta are transitioning from online-only listings to curated in-store assortments. This omnichannel presence improves product visibility, encourages consumer trial, and further normalizes sexual wellness within mainstream personal-care categories.

Zonal Insights and Trends

Affluence, Innovation, and Liberal Norms Underpin Zoneal Leadership

The Western United States, led by California, Washington, Colorado and other high-income states, accounts for the largest share of the U.S. sexual wellness market, with the segmentation indicating over 32.1% of national revenues in 2026. Zoneal income data show that the West consistently posts some of the highest median household incomes in the U.S., supporting greater discretionary spend on wellness and lifestyle categories. High levels of urbanization and broadband penetration further facilitate online purchasing of intimate products and rapid adoption of direct-to-consumer brands.

Performance is strengthened by a dense ecosystem of technology firms, e-commerce platforms and venture-backed sexual wellness start-ups clustered around hubs such as the San Francisco Bay Area, Los Angeles and Seattle. These companies drive innovation in connected devices, design-led toys and body-safe materials, often leveraging app integrations and data-driven personalization. Regulatory environments in many Western states are comparatively supportive of comprehensive sex education and access to contraceptives, which reinforces consumer familiarity with condoms and lubricants and creates a favorable backdrop for health-oriented positioning.

The competitive landscape includes both global incumbents and domestic manufacturers; for example, large U.S. pleasure-product manufacturers with substantial production in California supply a wide range of devices across price tiers. Investment activity is visible through ongoing product launches, collaborations and retail partnerships, including the expansion of sexual wellness in West-based beauty and lifestyle retailers. Combined, these factors suggest that the Western Zone will remain the strategic epicenter for high-value product launches and early-stage innovations, while also serving as a bellwether for consumer trends likely to diffuse to other Zones.

Dense Urban Markets and Retail Pilots Accelerate Category Expansion

The Northeastern United States is emerging as the fastest-growing Zonal market, with the segmentation assigning it an approximate 8.4% CAGR between 2026 and 2033. The Zone’s income profile is favorable; analyses of Census data show the Northeast recording median household incomes comparable to or slightly below the West, and well above those in the Midwest and South. This income advantage, concentrated in metropolitan areas such as New York City, Boston and Philadelphia, underpins demand for premium sexual wellness devices, lubricants and branded condom lines.

The Northeast is also a focal point for retail innovation, including the first in-store deployments of intimate-care and sexual wellness assortments in prestige beauty chains and upscale department stores. Reporting on Sephora’s intimate-care category launch and subsequent in-store expansion highlights how East-coast flagships are used as test-beds for merchandising pleasure products alongside skincare and wellness, which in turn normalizes category visibility and drives trial. Regulatory frameworks in many Northeastern states emphasize comprehensive sex education and reproductive-health access, helping sustain awareness of barrier methods and sexual health across younger demographics.

Competitive dynamics in the Northeast are shaped by the presence of global condom and lubricant brands, emerging D2C device brands, and boutique retailers in major urban centers. As more sexual wellness brands secure shelf space in pharmacies, supermarkets and beauty chains across the Zone, investment opportunities arise in localized marketing, culturally attuned education campaigns, and partnerships with universities and healthcare systems focused on STI prevention and consent education.

Competitive Landscape

The U.S. sexual wellness market is characterized by moderate fragmentation and intense competition, with the presence of global consumer-health companies, specialized sexual wellness brands, and independent device manufacturers. Major corporations such as Church & Dwight Co., Inc., Reckitt Benckiser Group plc, Doc Johnson Enterprises, and Lovehoney Group are actively competing for market leadership through strategic partnerships, product innovation, and targeted expansion strategies. Companies are increasingly focusing on advanced technologies, ergonomic product designs, and digital connectivity features to differentiate their offerings and strengthen brand positioning.

Marketing and promotional strategies also play a crucial role in shaping market dynamics. Many brands leverage social media platforms and digital campaigns to present sexual wellness products as lifestyle and wellness essentials rather than niche items. Collaborations with celebrities, wellness advocates, and social media influencers further help normalize conversations around sexual health and reach a wider consumer base. In the condom and lubricant categories, brands such as Durex, Trojan, and LifeStyles maintain strong market presence, while the sex-toy segment features prominent players including Lovehoney, LELO, TENGA, Doc Johnson, and CalExotics, alongside several European boutique brands.

Key Industry Developments

- In October 2024, Hello Cake acquired Nevada-based Trigg Laboratories, a pioneer in personal lubricants, strengthening its position as a vertically integrated sexual health company.

- In June 2024, U.S. sexual wellness brand Playground launched the hotline 1-888-PLY-GRND, hosted by Christina Aguilera, promoting open discussions about sexual wellness and addressing stigma around women’s sexual health.

- In April 2024, Simple HealthKit launched at-home diagnostic and follow-up care kits covering diabetes, respiratory health, and sexual wellness, including tests for Influenza A, B, and RSV to support early detection.

Companies Covered in U.S. Sexual Wellness Market

- Church & Dwight Co., Inc.

- Reckitt Benckiser Group plc

- Doc Johnson Enterprises

- Lovehoney Group

- LELO

- We-Vibe

- TENGA Co., Ltd.

- b-Vibe

- Fun Factory GmbH

- Satisfyer

- Hot Octopuss

- Blush Novelties

- Other Market Players

Frequently Asked Questions

The Sexual Wellness market is estimated to be valued at US$ 14.2 Bn in 2026.

The rising awareness of sexual health and STI prevention is the primary demand driver for the U.S. sexual wellness market. Growing public health campaigns, sex-education programs, and initiatives by organizations such as Planned Parenthood and UNAIDS have significantly increased awareness about safe sex practices.

In 2026, the West U.S. Zone will dominate the market with an exceeding 32.1% revenue share in the U.S. Sexual Wellness market.

Among product types, Sex Toys has the highest preference, capturing beyond 77% of the market revenue share in 2026, surpassing other product types.

Key companies operating in the U.S. sexual wellness market include Church & Dwight Co., Inc., Reckitt Benckiser Group plc, Doc Johnson Enterprises, Lovehoney Group, LELO, We-Vibe, TENGA Co., Ltd., b-Vibe, and Fun Factory GmbH, among others. These players compete through product innovation, brand expansion, and strategic partnerships to strengthen their market presence.