- Inks, Coatings, Adhesives & Sealants (ICAS)

- U.S. Release Coating Market

U.S. Release Coating Market Size, Share, and Growth Forecast 2026 - 2033

U.S. Release Coating Market by Material Type (Silicone, Non-silicone), Formulation (Solvent-based, Solventless, Emulsions, Others), Application (Labels, Tapes, Hygiene, Industrial, Medical, Food Bakery, Graphic Films, Others), and Regional Analysis, 2026 - 2033

U.S. Release Coating Market Size and Trend Analysis

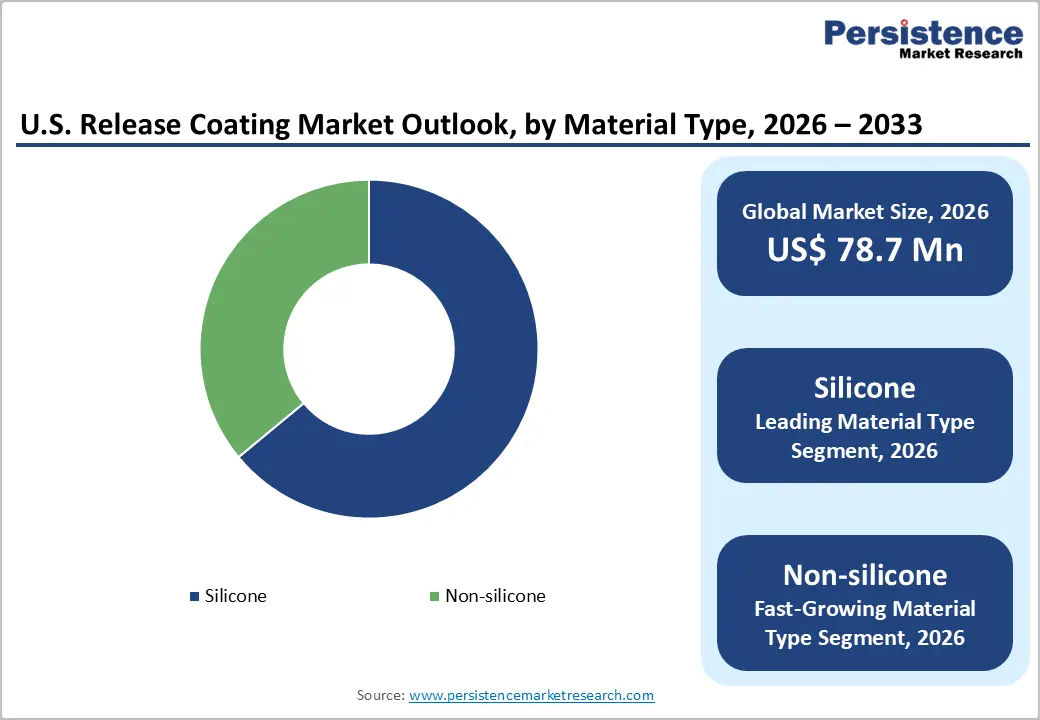

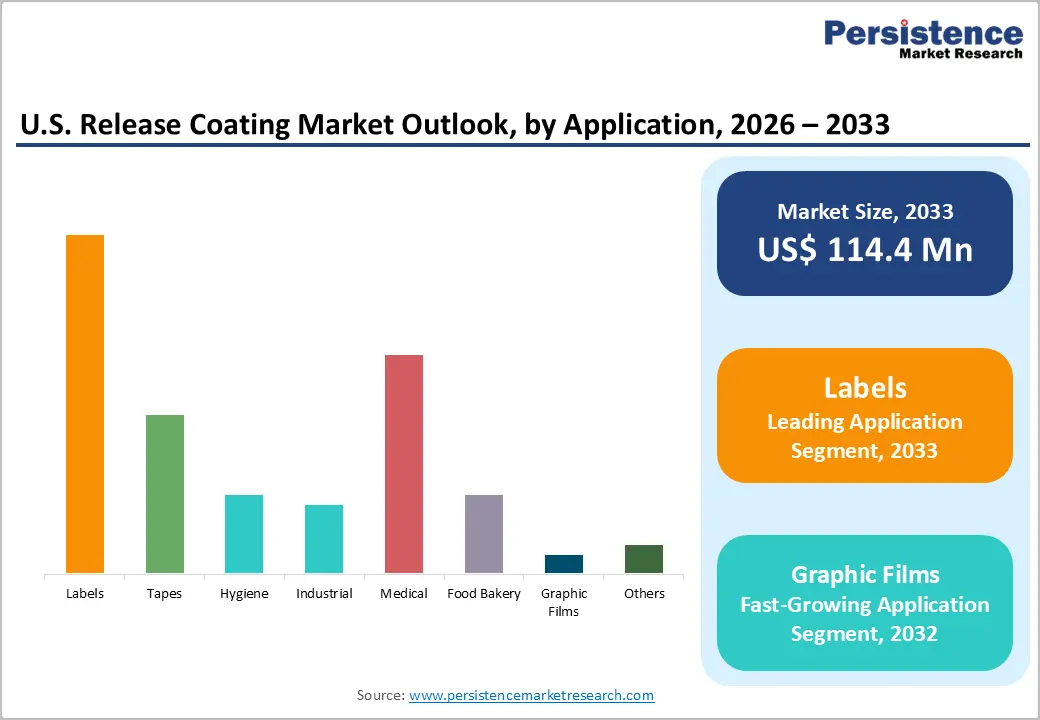

The U.S. release coating market size is expected to be valued at US$ 78.7 million in 2026 and is projected to reach US$ 114.4 million by 2033, growing at a CAGR of 5.5% between 2026 and 2033.

Sustained growth is propelled by expanding demand from pressure-sensitive label and tape manufacturing, rising consumption in hygiene and medical product applications, and the continued shift toward solventless and low-VOC coating technologies.

Regulatory pressure from the U.S. Environmental Protection Agency (EPA) to reduce volatile organic compound (VOC) emissions, combined with growing end-use demand from the packaging and healthcare sectors, reinforces the positive long-term outlook for U.S. release coating manufacturers and formulators.

Key Industry Highlights:

- Leading Region: The Northeast U.S. leads the release coating market, driven by a high density of pharmaceutical manufacturers, label converters, and specialty tape producers across New Jersey, Pennsylvania, and New York, sustaining robust demand for medical and pressure-sensitive release coating applications.

- Fast-Growing Market: The Southeast U.S. is the fast-growing market, fueled by rising investments in medical device and hygiene product manufacturing across North Carolina, Georgia, and Florida, alongside expanding e-commerce logistics infrastructure driving label and packaging demand.

- Dominant Material: Silicone release coatings dominate with approximately 64% market share in 2026, underpinned by unmatched thermal stability, controlled release precision, and established converter familiarity across label, medical, and industrial tape applications.

- Fast-Growing Material: Non-silicone release coatings are the fastest growing segment, projected at a CAGR of 6% by 2033, driven by demand from electronics, food-contact packaging, and medical devices where silicone migration is a regulatory or performance concern.

- Key Market Opportunity: The rapid adoption of solventless UV-curable release coating systems presents the highest-value commercial opportunity, enabling compliance with EPA and CARB VOC regulations while delivering superior line efficiency and substrate versatility for label, tape, and medical converters.

DRO Analysis

Drivers - Surging Demand from Pressure-Sensitive Labels and Packaging Applications

The pressure-sensitive labels segment remains one of the most significant demand anchors for release coatings in the U.S. According to the Tag and Label Manufacturers Institute (TLMI), the North American label industry consistently records annual output exceeding 65 billion square feet, with a substantial proportion dependent on silicone-based release liners for face-stock protection and dispensing efficiency.

Growth in e-commerce logistics, driven by platforms such as Amazon and Walmart, has accelerated demand for pressure-sensitive shipping labels and tamper-evident packaging, directly expanding release coating consumption. The U.S. Census Bureau reported that U.S. e-commerce retail sales surpassed US$ 1.1 trillion in 2023, reflecting a structural uplift in label-intensive packaging demand that continues to benefit the release coating supply chain.

Expansion in Medical and Hygiene Product Manufacturing

The medical and hygiene sectors represent a high-growth demand vertical for release coatings in the U.S. Release liners are integral to wound care dressings, transdermal drug delivery patches, ostomy products, and incontinence articles, all of which require precise, contamination-free release properties. The U.S. Food and Drug Administration (FDA) has approved a growing pipeline of transdermal drug delivery systems, with over 35 approved transdermal patch products in active distribution as of 2023.

The American Health Care Association (AHCA) reports consistent growth in adult incontinence product usage, driven by an aging U.S. population. The U.S. Census Bureau projects that adults aged 65 and above will constitute approximately 21% of the total U.S. population by 2030, sustaining long-term demand for hygiene-grade release coatings.

Restraints - Volatility in Silicone Raw Material Prices

Silicone-based release coatings dominate the U.S. market, making manufacturers highly susceptible to upstream price volatility in silicone raw materials, particularly polydimethylsiloxane (PDMS) and reactive silicone polymers. The global silicone supply chain experienced significant disruptions between 2021 and 2023 due to energy cost inflation in China, the world's leading silicone producer, and logistical bottlenecks.

According to the American Chemistry Council (ACC), chemical input costs in the U.S. rose by approximately 18% between 2020 and 2022, compressing operating margins for coating formulators. These cost pressures limit the ability of mid-sized manufacturers to sustain competitive pricing, potentially slowing adoption rates, particularly in price-sensitive packaging and consumer goods end markets.

Stringent Environmental and VOC Emission Regulations

The U.S. release coatings industry, particularly solvent-based formulations, faces mounting regulatory pressure from the EPA under the National Emission Standards for Hazardous Air Pollutants (NESHAP) program. Solvent-based coatings, which historically have offered superior thermal stability and substrate compatibility, are increasingly restricted due to their high VOC content.

Compliance with evolving EPA Title V permitting requirements and state-level air quality regulations, particularly in California under the California Air Resources Board (CARB), increases capital expenditure on emission control infrastructure. This regulatory burden disproportionately affects smaller regional formulators, potentially consolidating market share among larger, better-resourced players capable of transitioning to solventless or UV-curable systems.

Opportunities - Growth in Non-Silicone and Fluoropolymer-Based Release Coatings

Non-silicone release coatings, including fluoropolymer, polyolefin, and chrome-based systems, present a high-value growth opportunity as manufacturers seek to address applications incompatible with silicone migration, such as electronics, food-grade packaging, and certain medical devices. The FDA's increasing scrutiny of silicone contamination in food-contact materials and medical device surfaces is driving formulators and end-users toward non-silicone alternatives.

Non-silicone coatings are the fastest growing category, projected to expand at a CAGR of approximately 6% through 2033. Furthermore, the U.S. electronics manufacturing sector, valued at over US$ 400 billion annually per the Semiconductor Industry Association (SIA), increasingly requires silicone-free release materials for advanced circuit board and component protection, creating substantial demand for specialty non-silicone formulations.

Rising Adoption of Solventless UV-Curable Release Technologies

The transition toward solventless, UV-curable release coating systems offers a compelling commercial and environmental opportunity for industry participants. UV-curable coatings eliminate solvent emissions entirely, significantly reducing compliance costs under EPA and CARB regulations while enabling higher line speeds and reduced energy consumption compared to thermal-cure solvent systems.

According to the RadTech International North America association, UV and electron-beam (EB) curable coating technologies have recorded consistent adoption growth of 5-7% annually in North American industrial coating applications. Technology’s compatibility with a broad range of substrates, including films, papers, and foils, makes it particularly attractive for label, tape, and medical application converters seeking efficiency gains and regulatory compliance simultaneously, positioning early adopters for significant competitive advantage.

Category-wise Analysis

Material Type Insights

The Silicone segment is the dominant material type in the U.S. Release Coating market, commanding approximately 64% of market share in 2026. This dominance is underpinned by silicone's unmatched combination of controlled release properties, thermal stability across a wide temperature range (-65°C to 200°C), chemical inertness, and compatibility with a diverse range of substrates including paper, polyethylene films, and polyester films. Silicone release coatings are the industry benchmark for pressure-sensitive label liners, protective films, and medical release applications.

According to Dow Inc., one of the world's largest silicone producers, silicone chemistry remains the preferred solution for demanding release applications due to its precision anchorage control and long-term performance consistency. Established supply chains, converter familiarity, and decades of application development data further reinforce silicone's entrenched market position.

Formulation Insights

The Solvent-based formulation segment holds the leading share within the formulation category, accounting for approximately 38% of U.S. release coating revenues in 2026. Solvent-based systems continue to be preferred in applications demanding superior substrate wetting, precise coating weight control, and performance in high-temperature or chemically aggressive environments. Industries such as industrial tapes, specialty medical device liners, and high-performance graphic films have historically relied on solvent-based formulations for their reliable adhesion and release performance.

The Coating Research Group (CRG) of the American Coatings Association (ACA) notes that solvent-borne systems offer formulators the highest degree of rheological flexibility. However, growing regulatory and environmental pressure is gradually accelerating migration toward solventless alternatives, which are projected to be the fastest growing formulation segment over the forecast period.

Application Insights

The Labels application segment leads all end-use categories in the U.S. Release Coating market, accounting for approximately 30% of total application-based revenues in 2026. The dominance of labels is attributable to the omnipresence of pressure-sensitive label technology across food and beverage, logistics, pharmaceuticals, and retail sectors. The Flexible Packaging Association (FPA) and TLMI data confirm that label consumption in the U.S. continues to grow in tandem with expanding retail and e-commerce activity.

Pressure-sensitive labels require a precisely engineered release coating on the liner substrate to ensure reliable dispensing without adhesive transfer or premature release. The rapid growth of variable data printing for traceability and regulatory compliance labeling in food and pharmaceutical packaging further sustains the segment's commanding revenue share.

Regional Analysis

Northeast U.S. Release Coating Market Trends

The Northeast U.S. leads the regional market, driven by the high concentration of pharmaceutical manufacturers, specialty tape converters, and label printing facilities across states such as New Jersey, Pennsylvania, and New York. The region hosts a significant cluster of FDA-regulated drug manufacturing facilities, sustaining consistent demand for medical-grade release coatings used in transdermal patches and wound care products.

The Northeast's robust industrial and logistics infrastructure, combined with proximity to major consumer goods companies, reinforces its position as the leading revenue-generating region for U.S. release coating consumption.

Midwest U.S. Release Coating Market Trends

The Midwest U.S. is a significant market underpinned by its large-scale food processing, packaging, and automotive manufacturing industries. States such as Illinois, Ohio, and Michigan house major food and beverage producers that consume release coatings for food bakery liners and packaging applications. The region's automotive sector, a major consumer of specialty masking tapes and industrial release films, contributes to additional demand.

The Midwest benefits from a well-developed chemical manufacturing base, with companies such as Dow Inc. headquartered in Midland, Michigan, providing logistical and supply chain advantages to regional converters.

Southeast U.S. Release Coating Market Trends

The Southeast U.S. is an emerging growth region, supported by increasing investments in medical device manufacturing, hygiene product production, and e-commerce fulfillment infrastructure. States including North Carolina, Georgia, and Florida have attracted significant healthcare and consumer goods manufacturing investments, driving demand for medical and hygiene-grade release coatings. The region's growing population base and expanding distribution network infrastructure support rising label and packaging consumption.

Southwest U.S. Release Coating Market Trends

The Southwest U.S. market anchored by states such as Texas and Arizona, benefits from a diversified industrial base encompassing electronics manufacturing, food processing, and energy sector applications.

Texas hosts one of the highest concentrations of chemical processing and specialty coating manufacturers in the country, according to the Texas Chemical Council data, supporting both production and regional consumption of release coatings. The region's rapidly growing population and expanding logistics sector also drive label and tape demand.

West U.S. Release Coating Market Trends

The West U.S., particularly California, is a significant consumption hub for release coatings, despite facing the most stringent VOC and air quality regulations in the nation under CARB. The region's large technology, pharmaceutical, and food and beverage industries sustain demand for premium, compliant release coating systems.

California's regulatory environment is simultaneously acting as an accelerator for the adoption of solventless and UV-curable technologies, positioning the West as a leading region for next-generation release coating innovation and commercialization.

Competitive Landscape

The U.S. release coating market is moderately consolidated, with a handful of global chemical conglomerates, including Dow Inc., Wacker Chemie AG, Evonik Industries AG, and Momentive Performance Materials, commanding significant revenue share through their vertically integrated silicone supply chains and broad application expertise. These leaders differentiate through continuous R&D investment in low-migration and UV-curable formulations, strategic customer co-development programs, and sustainability-focused product lines.

Mid-tier and regional players such as HITAC Adhesives & Coatings, Mayzo, Inc., and Rayven, Inc. compete on application specialization and technical service agility. An emerging trend is the growing focus on bio-based and fluorine-free release technologies in response to evolving regulatory and sustainability imperatives.

Key Developments

- In March 2025, Dow Inc. announced the commercial launch of a new series of solventless silicone release coatings optimized for high-speed converting operations, targeting label and hygiene liner converters seeking improved throughput and lower VOC compliance costs.

- In October 2024, Wacker Chemie AG expanded its WACKER FINISH silicone release coating portfolio with new ultra-low-release-force grades designed for medical transdermal patch and wound care applications, responding to growing pharmaceutical demand in the U.S. and Europe.

- In June 2023, Evonik Industries AG introduced a new range of non-silicone, bio-based release coating additives under its TEGOMER platform, targeting food-contact and electronics applications where silicone migration poses regulatory or performance risks.

U.S. Release Coating Market - Key Insights

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 60.8 million |

| Current Market Value (2026) | US$ 78.7 million |

| Projected Market Value (2033) | US$ 114.4 million |

| CAGR (2026 - 2033) | 5.5% |

| Leading Region | Northeast U.S., 30% market share |

| Dominant Material Type | Silicone, 64% market share (2026) |

| Top-ranking Formulation | Solvent-based, 38% market share (2026) |

| Incremental Opportunity | US$ 35.7 million |

Companies Covered in U.S. Release Coating Market

- Dow Inc.

- Wacker Chemie AG

- Evonik Industries AG

- Momentive Performance Materials

- HITAC Adhesives & Coatings

- Mayzo Inc.

- Elkem

- Rayven Inc.

- Synthomer PLC

- Chemours Company

- Avery Dennison Corporation

- H.B. Fuller Company

- Ashland U.S. Holdings Inc.

- 3M Company

- MTI Polyexe

- Omnova Solutions Inc.

- Loparex LLC

- Lintec Corporation

- UPM Raflatac

- Sappi Limited

Frequently Asked Questions

The U.S. Release Coating market is expected to be valued at US$ 78.7 million in 2026, growing from US$ 60.8 million in 2020. The market is projected to reach US$ 114.4 million by 2033, expanding at a steady CAGR of 5.5% over the forecast period, driven by robust demand from label, medical, and hygiene applications.

The primary demand drivers include the rapid expansion of pressure-sensitive label consumption fueled by e-commerce growth, with U.S. e-commerce sales exceeding US$ 1.1 trillion in 2023 per the U.S. Census Bureau, and rising demand from the medical and hygiene sectors, particularly transdermal drug delivery systems and adult incontinence products, driven by an aging U.S. population.

The Northeast U.S. leads the release coating market, supported by the region's high concentration of FDA-regulated pharmaceutical manufacturers, specialty label converters, and industrial tape producers across New Jersey, Pennsylvania, and New York.

The most significant growth opportunity lies in the adoption of solventless UV-curable release coating technologies, which eliminate VOC emissions, reduce regulatory compliance costs under EPA and CARB mandates, and enable higher production throughput.

The leading companies operating in the U.S. Release Coating market include Dow Inc., Wacker Chemie AG, Evonik Industries AG, Momentive Performance Materials, Chemours Company, 3M Company, Avery Dennison Corporation, H.B. Fuller Company, Elkem, Synthomer PLC, and Ashland U.S. Holdings Inc., among others.