Industry: Chemicals and Materials

Published Date: February-2025

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 182

Report ID: PMRREP35118

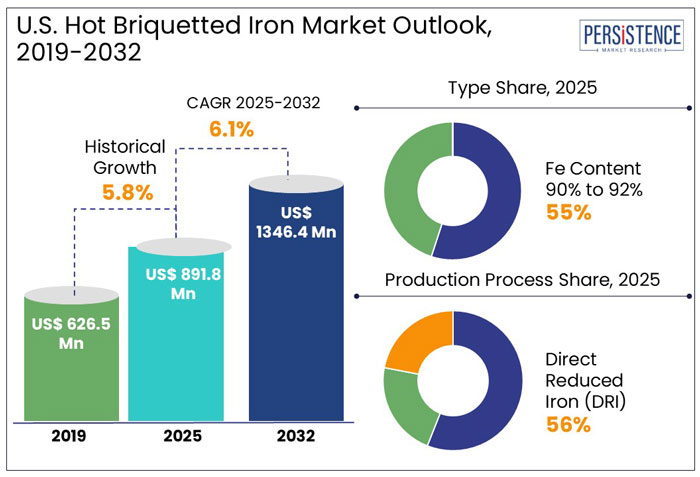

The U.S. hot briquetted iron market is predicted to reach a size of US$ 891.8 Mn by 2025. It is anticipated to experience a CAGR of 6.1% during the forecast period to attain a value of US$ 1,346.4 Mn by 2032.

The U.S. steel industry's transition from blast furnaces to Electric Arc Furnaces (EAF) is driving demand for Hot Briquetted Iron (HBI). By 2030, EAF is set to account for 75% of U.S. steel production, significantly boosting HBI consumption.

U.S. steel manufacturers are adopting HBI to reduce carbon emissions. HBI produces 50% less CO2 compared to traditional coke-based steelmaking processes. Investments in unique DRI technology, including hydrogen-based reduction, are enhancing the efficiency and environmental sustainability of HBI production.

HBI’s compact form enables better storage, handling, and reduced risk of oxidation during transportation, supporting its adoption in long-distance steel production facilities. The steel industry's push toward net-zero carbon emissions by 2050 is accelerating the shift to HBI, a cleaner alternative to scrap metal and pig iron.

Key Highlights of the Industry

|

Market Attributes |

Key Insights |

|

U.S. Hot Briquetted Iron Market Size (2025E) |

US$ 891.8 Mn |

|

Projected Market Value (2032F) |

US$ 1,346.4 Mn |

|

U.S. Market Growth Rate (CAGR 2025 to 2032) |

6.1% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

5.8% |

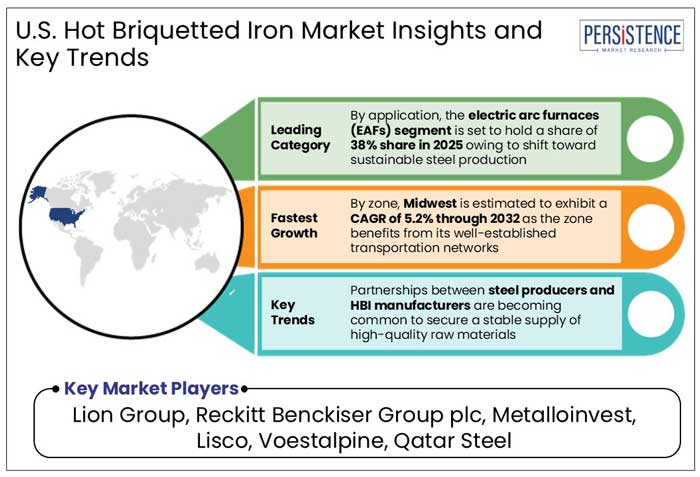

Midwest is predicted to lead the U.S. hot briquetted iron market with a share of 39% in 2025. The zone hosts the largest concentration of steel manufacturing facilities in the U.S. For instance,

Adoption of electric arc furnace (EAF) technology, which is compatible with HBI due to its high iron content and minimal impurities, is surging in the Midwest.

The zone benefits from its well-developed transportation networks, including access to the Great Lakes, railroads, and highways, enabling efficient distribution of HBI. Proximity to import terminals for iron ore and HBI from regions like Canada and South America further enhances supply chain efficiency.

Fe content 90% to 92% is projected to hold a share of 55% in 2025. Steel manufacturers in the U.S. are increasingly adopting Electric Arc Furnace (EAF) technology for cleaner and more energy-efficient steel production. For example,

HBI with Fe content between 90% and 92% contains minimal impurities like phosphorus and sulfur, which can compromise steel quality. These levels ensure greater strength, ductility, and durability in the final steel product, meeting the stringent quality requirements of industries such as automotive, construction, and machinery.

The 90% to 92% Fe grade offers an ideal price-to-performance ratio, with an average price that is 10% to 15% lower than ultra-high Fe content grades. This Fe content range helps reduce carbon emissions when used in EAF-based steel production compared to traditional blast furnace methods.

Direct Reduced Iron (DRO) is anticipated to hold a share of 56% in 2025. The U.S. steel industry is rapidly shifting from traditional blast furnaces to electric arc furnaces (EAF) for sustainable and cost-effective steel production. Direct Reduced Iron (DRI) is highly compatible with EAFs as a feedstock due to its high iron content and low impurity levels. For example,

DRI process uses natural gas instead of coke, significantly reducing CO2 emissions. Studies indicate that DRI-based steel production results in 50% lower CO2 emissions compared to traditional blast furnace routes. This shift aligns with the U.S. government's Inflation Reduction Act (IRA) and its incentives for clean energy manufacturing.

Availability of cheap natural gas in regions like Texas and Pennsylvania further supports the adoption of DRI technology.

Electric Arc Furnaces (EAFs) are anticipated to hold a share of 38% in 2025. EAFs are increasingly preferred due to their lower carbon footprint compared to traditional blast furnaces. For instance,

The U.S. government has implemented green initiatives like the Inflation Reduction Act (IRA), which incentivize the use of low-emission processes like EAFs. These policies promote the adoption of HBI as a feedstock for EAFs to produce cleaner steel. For instance,

EAFs are ideally suited for the use of scrap steel and DRI-based feedstock like HBI. HBI is used in EAFs as it offers higher iron content and lower impurities than traditional scrap, leading to higher-quality steel production.

Potential growth in the U.S. hot briquetted iron industry is predicted to be driven by investments in advanced DRI technologies. Hydrogen-based reduction, for instance, enhance the efficiency and environmental sustainability of HBI production. The period is likely to witness a rise in circular economy practices, thereby promoting HBI adoption as a way to recycle iron content and minimize waste in steelmaking.

The U.S. hot briquetted iron market growth was steady at a CAGR of 5.8% during the historical period. Growth during the period was prominently attributed to the rising demand for cleaner steel production and the transition towards sustainable practices by steel manufacturers.

U.S. steel manufacturers adopted direct reduced iron (DRI) technologies, which directly reduce iron ore using natural gas, eliminating the need for coke and reducing emissions.

The forecast period is likely to witness a rise in investments in new DRI plants. The industry is predicted to undergo technological innovations that will make processes more efficient and sustainable. The automotive and construction sectors are anticipated to continue driving HBI consumption in the U.S. steel industry throughout the assessment period.

Rising Investments in Hydrogen-based Technologies

The U.S. government has increased its focus on clean energy technologies, including the use of hydrogen in steelmaking, under initiatives like the Hydrogen Energy Earthshot program. This aims to reduce the cost of hydrogen to US$ 1 per kilogram by 2030. his initiative is part of the U.S. Department of Energy’s strategy to decarbonize the industrial sector, including the steel industry. For instance,

U.S. Steel has already begun pilot projects to implement hydrogen-based technologies in their DRI plants, with plans to transition from natural gas to hydrogen. Their US$ 3 billion hydrogen-powered plant aims to reduce CO? emissions by up to 80% compared to traditional methods.

The U.S. is aligning with global efforts to decarbonize steelmaking. Partnerships with European companies that have been pioneers in hydrogen-based steel production are paving the way for future investments in hydrogen technologies. This collaboration allows for knowledge transfer and technology sharing, which will benefit U.S. producers of HBI.

Supportive Government Policies and Incentives

In 2021, the Biden administration unveiled the American Jobs Plan, which includes US$ 174 billion to modernize and upgrade the U.S. steel industry. This funding aims to reduce the carbon footprint of steel production and promote clean technologies. The plan includes encouraging steelmakers to invest in cleaner technologies, like Electric Arc Furnaces (EAF) using HBI.

The government in the U.S. provide financial support for steel producers who implement carbon capture technologies can be paired with HBI to reduce CO? emissions from steel production. With funding from the Department of Energy (DOE), there is a clear focus on supporting the use of hydrogen in the steel industry as a cleaner reduction agent. This can significantly enhance the viability of Hydrogen-based Direct Reduction (H2-DR) methods using HBI.

The U.S. government has made it financially attractive for steelmakers to adopt cleaner production technologies. Tax credits decrease the upfront capital costs of investing in electric arc furnaces (EAF) and direct reduced iron (DRI) systems using HBI.

Limited Availability of Suitable Infrastructure

The production of HBI requires significant amounts of electricity and natural gas. As the production processes are energy-intensive, a steady and reliable supply of energy is crucial. This puts pressure on regions that either lack the necessary power grid capacity or have less access to renewable energy sources.

Green hydrogen production is still in the early stages of development in the U.S., and widespread hydrogen infrastructure is not yet established. According to the U.S. Department of Energy, the cost of hydrogen production is still high, and infrastructure for storage, transportation, and distribution of hydrogen is underdeveloped.

Hydrogen production is estimated to increase with projects like the Hydrogen Hub Initiative, but these projects are still in the early development phase. This lag in infrastructure development may delay the large-scale adoption of hydrogen-based technologies in HBI production.

Shift to Low-carbon and Green Steel

The steel industry is one of the largest industrial sources of carbon dioxide (CO2) emissions worldwide, contributing to 7% to 9% of global emissions. In the U.S., the steel sector accounts for 5% to 6% of national industrial emissions.

As the world pushes toward achieving climate goals outlined in the Paris Agreement and the U.S. Green New Deal, there is a strong emphasis on decarbonizing this crucial sector. The shift to low-carbon steel production involves transitioning from conventional methods, which are highly carbon-intensive, to cleaner technologies that minimize CO? emissions. This transformation is essential for meeting net-zero carbon targets by mid-century.

The U.S. government, as part of its climate action agenda, is encouraging the adoption of green steel through several regulatory measures and financial incentives. The Biden Administration has proposed policies to implement carbon taxes and cap-and-trade systems. This creates financial pressure on high-carbon steelmakers to adopt cleaner methods, including the use of HBI and hydrogen-based processes.

Rising Demand for Sustainable Steel Production

As consumers and industries become more conscious of environmental issues, there is growing demand for sustainable products, including steel. This shift in consumer preference is driven by increased awareness of the environmental impacts of traditional manufacturing processes.

The automotive industry is one of the largest consumers of steel, and major automakers like Ford, BMW, and Toyota have set ambitious sustainability goals, including sourcing green steel. For instance,

As part of the global push for sustainable construction, there is a growing demand for green steel in infrastructure projects. This includes the use of recycled steel and low-carbon steel in building construction, reducing the overall carbon footprint of urban development.

Companies in the U.S. hot briquetted iron market are investing in hydrogen-based direct reduction technologies to produce green steel and HBI with reduced carbon emissions. Through this, companies aim to align with sustainability goals and reduce production costs in the long run.

Investment in electric arc furnace (EAF) technology enables companies to improve energy usage efficiency, reduce emissions, and meet regulatory standards. As the push for green steel intensifies, businesses in the U.S. are transitioning to low-carbon HBI production processes.

Steel Dynamics is a prominent player moving towards sustainable practices by adopting low-carbon technologies like Electric Arc Furnaces and green hydrogen-based methods in HBI production.

Manufacturers are promoting a circular economy approach by increasing the use of recycled steel and investing in processes that minimize waste and maximize material reuse. This contributes to both cost reduction and sustainability.

Recent Industry Developments

|

Attributes |

Detail |

|

Forecast Period |

2025 to 2032 |

|

Historical Data Available for |

2019 to 2023 |

|

Market Analysis |

US$ Million for Value |

|

Key Countries Covered |

|

|

Key Market Segments Covered |

|

|

Key Companies Profiled in the Report |

|

|

Report Coverage |

|

|

Customization and Pricing |

Available upon request |

By Type

By Production Process

By Application

By Zone

To know more about delivery timeline for this report Contact Sales

The market is anticipated to reach a value of US$ 1,346.4 Mn by 2032.

Direct Reduced Iron (DRI) is predicted to hold a share of 56% in 2025.

Midwest is anticipated to emerge as the leading zone with a share of 39% in 2025.

Prominent players in the market include Lion Group, Reckitt Benckiser Group plc., and Metalloinvest.

The market is predicted to witness a CAGR of 6.1% throughout the forecast period.