Comprehensive Snapshot of the U.S. Gastrointestinal Point-of-care Testing Market Research Report, Including Segment Analysis and Competitive and Landscape in Brief.

Industry: Healthcare

Published Date: April-2025

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 130

Report ID: PMRREP35231

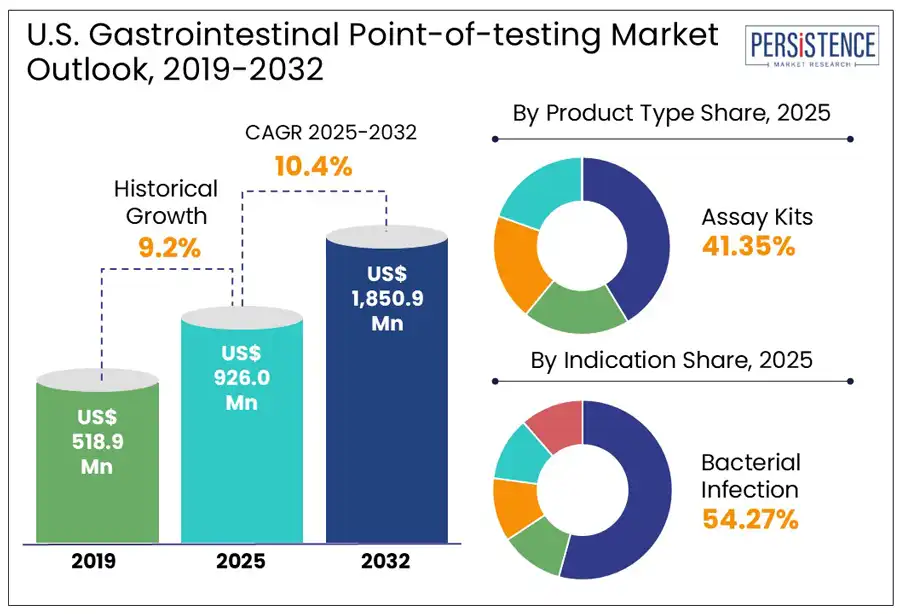

The U.S. gastrointestinal point of care testing (POCT) market is estimated to grow from US$ 926.0 million in 2025 to US$ 1,850.9 million to register a CAGR of 10.4% by 2032. According to the Persistence Market Research report, the rising prevalence of GI disorders, including infections, inflammatory bowel disease, and colorectal cancer, which demand accessible and rapid diagnostic solutions, is fueling the demand. Technological advancements, particularly in molecular diagnostics and immunoassays, have improved the accuracy, speed, and usability of point of care testing, making them ideal for early detection and treatment decisions.

Additionally, the shift toward decentralized, patient-centric healthcare has accelerated point of care testing (POCT) adoption, enabling quicker diagnosis and on-the-spot care across clinical and home settings. Government initiatives further support this trend. The Centers for Disease Control (CDC) highlights that digestive diseases affect millions of Americans annually, emphasizing the urgent need for reliable diagnostic tools. Meanwhile, the Food and Drug Administration (FDA) continues to promote the development and availability of point of care and home-based testing technologies.

Key Industry Highlights

|

Market Attribute |

Key Insights |

|

U.S. Gastrointestinal Point of Care Testing Market Size (2025E) |

US$ 926.0 Mn |

|

Market Value Forecast (2032F) |

US$ 1,850.9 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

10.4% |

|

Historical Market Growth (CAGR 2019 to 2024) |

9.2% |

One of the key drivers of the U.S. gastrointestinal point-of-care testing market is the rising prevalence of gastrointestinal diseases and infections that require rapid diagnosis and timely treatment. According to the Centers for Disease Control and Prevention (CDC), there are approximately 179 million cases of acute gastroenteritis in the U.S. each year. Norovirus alone accounts for an estimated 19 to 21 million illnesses, 109,000 hospitalizations, and nearly 900 deaths annually.

Additionally, bacterial infections such as Clostridioides difficile cause almost 223,900 hospitalizations and 12,800 deaths in the U.S. each year. Point-of-care tests help healthcare providers diagnose these conditions on-site, reducing the time between symptom onset and treatment. This is especially important in emergency departments, urgent care clinics, and long-term care facilities where timely diagnosis limits the spread of infection and improves outcomes. The growing trend toward decentralized healthcare, where patients receive care outside traditional settings increases the demand for portable and easy-to-use diagnostic tests. As the awareness of colorectal cancer screening increases through fecal immunochemical tests (FIT), the clinical demand for POCT procedures underscores the significance.

A key restraint in the U.S. gastrointestinal point-of-care testing market is the limited accuracy in the sensitivity and specificity of certain rapid diagnostic tests. While POCT offers convenience and speed, some tests may produce false positives or negatives, leading to misdiagnosis or delayed treatment. This can undermine clinician confidence and reduce adoption in critical care settings. Moreover, despite advancements, not all POCT devices are capable of detecting a wide range of pathogens simultaneously, limiting their use in complex gastrointestinal cases.

Regulatory challenges also act as a barrier, as approval processes for new diagnostic tools can be lengthy and complex. Reimbursement policies for POCT are not uniform across payers, and inadequate coverage may deter healthcare providers from integrating these tools into routine care. Additionally, initial costs of acquiring advanced POCT platforms can be high, especially for smaller practices and rural clinics, further limits market penetration.

The U.S. gastrointestinal point-of-care testing market presents strong growth opportunities through advancements in diagnostic technology and the increasing shift toward decentralized healthcare. One major opportunity lies in developing smartphone-compatible and digital POCT solutions, which enhance accessibility and allow patients to conduct tests at home with real-time results shared with healthcare providers. The growing popularity of telehealth services also creates a favorable environment for integrating POCT into remote care. Additionally, the emphasis on preventive healthcare and early disease detection supports the demand for non-invasive, easy-to-use tests such as fecal immunochemical tests (FIT) for colorectal cancer screening.

Expanding awareness campaigns and government-backed screening programs further drive interest in early diagnosis. Moreover, underserved rural and community health settings offer untapped potential for point-of-care diagnostic expansion, as these areas often lack access to centralized laboratories. Together, these trends highlight the market's potential for innovation and wider adoption across diverse healthcare environments.

In the U.S., gastrointestinal point-of-care testing assay kits are expected to lead the by a 41.4% market share in 2025, primarily due to their accuracy, reliability, and broad application in detecting various GI conditions such as H. pylori, Clostridioides difficile, and Salmonella. These kits, which include rapid immunoassays and molecular diagnostic tools are widely used across hospitals, clinics, and even home settings due to their convenience and ability to deliver quick results. Additionally, dipsticks represent the fastest growing segment, particularly for fecal occult blood testing (FOBT), a common non-invasive method for colorectal cancer screening. Their affordability and simplicity make them accessible in primary care and community health environments, although technological limitations have slowed their growth compared to newer formats.

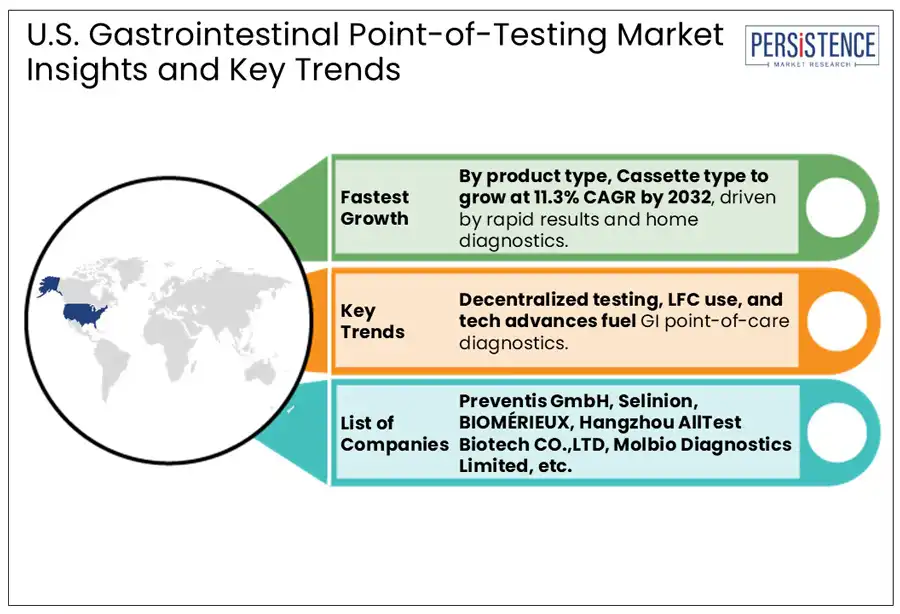

Furthermore, cassette-based tests, often built on lateral flow assay technology, are rapidly gaining momentum as the second fast-growing. Their user-friendly design and minimal sample preparation requirements make them ideal for urgent care, physician offices, and telemedicine kits.

Gastrointestinal point-of-care testing in the U.S. is primarily driven by the need to quickly identify and manage infectious diseases. Bacterial infections, such as those caused by Clostridioides difficile, Salmonella, and Helicobacter pylori, account for a large share of diagnostic demand due to their severity and potential complications. Viral infections, especially those caused by Norovirus and Rotavirus, are widespread and highly contagious, contributing to millions of cases each year. These infections often lead to outbreaks in schools, long-term care facilities, and other communal environments, highlighting the necessity of fast, on-site testing.

Parasitic infections, though less prevalent, remain important for specific populations, including travelers and immunocompromised individuals. Pathogens such as Giardia lamblia and Cryptosporidium require targeted diagnostics, particularly in clinical and public health settings. Additionally, colorectal cancer screening using fecal immunochemical tests (FIT) is gaining traction for early detection. These various indications underscore the critical role of accessible diagnostics in both treatment and prevention.

The U.S. gastrointestinal point of care testing (POCT) market is moderately competitive, with a mix of established diagnostic companies and emerging players. Leading firms such as Abbott Laboratories, QuidelOrtho Corporation, Bio-Rad Laboratories, and Thermo Fisher Scientific dominate due to their extensive product portfolios, technological innovation, and strong distribution networks. These companies focus on developing rapid, accurate, and easy-to-use diagnostic kits and devices that cater to the growing demand in clinical and home settings.

Mid-sized players and startups are also entering space, offering specialized tests and niche technologies such as microfluidics and smartphone-enabled diagnostics. Strategic partnerships, acquisitions, and continuous R&D investment are common strategies used to gain a competitive edge. Additionally, companies are aligning their offerings with regulatory guidelines to ensure faster approvals and broader market access. As demand for decentralized healthcare grows, the competition is expected to intensify with innovation and cost-effectiveness becoming key differentiators in the market.

|

Report Attribute |

Details |

|

Historical Data/Actuals |

2019 - 2024 |

|

Forecast Period |

2025 - 2032 |

|

Market Analysis Units |

Value: US$ Mn, Volume: As Applicable |

|

Segmental Coverage |

|

|

Competitive Analysis |

|

|

Report Highlights |

|

|

Customization and Pricing |

Available upon request |

By Product

By Test Type

By Indication

By Sample Type

By End-user

To know more about delivery timeline for this report Contact Sales

The U.S. gastrointestinal point of care testing market is estimated to increase from US$ 926.0 Mn in 2025 to US$ 1,850.9 Mn in 2032.

Rising GI disease burden, demand for rapid diagnostics, technological advancements, and decentralized healthcare models are fueling U.S. market growth.

The market is projected to record a CAGR of 10.4% by 2032.

Expanding home testing, AI integration, untapped rural areas, and increasing preventive screening present major opportunities for market expansion.

Major players in the U.S. Gastrointestinal Point of Care Testing market report include Preventis GmbH, Selinion, BIOMÉRIEUX, Hangzhou AllTest Biotech CO., Ltd., and Molbio Diagnostics Limited.