Comprehensive Snapshot for U.S. Durable Medical Equipment Market Including Zone and Segment Analysis in Brief.

Industry: Healthcare

Published Date: April-2025

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 120

Report ID: PMRREP35218

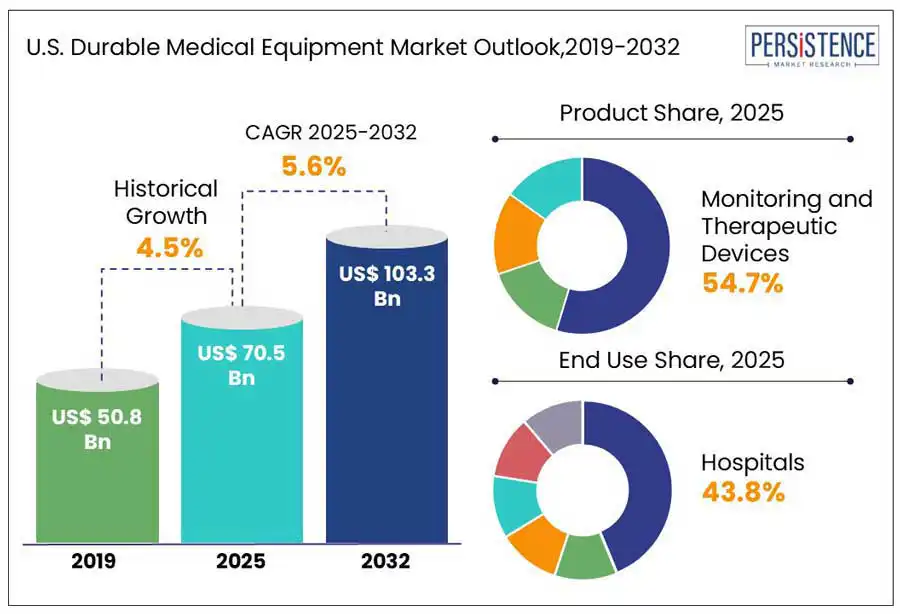

The U.S. durable medical equipment market size is projected to rise from US$ 70.5 Bn in 2025 to US$ 103.3 Bn by 2032. It is anticipated to witness a CAGR of 5.6% during the forecast period from 2025 to 2032.

Increasing prevalence of chronic diseases in the U.S. is estimated to open the door to new opportunities. America’s Health Rankings 2023 annual report, for example, stated that in 2022 alone, around 133 Mn individuals, i.e., nearly 43% of the population in the U.S., was living with one or more chronic diseases. A few major conditions, including diabetes, chronic kidney disease, arthritis, cardiovascular disease, asthma, cancer, and depression together led to the surging requirement for hospitalization, thereby boosting demand.

Key Industry Highlights

|

Market Attribute |

Key Insights |

|

U.S. Durable Medical Equipment Market Size (2025E) |

US$ 70.5 Bn |

|

Market Value Forecast (2032F) |

US$ 103.3 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.5% |

Reimbursement and policy changes in the U.S. are projected to ease access to durable medical equipment by 2032. Rapid inclination of patients toward value-based care from conventional fee-for-service models is a key factor propelling these changes. Implementation of targeted reforms by the Centers for Medicare and Medicaid Services (CMS) is also expected to help enhance confidence and extend coverage of durable medical equipment.

CMS has already put forward Durable Medical Equipment, Prosthetics, Orthotics, and Supplies (DMEPOS) Competitive Bidding Program to control costs. It helped in significantly lowering Medicare spending between 2013 and 2018 by nearly US$ 1.6 Bn. CMS suspended competitive bidding for majority of the product categories back in 2021, providing suppliers with greater flexibility and patient access. This halt enabled existing and new durable equipment suppliers to serve Medicare beneficiaries without being hampered by bidding limitations.

Adoption of durable medical equipment in the U.S. is envisioned to be hampered to a certain extent due to high patient out-of-pocket costs. It is evident among those who fall outside Medicaid or Medicare coverage eligibility, are privately insured, or underinsured. Despite being essential for regular health maintenance and functioning, durable equipment is gradually becoming unaffordable for several individuals in the country.

The Peterson-KFF Health System Tracker (2023) mentioned that individuals in the U.S. now pay an average of US$ 1,650 every year in out-of-pocket healthcare expenses. Durable equipment constitutes a significant portion of these costs for disabled and chronically ill people. Patients are liable for the remaining 20% of the approved cost of such equipment, even though Medicare Plan B pays 80% of it. This amount, when applied to high-ticket items, is anticipated to be overwhelming.

The U.S. has been facing physician shortages and rural hospital closures in recent years. It is anticipated to create new opportunities for durable medical equipment manufacturers to emphasize rural healthcare markets. Local suppliers are expected to witness high demand for at-home care solutions as rural areas are usually underserved in terms of healthcare facilities.

Chartis Center for Rural Health, for example, stated that in the U.S., more than 130 rural hospitals have shutdown operations in the past decade. It is predicted to propel demand for mobile durable medical equipment delivery services. Companies offering door-to-door delivery and remote monitoring through such equipment are likely to have high potential to reach a wide patient base across underserved areas.

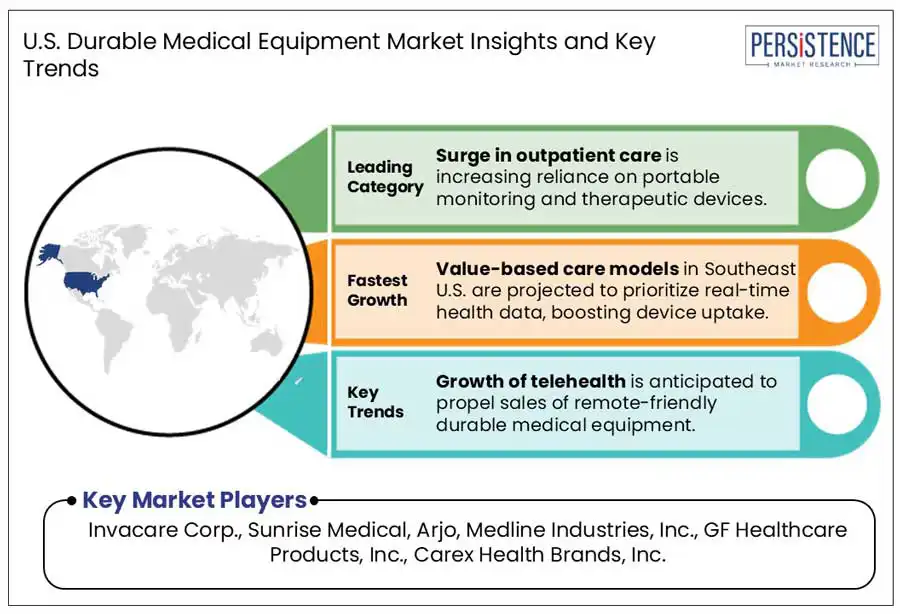

Ongoing shift toward proactive healthcare from reactive is expected to be a leading trend in the U.S. Increasing focus on predictive healthcare and preventative care has led to a high demand for durable medical equipment that aid in the management of chronic illnesses before they turn to severe issues. Continuous monitoring devices are showcasing surging demand as the prevalence of hypertension, heart disease, and diabetes continues to surge in the country.

Continuous monitoring devices enable clinicians to detect early signs of health issues, thereby initiating timely interventions to lower the risks of long-term health costs and hospitalizations. Companies are also integrating Artificial Intelligence (AI) into smart diabetes management devices to scrutinize potential health issues. Livongo Health, for instance, uses AI to offer personalized insights and coaching to patients suffering from diabetes.

Based on product, the market is segregated into personal mobility devices, bathroom safety devices and medical furniture, and monitoring and therapeutic devices. Among these, monitoring and therapeutic devices are projected to generate a share of about 54.7% in 2025, finds Persistence Market Research. Growth is attributed to rising patient preference for remote medical services or at-home treatment options over in-patient settings.

Neuromonitoring techniques are poised to become a significant part of several surgical procedures and standard medical practices. In May 2024, the Centers for Disease Control and Prevention (CDC) found that nearly 38 Mn people in the U.S. are suffering from diabetes, and around 98 Mn adults in the country are prediabetic. Hence, rising patient population living with chronic diseases in the U.S. is expected to bolster the segment.

Personal mobility devices, on the other hand, are likely to exhibit decent growth in the foreseeable future. Rising cases of mobility-related health issues are predicted to spur the segment. As per the U.S. Census Bureau, all baby boomers are estimated to fall under the age group of 65 years and older by 2030, making 1 in 5 individuals of retirement age. This rapid shift is presumed to directly affect the requirement for devices such as rollators, wheelchairs, and mobility scooters.

In terms of end-use, the market is divided into hospitals, specialty clinics, ambulatory surgical centers, diagnostic centers, and home healthcare. Out of these, hospitals are estimated to outpace the other segments by holding around 43.8% U.S. durable medical equipment share in 2025. Hospitals are typically equipped with skilled healthcare professionals and modern healthcare technology.

Increasing number of hospitals across the U.S. is another key factor speculated to propel durable medical equipment demand. Orlando Health, for example, launched the first orthopedic hospital in Florida in September 2023 to offer rehabilitation space, orthopedic care, and physician training. Hence, with rapid expansion of hospital networks, demand for durable equipment such as patient positioning devices, bedding devices, and mattresses is poised to rise.

Home healthcare is also envisioned to showcase steady growth through 2032 as it is considered a cost-effective approach for patients. Increasing desire for convenience will likely accelerate patient preference for home-based care, thereby driving demand for durable equipment.

Increasing number of senior citizens who require home healthcare services is a significant factor bolstering the West U.S. durable medical equipment market growth. Between 2020 and 2040, the number of individuals aged 65 years and over are envisioned to rise by more than 40% in California, as per a new study. This demonstrates a surging demand for sleep apnea machines, home oxygen therapy equipment, and wheelchairs.

West U.S. is further showcasing steady growth in the smart inhaler segment, especially for asthma management. However, availability of specific types of novel medical equipment will likely be limited in states such as Arizona, where access to healthcare is not as extensive as California. The Arizona Department of Health Services revealed that nearly 60% of the rural population in the state faces issues accessing healthcare, including durable medical equipment, compared to cities such as Phoenix.

Southeast U.S. is expected to account for a share of nearly 29.4% in 2025. Chronic Obstructive Pulmonary Disease (COPD) is considered a significant concern in this zone, especially in states such as Tennessee and Louisiana. The prevalence of COPD is higher in these states than the national average. Louisiana stands in the sixth position in the U.S. for COPD prevalence, according to the American Lung Association. Hence, demand for nebulizers and oxygen concentrators is estimated to remain high in these states.

North Carolina is also envisioned to witness steady growth due to the surging patient preference for home healthcare services. Under the Affordable Care Act (ACA), the state recently extended its Medicaid program. This enabled low-income patients to gain access to home healthcare services.

In the U.S. the Midwest has been seeing a rising prevalence of arthritis, cardiovascular issues, and diabetes as the zone is considered to have one of the most prominent obesity rates. These require the use of durable medical equipment. The CDC mentioned that in 2022, Ohio (35.5%), Indiana (35.3%), and Missouri (35.8%) had obesity rates above the national average. Hence, demand for extra-wide walkers, reinforced wheelchairs, insulin pumps, and CPAP machines rose significantly.

Several states in the zone have, however, faced complexities in terms of Medicaid expansion due to political resistance, thereby affecting low-income families. For instance, Kansas has not extended Medicaid under the ACA. Kansas Health Institute revealed that around 130,000 low-income patients were devoid of affordable health coverage in 2022, including reimbursement for breathing aids and orthopedic braces.

Leading companies in the U.S. durable medical equipment market are focusing on developing innovative products infused with novel technologies. The market houses various local suppliers, distributors, and renowned manufacturers striving to obtain a high share. A few companies are aiming to provide cost-effective equipment with remote usability. Some of the emerging players are embracing strategies such as mergers and acquisitions and collaborations to strengthen their presence.

|

Report Attribute |

Details |

|

Historical Data/Actuals |

2019 - 2024 |

|

Forecast Period |

2025 - 2032 |

|

Market Analysis Units |

Value: US$ Bn/Mn, Volume: As Applicable |

|

Geographical Coverage |

|

|

Segmental Coverage |

|

|

Competitive Analysis |

|

|

Report Highlights |

|

|

Customization and Pricing |

Available upon request |

By Product

By End-use

By Region

To know more about delivery timeline for this report Contact Sales

The U.S. durable medical equipment market is projected to be valued at US$ 70.5 Bn in 2025.

Rapid changes in reimbursement policies and increasing prevalence of chronic illnesses are the key market drivers.

The market is poised to witness a CAGR of 5.6% from 2025 to 2032.

Closure of hospitals in rural areas and increasing shift toward proactive healthcare are the key market opportunities.

Invacare Corp., Sunrise Medical, Arjo, and Medline Industries, Inc. are a few key players.