- Bulk Chemicals

- U.S. and Canada Chemical Palliatives for Dust Suppression Market

U.S. and Canada Chemical Palliatives for Dust Suppression Market Size, Share, and Growth Forecast 2026 - 2033

U.S. and Canada Chemical Palliatives for Dust Suppression Market by Product Type (Water Absorbing Products (Magnesium Chloride, Calcium Chloride), Organic Nonpetroleum Products (Lignosulfate, Tall Oil Products, Molasses/Sugar Beet Products, Animal Fats, Vegetable Oil), Synthetic Polymer Products (Acrylic Co-polymers, Polyvinyl Acetates), Synthetic Fluids and Others) By Form (Powder, Liquid), Application (Haul Road Dust Suppression, High Traffic Area Dust Suppression, Stockpile Dust Suppression, Others), and Regional Analysis, 2026 - 2033

U.S. and Canada Chemical Palliatives for Dust Suppression Market Size and Trend Analysis

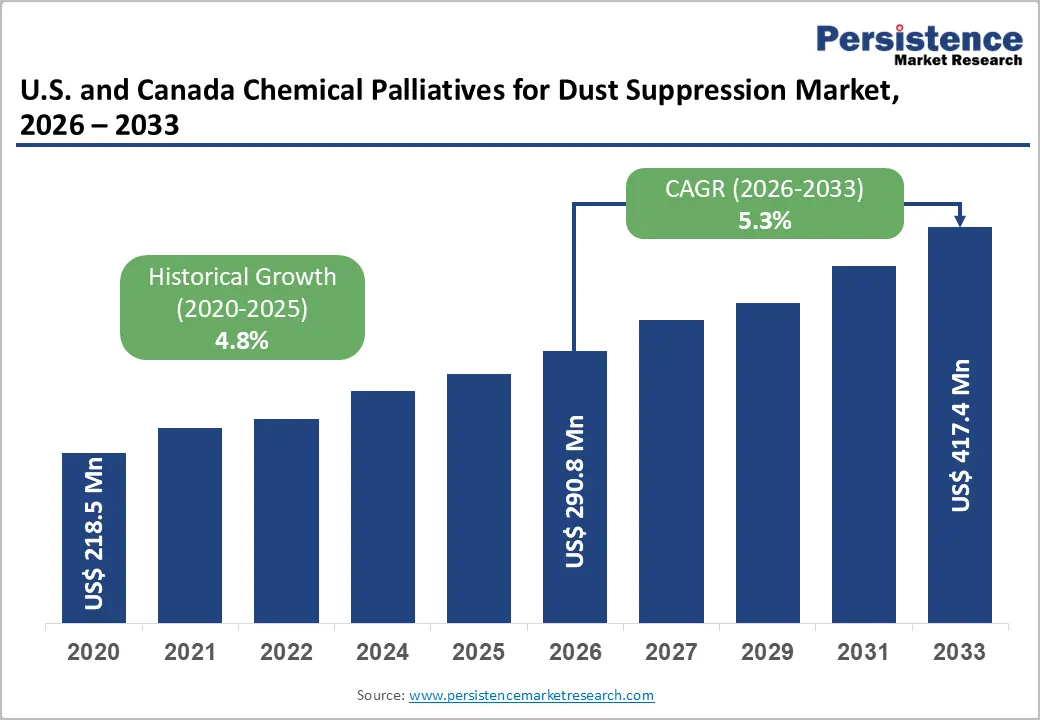

The U.S. and Canada chemical palliatives for dust suppression market size is likely to be valued at US$ 290.8 million in 2026 and is projected to reach US$ 417.4 million by 2033, growing at a CAGR of 5.3% between 2026 and 2033. This steady market trajectory is underpinned by demand from the mining, construction, and transportation sectors, where regulatory enforcement of fugitive dust emission standards is compelling operators to adopt advanced chemical palliative programs.

The U.S. Environmental Protection Agency (EPA) National Ambient Air Quality Standards (NAAQS) for PM10 and PM2.5 particulate matter create non-negotiable compliance requirements for industrial facilities managing unpaved haul roads, stockpiles, and open areas.

Key Industry Highlights:

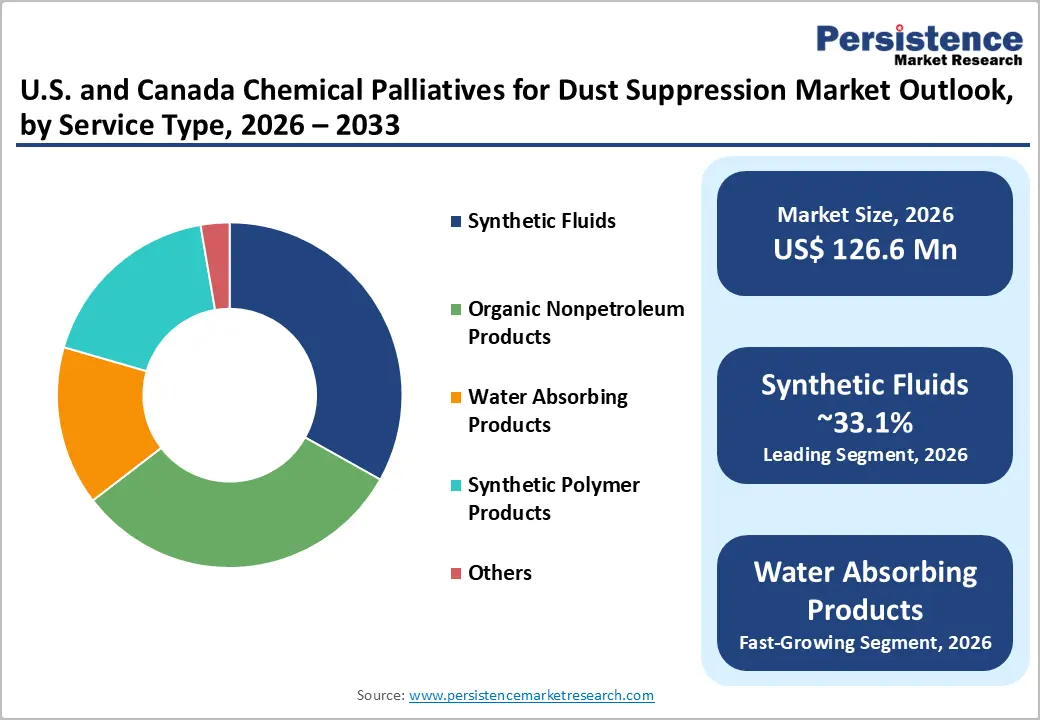

- Leading Product Type: Synthetic Fluids lead the product type segment at 33.1% market share in 2026, while Water Absorbing Products are the fastest growing sub-segment, driven by cost accessibility for smaller operators and pre-approved status across multiple U.S. state DOT and federal land management agency specifications.

- Leading Form Type: Liquid formulations dominate with 56.5% form share in 2026, reflecting operational advantages in large-scale industrial applications, and Powder formulations represent the fastest growing form segment through logistics advantages in remote mine site deployment scenarios.

- Leading Application: Haul road dust suppression leads application demand at 30.7% share in 2026, driven by MSHA/EPA regulatory requirements at surface mines; Airborne Dust Suppression is the fastest growing application, accelerated by the EPA's 2024 PM2.5 NAAQS revision to 9 µg/m³ and CARB BACM mandates in California.

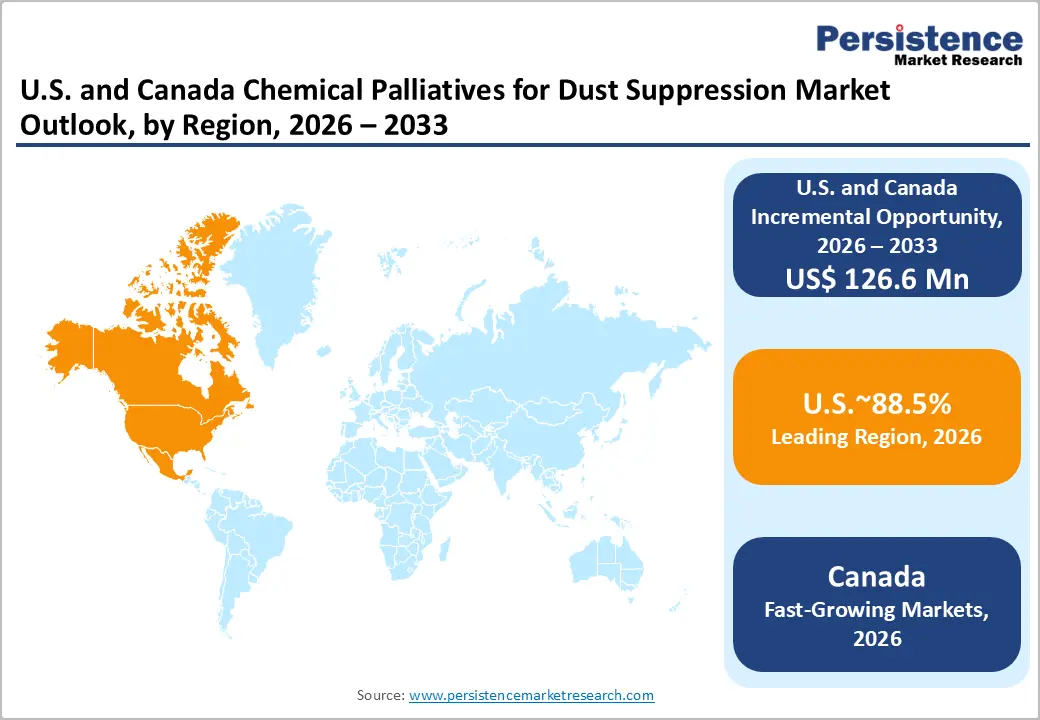

- Leading Country: The United States commands 88.5% of combined market revenue in 2026, underpinned by the FHWA's documented 2.3 million unpaved road miles and EPA/MSHA regulatory compliance requirements

DRO Analysis

EPA Regulatory Enforcement of PM2.5/PM10 Standards Mandating Chemical Dust Control Programs

The U.S. and Canada Chemical Palliatives for Dust Suppression Market is fundamentally shaped by the U.S. EPA's enforceable air quality standards that make chemical dust suppression a compliance imperative rather than an operational choice. The EPA's 2024 revision of the PM2.5 annual standard to 9 µg/m³, the most significant tightening in over two decades, significantly expands the number of industrial facilities required to implement dust suppression programs to achieve attainment. Facilities operating unpaved haul roads, active mining operations, and material stockpiles must demonstrate compliance through Best Available Control Technology (BACT) documentation.

Under Title V Operating Permits and Title I New Source Review of the Clean Air Act, facilities in non-attainment areas must implement Reasonably Available Control Technology (RACT), including chemical palliative applications. In 2023, the EPA finalised revised NAAQS requiring states to submit revised State Implementation Plans (SIPs). The Mine Safety and Health Administration (MSHA) additionally enforces dust control requirements at surface coal and metal/nonmetal mines across the U.S., creating a parallel compliance demand driver.

Canada's Canadian Ambient Air Quality Standards (CAAQS) for PM2.5 at 8.8 µg/m³ by 2025 create equivalent enforcement pressure in British Columbia, Alberta, and Ontario industrial operations.

Infrastructure Investment Programs Generating Unpaved Road and Construction Dust Control Demand

The passage of the U.S. Infrastructure Investment and Jobs Act (IIJA) in 2021, authorising US$1.2 trillion in infrastructure spending over a decade, is creating a sustained multi-year wave of construction site and unpaved access road dust suppression demand across highway, bridge, and utilities construction programs. Large-scale construction projects typically generate PM10 and PM2.5 dust loadings requiring chemical palliative application under National Pollution Discharge Elimination System (NPDES) stormwater and dust control permits.

The U.S. and Canada Chemical Palliatives for Dust Suppression Market is directly benefiting from project proliferation across the Western U.S. states, California, Nevada, Arizona, Utah, where low precipitation and high wind speed amplify fugitive dust generation from unpaved surfaces.

The Federal Highway Administration (FHWA) estimates approximately 2.3 million miles of unpaved roads in the U.S., representing the largest addressable application surface for chemical dust palliatives. Mining and aggregate production operations in Nevada, Arizona, and Wyoming, among the nation's largest producing states, require year-round dust suppression programs per state-level AQMD (Air Quality Management District) rules. Canada's Natural Resources Canada documents active mining operations across 1,200-plus mine sites requiring dust management compliance programs, sustaining consistent industrial demand for both liquid and powder chemical palliatives in the Canadian market.

Restraints - Environmental and Toxicological Concerns Restricting Chloride-Based Product Application

Magnesium chloride and calcium chloride, two of the most widely used water-absorbing dust palliative products, face application restrictions in ecologically sensitive areas due to their documented toxicity to roadside vegetation and potential for groundwater chloride accumulation.

The U.S. Forest Service and multiple state transportation agencies have implemented application rate limits and setback requirements from water bodies for chloride-based dust suppressants following studies documenting adverse impacts on native vegetation and soil structure. For operators managing dust near waterways, wetlands, or protected lands, these restrictions narrow the approved product spectrum, increasing program complexity and potentially requiring more costly synthetic polymer or organic alternatives.

Opportunities - Synthetic Polymer-Based Palliatives for Long-Duration Performance in High-Erosion Environments

A high-value opportunity exists for chemical palliative manufacturers offering next-generation synthetic polymer formulations, specifically acrylic co-polymer and polyvinyl acetate products, that provide extended service life of 6–12 months between application cycles versus the 1-4 week intervals required by water-absorbing chloride-based products. This performance advantage directly reduces total annual application program cost and compliance management complexity for operators managing large surface areas. The U.S. and Canada Chemical Palliatives for Dust Suppression Market is at an inflexion point where total cost of ownership analysis is compelling procurement upgrades from commodity chloride products to premium performance polymer palliatives.

The Western Governors' Association's dust management framework and BLM (Bureau of Land Management) right-of-way permit requirements increasingly specify documented treatment effectiveness duration, a metric that polymer palliatives consistently outperform chloride alternatives on. Federal lands management agencies in Arizona, Nevada, California, and New Mexico, representing millions of acres of surface mining and energy development activity, present specific opportunity for polymer palliative product positioning, particularly where environmental sensitivity near waterways precludes chloride-based alternatives.

Airborne Dust Suppression Technology for PM2.5 Compliance Near Sensitive Receptors

The EPA's 2024 PM2.5 standard revision to 9 µg/m³ down from 12 µg/m³ creates immediate compliance pressure for industrial facilities adjacent to residential communities and schools that are now classified in non-attainment under the revised standard. This regulatory development opens a high-priority opportunity for airborne dust suppression chemical palliative applications, including misting system chemical additives, canopy suppression programs, and boundary perimeter treatment that specifically address fugitive PM2.5 emissions from stockpile and active processing areas.

The U.S. and Canada Chemical Palliatives for Dust Suppression Market stands to benefit as facilities revise their Title V permit emission inventories to demonstrate compliance.

The California Air Resources Board (CARB), with the nation's most stringent PM2.5 and PM10 local rules across its 35 Air Quality Management Districts, has mandated chemical palliative programs at aggregate operations, construction sites, and unpaved lots as fugitive dust Best Available Control Measures (BACM) under multiple areas adopted Dust Control Plans. San Joaquin Valley APCD's Rule 4550 and South Coast AQMD's Rule 403 explicitly require chemical stabilisation as approved dust control measures, creating a regulatory-mandate procurement channel that directly supports speciality palliative product development targeting PM2.5-specific control efficiency documentation.

Category-wise Analysis

Product Type Insights

Synthetic fluids hold the leading product type position at approximately 33.1% market share in 2026, a dominance rooted in the segment's superior combination of long-duration efficacy, compatibility with diverse application conditions (extreme temperature ranges, freeze-thaw cycling), and compliance with increasingly stringent ecological sensitivity requirements that restrict chloride-based alternatives.

Synthetic fluid palliatives formulated from petroleum-derived or bio-based speciality chemical carriers form flexible, durable surface binding films that maintain structural integrity across the temperature extremes of the U.S. and Canadian mining and construction environments from sub-zero Canadian prairie winters to Arizona desert summers. The U.S. Bureau of Reclamation and Western states DOTs have documented synthetic fluid palliatives as the preferred specification for permanent access road treatments where repeated application is impractical.

Water Absorbing Products, including magnesium chloride and calcium chloride, are the fastest growing product type segment, projected to expand at above-average CAGR through 2033, driven by cost accessibility for smaller operators and the segment's established approval across multiple state DOT and BLM regulatory frameworks as a pre-approved chemical palliative for unpaved road dust control programs.

Application Insights

Haul road dust suppression commands the application category at approximately 30.7% market share in 2026, reflecting the structural reality that haul roads are the single highest-frequency dust generation source in surface mining, quarrying, and large construction projects, with heavy truck traffic exceeding 100 plus daily pass cycles on active mining haul roads capable of generating PM10 concentrations dramatically exceeding NAAQS limits without treatment.

The MSHA and EPA both identify unpaved haul roads as a primary fugitive dust emission source requiring documented control programs in surface mining Operations Plans. Haul road treatments typically require application every 1-14 days, depending on product type, traffic intensity, and precipitation, creating a recurring, high-frequency procurement cycle that sustains this application segment's market leadership.

Airborne Dust Suppression is the fastest growing application segment, driven by the EPA's 2024 PM2.5 standard revision, creating compliance urgency for facilities adjacent to residential communities, and CARB's BACM requirements in California, mandating chemical palliative programs at aggregate and construction sites across the nation's most air-quality-regulated state.

Country Insights

U.S. Chemical Palliatives for Dust Suppression Market Trends and Insights

The United States accounts for approximately 88.5% of the combined U.S. and Canada market revenue in 2026, establishing it as the overwhelmingly dominant national market for chemical dust palliatives in North America. This dominance reflects the scale of the U.S. industrial complex, particularly its surface mining, aggregate production, construction, and energy sectors, combined with the world's most extensively regulated ambient air quality enforcement framework that makes chemical dust suppression a compliance-driven, non-discretionary operational expenditure.

The EPA's 2024 revision of the annual PM2.5 NAAQS to 9 µg/m³, likely to be effective in the near future for most areas, is the most significant regulatory development affecting U.S. dust suppression procurement in recent years. This revision reclassifies numerous counties as non-attainment, triggering SIP revision requirements that mandate chemical palliative programs at industrial facilities contributing to area PM2.5 loadings. The FHWA's documentation of 2.3 million unpaved road miles, primarily in Western and rural states, identifies the scale of the addressable application surface.

Canada Chemical Palliatives for Dust Suppression Market Trends and Insights

Canada is a key demand centre in North America’s dust suppression market, driven by large-scale oil sands surface mining in Alberta and extensive metallic mining activities across Ontario and British Columbia, where continuous haul road operations require chemical palliatives for operational stability and dust control. Strict air quality regulations under Canada’s CAAQS PM2.5 standards (8.8 µg/m³ by 2025) further reinforce compliance-driven adoption across industrial and construction sites.

The presence of over 1,200 active mine sites nationwide and ongoing expansion in oil sands and critical mineral projects continues to support sustained market demand, with steady long-term growth expected through 2033.

Competitive Landscape

The U.S. and Canada chemical palliatives for dust suppression market exhibit a moderately fragmented competitive structure, with a mix of large speciality chemical companies serving national and international accounts alongside regional suppliers serving local industrial clusters. Key market participants include Dustrol, Inc., Midwest Industrial Supply, Inc., Cargill Road Solutions, Envirofluid Group, Sripath Technologies, and Applied Dust Control, Inc.

The dominant competitive strategies in this market are regulatory compliance documentation capability (enabling OEM procurement at permitted industrial facilities), technical application engineering support (optimising treatment protocols for site-specific conditions), and environmental certification differentiation (NSF/ANSI 60, USDA BioPreferred) that opens federal lands and water-adjacent application procurement channels close to conventional chloride-based products. Product longevity documentation is emerging as the key differentiator for premium palliative positioning.

Key Developments:

- In 2024, sustainable dust control and road stabilisation solutions gained strong traction with the advancement of Borregaard ASA’s lignin-based biopolymer Dustex®, a cost-effective and environmentally friendly alternative to conventional suppressants. Derived from lignin, a natural wood fibre binder, Dustex demonstrated superior soil binding and stabilisation performance, making it highly effective for both dust suppression and unpaved road applications.

U.S. and Canada Chemical Palliatives for Dust Suppression Market Report-Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 218.5 Mn |

| Current Market Value (2026) | US$ 290.8 Mn |

| Projected Market Value (2033) | US$ 417.4 Mn |

| CAGR (2026 - 2033) | 5.3% |

| Leading Country | United States, 88.5% share |

| Dominant Product Type | Synthetic Fluids, 33.1% share |

| Top-ranking Application | Haul Road Dust Suppression, 30.7% |

| Incremental Opportunity | US$ 126.6 Mn |

Companies Covered in U.S. and Canada Chemical Palliatives for Dust Suppression Market

- Arboris, LLC

- Borregaard

- Cargill, Incorporated

- Cypher Environmental

- Quaker Houghton (Quaker Chemical Corp.)

- Ecolab Inc. (Nalco Water)

- FUCHS Group

- BASF SE

- Archer Daniels Midland (ADM)

- Huntsman International LLC

- Hexion Inc.

- Arclin, Inc.

- Pine Chemical Group

- Norcal Ag Service

- Telfer Pavement Technologies, LLC

Frequently Asked Questions

The U.S. Chemical Palliatives for Dust Suppression Market is projected to be valued at US$ 290.8 Mn in 2026.

Synthetic Fluids leads to service type demand at 33.1% share, anchored by its superior surface sealing performance, long-lasting dust control efficiency, and widespread adoption across mining haul roads, high-traffic industrial zones, and infrastructure projects.

The Haul Road Dust Suppression segment holds the largest share of the U.S. Chemical Palliatives for Dust Suppression market, driven by extensive usage in mining operations, heavy industrial transport routes, and unpaved roads requiring continuous dust control.

The U.S. chemical palliatives for dust suppression market is expected to witness a CAGR of 5.3% from 2026 to 2033.

The U.S. and Canada Chemical Palliatives for Dust Suppression market is primarily driven by stringent EPA and CAAQS PM2.5/PM10 regulatory enforcement mandating chemical dust control as a compliance requirement, alongside large-scale infrastructure investments under the IIJA and extensive mining, construction, and unpaved road networks that continuously generate fugitive dust requiring sustained suppression programs.

The key market opportunities in the U.S. and Canada Chemical Palliatives for Dust Suppression market include the growing adoption of synthetic polymer-based palliatives for long-duration, cost-efficient dust control and increasing demand for advanced airborne dust suppression solutions driven by stricter PM2.5 compliance regulations and regional environmental mandates such as CARB and BLM.

Key players in the U.S. and Canada Chemical Palliatives for Dust Suppression Market include Cargill, Incorporated, Borregaard ASA, Quaker Houghton (Quaker Chemical Corporation), BASF SE, Cypher Environmental Ltd., Ecolab Inc., Arboris, LLC, and Archer Daniels Midland Company, among others.