- Beverages

- Fruit Infused Water Market

Fruit Infused Water Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Fruit Infused Water Market by Product Type (Still Flavored Water, Sparkling Flavored Water), Nature (Organic, Conventional), Flavor (Apple, Mango, Orange, Pineapple, Strawberry, Watermelon, Berries, Citrus Fruits), Distribution Channel (B2B, B2C), and Regional Analysis from 2026 to 2033

Fruit Infused Water Market Size and Share Analysis

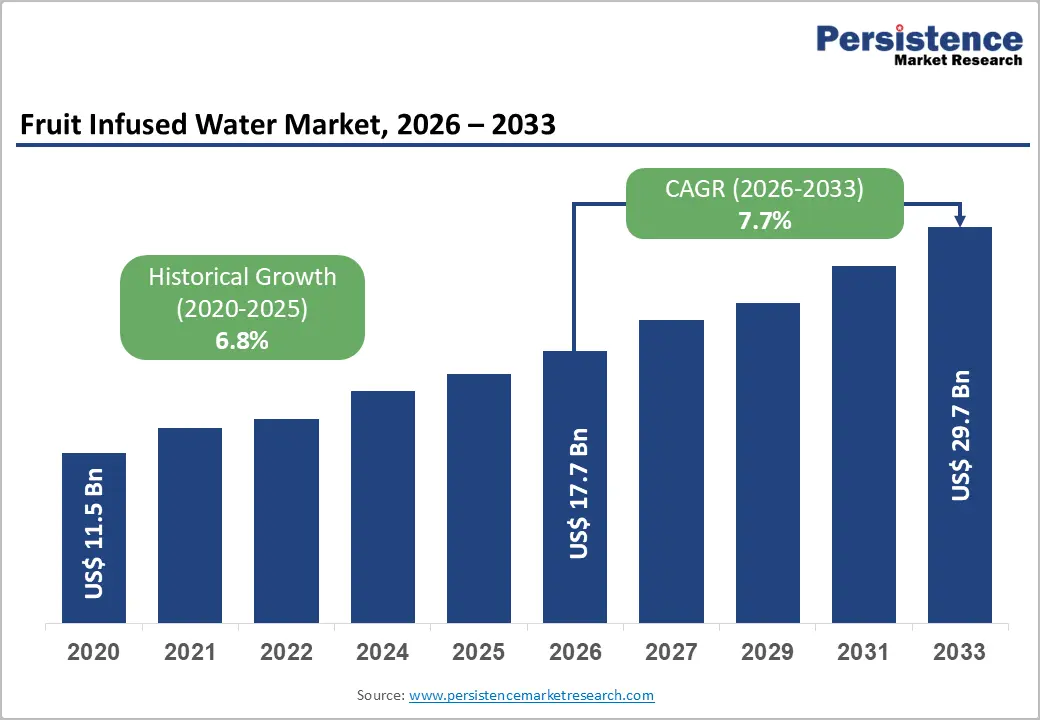

The global fruit infused water market is estimated to grow from US$ 17.7 Bn in 2026 to US$ 29.7 Bn by 2033. The market is projected to record a CAGR of 7.7% during the forecast period from 2026 to 2033.

The global fruit infused water market is experiencing steady growth, driven by rising health awareness, demand for low-calorie beverages, and preference for natural, clean-label drinks. North America dominates due to strong functional beverage consumption, while Asia-Pacific is the fastest-growing region, supported by urbanization, lifestyle shifts, and increasing health-conscious consumers.

Key Industry Highlights

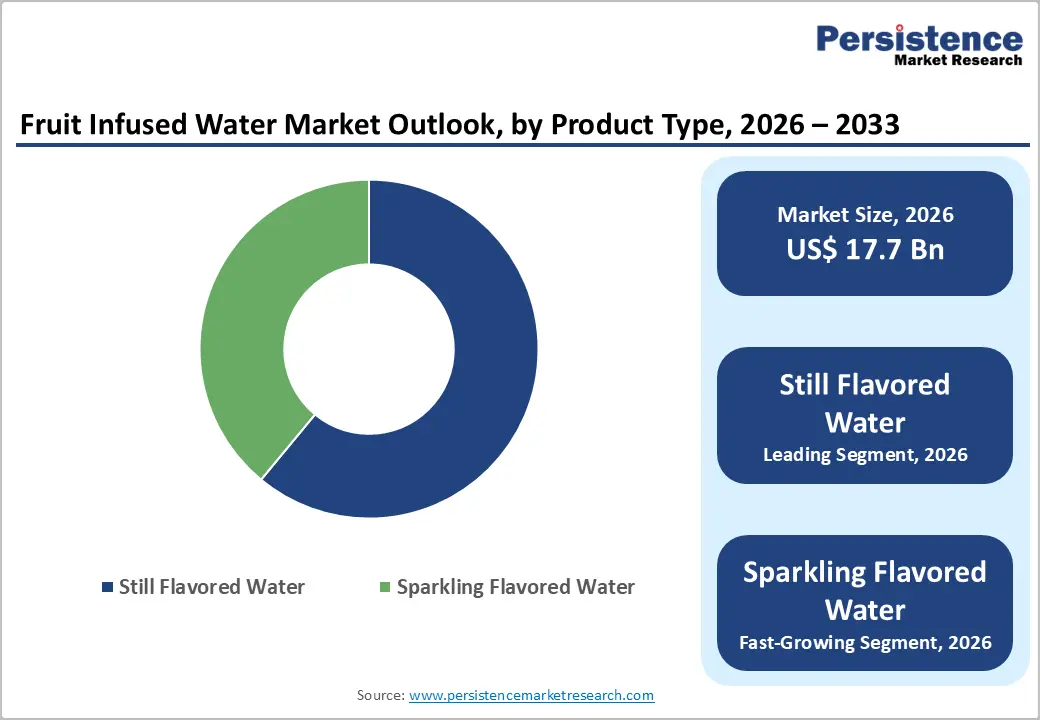

- Dominant Segment: Still flavored water held the largest share 61.0% in 2025, driven by high daily consumption, convenience, and preference for non-carbonated, natural hydration options.

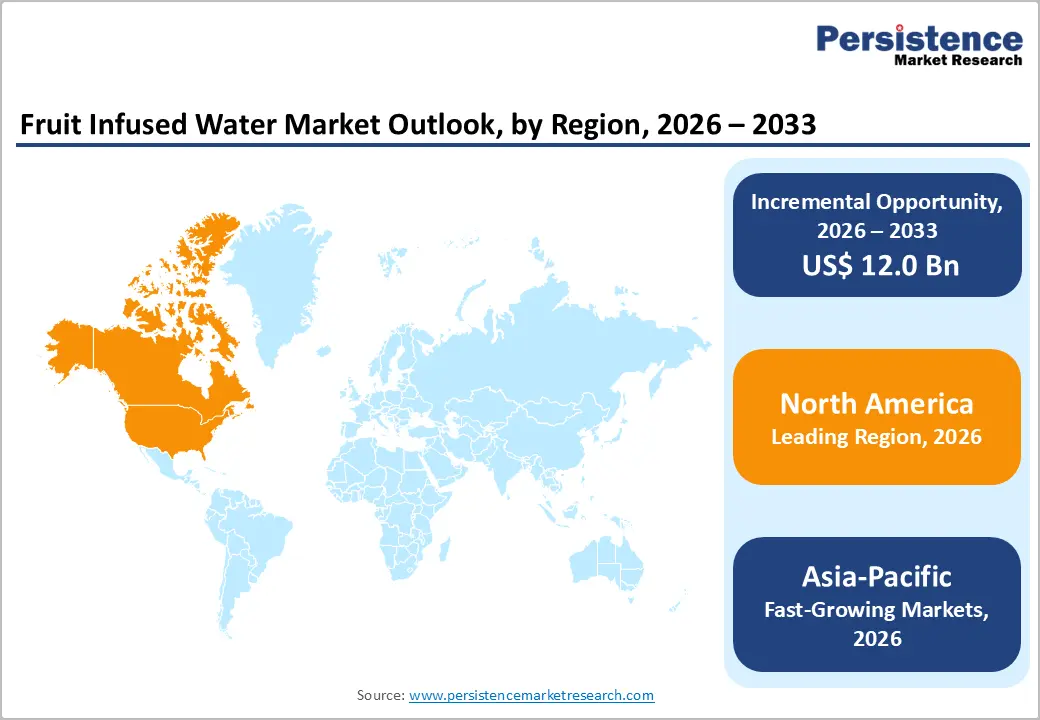

- Dominant Region: North America led the market in 2025 with 40.6% share, supported by strong demand for functional beverages and widespread availability of premium infused water brands.

- Market Drivers: Growth is driven by rising health consciousness, demand for low-calorie beverages, increasing preference for natural ingredients, and shift away from sugary carbonated drinks.

- Market Opportunity: Opportunities exist in organic and clean-label products, expansion in Asia-Pacific, innovative flavor combinations, functional ingredient infusion, and growing demand for premium and wellness beverages.

| Global Market Attributes | Key Insights |

|---|---|

| Global Fruit Infused Water Market Size (2026E) | US$ 17.7 Bn |

| Market Value Forecast (2033F) | US$ 29.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.8% |

Market Dynamics

DRIVER: Increasing Health and Wellness Awareness Among Consumers

Rising health awareness is a primary driver of the fruit infused water market, as consumers actively reduce sugar intake and shift toward healthier hydration options. According to the Centers for Disease Control and Prevention (CDC), about 49% of U.S. adults consume sugar-sweetened beverages daily, which are strongly linked to obesity, type 2 diabetes, and heart disease. This widespread consumption has triggered public health campaigns encouraging reduced sugar intake. As a result, consumers are increasingly replacing sugary drinks with low-calorie, natural alternatives like fruit infused water that provide flavor without added sugars.

Additionally, global dietary trends reflect a broader transition toward preventive healthcare and clean-label consumption. The CDC also reports that over 60% of adults are trying to reduce sugar intake, reinforcing the demand for healthier beverage alternatives. At the same time, countries like Australia have seen sugary drink consumption decline from 49.2% in 1995 to 28.9% in 2023, indicating a structural shift toward healthier beverages. Fruit infused water aligns directly with these trends, offering hydration, natural ingredients, and perceived wellness benefits, making it highly attractive to health-conscious consumers globally.

RESTRAINT: High Product Cost Compared to Regular Bottled Water

High product cost remains a key restraint in the fruit infused water market, limiting its penetration, especially in price-sensitive regions. Unlike standard bottled water, fruit infused water requires fresh fruit extracts, natural flavoring, and preservative-free processing, which significantly increases production costs. These products often also rely on sustainable or premium packaging, further elevating prices. As a result, manufacturers face challenges in maintaining competitive pricing compared to conventional bottled water or low-cost flavored beverages.

From a consumer behavior perspective, price sensitivity plays a major role in beverage choices. Government-backed consumption data shows that despite health risks, a large proportion of consumers continue to purchase sugary drinks due to affordability and availability. For instance, the CDC reports that 63% of adults consume sugary beverages at least once daily, highlighting that low-cost alternatives still dominate purchasing decisions. This indicates that although healthier options like infused water are preferred, their premium pricing can hinder mass adoption, particularly in developing markets where affordability outweighs health considerations.

OPPORTUNITY: Rising Demand for Organic and Clean-Label Infused Water

The growing demand for organic and clean-label products presents a significant opportunity in the fruit infused water market. Consumers are increasingly seeking beverages made with natural, recognizable ingredients and minimal processing, avoiding artificial additives and preservatives. This shift is supported by rising awareness of food transparency and ingredient safety. Clean-label beverages, including organic infused water, are perceived as safer and healthier, particularly among urban and younger populations who prioritize wellness and sustainability in purchasing decisions.

Supporting this trend, public health data indicates a strong behavioral shift toward healthier consumption patterns. The CDC highlights that more than 60% of adults are actively reducing sugar intake, reflecting a broader move toward natural and minimally processed products. Additionally, declining consumption of sugary drinks in countries like Australia further reinforces this transition toward clean-label beverages. This creates a favorable environment for organic infused water brands to expand, innovate with plant-based ingredients, and position themselves in premium and functional beverage segments, unlocking strong growth potential globally.

Category-wise Analysis

By Product Type, Still Flavored Water Dominates the Fruit Infused Water Market

Still flavored water dominates with 61.0% share due to strong consumer preference for natural, non-carbonated hydration. According to the Centers for Disease Control and Prevention (CDC), adults consume significant amounts of plain water daily, reflecting reliance on still water for hydration. Health agencies also emphasize water as the healthiest beverage, supporting its widespread acceptance. Unlike carbonated drinks, still water is easier to consume in large quantities and does not cause bloating or discomfort. Additionally, rising concerns over sugar intake, linked to obesity and diabetes have pushed consumers toward zero-calorie alternatives. Flavored still water provides taste without carbonation or additives, making it more suitable for daily consumption across all age groups.

By Nature, Conventional Dominates the Fruit Infused Water Market

Conventional fruit infused water dominates due to its affordability and large-scale availability. Compared to organic products, conventional variants use cost-efficient ingredients and established supply chains, allowing competitive pricing. According to the Centers for Disease Control and Prevention (CDC), many consumers still prioritize cost and accessibility in beverage choices, contributing to continued demand for affordable options. Additionally, global health organizations emphasize increasing overall water intake rather than specific product types, supporting conventional consumption. Organic infused water, while growing, remains premium-priced and less accessible, particularly in developing regions. As a result, conventional products lead due to their mass-market appeal, wider distribution, and ability to meet high-volume consumer demand.

Regional Insights

North America Fruit Infused Water Market Trends

North America dominates due to strong health awareness and high consumption of alternative beverages. According to the Centers for Disease Control and Prevention (CDC), about 49% of U.S. adults consume sugary drinks daily, which are linked to obesity, diabetes, and heart disease. This has driven a major shift toward healthier substitutes like infused water. Additionally, public health campaigns such as “Rethink Your Drink” actively promote replacing sugary beverages with water or flavored water alternatives.

Moreover, declining sugar consumption further supports this transition. Recent data shows sugar consumption in the U.S. has decreased by 4.4% in recent years, reflecting changing dietary habits. High disposable income, strong retail infrastructure, and early adoption of functional beverages reinforce market leadership, making North America the dominant region.

Europe Fruit Infused Water Market Trends

Europe is a key region due to strong regulatory pressure on sugar reduction and growing demand for healthy hydration. The World Health Organization (WHO) highlights that sugary drinks are major contributors to non-communicable diseases, prompting many European countries to introduce sugar taxes and reformulation policies. This has accelerated the shift toward low-calorie beverages like infused water.

Additionally, recent industry data shows Europe’s bottled water market grew by 5% in value and 3% in volume, driven by increasing consumer awareness of healthy hydration. Countries like the UK and France are witnessing rapid adoption of water-based beverages due to lifestyle changes and on-the-go consumption, positioning Europe as a mature yet steadily growing market.

Asia-Pacific Fruit Infused Water Market Trends

Asia-Pacific is the fastest-growing region due to rapid urbanization and changing dietary patterns. Governments and health bodies across the region are increasingly addressing rising obesity and diabetes rates linked to sugary beverage consumption. The World Health Organization (WHO) reports that sugary drink consumption contributes significantly to non-communicable diseases, which are increasing in developing economies.

Additionally, population growth and income expansion are key drivers. Asia-Pacific houses over 50% of the global population, leading to a massive consumer base for healthier beverages. As urban consumers adopt westernized lifestyles, demand for convenient, low-calorie drinks is rising. Combined with increasing awareness of fitness and wellness, this is accelerating the adoption of fruit infused water across emerging economies like India and China.

Competitive Landscape:

The fruit infused water market is competitive, led by key players focusing on flavor innovation, clean-label formulations, and functional hydration benefits. Companies prioritize expanding product portfolios, enhancing production capacity, ensuring regulatory compliance, and strengthening distribution networks to meet rising demand across beverages, fitness, wellness, and on-the-go consumption segments globally.

Key Industry Developments:

- In April 2026, Nestlé introduced “Inspired by Buxton Peak,” a new premium range under its Buxton brand, expanding its presence in the flavored and infused water segment. The launch focused on naturally inspired flavors, targeting consumers seeking healthier, low-calorie hydration alternatives with a premium positioning.

- In January 2026, PepsiCo introduced two limited-time flavors to its fan-favorite beverage lineup, aiming to boost consumer engagement and drive seasonal demand. The launch targeted younger consumers and loyal brand followers by offering new, exciting taste experiences for a limited duration.

Companies Covered in Fruit Infused Water Market

- Nestle Group

- PepsiCo, Inc.

- The Coco Cola Company

- Treo Brands LLC.

- Dr. Pepper Snapple Group

- Eslena LLC

- Hint Inc.

- Just Good, Inc.

- Core Nutrition, LLC

- Propel Water

- Dash-Water

- Spindrift

- Gloe Water

- Perrier

- Ocean Spray

- Others

Frequently Asked Questions

The global fruit infused water market is projected to be valued at US$ 17.7 Bn in 2026.

Rising health awareness, demand for low-calorie beverages, clean-label trends, and shift from sugary drinks.

The global fruit infused water market is poised to witness a CAGR of 7.7% between 2026 and 2033.

Organic products growth, emerging markets expansion, innovative flavors, functional ingredients, and premium beverage demand.

Nestle Group, PepsiCo, Inc., The Coco Cola Company, Treo Brands LLC., Dr. Pepper Snapple Group, Eslena LLC.