- Healthcare Services

- Vaccine Storage Equipment Market

Vaccine Storage Equipment Market Size, Share, Growth Forecast, 2026 - 2033

Vaccine Storage Equipment Market by Product (Ice-Lined Refrigerators (ILRs), Deep Freezers (DFs), Cold Boxes, Vaccine Carriers, Solar-Powered Refrigerators, Others), End-user (Hospitals and Clinics, and Others), and Regional Analysis for 2026 - 2033

Vaccine Storage Equipment Market Share and Trends Analysis

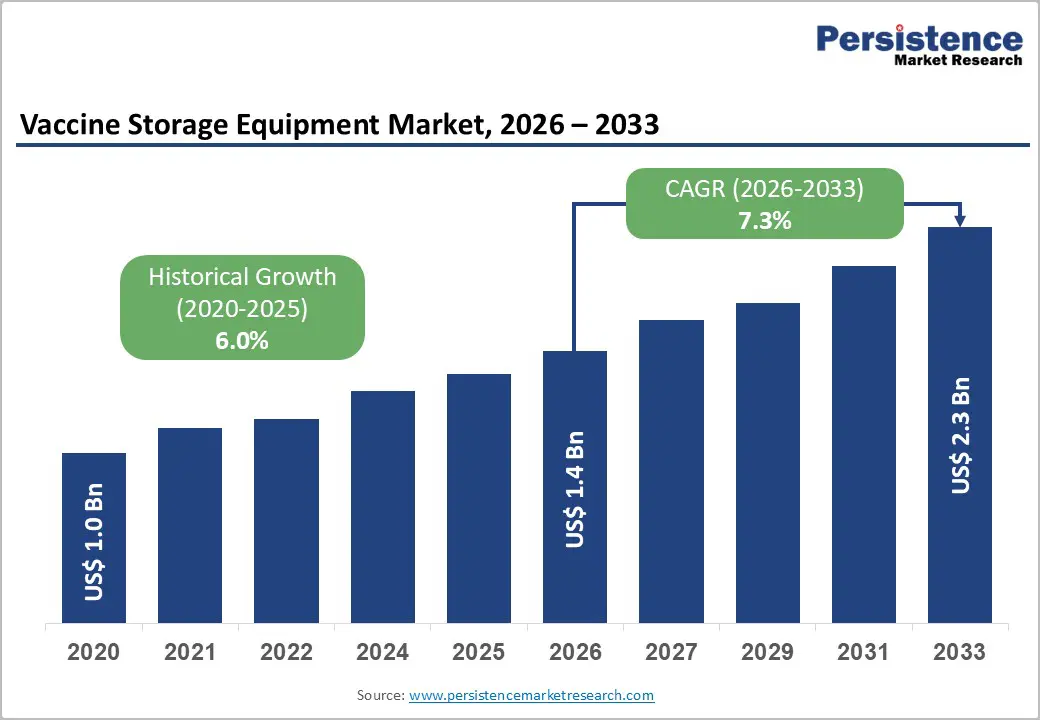

The global vaccine storage equipment market size is likely to be valued at US$1.4 billion in 2026 and is projected to reach US$2.3 billion by 2033, growing at a CAGR of 7.3% during the forecast period from 2026 to 2033, driven by strengthening global immunization programs, rising demand for cold chain logistics infrastructure, and increasing deployment of temperature-sensitive biologics.

According to WHO and UNICEF immunization supply chain initiatives, expanded vaccine coverage in emerging economies continues to increase demand for reliable refrigeration systems. Additionally, post-pandemic investments in healthcare resilience and stricter vaccine cold storage compliance standards are reinforcing procurement cycles across public health systems and private healthcare providers.

Key Industry Highlights:

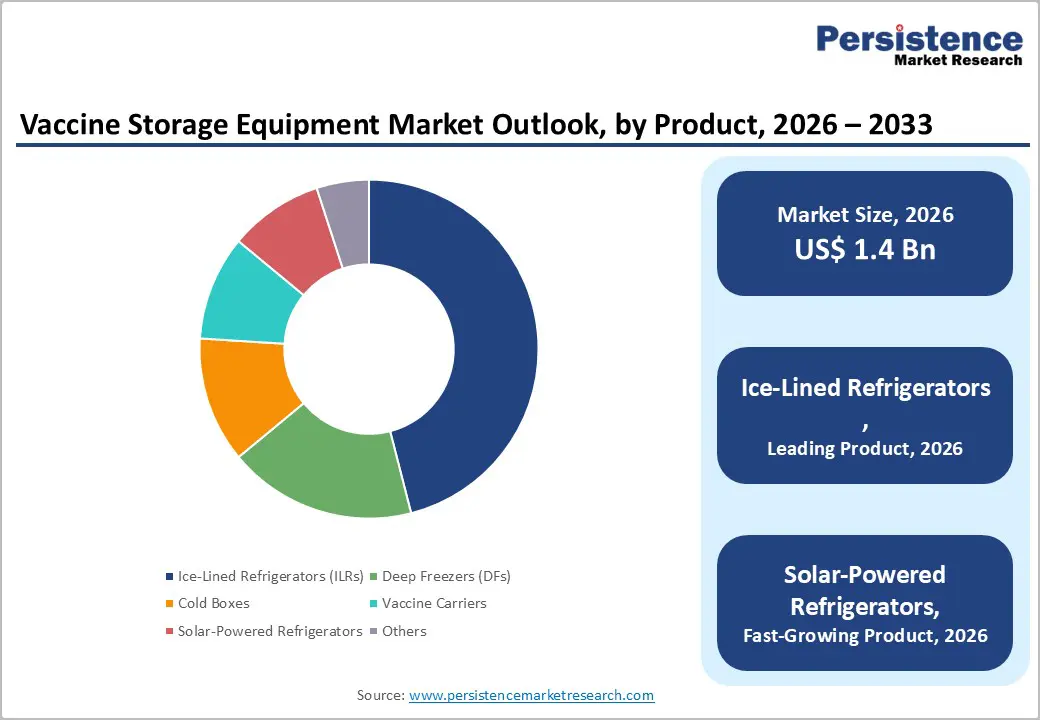

- Dominant Product Category: Ice-lined refrigerators (ILRs) are expected to lead with an estimated 46% share in 2026, supported by large-scale integration into WHO/UNICEF EPI programs and consistent demand for +2°C to +8°C vaccine storage across primary healthcare facilities.

- Fastest-growing Product Category: Solar-powered vaccine refrigerators are likely to be the fastest-growing segment through 2033, driven by off-grid healthcare expansion, rural immunization outreach, and increasing adoption of renewable-powered cold chain equipment to reduce vaccine spoilage risks.

- End-user Dynamics: Hospitals and clinics are expected to dominate with an estimated 62% share in 2026, supported by structured immunization delivery systems and continuous vaccine administration requirements, while decentralized immunization units are projected to grow at the fastest pace due to last-mile healthcare expansion.

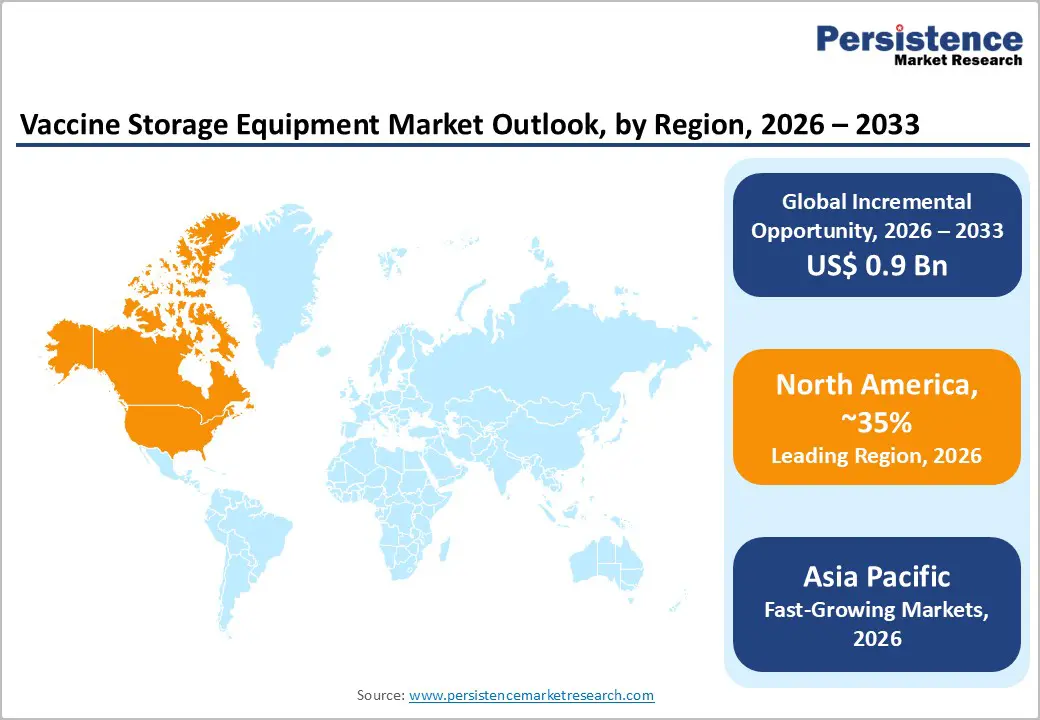

- Regional Leadership: North America is expected to remain the dominant regional market with an estimated 35% share in 2026, driven by advanced healthcare infrastructure, stringent CDC/FDA vaccine storage compliance regulations, and high penetration of ultra-low temperature storage systems for mRNA and specialty vaccines.

- Competitive Environment: Market competition is shaped by investments in WHO-compliant vaccine cold storage systems, expansion of solar-powered refrigeration technologies, and strategic geographic expansion by global manufacturers targeting emerging immunization markets in Asia, Africa, and Latin America.

DRO Analysis

Driver - Expansion of Global Immunization Programs and Public Health Cold Chain Infrastructure

The most significant driver of the vaccine storage equipment market is the expansion of global immunization initiatives led by organizations such as the World Health Organization (WHO), UNICEF, and Gavi, the Vaccine Alliance. WHO’s Expanded Programme on Immunization (EPI) supports vaccination for over 80% of the world’s infant population, significantly increasing demand for ice-lined refrigerators (ILRs), vaccine carriers, and deep freezers. UNICEF Supply Division reports that millions of vaccine doses are shipped annually under strict temperature conditions between +2°C and +8°C or ultra-low conditions for mRNA vaccines.

Governments in India, Africa, and Southeast Asia are investing heavily in cold chain expansion under national immunization missions. For example, India’s Universal Immunization Programme (UIP) supports one of the largest vaccine distribution networks globally. This scale directly translates into continuous procurement of vaccine cold storage equipment, strengthening market demand across primary healthcare facilities and rural distribution networks.

Restraint - High Capital and Operational Costs of Advanced Cold Chain Systems

A key restraint in the vaccine storage equipment market is the high cost of procurement, installation, and maintenance of advanced refrigeration systems, particularly solar-powered refrigerators and ultra-low temperature freezers. Equipment costs are further amplified by requirements for backup power systems, temperature monitoring sensors, and maintenance protocols mandated by WHO Performance Quality and Safety (PQS) standards. In low- and middle-income countries (LMICs), budget constraints in public healthcare systems limit large-scale deployment, especially in rural and remote regions.

Additionally, operational costs such as electricity consumption and refrigerant servicing create long-term financial burdens. According to World Bank healthcare infrastructure assessments, cold chain logistics can account for a significant portion of immunization program budgets in developing economies. These cost pressures slow down adoption rates and create dependency on donor-funded procurement programs, limiting organic market expansion despite strong demand potential.

Opportunity - Expansion of Solar-Powered Cold Chain Solutions in Off-Grid Regions

A major growth opportunity in the vaccine storage equipment market is the rapid adoption of solar-powered vaccine refrigerators, especially in off-grid and energy-insecure regions across Sub-Saharan Africa, South Asia, and parts of Latin America. WHO PQS-certified solar refrigeration units are increasingly deployed under programs such as Gavi’s Cold Chain Equipment Optimization Platform (CCEOP), which aims to improve vaccine accessibility in remote communities. These systems eliminate reliance on unstable electricity grids and significantly reduce vaccine spoilage rates, which WHO estimates can exceed 20% in weak cold chain environments.

Market expansion in this segment is expected to accelerate as governments integrate renewable energy policies into healthcare infrastructure. Additionally, manufacturers are investing in hybrid refrigeration technologies combining solar and battery storage systems. This creates a scalable opportunity for manufacturers, with the solar-powered vaccine storage equipment segment emerging as a high-value growth vector within the broader vaccine cold chain market.

Category-wise Analysis

Product Insights

The ice-lined refrigerators (ILRs) segment is expected to lead the vaccine storage equipment market with an estimated 46% share in 2026, supported by widespread deployment across WHO/UNICEF-backed EPI cold chain networks. Their dominance is attributed to consistent use in primary healthcare settings where +2°C to +8°C stability is required despite intermittent power supply conditions. ILRs are likely to remain the preferred configuration in large-scale public immunization programs across emerging economies, where standardized procurement and operational reliability are prioritized over advanced system complexity.

The solar-powered vaccine refrigerators segment is expected to be the fastest-growing, expanding at an estimated 8.5% CAGR (2026 - 2033), driven by increasing deployment in off-grid and energy-insecure regions. Adoption is anticipated to rise across rural healthcare systems in South Asia and Sub-Saharan Africa, where conventional refrigeration infrastructure remains limited. Growth is further supported by WHO PQS certification standards and multilateral funding programs, with ongoing rollout initiatives improving vaccine accessibility in remote and hard-to-reach populations.

End-user Insights

On the end-user side, hospitals and clinics are expected to dominate the market with an estimated 62% share in 2026, driven by continuous immunization schedules, institutional vaccine storage requirements, and compliance with pharmaceutical cold chain regulations. These facilities are likely to remain the primary procurement base due to structured healthcare delivery systems and recurring replacement cycles aligned with public health programs. Demand is expected to remain stable across developed and emerging healthcare markets, supported by routine vaccination and biologics administration.

The fastest-growing end-user segment is expected to be decentralized healthcare facilities and mobile immunization units, projected to expand at an estimated 7.8% CAGR (2026 - 2033), driven by increasing emphasis on last-mile vaccine delivery. Growth is anticipated from the expansion of outreach immunization programs targeting rural and underserved populations, supported by WHO-led initiatives and NGO-led public health campaigns. Rising deployment of portable cold boxes and vaccine carriers in outbreak response and preventive immunization drives is expected to further strengthen decentralized cold chain infrastructure.

Regional Analysis

North America Vaccine Storage Equipment Market Trends

North America is expected to account for approximately 35% of the global vaccine storage equipment market in 2026, and its response is largely shaped by a mature, regulation-intensive healthcare ecosystem. The region is witnessing a steady transition toward next-generation cold chain infrastructure, driven by CDC and FDA compliance requirements that emphasize continuous temperature integrity and audit-ready storage systems. Adoption is increasingly shifting toward IoT-enabled refrigeration units and ultra-low temperature freezers, particularly to support diversified vaccine portfolios including mRNA-based and specialty biologics.

The overall response is characterized more by replacement and technology upgrade cycles than by capacity expansion.

The U.S. is expected to represent nearly 85% of North America’s demand, driven by large-scale immunization infrastructure and ongoing modernization of hospital-based storage systems. Federal preparedness investments and post-pandemic healthcare resilience programs are supporting adoption of digitally integrated cold chain systems across public health networks.

Canada, with around 15% regional share, is expected to respond through gradual expansion of cold chain access in remote and low-density regions, with increasing deployment of portable refrigeration systems and energy-efficient storage solutions to strengthen equitable vaccine delivery coverage.

Europe Vaccine Storage Equipment Market Trends

Europe is expected to hold approximately a 25% share of the global vaccine storage equipment market in 2026, and its response is primarily driven by regulatory harmonization, sustainability targets, and structured healthcare procurement systems. The region is increasingly focused on energy-efficient and environmentally compliant cold chain modernization, supported by EMA regulatory standards and EU-wide healthcare quality frameworks. Demand is largely replacement-led, as healthcare systems upgrade aging refrigeration infrastructure to meet stricter efficiency, traceability, and environmental performance requirements. This creates a stable but technologically upgrading demand environment across hospital and centralized vaccine distribution networks.

Germany is expected to contribute around 30% of Europe’s demand, with strong adoption driven by advanced hospital infrastructure and pharmaceutical logistics integration. The country’s response is centered on digital cold chain monitoring systems and precision refrigeration upgrades across healthcare facilities.

The U.K., with approximately 18% regional share, is expected to respond through NHS-led cold chain modernization programs, focusing on centralized vaccine distribution efficiency and enhanced temperature monitoring systems. Both markets reflect Europe’s broader shift toward controlled modernization and sustainability-led cold chain transformation.

Asia Pacific Vaccine Storage Equipment Market Trends

Asia Pacific is expected to account for approximately 32% of the global vaccine storage equipment market in 2026, and it represents the most expansion-driven regional response. The region is actively scaling vaccine cold chain infrastructure, supported by large immunization programs and increasing healthcare access in rural and semi-urban areas. Unlike mature markets, the response is primarily capacity expansion-led, with strong investments in ice-lined refrigerators, solar-powered systems, and portable cold chain equipment. Support from WHO and Gavi-linked initiatives is further accelerating deployment across primary healthcare networks.

China is expected to hold around 35% of Asia Pacific demand, with a response focused on large-scale expansion and modernization of national immunization cold chain infrastructure. Investments are directed toward strengthening county-level storage capacity and improving digital integration across public health logistics systems.

India is expected to account for around 25% of the regional market in 2026, with a strong response driven by the Universal Immunization Programme and increasing deployment of solar refrigeration systems and digital tracking platforms such as eVIN. The focus remains on improving last-mile vaccine delivery and expanding cold chain reach into underserved rural and tribal regions.

Competitive Landscape

The global vaccine storage equipment market is moderately consolidated, with key players such as Thermo Fisher Scientific, Haier Biomedical, PHC Holdings, and Vestfrost Solutions holding a significant share of revenues. These companies maintain leadership through strong global supply networks, compliance with WHO PQS standards, and long-term contracts with governments and immunization agencies. Competition is increasingly driven by advancements in ultra-low temperature storage, energy-efficient refrigeration, and IoT-enabled monitoring systems, supporting growing demand for temperature-sensitive vaccines.

Regional and niche players such as B Medical Systems, Dometic Group, Arctiko, and Godrej & Boyce are expanding through cost-effective and application-specific solutions, including solar-powered refrigerators and portable cold chain systems for last-mile delivery. Although high regulatory and certification requirements limit new entrants, rising demand for decentralized immunization infrastructure is enabling niche growth. The market is expected to gradually consolidate through acquisitions, partnerships, and integration of smart monitoring technologies into traditional cold chain equipment.

Key Industry Developments:

- In October 2025, Thermo Fisher Scientific announced the acquisition of Clario for up to US$9.4 billion, strengthening its clinical data and digital health ecosystem tied to biologics and vaccine supply chains.

- In February 2025, B Medical Systems launched the Ultra-Low Freezer U201, the first-ever WHO PQS prequalified ultra-low freezer. The 214L capacity unit ensures -86°C to -20°C storage with real-time monitoring and NFC-based security. CEO Luc Provost highlighted its role in supporting mRNA vaccines and cell therapy in extreme climates.

Companies Covered in Vaccine Storage Equipment Market

- Thermo Fisher Scientific

- Haier Biomedical

- Vestfrost Solutions

- Dometic Group

- PHC Holdings Corporation

- Godrej & Boyce

- B Medical Systems

- Liebherr Group

- Arctiko

- Follett Products

- Helmer Scientific

- Panasonic Healthcare

- Stirling Ultracold

- Zanotti

- Aucma

Frequently Asked Questions

The global vaccine storage equipment market is expected to reach US$1.4 billion in 2026.

Rising immunization programs, expanding cold chain infrastructure, and increasing demand for temperature-sensitive vaccines drive the market.

The vaccine storage equipment market is projected to grow at a 7.3% CAGR from 2026 to 2033.

Growth opportunities emerge from solar-powered refrigeration adoption, rural healthcare expansion, and last-mile vaccine delivery systems.

Key players include Thermo Fisher Scientific, Haier Biomedical, PHC Holdings, Vestfrost Solutions, and B Medical Systems.