- Biotechnology

- Viral Vector Vaccines Market

Viral Vector Vaccines Market Size, Share, and Growth Forecast, 2026 - 2033

Viral Vector Vaccines Market by Product Type (Adenovirus, Fowlpox Virus, Attenuated Yellow Fever, Vaccinia Virus Vectors), Application (Antisense and RNAi, Gene Therapy, Cell Therapy, Vaccinology), and Regional Analysis for 2026 - 2033

Viral Vector Vaccines Market Size and Trends Analysis

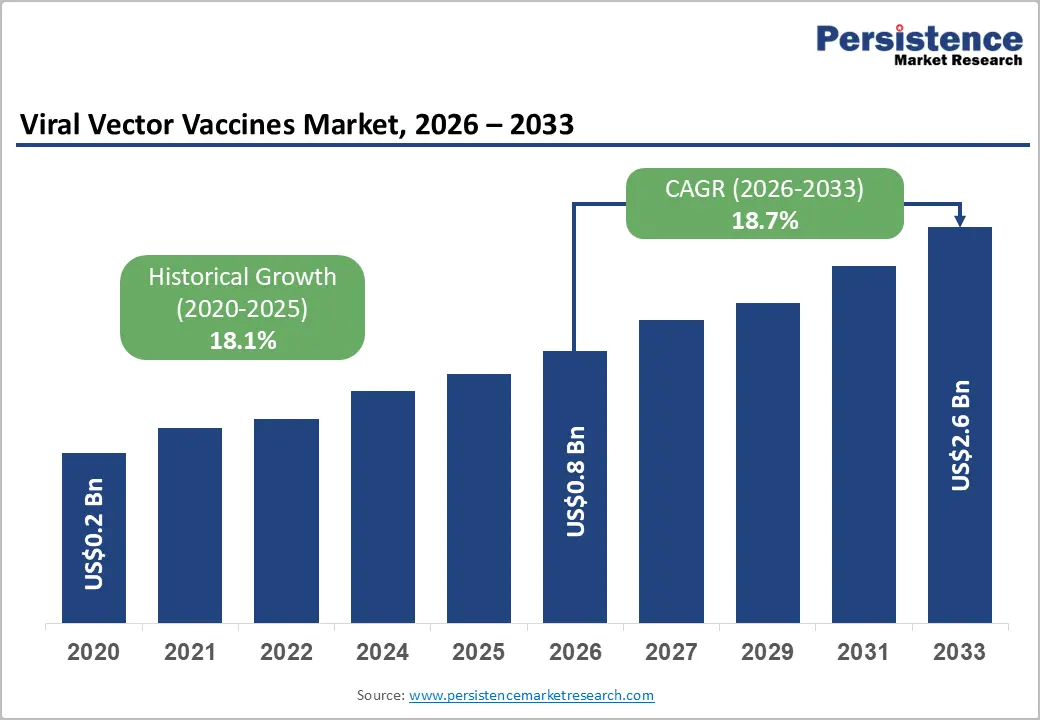

The global viral vector vaccines market size is likely to be valued at US$0.8 billion in 2026 and is expected to reach US$2.6 billion by 2033, growing at a CAGR of 18.7% during the forecast period from 2026 to 2033, driven by increasing focus on advanced immunization technologies, rising infectious disease outbreaks, and growing adoption of viral vectors in gene-based therapies and vaccine development.

Viral vector platforms are widely used for inducing strong cellular and humoral immune responses against diseases such as COVID-19, Ebola, and emerging viral infections. In 2025, the World Health Organization (WHO) highlighted the continued expansion of global vaccine technology programs and regional manufacturing initiatives to strengthen pandemic preparedness and vaccine accessibility.

Key Industry Highlights:

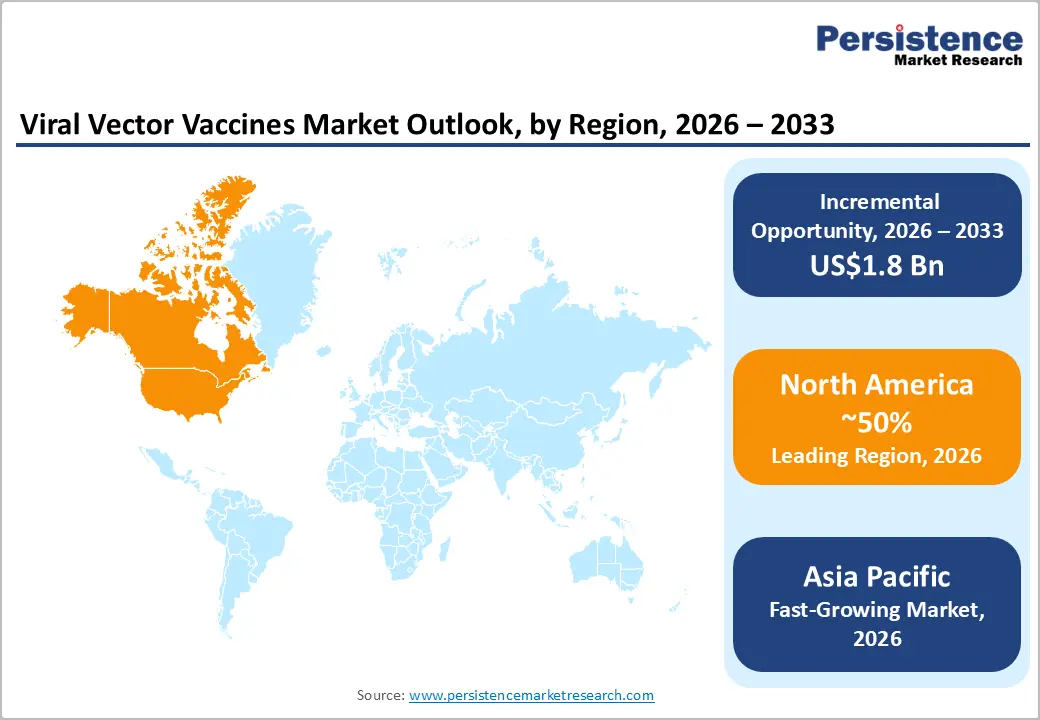

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 50% in 2026, driven by strong U.S. regulatory support, advanced biotechnology infrastructure, and extensive vaccine innovation activities.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by expanding vaccine manufacturing capabilities and growing healthcare investments.

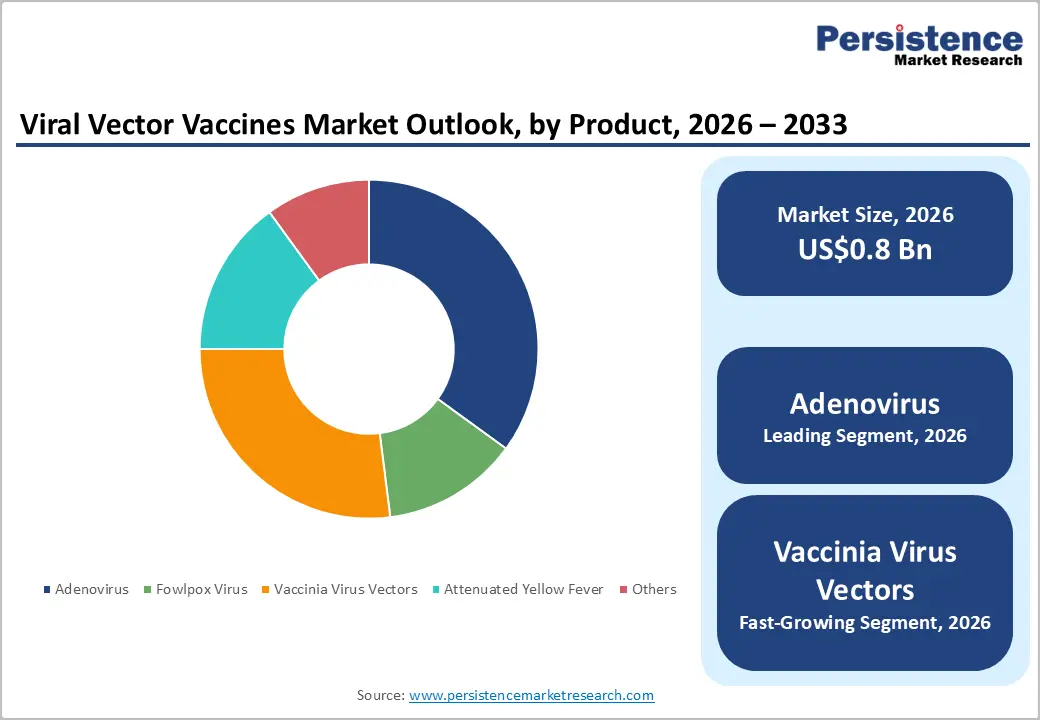

- Leading Product Type: Adenovirus vectors are projected to represent the leading product type in 2026, accounting for 45% of the revenue share, for its widespread use in infectious disease vaccines and strong delivery efficiency.

- Leading Application: Vaccinology is anticipated to be the leading application, accounting for over 50% of the revenue share in 2026, owing to extensive use in preventive immunization programs worldwide.

- Key Opportunity: The key market opportunity in the viral vector vaccines market lies in the integration of next-generation vector engineering, AI-driven vaccine development, and expanding gene therapy applications to enable faster, more targeted, and scalable therapeutic solutions worldwide.

DRO Analysis

Driver - Rising Prevalence of Infectious Diseases and Need for Rapid Response Platforms

Frequent outbreaks of respiratory viruses, zoonotic infections, and emerging pathogens have intensified the need for rapid and adaptable vaccine development platforms. Viral vector technologies enable faster vaccine design, strong immune activation, and scalable deployment compared with traditional vaccine methods. Governments and healthcare organizations worldwide are prioritizing pandemic preparedness programs, supporting investments in advanced vaccine research and manufacturing infrastructure.

Growing awareness regarding immunization, combined with expanding biotechnology capabilities, continues to strengthen the adoption of viral vector vaccines across both developed and emerging healthcare markets. The success of viral vector-based vaccines during recent health emergencies significantly increased confidence in these platforms among pharmaceutical companies, regulatory agencies, and public health institutions.

Adenoviral vector vaccines demonstrated rapid clinical advancement and effective immune responses, encouraging research into next-generation vaccines targeting influenza, HIV, malaria, and oncology indications. Rising collaborations between biotechnology firms, academic institutions, and government agencies are accelerating innovation and commercialization activities.

Restraint - Manufacturing Scalability and Production Complexity

Viral vector vaccine production requires highly specialized bioprocessing facilities, advanced purification systems, and stringent quality control standards, which increase operational costs considerably. Maintaining vector stability, potency, and sterility during large-scale production presents technical challenges for manufacturers. The manufacturing process often involves complex cell culture systems and sophisticated downstream processing technologies that demand skilled professionals and extensive infrastructure investments.

The complexity associated with regulatory compliance and manufacturing consistency also affects the widespread adoption of viral vector vaccines. Variability in vector yield and difficulties in maintaining batch-to-batch consistency can impact production efficiency and increase overall development risks. Small and mid-sized biotechnology companies struggle to manage the financial burden associated with advanced manufacturing technologies and facility expansion.

Opportunity - Technological Convergence with AI and Next-Generation Vectors

AI-driven analytics are increasingly being used to optimize vaccine design, improve antigen selection, and accelerate clinical research processes. Machine learning algorithms help researchers predict immune responses and identify effective viral vector combinations with greater accuracy and speed.

Advancements in next-generation vectors, including modified adenoviral and self-amplifying viral systems, are improving vaccine safety, efficacy, and delivery efficiency. These innovations support the development of personalized vaccines and targeted immunotherapies for infectious diseases and cancer, creating new commercial opportunities for biotechnology and pharmaceutical companies worldwide.

The integration of AI with advanced vector engineering technologies is also enhancing manufacturing optimization and regulatory compliance in vaccine production. Predictive analytics and automation tools enable manufacturers to improve production yields, reduce contamination risks, and streamline quality control procedures. Emerging vector platforms with lower immunogenicity and higher gene delivery efficiency are expanding applications beyond traditional infectious disease prevention into gene therapy and oncology treatments.

Category-wise Analysis

Product Type Insights

Adenovirus vectors are anticipated to dominate the market, accounting for approximately 45% of total revenue in 2026, driven by their strong immunogenic properties, efficient gene delivery performance, and extensive application in vaccine development programs. These vectors are widely favored for their ability to generate robust cellular and humoral immune responses while also supporting scalable manufacturing capabilities. A prominent example is the COVID-19 vaccine developed by AstraZeneca in partnership with the University of Oxford, which leveraged an adenoviral vector platform and achieved broad global deployment.

Vaccinia virus vectors are likely to represent the fastest-growing segment, supported by increasing research activities focused on oncology, immunotherapy, and complex antigen delivery applications. These vectors offer large genetic carrying capacity and strong immune stimulation capabilities, making them highly suitable for advanced therapeutic vaccine development. For instance, the development of vaccinia-based oncolytic immunotherapies by Merck KGaA and research collaborators is targeting advanced cancer treatments.

Application Insights

Vaccinology is projected to lead the market, capturing around 50% of the revenue share in 2026, supported by increasing use of viral vector technologies in infectious disease prevention programs worldwide. Governments and healthcare organizations continue prioritizing large-scale immunization initiatives to combat viral outbreaks and improve public health preparedness. For example, the Ebola vaccine developed by Johnson & Johnson, which utilized viral vector technology to support infectious disease control initiatives in affected regions.

Gene therapy is likely to be the fastest-growing application, due to rising advancements in genetic medicine and increasing approvals for treatments targeting rare and chronic diseases. Viral vectors play a critical role in delivering therapeutic genes into target cells with high precision and efficiency, making them essential for modern gene therapy platforms. A notable example includes the gene therapy platform developed by uniQure N.V. for treating rare genetic disorders using advanced viral vector delivery technologies.

Regional Insights

North America Viral Vector Vaccines Market Trends

North America is anticipated to be the leading region, accounting for a market share of 50% in 2026, supported by strong biotechnology infrastructure, extensive vaccine research activities, and substantial government funding for infectious disease preparedness. The region benefits from the presence of major pharmaceutical and biotechnology companies actively investing in viral vector platforms for vaccine development, oncology, and gene therapy applications. A notable example includes Moderna expanding research collaborations and manufacturing investments in advanced viral delivery and next-generation vaccine technologies.

U.S. Viral Vector Vaccines Market Trends

The U.S. dominates the regional market, accounting for approximately 78% share of the market, driven by strong pharmaceutical research infrastructure and significant biotechnology investments. The country has a high concentration of vaccine developers, contract manufacturing organizations, and advanced biologics facilities supporting large-scale viral vector production. Increasing clinical trials focused on oncology and gene therapy applications are driving additional market growth.

Canada Viral Vector Vaccines Market Trends

Canada is a significant market for viral vector vaccines, holding approximately 22% of the market share, supported by increasing government support for biotechnology innovation and domestic vaccine manufacturing capabilities. The country is strengthening investments in biologics production infrastructure to reduce dependency on imported vaccines and therapeutics. Canadian research institutions are actively engaged in viral vector vaccine and gene therapy development programs.

Europe Viral Vector Vaccines Market Trends

Europe is likely to be a significant market for viral vector vaccines in 2026, due to rising investments in biotechnology research, advanced healthcare infrastructure, and increasing adoption of innovative vaccine technologies. The region benefits from strong regulatory frameworks supporting biologics development and commercialization across multiple therapeutic applications. For instance, Oxford Biomedica is strengthening viral vector manufacturing partnerships to support gene therapy and vaccine production across Europe.

U.K. Viral Vector Vaccines Market Trends

The U.K. is expected to represent a significant market for viral vector vaccines, accounting for approximately 28% of the European market share in 2026. Growth is supported by the country’s strong academic research ecosystem and rapidly expanding biotechnology sector. The U.K. has emerged as a major hub for advanced vaccine development and viral vector innovation, driven by increasing investments in healthcare technologies and life sciences research. Academic institutions and pharmaceutical companies across the country are actively involved in the development of adenoviral- and vaccinia-based therapies targeting infectious diseases and oncology applications.

Germany Viral Vector Vaccines Market Trends

Germany is projected to account for approximately 34% of the European market in 2026, driven by its advanced pharmaceutical manufacturing industry and strong biotechnology research ecosystem. The country benefits from well-established vaccine production capabilities supported by substantial investments from both the government and private sector organizations. German biotechnology companies are actively engaged in the development of viral vector-based therapies for oncology, infectious diseases, and rare genetic disorders.

Asia Pacific Viral Vector Vaccines Market Trends

The Asia Pacific region is likely to be the fastest-growing region, driven by the increasing healthcare investments, expanding biotechnology infrastructure, and rising demand for advanced immunization technologies. For example, CanSino Biologics is expanding its viral vector vaccine development programs and international collaborations for infectious disease prevention.

China Viral Vector Vaccines Market Trends

China is expected to dominate the regional market, holding around 41% share of the market in 2026, supported by rapid biotechnology expansion and substantial government investments in vaccine research and manufacturing infrastructure. The country has significantly increased support for domestic biologics production and infectious disease preparedness programs. Chinese pharmaceutical companies are actively developing adenoviral and viral vector-based vaccines for multiple therapeutic applications.

India Viral Vector Vaccines Market Trends

India is expected to be a significant market for viral vector vaccines, accounting for approximately 24% share of the market in 2026, due to expanding pharmaceutical manufacturing capabilities and increasing investments in biotechnology innovation. The country benefits from a strong vaccine production ecosystem and growing government initiatives supporting healthcare modernization and immunization programs. Indian biotechnology companies are actively involved in developing viral vector-based vaccines and advanced biologics for infectious diseases and therapeutic applications.

Competitive Landscape

The global viral vector vaccines market exhibits a moderately fragmented structure, driven by increasing investments in biotechnology innovation, expanding vaccine research programs, and rising demand for advanced immunization technologies. Market growth is supported by continuous advancements in adenoviral, vaccinia, and other viral vector platforms used across infectious disease prevention, oncology, and gene therapy applications.

With key leaders, including Merck KGaA, Thermo Fisher Scientific, Charles River Laboratories, uniQure N.V., and Aldevron, the market continues to experience strong competitive activity across vaccine development and vector manufacturing services. These players compete through strategic collaborations, expansion of viral vector production facilities, technological advancements in vector engineering, acquisitions, and increasing investments in gene therapy and oncology research.

Key Industry Developments:

- In May 2026, GeoVax Labs announced Phase 3 trial implementation plans for its GEO-MVA modified vaccinia Ankara (MVA) vaccine candidate targeting mpox and smallpox, aiming to strengthen global orthopoxvirus vaccine supply capabilities.

- In February 2026, Bavarian Nordic received a USD 22.5 million contract from the Canadian government for the supply and manufacturing of its MVA-BN mpox and smallpox vaccine under long-term public health preparedness initiatives.

- In December 2025, University of Oxford launched the world’s first Phase II clinical trial for the ChAdOx1 NipahB viral vector vaccine candidate designed to combat Nipah virus outbreaks in Bangladesh.

Companies Covered in Viral Vector Vaccines Market

- Novasep

- MerckKGaA

- Charles River Laboratories

- uniQure N.V.

- Waisman Biomanufacturing

- Creative-Biogene

- Aldevron

- Addgene

- Thermo Fisher Scientific Inc.

- AstraZeneca

- Johnson & Johnson

- CanSino Biologics

- Oxford Biomedica

- Bavarian Nordic

Frequently Asked Questions

The global viral vector vaccines market is projected to reach US$0.8 billion in 2026.

The viral vector vaccines market is driven by rising infectious disease prevalence, growing demand for rapid vaccine development platforms, and increasing investments in gene therapy and advanced biotechnology research.

The viral vector vaccines market is expected to grow at a CAGR of 18.7% from 2026 to 2033.

Key opportunities include AI-integrated vaccine development, expansion of gene therapy applications, and advancements in next-generation viral vector engineering technologies.

Novasep, Merck KGaA, Charles River Laboratories, uniQure N.V., and Waisman Biomanufacturing are the leading players.