Powder Metallurgy Market

Industry: Chemicals and Materials

Published Date: December-2024

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 188

Report ID: PMRREP35013

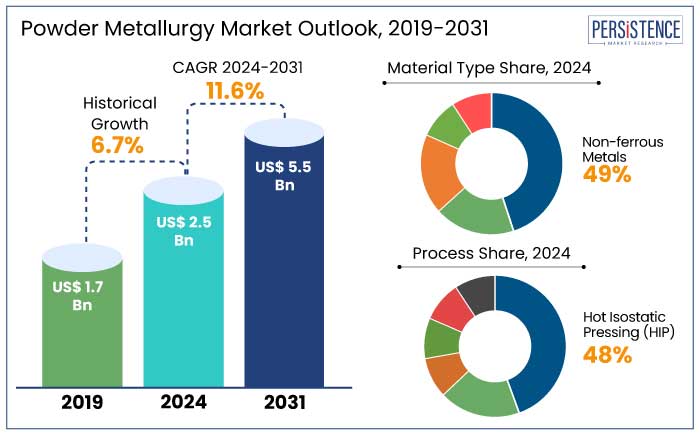

The global Powder Metallurgy (PM)) Market is estimated to reach a size of US$ 2.5 Bn by 2024. It is anticipated to experience a CAGR of 11.6% during the forecast period to reach a value of US$ 5.5 Bn by 2031. Governments are increasingly supporting the recycling of metals, which is closely linked to powder metallurgy.

In the European Union (EU), metal recycling rates have improved dramatically, with the EU Commission aiming for 90% recycling of metals by 2030 under its Circular Economy Action Plan. Government authorities around the world are offering incentives to companies that adopt sustainable manufacturing practices.

As power metallurgy is energy-efficient and generates less waste compared to traditional methods, it qualifies for many of these incentives. For instance, the U.S. Department of Energy offers grants to companies that implement energy-efficient practices in manufacturing.

The EU’s Green Deal, aimed at making Europe the first carbon-neutral continent by 2050, includes incentives for industries adopting low-carbon and circular economy practices. Countries like Germany and the U.K. provide tax breaks and financial support to manufacturing companies that integrate sustainable technologies. These incentives help PM manufacturers invest in cleaner, more energy-efficient equipment, further boosting growth.

Key Highlights of the Industry

|

Market Attributes |

Key Insights |

|

Powder Metallurgy Market Size (2024E) |

US$ 2.5 Bn |

|

Projected Market Value (2031F) |

US$ 5.5 Bn |

|

Global Market Growth Rate (CAGR 2024 to 2031) |

11.6% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

6.7% |

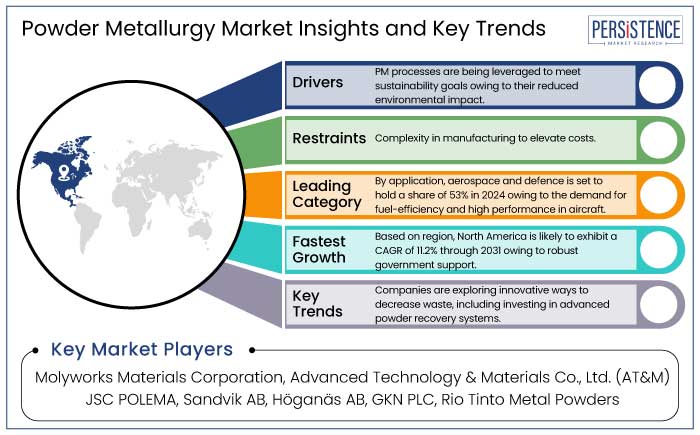

Powder metallurgy market in North America is estimated to hold a share of 36% in 2024. The region, particularly the U.S., is home to a significant portion of the global automotive industry. Growing demand for electrification in vehicles is posing a demand for PM as it is critical for the production of components like gears, rotors, motor parts, and structural elements, where lightweight and high-strength materials are essential.

Based on statistics provided by the Automotive Industry Action Group (AIAG), PM parts are used extensively in 30% of parts in modern cars. The aerospace industry in North America alone accounted for over 40% of global aerospace production in 2023, which directly supports the demand for high-performance materials like titanium alloys, superalloys, and other advanced metal powders produced using powder metallurgy.

The U.S. Department of Energy (DOE) and National Science Foundation (NSF) allocate billions of dollars annually for research into sustainable manufacturing techniques, including the development of new metal powders and PM processes. North America is home to some of the largest companies and research institutions pushing the envelope in 3D printing and additive manufacturing, which are closely integrated with powder metallurgy.

Non-ferrous metals are estimated to hold a share of 49% in 2024. These metals offer an excellent strength-to-weight ratio, which is crucial for industries where reducing weight is a priority. Non-ferrous metals exhibit high corrosion resistance, making them ideal for applications in harsh environments. These properties are highly valued in industries including electronics, marine, and automotive.

Copper and aluminum are particularly prized for their high electrical and thermal conductivity. This property makes these metals essential in the electronics industry for applications such as connectors, terminals, and heat exchangers.

Non-ferrous metals like titanium and aluminum are particularly suitable for metal 3D printing, where they are used to create complex, lightweight, and custom components. Copper is a primary metal used in wind turbines and solar photovoltaic cells. Consequently, making non-ferrous metals crucial in the production of highly conductive and corrosion-resistant components used in renewable energy applications.

It is estimated that 95% of aluminum used in the automotive industry is recycled. This trend not only reduces material costs but also contributes to the sustainability goals of the industry, making non-ferrous metals more attractive in the powder metallurgy market.

Hot isostatic pressing (HIP) is predicted to hold a share of 48% in 2024. A key advantage of HIP is its ability to create high-density parts with a uniform structure, which is essential for industries requiring high-performance materials. HIP involves applying high temperature and pressure to metal powder within a sealed container, enabling the material to densify and eliminate porosity.

HIP ensures that parts are near 100% dense, thereby enhancing the material's mechanical properties, such as strength, toughness, and fatigue resistance. Components produced via HIP exhibit far fewer internal voids and defects compared to other PM processes, making it highly suitable for critical applications in aerospace, defense, and medical industries.

High density achieved through HIP results in improved fatigue resistance, which is crucial for parts that will be exposed to high stresses or harsh environments.

Aerospace and defence is anticipated to hold a share of 53% in 2024. The aerospace industry is focused on producing lightweight components that enhance fuel efficiency and reduce emissions. Powder metallurgy enables the production of lightweight, strong, and durable components that meet the stringent requirements of aerospace applications.

As demand for fuel-efficient, high-performance aircraft increases, the need for lightweight and high-strength components will drive the adoption of PM techniques in the production of aircraft parts. Aerospace applications often require materials that can withstand extreme temperatures and high pressures, particularly in jet engines and turbine systems.

PM processes are ideal for producing parts from superalloys and nickel-based alloys that offer exceptional heat resistance, fatigue resistance, and corrosion resistance. The defense industry requires durable, high-strength components that can withstand extreme conditions such as high stress, fatigue, and impact.

PM is an effective method for producing parts like armor plating, missile components, firearms, and munitions owing to its ability to achieve high-density materials with enhanced properties. Powder metallurgy is known for its cost-effectiveness, especially in producing complex shapes with minimal material waste. Aerospace and defense industries benefit from PM as it allows for near-net-shape manufacturing, reducing material waste and post-processing steps.

Potential growth in the global powder metallurgy industry is predicted to be driven by innovations in PM materials, including high-performance alloys and nanostructured powders, thereby enabling broader adoption across industries. As industries continue their focus on decreasing weight to enhance fuel efficiency and performance, the demand for PM-products parts offering high strength to weight ratios is estimated to grow.

Rising focus on recycling metal waste for the production of metal powders, is predicted to further contribute to the expansion of the market. AM technologies are expected to witness exorbitant growth during the assessment period, thereby augmenting a steady demand for PM.

The powder metallurgy market is estimated to witness a CAGR of 6.7% during the historical period. Growth during the period was prominently fuelled by demand in the automotive sector, particularly for lightweight and high-performance components.

The COVID-19 pandemic disrupted supply chains, slowing market growth. The market, however, still managed to expand as industries like medical and electronics showed resilience. Remote working trend facilitated demand for consumer electronics, positively impacting the growth of PM components used in electronic devices. The adoption of PM in electric vehicles (EVs) and renewable energy applications contributed to its growth further.

Increased investment in additive manufacturing (AM) and the growing emphasis on sustainability fueled market growth further. Advancements in PM technologies, such as hot isostatic pressing (HIP) and metal injection molding (MIM), gained traction.

Increasing integration of PM with 3D printing technologies is expected to significantly expand design possibilities and market reach during the forecast period. Rising emphasis on green manufacturing is likely to further boost adoption due to its energy efficiency and minimal material waste.

Rising Adoption in Additive Manufacturing

Integration of additive manufacturing (AM), popularly known as 3D printing with powder metallurgy (PM) is substantially transforming manufacturing processes across several industries. Continuous improvements in AM technologies including enhanced printing speeds, precision, and the development of new metal powders, are broadening the application scope of AM in industries like aerospace, automotive, and healthcare.

Several industries are increasingly adopting AM to produce intricate and lightweight metal parts that are challenging to manufacture using conventional methods. AM enables rapid prototyping and the production of customized components, thereby decreasing time-to-market while enabling efficient design iterations. AM is increasingly used in the medical field to create patient-specific implants and prosthetics, offering enhanced compatibility and performance.

Lightweight Trends Across Industries

Lightweighting assists in improving fuel efficiency, decreasing emissions, and enhancing operational efficiency. Aircraft manufacturers are progressively utilizing composite materials to decrease weight. For instance, the Boeing 787 Dreamliner is constructed with approximately 50% composite materials, thereby enhancing fuel efficiency and performance.

Construction sector is adopting lightweight concrete and engineered wood products to decrease structural weight, resulting in quick project completion times and cost savings in foundation and structural support. The automotive industry is increasingly adopting high strength steel (HSS) and advanced high strength steel (AHSS) to achieve weight reduction while maintaining structural integrity and safety standards.

The integration of polymers and composites in manufacturing processes is contributing to weight reductions across various industries, thereby enhancing product performance and efficiency.

Complexity in Manufacturing Restraints Market Growth

The intricate nature of PM processes requires precise control and monitoring, which can result in elevated costs, slower production cycles, and potential quality issues. PM relies on powders with precise characteristics such as particle size, shape, and composition. Variations in these properties can lead to inconsistent component quality.

Studies suggest that 30% of PM components may experience reduced strength or reliability due to porosity during manufacturing. Variations in compaction pressure can result in density differences of up to 15%, thereby affecting mechanical properties. While PM can produce intricate shapes, components with hollow structures or deep cavities remain challenging.

Approximately 25% to 40% of PM components require additional machining or finishing processes to meet final specifications. This further increases production time and costs, thereby limiting PM’s competitiveness compared to conventional manufacturing. PM component development can take 20% to 50% longer than traditional methods for new product designs. The time required for tooling, prototyping, and process optimization can delay mass production.

Renewable Energy Sector

Global investments in renewable energy have been increasing, with significant funding directed toward the development and deployment of sustainable energy technologies. PM plays a crucial role in advancing technologies that harness sustainable energy sources. It is instrumental in manufacturing high-performance gears, bearings, and structural parts for wind turbines, contributing to enhanced efficiency and durability.

The global solar energy capacity has been increasing, with substantial investments in solar power infrastructure. PM techniques are progressively utilized in producing metal contacts and components for PV cells, essential for solar panels.

PM processes are energy-efficient, consuming 15% less energy compared to conventional manufacturing methods, thereby supporting the sustainable production of renewable energy components. It offers high material utilization rates, thereby decreasing waste and contributing to the overall sustainability of manufacturing processes in the renewable energy sector.

Electrification and Electronics

Powder metallurgy is extensively utilized in producing electrical contacts, connectors, magnetic components, and electronic packaging which are essential for electronic devices and systems, contributing to enhanced performance and miniaturization. The increasing demand for miniaturized and efficient electronic devices is driving the adoption of PM in the electronics sector.

Shift toward electrification in the automotive industry has resulted in increased utilization of PM for manufacturing components including soft magnetic composites used in electric motors, enhancing efficiency and performance. The burgeoning EV market is estimated to have a positive influence on the powder metallurgy market, as the demand for PM components in electric drivetrains and related systems increases.

Companies in the powder metallurgy market are focusing on creating high-performance materials with enhanced thermal and wear resistance. They are progressively incorporating 3D printing and other additive manufacturing technologies to produce complex and customized parts.

Businesses are also developing eco-friendly powders and processes that minimize environmental impact. They are targeting automotive, aerospace, medical, electronics, and energy industries to expand their reach.

Brands are also adapting to trends like electric vehicles (EVs) by producing specialized components, such as soft magnetic materials for motors. They are implementing automation and advanced technologies, like artificial intelligence (AI) and machine learning (ML), for quality control and production efficiency. Companies are also utilizing economies of scale to reduce production costs and improve profitability.

Recent Industry Developments

|

Attributes |

Detail |

|

Forecast Period |

2024 to 2031 |

|

Historical Data Available for |

2019 to 2023 |

|

Market Analysis |

US$ Billion for Value |

|

Key Regions Covered |

|

|

Key Market Segments Covered |

|

|

Key Companies Profiled in the Report |

|

|

Report Coverage |

|

|

Customization and Pricing |

Available upon request |

By Material Type

By Process

By Application

By Region

To know more about delivery timeline for this report Contact Sales

The market is anticipated to reach a value of US$ 5.5 Bn by 2031.

It is used in the automotive, industrial machinery, and medical.

Powder metallurgy can produce harder and tougher components compared to casting.

It enables complex shapes and intricate detail in a less costly manner.

A few of the industry players in the market are Molyworks Materials Corporation, Advanced Technology & Materials Co., Ltd. (AT&M), and JSC POLEMA.