- Healthcare IT

- Medical Transcription Services Market

Medical Transcription Services Market Size, Share and Growth Forecast, 2026 - 2033

Medical Transcription Services Market by Procurement mode (Outsourcing, Offshoring), Services (History and Physical Report, Discharge Summary, Operative Note, Consultation Report, Others), End-user (Hospitals, Clinics, Diagnostic centers, Others), and Regional Analysis for 2026 - 2033

Medical Transcription Services Market Share and Trends Analysis

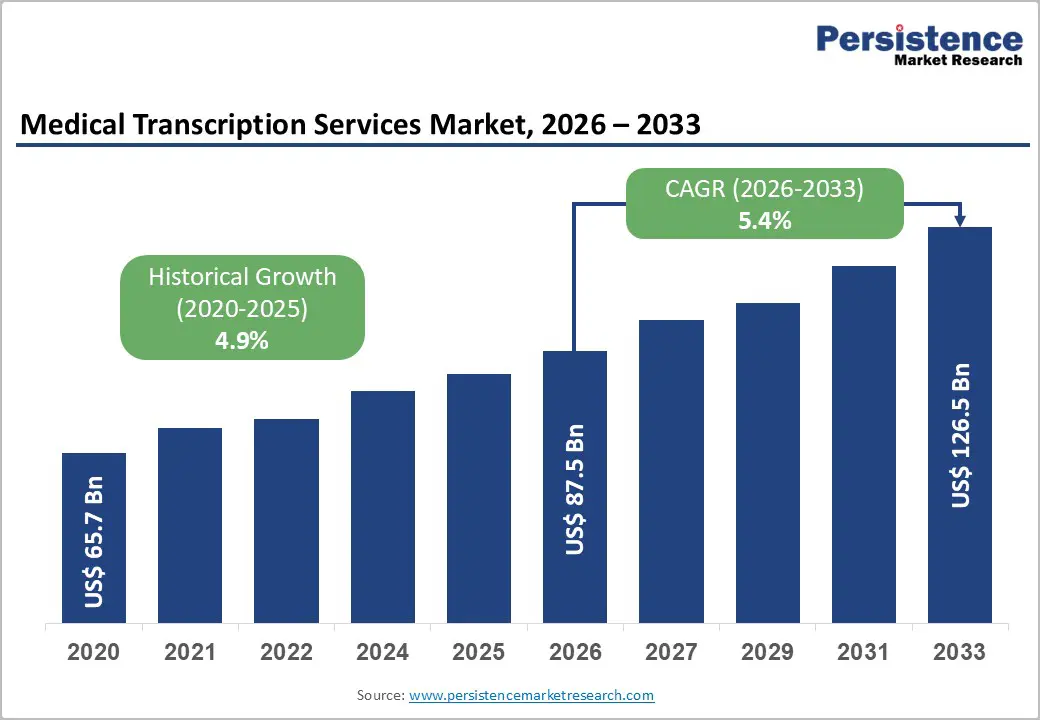

The global medical transcription services market size is likely to be valued at US$ 87.5 billion in 2026 and is projected to reach US$ 126.5 billion by 2033, growing at a CAGR of 5.4% during the forecast period 2026–2033. It is expanding due to the rapid shift toward digital healthcare documentation and increasing reliance on electronic health records (EHRs) across hospitals and clinics. Healthcare providers are prioritizing outsourcing and offshoring to reduce administrative workload, improve documentation accuracy, and enhance operational efficiency.

Key Industry Developments:

- Procurement Mode Leadership: Outsourcing medical transcription dominates with 62% share in 2026, while offshoring is the fastest-growing due to cost efficiency and rising demand for scalable clinical documentation.

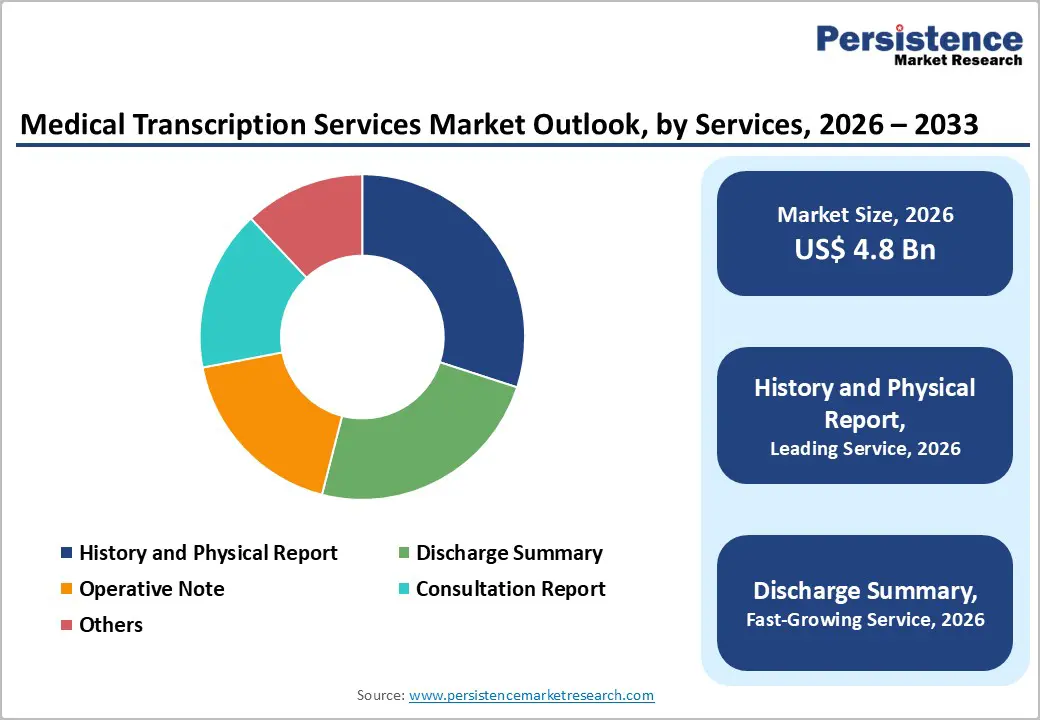

- Service Segments: History & physical reports lead the market with approximately 30% share in 2026, while discharge summaries are the fastest-growing, supported by continuity-of-care and regulatory documentation needs.

- End-user Landscape: Hospitals account for 55% of demand in 2026, while diagnostic centers are the fastest-growing segment due to rising diagnostic testing volumes and outpatient expansion.

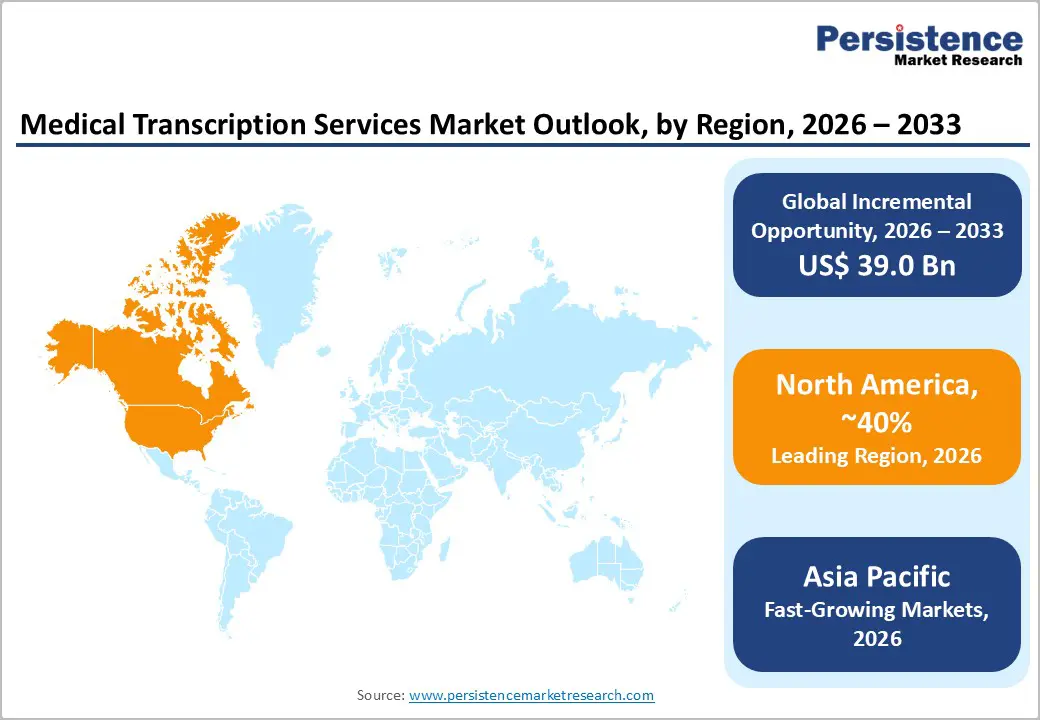

- Regional Leadership: North America leads with 40% share in 2026, while Asia Pacific is the fastest-growing region, registering a CAGR of 6.8% through 2033, driven by strong offshoring medical transcription services and healthcare digitization.

- Competitive Environment: Market is shifting toward AI-enabled hybrid transcription models, integrating automation with human validation to improve accuracy, efficiency, and turnaround time.

| Key Insights | Details |

|---|---|

|

Medical Transcription Services Market Size (2026E) |

US$ 87.5 Bn |

|

Market Value Forecast (2033F) |

US$ 126.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.9% |

DRO Analysis

Driver - Rising Adoption of Electronic Health Records (EHR) and Digital Healthcare Systems

The global healthcare industry has rapidly transitioned toward digitized recordkeeping, with EHR adoption exceeding 90% in major developed markets such as the United States, according to federal healthcare digitization programs under the U.S. Office of the National Coordinator for Health IT. This shift is significantly increasing demand for structured clinical documentation, directly boosting the medical transcription services market.

Hospitals require accurate conversion of physician voice notes into standardized digital formats. Interoperability mandates and compliance frameworks further reinforce this need. As a result, transcription services have become integral to healthcare IT ecosystems. Microsoft’s expansion of its Dragon Copilot AI clinical documentation into hospital workflows reflects how EHR systems are evolving into AI-assisted platforms requiring structured transcription validation.

The transition toward fully integrated digital healthcare systems is reshaping clinical workflows and increasing reliance on real-time documentation for diagnosis, treatment, and insurance processing. The rising complexity of patient records across specialties is also increasing demand for standardized medical language conversion. These factors strengthen dependency on professional transcription support for seamless data exchange.

Recent deployments of AI-enabled clinical documentation tools across hospitals further highlight a hybrid model, where automation is combined with human-verified transcription. This ensures regulatory compliance, reduces documentation delays, and improves interoperability across healthcare systems.

Growing Pressure to Reduce Healthcare Operational Costs and Workforce Optimization

Healthcare providers globally face rising operational expenditures, with administrative costs accounting for nearly 25–30% of total healthcare spending in some developed economies. This has accelerated the adoption of outsourcing medical transcription as a cost-efficient alternative to in-house teams. Outsourcing reduces labor costs by 40–60% while maintaining accuracy and turnaround efficiency.

Offshoring to countries such as India and the Philippines further strengthens cost advantages through skilled, lower-cost labor access. This cost optimization trend is a structural driver for the medical transcription services industry, especially among smaller healthcare facilities. AI-assisted documentation tools have further reinforced demand for hybrid outsourcing models combining automation and human review.

Beyond cost savings, healthcare organizations are prioritizing workforce efficiency and clinical productivity. Outsourcing transcription allows medical professionals to focus more on patient care and less on administrative documentation. This helps reduce clinician burnout, a growing global concern.

Rising patient volumes and limited administrative staffing further increase reliance on external transcription support. At the same time, AI-driven documentation adoption across healthcare systems has strengthened the need for secure, structured transcription workflows. This is particularly critical in regulated environments where compliance frameworks require audit-ready and accurate clinical records.

Restraints - Data Security Risks and Regulatory Compliance Challenges

One of the key restraints in the medical transcription services market is the rising risk of data breaches combined with strict regulatory requirements. Healthcare data is highly sensitive and governed by frameworks such as HIPAA in the U.S. and GDPR in Europe, where even minor workflow violations can lead to heavy penalties and reputational loss. Increasing cyberattacks on healthcare systems have made providers more cautious about outsourcing transcription services, particularly in regions with weaker cybersecurity infrastructure. This has slowed market adoption and increased compliance-related onboarding complexity for vendors. This risk has been reinforced by several incidents involving healthcare organizations and third-party vendors.

Notable cases include the Frederick Health ransomware attack and the Episource healthcare data breach, which exposed large volumes of patient records through compromised digital healthcare systems. In addition, multiple cloud-related misconfigurations in healthcare IT environments reported during 2025–2026 highlighted persistent vulnerabilities in outsourced documentation workflows. These incidents, disclosed through official healthcare data security reporting channels, have led to tighter HIPAA enforcement, stricter audit requirements, and increased demand for secure, certified transcription partners, ultimately slowing outsourcing expansion.

Accuracy, Dependency, and Technological Disruption Risks

Medical transcription demands high precision, as even small errors in clinical documentation can directly impact patient safety, treatment decisions, and legal outcomes. This creates a strong dependency on quality-controlled transcription workflows. However, the rapid adoption of AI-based speech recognition and ambient clinical documentation tools is disrupting traditional transcription services by reducing manual intervention and shifting documentation toward automation. While efficiency improves, challenges remain in handling complex medical terminology, accents, and multilingual clinical environments.

Large-scale deployment of AI-powered ambient documentation systems integrated into hospital EHR platforms has accelerated this shift, reducing reliance on manual transcription in several healthcare settings. However, the hospital's use has also revealed inconsistent accuracy in AI-generated clinical notes, increasing the need for human verification.

Regulatory and healthcare governance reviews during this period have further flagged risks such as unreliable generative AI outputs, data integrity issues, and compliance gaps when non-certified tools are used in clinical workflows. Instances of healthcare staff using unauthorized AI transcription tools have also raised liability concerns, prompting stricter oversight. As a result, healthcare providers are increasingly adopting hybrid models that combine AI efficiency with human-reviewed transcription to maintain accuracy and regulatory compliance.

Opportunity - Expansion in Emerging Healthcare Markets

Emerging economies in Asia Pacific, Latin America, and parts of Africa represent a significant growth opportunity for the medical transcription services market, where healthcare digitization is still in early stages. Countries such as India and China are investing heavily in hospital infrastructure and digital health systems. The market opportunity in these regions is estimated to exceed US$ 15–20 billion, driven by rising hospital admissions and government-backed healthcare modernization programs.

The availability of skilled English-speaking medical professionals makes these regions highly suitable for global outsourcing and offshoring models. Expanding healthcare access and growing digital hospital networks are further increasing demand for structured clinical documentation.

This opportunity has been strengthened through large-scale national digital health initiatives and real-world deployment of structured electronic medical record systems. For example, the UK’s National Health Service (NHS) began rolling out AI-powered ambient clinical documentation tools in 2025 to reduce physician workload, reflecting growing government support for digitized clinical workflows.

Similarly, India’s ongoing expansion of the Ayushman Bharat Digital Mission (ABDM) is accelerating the adoption of interoperable digital health records across public hospitals, while China continues scaling hospital digitization under its national e-health modernization agenda. These developments highlight a global shift toward standardized, high-volume healthcare documentation systems, reinforcing long-term demand for scalable and compliant transcription services.

Integration of AI-Assisted Transcription with Human Verification

A major opportunity lies in hybrid transcription models combining artificial intelligence with human expertise. AI-based speech-to-text tools can reduce turnaround time by 30–50%, while human transcriptionists ensure clinical accuracy and contextual validation. This hybrid approach is increasingly adopted by hospitals aiming to improve workflow efficiency without compromising quality. Vendors offering AI-integrated clinical documentation services are expected to capture a growing share of the medical transcription services industry, particularly in North America and Europe, where regulatory and compliance standards require high documentation accuracy. This opportunity has expanded due to wider enterprise adoption of AI-enabled clinical documentation tools integrated into hospital EHR systems.

Leading healthcare institutions, such as Mayo Clinic have continued scaling AI-assisted documentation pilots in 2025 to reduce physician administrative burden, while still maintaining structured human review processes for clinical safety and accuracy.

Healthcare regulatory discussions in 2026 in the U.S. have increasingly emphasized requirements for auditability, traceability, and governance of AI-generated medical records. These developments reinforce a clear industry direction where AI enhances documentation speed and efficiency, but human-in-the-loop validation remains essential for compliance, safety, and legal accountability, strengthening long-term demand for hybrid transcription service models.

Category-wise Analysis

Procurement Mode Insights

The outsourcing medical transcription segment dominates procurement mode, accounting for approximately 62% of the global market share in 2026. Hospitals and clinics increasingly depend on third-party vendors to manage rising documentation workloads efficiently. Outsourcing reduces costs by up to 60% compared to in-house teams, making it a preferred operational model. It also ensures scalability during peak patient volumes and improves turnaround time for clinical documentation.

The growth of cloud-based healthcare systems and secure data transfer technologies has further strengthened adoption. U.S. hospital networks expanded outsourcing contracts to manage EHR workload pressure and clinician burnout, while stricter BAA (Business Associate Agreement) compliance enforcement in 2026 pushed demand toward certified and secure vendors, strengthening structured outsourcing adoption.

The offshoring medical transcription segment is expected to be the fastest-growing procurement model. India and the Philippines continue to lead as global hubs due to low operational costs and a strong base of skilled professionals. Offshoring also enables 24/7 documentation processing through time-zone advantages, improving operational efficiency. Secure VPN-based healthcare systems are enhancing data protection and regulatory compliance. These factors are accelerating global adoption of offshore transcription services.

India expanded healthcare IT-enabled service exports through government-supported digital workforce initiatives, while Southeast Asia saw rising outsourcing partnerships to manage growing patient volumes, further supported by stricter U.S. cybersecurity guidance promoting secure offshore documentation frameworks.

Service Insights

The history and physical report segment is expected to lead the market with approximately 30% share in 2026, making it the largest service category. These reports are critical for patient assessment, diagnosis, and treatment planning, forming a core part of hospital workflows. High patient admissions ensure steady demand across healthcare facilities. Their structured format supports standardized documentation and improves clinical decision-making. Integration with EHR systems has further increased their importance.

In 2026, hospitals implemented EHR modernization programs focused on standardizing admission templates to reduce documentation errors, while European healthcare systems strengthened structured intake reporting to improve interoperability and data consistency.

The discharge summary segment is projected to be the fastest-growing service. The growth is driven by rising hospital throughput and the need for structured post-treatment documentation. These summaries ensure continuity of care after patient discharge and support insurance and reimbursement processes. Value-based healthcare models are also increasing their importance. Hospitals are prioritizing accuracy and speed in discharge documentation.

Regional Analysis

North America Medical Transcription Services Market Trends

North America is expected to lead the medical transcription services market, accounting for approximately 40% of global revenue in 2026, driven primarily by the United States. The region benefits from advanced healthcare IT infrastructure, widespread EHR adoption, and strong regulatory frameworks such as HIPAA. Hospitals and integrated healthcare systems increasingly rely on outsourced transcription services to manage high documentation volumes efficiently. Strong digital health penetration further supports structured clinical documentation demand. High healthcare spending and mature hospital networks continue to reinforce market leadership. The region also shows strong adoption of AI-integrated transcription solutions and secure cloud-based documentation platforms.

North America has seen increased hospital-level investment in digital documentation efficiency, particularly through workflow modernization initiatives aimed at reducing clinician administrative burden. For instance, large U.S. healthcare systems such as Cleveland Clinic have expanded enterprise-wide deployment of AI-supported clinical documentation tools to improve physician workflow efficiency and reduce documentation turnaround time, reflecting broader institutional adoption of hybrid documentation systems.

U.S. Centers for Medicare & Medicaid Services (CMS) documentation compliance updates in 2026 have emphasized stricter auditability and accuracy requirements for electronic clinical records, reinforcing demand for structured transcription services. These developments highlight a dual trend of automation adoption alongside stronger regulatory enforcement, sustaining demand for compliant transcription workflows.

Europe Medical Transcription Services Market Trends

Europe is a major market for medical transcription services, driven by strong healthcare systems in countries such as Germany, the U.K., France, and Spain. The region benefits from harmonized data protection regulations under GDPR, ensuring standardized healthcare data privacy across countries. Demand is strongly influenced by an aging population and rising chronic disease burden, which increases clinical documentation requirements.

Hospitals are increasingly investing in structured digital record systems to improve efficiency and care coordination. Germany leads in hospital digitization, while the U.K.’s NHS continues advancing digital health transformation initiatives. France and Spain are also strengthening outpatient and hospital documentation systems across public healthcare networks.

Europe has accelerated healthcare digitalization through national hospital modernization programs and system-wide documentation upgrades. For example, Germany’s KHZG-backed hospital digitization rollout expanded in 2026, supporting large-scale implementation of electronic documentation systems across public hospitals, increasing reliance on structured clinical transcription. In France, public healthcare modernization initiatives in 2026 focused on improving interoperability between hospital systems and national health databases, driving greater standardization of patient records. Additionally, the U.K. healthcare system has continued efficiency programs aimed at reducing administrative burden through structured digital documentation workflows.

Asia Pacific Medical Transcription Services Market Trends

Asia Pacific is projected to be the fastest-growing region in the medical transcription services market, expected to expand at a CAGR of 6.8% by 2033. Growth is driven by rapid healthcare infrastructure development across China, India, Japan, and ASEAN countries. The region is witnessing strong expansion in hospital capacity and digital health adoption. Increasing medical tourism is also contributing to higher documentation requirements.

Cost advantages and the availability of skilled professionals support strong outsourcing and offshoring demand. Government-led healthcare digitization programs are further accelerating structured documentation adoption across hospitals.

Asia Pacific has experienced strong momentum through large-scale digital health infrastructure expansion and hospital digitization initiatives. For instance, in China, ongoing National Health Commission-backed hospital digital transformation initiatives in 2026 have further expanded electronic medical record adoption across tier-2 and tier-3 cities, improving standardization of clinical data.

Japan’s Ministry of Health-led digital healthcare efficiency programs in 2025 have focused on reducing administrative workload in aging-care hospitals through digitized documentation systems, reinforcing steady transcription demand. These developments collectively strengthen Asia Pacific’s position as the fastest-growing regional market, driven by scale, digitization speed, and healthcare system modernization.

Competitive Landscape

The global medical transcription services market is moderately fragmented, with leading players such as Nuance Communications (Microsoft), 3M Health Information Systems, Optum, and iMedX holding significant shares due to strong EHR integration and established healthcare contracts. These companies leverage advanced AI-enabled documentation tools, secure transcription platforms, and deep hospital partnerships. Their dominance is supported by compliance expertise across HIPAA and GDPR frameworks. Continuous investment in automation and cloud-based clinical documentation further strengthens their market position.

Mid-sized and regional players such as Acusis, ScribeAmerica, and MTBC (CareCloud) compete through cost-efficient outsourcing, offshore delivery models, and faster turnaround capabilities. The market is also seeing rising participation from AI-driven transcription and ambient documentation providers, enabling hybrid service models. High regulatory requirements and data security standards limit new entrants, pushing the market toward consolidation at the top. At the same time, partnerships between healthcare providers and technology firms are driving gradual platform-based competition.

Key Developments:

- In January 2026, Rapid Care Group acquired DeepDoc to strengthen its AI-driven medical documentation and record intelligence capabilities. The deal enhances automation of unstructured clinical data using generative AI, improving summarization accuracy and reducing manual transcription effort. It also supports faster workflow processing across claims and utilization review systems.

- In August 2025, Optum acquired Holston Medical Group to expand its physician network and strengthen integrated care delivery. The acquisition supports its value-based care strategy by improving clinical coordination across a large provider base. It also indirectly increases demand for structured clinical documentation within large healthcare systems.

Companies Covered in Medical Transcription Services Market

- Microsoft

- Optum

- 3M Health Information Systems

- iMedX Information Services

- Acusis LLC

- ScribeAmerica

- MModal

- TransPerfect

- InSync Healthcare Solutions

- Medscribe

- Global Medical Transcription

- Athreon Corporation

- VIVA Transcription

- iMedAtions

- MTBC

Frequently Asked Questions

The global medical transcription services market is projected to reach US$ 87.5 billion in 2026.

The market is driven by rising EHR adoption, increasing healthcare documentation needs, and growing outsourcing of clinical transcription services.

The medical transcription services market is expected to grow at a CAGR of 5.4% from 2026 to 2033.

Key opportunities include expansion in emerging healthcare markets and adoption of AI-enabled hybrid transcription models.

Key players include Nuance (Microsoft), 3M Health Information Systems, Optum, and iMedX.