- Executive Summary

- Global Medical Waste Management Market Snapshot, 2025 and 2033

- Market Opportunity Assessment, 2025 - 2033, US$ Mn

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Key Trends

- Macro-economic Factors

- Global Sectoral Outlook

- Global GDP Growth Outlook

- COVID-19 Impact Analysis

- Forecast Factors - Relevance and Impact

- Value Added Insights

- Tool Adoption Analysis

- Regulatory Landscape

- Value Chain Analysis

- PESTLE Analysis

- Porter’s Five Force Analysis

- Price Analysis, 2025A

- Key Highlights

- Key Factors Impacting Deployment Costs

- Pricing Analysis, By Waste Type

- Global Medical Waste Management Market Outlook

- Key Highlights

- Market Volume (Units) Projections

- Market Size (US$ Mn) and Y-o-Y Growth

- Absolute $ Opportunity

- Market Size (US$ Mn) and Volume (Units) Analysis and Forecast

- Historical Market Size (US$ Mn) Analysis, 2025-2025

- Market Size (US$ Mn) Analysis and Forecast, 2025 - 2033

- Global Medical Waste Management Market Outlook: Waste Type

- Introduction / Key Findings

- Historical Market Size (US$ Mn) and Volume (Units) Analysis, By Waste Type, 2025 - 2025

- Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Waste Type, 2025 - 2033

- Hazardous

- Non-Hazardous

- Market Attractiveness Analysis: Waste Type

- Global Medical Waste Management Market Outlook: Treatment Technology

- Introduction / Key Findings

- Historical Market Size (US$ Mn) Analysis, By Treatment Technology, 2025 - 2025

- Market Size (US$ Mn) Analysis and Forecast, By Treatment Technology, 2025 - 2033

- Thermal

- Sterilization

- Chemical

- Advanced

- Market Attractiveness Analysis: Treatment Technology

- Global Medical Waste Management Market Outlook: Service & Delivery Model

- Introduction / Key Findings

- Historical Market Size (US$ Mn) Analysis, By Service & Delivery Model, 2025 - 2025

- Market Size (US$ Mn) Analysis and Forecast, By Service & Delivery Model, 2025 - 2033

- Collection

- Transportation

- Storage

- Treatment

- Disposal

- Recycling

- Compliance Services

- Market Attractiveness Analysis: Service & Delivery Model

- Key Highlights

- Global Medical Waste Management Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Mn) and Volume (Units) Analysis, By Region, 2025 - 2025

- Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Region, 2025 - 2033

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Medical Waste Management Market Outlook

- Key Highlights

- Historical Market Size (US$ Mn) Analysis, By Market, 2025 - 2025

- By Country

- By Waste Type

- By Treatment Technology

- By Service & Delivery Model

- Market Size (US$ Mn) Analysis and Forecast, By Country, 2025 - 2033

- U.S.

- Canada

- Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Waste Type, 2025 - 2033

- Hazardous

- Non-Hazardous

- Market Size (US$ Mn) Analysis and Forecast, By Treatment Technology, 2025 - 2033

- Thermal

- Sterilization

- Chemical

- Advanced

- Market Size (US$ Mn) Analysis and Forecast, By Service & Delivery Model, 2025-2033

- Semiconductor & Electronics Manufacturing

- Chemical Processing

- Energy & Power Generation

- Market Attractiveness Analysis

- Europe Medical Waste Management Market Outlook

- Key Highlights

- Historical Market Size (US$ Mn) Analysis, By Market, 2025 - 2025

- By Country

- By Waste Type

- By Treatment Technology

- Service & Delivery Model

- Market Size (US$ Mn) Analysis and Forecast, By Country, 2025 - 2033

- Germany

- France

- U.K.

- Italy

- Spain

- Russia

- Türkiye

- Rest of Europe

- Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Waste Type, 2025 - 2033

- Hazardous

- Non-Hazardous

- Market Size (US$ Mn) Analysis and Forecast, By Treatment Technology, 2025 - 2033

- Thermal

- Sterilization

- Chemical

- Advanced

- Market Size (US$ Mn) Analysis and Forecast, By Service & Delivery Model, 2025-2033

- Collection

- Transportation

- Storage

- Treatment

- Disposal

- Recycling

- Compliance Services

- Market Attractiveness Analysis

- East Asia Medical Waste Management Market Outlook

- Key Highlights

- Historical Market Size (US$ Mn) Analysis, By Market, 2025 - 2025

- By Country

- By Waste Type

- By Treatment Technology

- By Service & Delivery Model

- Market Size (US$ Mn) Analysis and Forecast, By Country, 2025 - 2033

- China

- Japan

- South Korea

- Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Waste Type, 2025 - 2033

- Hazardous

- Non-Hazardous

- Market Size (US$ Mn) Analysis and Forecast, By Treatment Technology, 2025 - 2033

- Thermal

- Sterilization

- Chemical

- Advanced

- Market Size (US$ Mn) Analysis and Forecast, By Service & Delivery Model, 2025-2033

- Collection

- Transportation

- Storage

- Treatment

- Disposal

- Recycling

- Compliance Services

- Market Attractiveness Analysis

- South Asia & Oceania Medical Waste Management Market Outlook

- Key Highlights

- Historical Market Size (US$ Mn) Analysis, By Market, 2025 - 2025

- By Country

- By Waste Type

- By Treatment Technology

- By Service & Delivery Model

- Market Size (US$ Mn) Analysis and Forecast, By Country, 2025 - 2033

- India

- Southeast Asia

- ANZ

- Rest of South Asia & Oceania

- Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Waste Type, 2025 - 2033

- Hazardous

- Non-Hazardous

- Market Size (US$ Mn) Analysis and Forecast, By Treatment Technology, 2025 - 2033

- Thermal

- Sterilization

- Chemical

- Advanced

- Market Size (US$ Mn) Analysis and Forecast, By Service & Delivery Model, 2025-2033

- Collection

- Transportation

- Storage

- Treatment

- Disposal

- Recycling

- Compliance Services

- Market Attractiveness Analysis

- Latin America Medical Waste Management Market Outlook

- Key Highlights

- Historical Market Size (US$ Mn) Analysis, By Market, 2025 - 2025

- By Country

- By Waste Type

- By Treatment Technology

- By Service & Delivery Model

- Market Size (US$ Mn) Analysis and Forecast, By Country, 2025 - 2033

- Brazil

- Mexico

- Rest of Latin America

- Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Waste Type, 2025 - 2033

- Hazardous

- Non-Hazardous

- Market Size (US$ Mn) Analysis and Forecast, By Treatment Technology, 2025 - 2033

- Thermal

- Sterilization

- Chemical

- Advanced

- Market Size (US$ Mn) Analysis and Forecast, By Service & Delivery Model, 2025-2033

- Collection

- Transportation

- Storage

- Treatment

- Disposal

- Recycling

- Compliance Services

- Market Attractiveness Analysis

- Middle East & Africa Medical Waste Management Market Outlook

- Key Highlights

- Historical Market Size (US$ Mn) Analysis, By Market, 2025 - 2025

- By Country

- By Waste Type

- By Treatment Technology

- By Service & Delivery Model

- Market Size (US$ Mn) Analysis and Forecast, By Country, 2025 - 2033

- GCC Countries

- Egypt

- South Africa

- Northern Africa

- Rest of Middle East & Africa

- Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Waste Type, 2025 - 2033

- Hazardous

- Non-Hazardous

- Market Size (US$ Mn) Analysis and Forecast, By Treatment Technology, 2025 - 2033

- Thermal

- Sterilization

- Chemical

- Advanced

- Market Size (US$ Mn) Analysis and Forecast, By Service & Delivery Model, 2025-2033

- Collection

- Transportation

- Storage

- Treatment

- Disposal

- Recycling

- Compliance Services

- Market Attractiveness Analysis

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping By Market

- Competition Dashboard

- Company Profiles (Details - Overview, Financials, Strategy, Recent Developments)

- SteriTech Global

- Overview

- Segments and Deployments

- Key Financials

- Market Developments

- Market Strategy

- CleanEarth Waste Management

- GreenCycle Medical Services

- BioSafe Solutions

- EcoWaste Systems

- MediClear Services

- AsiaMed Waste Solutions

- TerraMed Inc.

- SafePath Waste Solutions

- RenewMed Solutions

- MedWaste Compliance Group

- CleanTech Disposal

- SteriTech Global

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Healthcare Services

- Medical Waste Management Market

Medical Waste Management Market Size, Share, and Growth Forecast, 2026 - 2033

Medical Waste Management Market by Waste Type (Hazardous, Non-Hazardous), Treatment Technology (Thermal, Sterilization, Chemical, Advanced), Service & Delivery Model (Collection, Transportation, Storage, Treatment, Disposal, Recycling, Compliance Services), and Regional Analysis for 2026 - 2033

Key Industry Highlights

- Dominant Waste Type: Hazardous waste is set to command around 43% revenue share in 2026, while non-hazardous waste is likely to grow the fastest through 2033, driven by recycling mandates.

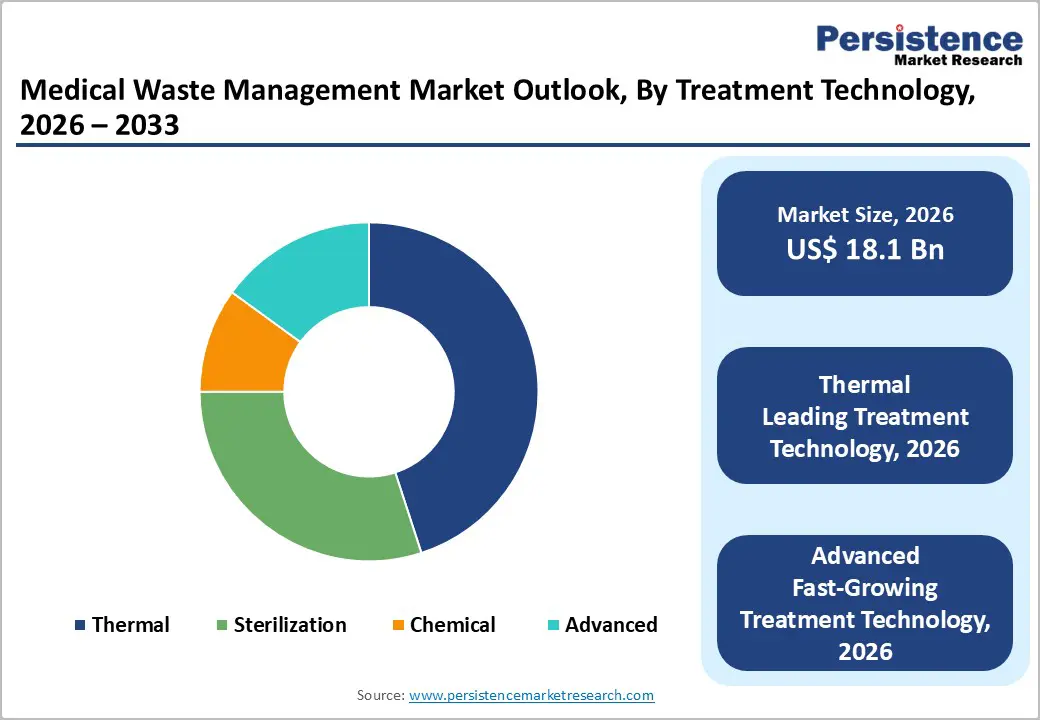

- Leading Treatment Technology: Thermal treatment is expected to hold about 40% revenue share in 2026, with advanced technologies likely to grow the fastest at about 12.3% CAGR through 2033, due to environmental and efficiency advantages.

- Dominant Service: Treatment services are projected to account for 39% of market revenue in 2026, whereas compliance services are poised to grow the fastest through 2033, reflecting regulatory tightening.

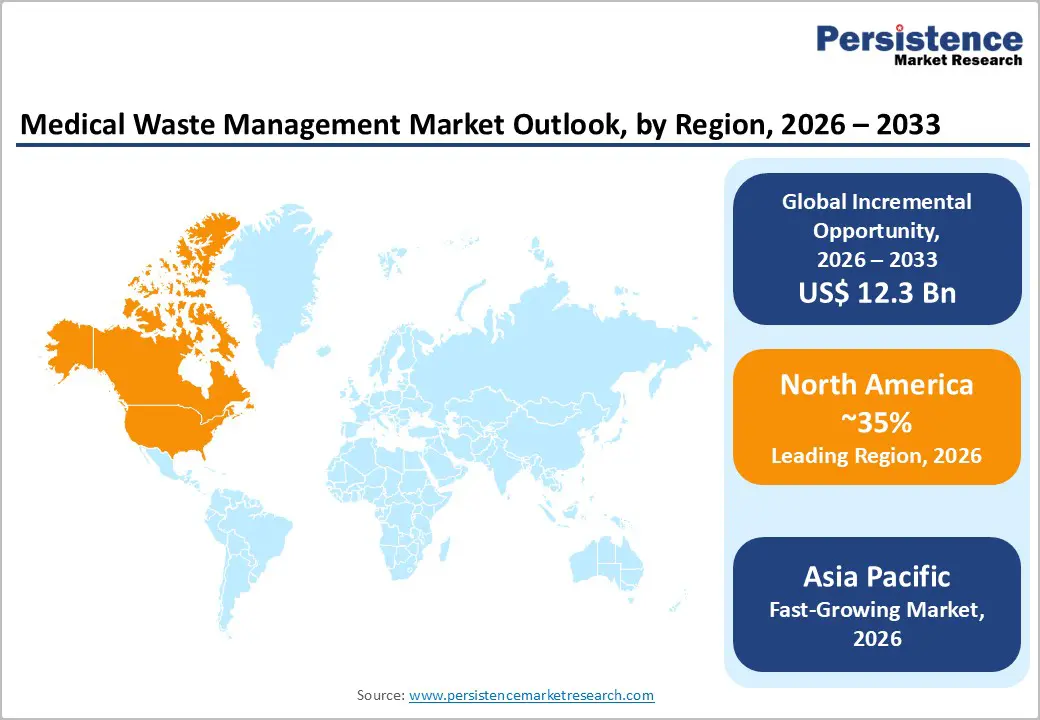

- Regional Leadership: North America is poised to lead with an estimated 35% share in 2026, while Asia Pacific is expected to register the fastest growth at roughly 12.2% CAGR through 2033, driven by healthcare infrastructure expansion.

- Competitive Dynamics: Mergers, technology partnerships, and geographic expansions are reshaping the market, targeting enhanced treatment capacity, digital compliance solutions, and emerging markets in India and Southeast Asia.

| Key Insights | Details |

|---|---|

|

Substation Automation Market Size (2026E) |

US$ 18.1 Bn |

|

Market Value Forecast (2033F) |

US$ 30.4 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

10.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Healthcare Activities and Waste Generation

Healthcare service demand is increasing globally powered by aging populations and surging prevalence of non-communicable diseases (NCDs), leading to higher volumes of medical and hazardous waste. According to the WHO, about 15% of health-care waste is hazardous, requiring specialized handling and treatment due to infection and contamination risks. Regions such as North America and Europe continue to report annual per capita increases in medical waste generation, driven by more surgeries, diagnostics, vaccinations, and outpatient services. This trend accelerates demand for advanced treatment, compliance, and disposal services.

In response, cities and healthcare systems are upgrading capacity to handle this rising waste. For example, the Delhi government has announced new biomedical waste treatment facilities to address increasing waste volumes by installing modern autoclaving, shredding, and disposal systems to support daily waste needs. These initiatives reflect how rising healthcare activities are creating sustained demand for scalable medical waste management infrastructure, making waste generation a primary growth driver for the sector.

Strengthened Regulations and Technological Innovation

Governments and global institutions have significantly reinforced regulatory frameworks governing medical waste handling and disposal. Policies such as the U.S. Resource Conservation and Recovery Act (RCRA) and EU packaging waste reforms (Regulation (EU) 2025/40) impose rigorous traceability, segregation, and environmental requirements that healthcare facilities must meet to avoid penalties. In India, local health departments are actively cracking down on improper medical waste disposal, conducting inspections and threatening punitive actions against non-compliant facilities, a clear sign of regulatory enforcement strengthening in 2025.

Technological innovation is further supporting compliance and efficiency. Hospitals and treatment facilities are adopting fully automated waste collection and treatment systems, such as the automated infectious waste solution installed at Rennes University Hospital in France, which processes hazardous waste in under 20-seconds without direct human contact. Digital solutions such as IoT-enabled tracking and real-time monitoring are helping healthcare providers reduce handling costs and improve regulatory documentation. Together, stricter regulations and advanced technology adoption are driving market growth by improving safety, efficiency, and compliance outcomes.

High Capital Expenditure and Infrastructure Barriers

Establishing medical waste management infrastructure, such as thermal treatment plants, advanced sterilization units, and digital tracking systems, requires significant upfront capital, creating a barrier for smaller hospitals and clinics in resource-limited regions. According to a World Bank healthcare infrastructure survey, nearly 40% of facilities in lower-middle-incomeincome countries lack proper treatment technologies, directly reflecting cost constraints. Limited budgets often result in outdated methods or informal disposal practices that compromise safety and environmental integrity. These high costs also include ongoing maintenance, staff training, and regulatory compliance, which many facilities cannot sustain.

Recent global reporting shows that billions of people still receive care in facilities without basic waste management services, underlining persistent infrastructure gaps despite expansion efforts. The WHO/UNICEF 2025 progress report finds that 2.8 billion people are served by healthcare facilities without basic waste services, stressing that investment remains insufficient to close this gap by 2030. As a result, many healthcare providers continue to rely on unsafe disposal methods or local informal solutions. The combination of high capital costs and inadequate funding prevents widespread adoption of standardized solutions, slowing overall market growth and widening regional disparities.

Fragmented Supply Chain and Skilled Labor Shortages

Effective medical waste management requires coordinated logistics spanning collection, segregation, transport, treatment, and recycling. However, fragmented supply chains and inconsistent infrastructure distribution, particularly in rural or underserved areas, lead to logistical bottlenecks, operational inefficiencies, and delayed waste treatment. For example, India’s Common Biomedical Waste Treatment Facilities (CBWTFs) are unevenly accessible, leaving remote regions to rely on distant or suboptimal systems, which hinders reliable service delivery. Coordination challenges among multiple vendors further exacerbate delays, increasing operational risk.

Skilled personnel shortages also significantly constrain market performance. India’s healthcare waste system, despite having regulations in place, suffers from limited training and monitoring gaps, with many workers lacking adequate expertise in waste categorization and advanced treatment equipment handling. Recent news from Gujarat shows biomedical waste rule violations increasing five-fold in 2024 as monitoring and compliance challenges grow, even where treatment infrastructure exists. These labor and logistical constraints remain critical restraints, limiting the ability to standardize and scale safe medical waste management globally while maintaining regulatory compliance.

Expansion in Emerging Economies through Healthcare Infrastructure Growth

Rapid healthcare infrastructure growth in regions such as Asia Pacific, Latin America, and parts of Africa is generating higher volumes of medical waste, creating a scalable demand for waste management services. Investments in hospitals, diagnostic centers, vaccination campaigns, and outpatient services continue to expand healthcare delivery, especially in India, China, and Southeast Asia. The World Bank projects healthcare spending in developing Asia will grow 6–8% annually through 2030, driving proportional increases in waste management demand. Adoption of joint ventures and public-private partnerships (PPPs) enables global and regional players to establish local expertise and secure long-term service contracts.

On the ground, new healthcare system expansions and facility modernization plans are already underway. For instance, the Delhi government is planning a next-generation healthcare system with digital hospitals and advanced medical technology integration, signaling further infrastructure growth that will require enhanced waste management services. The rollout of 1,100 Ayushman Arogya Mandirs and expanded hospital capacity in Delhi, including new beds and advanced equipment, reiterates sustained investment in public healthcare delivery. These developments make emerging economies a high-growth platform for integrated waste solutions, training programs, and facility partnerships.

Sustainable and Digital Waste Management Solutions

Environmental sustainability and circular economy principles are reshaping medical waste management strategies, creating opportunities for green and digital solutions. Innovations such as sterilization methods that enable material reuse, biodegradable packaging, and bioenergy recovery align with global carbon reduction agendas. Digital platforms that enable real-time tracking and regulatory reporting help providers meet tightening environmental standards. In Bhutan, the government, supported by the UN Development Programme (UNDP), launched the mWASTE digital platform to monitor healthcare waste from generation to disposal, illustrating how digital tools enhance planning and compliance.

Similarly, regional initiatives are emphasizing smart systems and accountability. The UNDP’s Regional Dialogue on Sustainable Healthcare Waste Management in Asia Pacific highlighted priorities such as digital tracking systems and circular models to reduce, reuse, and recycle health-care waste. These developments reflect rising global recognition of sustainable medical waste practices. Complementing this, urban experiments with IoT-enabled smart bins for real-time waste monitoring demonstrate broader municipal interest in sensor-based segregation and monitoring technologies. Together, these shifts toward green treatment technologies and smart compliance systems create robust opportunities for suppliers and service providers focused on sustainability and regulatory integration.

Category-wise Analysis

Waste Type Insights

Hazardous medical waste, including infectious sharps, pathological tissues, and chemical residues, is likely to remain the largest revenue contributor at around 43% in 2026 due to stringent handling regulations and specialized treatment needs. Governments require careful segregation, licensing, and documented disposal to mitigate infection and environmental risks. In early 2026, the UK’s Environment Agency updated guidance on hazardous healthcare waste storage and transport, reinforcing tighter controls across the National Health Service (NHS) and private facilities. Enhanced waste handler training and certification programs in Europe and North America ensure compliance with regulatory frameworks. These combined enforcement and preparedness efforts sustain premium demand for hazardous treatment services, reinforcing the segment’s leadership position.

Non-hazardous waste, such as uncontaminated paper, packaging, and plastics, is projected to expand at a CAGR of approximately 11.8% through 2033, driven by rising procedural volumes, outpatient services, and recycling mandates. Proactive source segregation is reducing treatment costs and enabling more efficient recycling pathways across healthcare networks. In 2025, Canada’s Nova Scotia health authorities announced expanded recycling programs for uncontaminated health facility waste, illustrating proactive provincial action on non-hazardous streams. Structured recycling efforts and environmental incentives are accelerating the adoption of cost-efficient non-hazardous waste solutions, reinforcing its rapid growth trajectory worldwide.

Treatment Technology Insights

Thermal treatment solutions, including high-temperature incineration and autoclaving, are poised lead with an estimated 40% of the medical waste management market revenue share in 2026, particularly in regions with mandated disposal protocols. Regulatory frameworks in North America and Europe favor established thermal methods for reliable pathogen neutralization and volume reduction. In late 2025, the U.S. Department of Energy reported support for upgraded catalytic air pollution control units on medical incinerators to ensure compliance with stricter Clean Air Act emissions standards. Continued investment in emissions controls and robust performance benchmarks sustains thermal technologies as the backbone of large-scale treatment infrastructure.

Advanced treatment technologies, including microwave systems, plasma gasification, and hybrid processes, are expanding at a CAGR of approximately 12.3% through 2033, supported by environmental and sustainability mandates. These systems lower emissions, reduce residual waste, and enable energy recovery potential. In 2025, the Australian Department of Health funded pilot projects for non-combustion waste technologies at major regional hospitals, highlighting government support for eco-efficient solutions. As decarbonization and sustainable infrastructure goals intensify, the adoption of advanced treatment systems rises rapidly, especially where governments offer incentives or pilot program support.

Regional Insights

North America Medical Waste Management System Trends

North America is projected to holds the largest share of the medical waste management market around 35% in 2026, led by the U.S. due to advanced healthcare infrastructure, high per?capita waste generation, and stringent environmental and worker safety regulations. Regulatory bodies such as the U.S. EPA and the Occupational Safety and Health Administration (OSHA) enforce rigorous hazardous waste handling, transport, and disposal standards, driving demand for compliance outsourcing and sophisticated treatment services. In 2025, major waste management players reported strong revenue growth in North America, reflecting increased investment in environmental security and integrated waste services.

Hospital systems and clinics increasingly adopt digital tracking, automated sterilization, and integrated compliance platforms, spurred by federal funding aimed at modernizing healthcare infrastructure. Competitive dynamics include consolidation among established service providers and technology integration for traceability and emissions reduction. Collaborative initiatives between municipal health departments and private firms are expanding regional treatment capacity. Projections show the region maintaining a strong growth trajectory, supported by innovation in low?emission thermal processing and advanced treatment deployment, reinforcing North America’s leadership position.

Europe Medical Waste Management System Trends

Europe is a major regional market, anchored by Germany, the U.K., France, and Spain, with well-established healthcare systems and strong regulatory oversight. Updated EU regulations, including the packaging and waste shipment rules effective in 2026, are tightening standards for waste prevention, recycling, and environmentally sound disposal, requiring healthcare facilities and waste handlers to adopt standardized protocols. Hospitals and clinics must ensure proper segregation, documented handling, and timely reporting of both hazardous and non-hazardous waste streams. These regulations also promote higher-value recycling and safe end-of-life treatment, encouraging investment in advanced technologies and compliance systems. Cross-border waste shipments are closely monitored, and facilities are increasingly integrating digital.

Key market drivers include investment in advanced treatment systems, expansion of compliance services, and alignment with EU circular economy initiatives. Germany leads with robust tracking and treatment enforcement, France and Spain invest in emissions reduction technologies, while the U.K. prioritizes domestic treatment standards post?Brexit. Cross?border waste logistics have been affected by new EU shipment rules, prompting healthcare providers and waste firms to optimize regional networks. Market growth is supported by technological modernization, regulatory harmonization, and structured public?private collaborations in sustainable waste management.

Asia Pacific Medical Waste Management System Trends

Asia Pacific is expected to be the fastest?growing regional market for medical waste management solutions, projected to expand at approximately 12.2% CAGR through 2033, driven by rapid healthcare system expansion, rising healthcare spending, and policy support for waste infrastructure enhancements. Countries across the region are modernizing medical waste practices and investing in scalable compliance solutions. China’s healthcare sector continues to invest heavily in facilities and treatment systems to meet rising waste volumes. Regulatory frameworks in the region emphasize real?time monitoring and treatment compliance, further enabling market growth.

In 2025 and early 2026, governments and health ministries across Asia Pacific highlighted initiatives to upgrade waste management systems with advanced technologies and data tracking platforms, reflecting an ongoing commitment to environmental safety and public health. Collaboration with international health agencies has also encouraged adoption of sustainable practices. ASEAN nations are leveraging public?private partnerships to strengthen region?wide waste treatment networks. With expanding healthcare capacity and supportive policy environments, Asia Pacific is capturing significant market momentum, complementing the leadership position of North America and Europe.

Competitive Landscape

The global medical waste management market structure is moderately consolidated, with top players, including Veolia, Stericycle, Clean Harbors, and Remondis, controlling a significant portion of market revenue. These established firms leverage long-standing relationships with hospitals, diagnostic centers, and government agencies, combined with expertise in regulatory compliance, treatment technology, and integrated service offerings. They continue to invest heavily in R&D, adopting advanced sterilization systems, thermal treatment upgrades, digital compliance platforms, and smart waste tracking solutions to maintain a competitive edge.

Regional and niche competitors, such as SUEZ, Daniels Health, and Steri?Tech, focus on specialized waste streams or target specific geographic markets. Barriers such as stringent environmental regulations, hazardous material handling compliance, and complex logistics limit new entrants. However, digitalization trends, including IoT-enabled tracking, cloud-based reporting, and automated treatment monitoring, are enabling technology-driven firms to enter the market via partnerships and software integration. Market consolidation is expected to rise gradually as global leaders acquire smaller regional providers to expand geographically and technologically, while innovation partnerships accelerate adoption of sustainable and advanced treatment solutions.

Key Industry Developments

- In February 2026, the Delhi government announced plans to establish new common biomedical waste treatment facilities to address rising waste volumes of around 40 tons per day, with projected capacity reaching 46 tons daily to meet future demand. The initiative aims to improve processing efficiency, reduce treatment backlogs, and deploy advanced technologies such as autoclaving and shredding.

- In January 2026, Daniels Health expanded with its first dedicated medical waste facility in Long Island, USA, through a US$ 6.69?million property purchase in early 2026, indicating strategic growth in physical treatment infrastructure.

- In June 2025, CSIR-NIIST developed an in-situ biomedical waste disposal technology that disinfects pathogenic waste such as blood and laboratory disposables without using energy-intensive incineration, converting it into safe, value-added soil additives. The system reduces environmental risks, minimizes human exposure, and offers a cost-effective alternative for healthcare facilities.

Companies Covered in Medical Waste Management Market

- SteriTech Global

- CleanEarth Waste Management

- GreenCycle Medical Services

- BioSafe Solutions

- EcoWaste Systems

- MediClear Services

- AsiaMed Waste Solutions

- TerraMed Inc.

- SafePath Waste Solutions

- RenewMed Solutions

- MedWaste Compliance Group

- CleanTech Disposal

Frequently Asked Questions

The global medical waste management market is projected to reach US$ 18.1 billion in 2026.

Rising healthcare waste generation, stringent regulations, and adoption of advanced treatment and compliance solutions are driving market growth.

The market is expected to grow at a CAGR of 7.7% from 2026 to 2033.

Expansion in emerging economies, adoption of sustainable treatment technologies, and digital compliance services are major opportunities.

Veolia, Stericycle, Clean Harbors, Remondis, SUEZ, Daniels Health are some of the leading players globally.