- Executive Summary

- Global Medical Imaging Informatics Market Snapshot, 2025 and 2033

- Market Opportunity Assessment, 2025 - 2033, US$ Bn

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Key Trends

- Macro-economic Factors

- Global Sectoral Outlook

- Global GDP Growth Outlook

- COVID-19 Impact Analysis

- Forecast Factors - Relevance and Impact

- Value Added Insights

- Tool Adoption Analysis

- Regulatory Landscape

- Value Chain Analysis

- PESTLE Analysis

- Porter’s Five Force Analysis

- Price Analysis, 2025A

- Key Highlights

- Key Factors Impacting Deployment Costs

- Pricing Analysis, By Product Type

- Global Medical Imaging Informatics Market Outlook

- Key Highlights

- Market Volume (Units) Projections

- Market Size (US$ Bn) and Y-o-Y Growth

- Absolute $ Opportunity

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast

- Historical Market Size (US$ Bn) Analysis, 2025-2025

- Market Size (US$ Bn) Analysis and Forecast, 2025 - 2033

- Global Medical Imaging Informatics Market Outlook: Product Type

- Introduction / Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis, By Product Type, 2025 - 2025

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2025 - 2033

- Picture Archiving & Communication System (PACS)

- Radiology Information System (RIS)

- Vendor Neutral Archive (VNA)

- Cardiology Information System

- Enterprise Imaging Platforms

- Imaging Analytics & AI

- Market Attractiveness Analysis: Product Type

- Global Medical Imaging Informatics Market Outlook: Deployment Mode

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Deployment Mode, 2025 - 2025

- Market Size (US$ Bn) Analysis and Forecast, By Deployment Mode, 2025 - 2033

- On-Premise

- Cloud-Based

- Hybrid

- Market Attractiveness Analysis: Deployment Mode

- Global Medical Imaging Informatics Market Outlook: End-User

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By End-User, 2025 - 2025

- Market Size (US$ Bn) Analysis and Forecast, By End-User, 2025 - 2033

- Hospitals

- Diagnostic Imaging Centers

- Ambulatory Care Centers

- Research & Academic Institutes

- Market Attractiveness Analysis: End-User

- Key Highlights

- Global Medical Imaging Informatics Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Units) Analysis, By Region, 2025 - 2025

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Region, 2025 - 2033

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Medical Imaging Informatics Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2025 - 2025

- By Country

- By Product Type

- By Deployment Mode

- By End-User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 - 2033

- U.S.

- Canada

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2025 - 2033

- Picture Archiving & Communication System (PACS)

- Radiology Information System (RIS)

- Vendor Neutral Archive (VNA)

- Cardiology Information System

- Enterprise Imaging Platforms

- Imaging Analytics & AI

- Market Size (US$ Bn) Analysis and Forecast, By Deployment Mode, 2025 - 2033

- On-Premise

- Cloud-Based

- Hybrid

- Market Size (US$ Bn) Analysis and Forecast, By End-User, 2025-2033

- Hospitals

- Diagnostic Imaging Centers

- Ambulatory Care Centers

- Research & Academic Institutes

- Market Attractiveness Analysis

- Europe Medical Imaging Informatics Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2025 - 2025

- By Country

- By Product Type

- By Deployment Mode

- End-User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 - 2033

- Germany

- France

- U.K.

- Italy

- Spain

- Russia

- Türkiye

- Rest of Europe

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2025 - 2033

- Picture Archiving & Communication System (PACS)

- Radiology Information System (RIS)

- Vendor Neutral Archive (VNA)

- Cardiology Information System

- Enterprise Imaging Platforms

- Imaging Analytics & AI

- Market Size (US$ Bn) Analysis and Forecast, By Deployment Mode, 2025 - 2033

- On-Premise

- Cloud-Based

- Hybrid

- Market Size (US$ Bn) Analysis and Forecast, By End-User, 2025-2033

- Hospitals

- Diagnostic Imaging Centers

- Ambulatory Care Centers

- Research & Academic Institutes

- Market Attractiveness Analysis

- East Asia Medical Imaging Informatics Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2025 - 2025

- By Country

- By Product Type

- By Deployment Mode

- By End-User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 - 2033

- China

- Japan

- South Korea

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2025 - 2033

- Picture Archiving & Communication System (PACS)

- Radiology Information System (RIS)

- Vendor Neutral Archive (VNA)

- Cardiology Information System

- Enterprise Imaging Platforms

- Imaging Analytics & AI

- Market Size (US$ Bn) Analysis and Forecast, By Deployment Mode, 2025 - 2033

- On-Premise

- Cloud-Based

- Hybrid

- Market Size (US$ Bn) Analysis and Forecast, By End-User, 2025-2033

- Hospitals

- Diagnostic Imaging Centers

- Ambulatory Care Centers

- Research & Academic Institutes

- Market Attractiveness Analysis

- South Asia & Oceania Medical Imaging Informatics Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2025 - 2025

- By Country

- By Product Type

- By Deployment Mode

- By End-User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 - 2033

- India

- Southeast Asia

- ANZ

- Rest of South Asia & Oceania

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2025 - 2033

- Picture Archiving & Communication System (PACS)

- Radiology Information System (RIS)

- Vendor Neutral Archive (VNA)

- Cardiology Information System

- Enterprise Imaging Platforms

- Imaging Analytics & AI

- Market Size (US$ Bn) Analysis and Forecast, By Deployment Mode, 2025 - 2033

- On-Premise

- Cloud-Based

- Hybrid

- Market Size (US$ Bn) Analysis and Forecast, By End-User, 2025-2033

- Hospitals

- Diagnostic Imaging Centers

- Ambulatory Care Centers

- Research & Academic Institutes

- Market Attractiveness Analysis

- Latin America Medical Imaging Informatics Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2025 - 2025

- By Country

- By Product Type

- By Deployment Mode

- By End-User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 - 2033

- Brazil

- Mexico

- Rest of Latin America

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2025 - 2033

- Picture Archiving & Communication System (PACS)

- Radiology Information System (RIS)

- Vendor Neutral Archive (VNA)

- Cardiology Information System

- Enterprise Imaging Platforms

- Imaging Analytics & AI

- Market Size (US$ Bn) Analysis and Forecast, By Deployment Mode, 2025 - 2033

- On-Premise

- Cloud-Based

- Hybrid

- Market Size (US$ Bn) Analysis and Forecast, By End-User, 2025-2033

- Hospitals

- Diagnostic Imaging Centers

- Ambulatory Care Centers

- Research & Academic Institutes

- Market Attractiveness Analysis

- Middle East & Africa Medical Imaging Informatics Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2025 - 2025

- By Country

- By Product Type

- By Deployment Mode

- By End-User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 - 2033

- GCC Countries

- Egypt

- South Africa

- Northern Africa

- Rest of Middle East & Africa

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2025 - 2033

- Picture Archiving & Communication System (PACS)

- Radiology Information System (RIS)

- Vendor Neutral Archive (VNA)

- Cardiology Information System

- Enterprise Imaging Platforms

- Imaging Analytics & AI

- Market Size (US$ Bn) Analysis and Forecast, By Deployment Mode, 2025 - 2033

- On-Premise

- Cloud-Based

- Hybrid

- Market Size (US$ Bn) Analysis and Forecast, By End-User, 2025-2033

- Hospitals

- Diagnostic Imaging Centers

- Ambulatory Care Centers

- Research & Academic Institutes

- Market Attractiveness Analysis

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping By Market

- Competition Dashboard

- Company Profiles (Details - Overview, Financials, Strategy, Recent Developments)

- GE HealthCare

- Overview

- Segments and Deployments

- Key Financials

- Market Developments

- Market Strategy

- Siemens Healthineers

- Philips Healthcare

- Fujifilm Holdings Corporation

- Agfa-Gevaert Group

- Sectra AB

- Carestream Health

- Merge Healthcare

- Intelerad Medical Systems

- RamSoft

- INFINITT Healthcare

- Novarad Corporation

- Koninklijke Philips NV

- GE HealthCare

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Healthcare Services

- Medical Imaging Informatics Market

Medical Imaging Informatics Market Size, Share, and Growth Forecast, 2026 - 2033

Medical Imaging Informatics Market by Product Type (Picture Archiving & Communication System (PACS), Radiology Information System (RIS), Vendor Neutral Archive (VNA), Cardiology Information System (CVIS), Enterprise Imaging Platforms, Imaging Analytics & AI), Deployment Mode (On-Premise, Cloud-Based, Hybrid), End-User (Hospitals, Diagnostic Imaging Centers, Ambulatory Care Centers, Research & Academic Institutes), and Regional Analysis for 2026 - 2033

Key Industry Highlights

- Regional Leadership: North America is set to dominate with about 40% share in 2026, while Asia Pacific is forecast to record the fastest regional growth at 8.8% CAGR through 2033, supported by healthcare digitalization and imaging infrastructure expansion.

- Dominant End-Users: Hospitals are projected to account for approximately 48% revenue share in 2026, while diagnostic imaging centers are expected to grow the fastest at 8.5% CAGR through 2033, driven by increasing outpatient imaging demand.

- Dominant Product: Picture archiving & communication system (PACS) is expected to lead with about 32% share in 2026, while imaging analytics & AI is projected to grow the fastest through 2033, supported by demand for automated diagnostic insights.

- Industry Trends: AI-enabled imaging platforms and cloud-based enterprise imaging systems are emerging as key innovation areas, with vendors expanding partnerships and product portfolios to strengthen interoperability and workflow automation.

| Key Insights | Details |

|---|---|

|

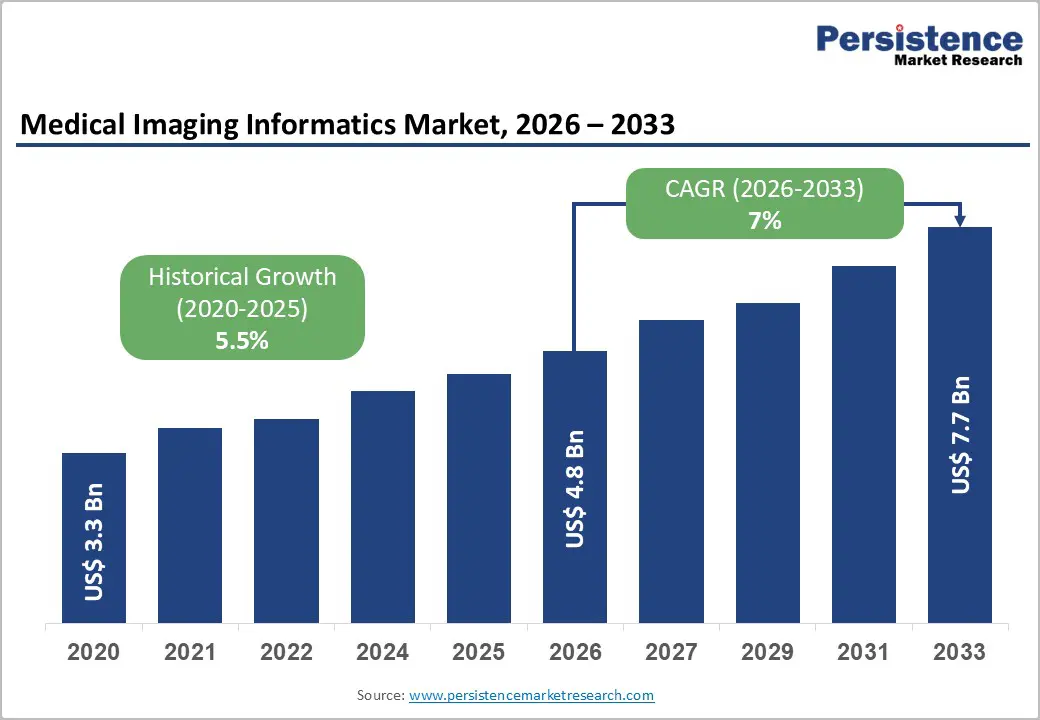

Substation Automation Market Size (2026E) |

US$ 4.8 Bn |

|

Market Value Forecast (2033F) |

US$ 7.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.5% |

DRO Analysis

Rising Diagnostic Imaging Volumes and Expansion of Digital Healthcare Infrastructure

The rapid increase in diagnostic imaging procedures globally is a major factor accelerating demand for medical imaging informatics systems. According to the World Health Organization (WHO) and OECD health statistics, the number of diagnostic imaging procedures such as CT, MRI, and ultrasound examinations continues to rise annually due to population aging and increased prevalence of chronic diseases. For example, the United States performs over 80 million CT scans annually, while MRI utilization has increased steadily across OECD countries. This sustained growth in imaging procedures is creating significant pressure on healthcare providers to manage and store large volumes of medical imaging data efficiently.

As imaging volumes grow, healthcare facilities require robust digital systems to manage, store, and analyze large datasets. PACS and vendor neutral archives (VNA) help streamline image storage and retrieval while enabling seamless data sharing across departments. Hospitals increasingly adopt enterprise imaging platforms to consolidate imaging data from radiology, cardiology, and pathology departments. Industry developments further support this trend. In 2025, several large healthcare networks in North America and Europe expanded enterprise imaging deployments to unify imaging data across multiple facilities, according to coverage by major healthcare technology news outlets such as Healthcare IT News. Such initiatives highlight the increasing importance of scalable imaging data infrastructure to support growing diagnostic workloads across global healthcare systems.

AI Integration and Government Support for Interoperable Digital Health Systems

AI and advanced analytics technologies are transforming the medical imaging informatics landscape. AI-powered tools assist radiologists in image interpretation, automate workflow management, and improve diagnostic accuracy. According to the Radiological Society of North America (RSNA), more than 70% of newly developed radiology software solutions now incorporate AI capabilities to enhance diagnostic support and clinical efficiency. These technologies enable faster image analysis, reduce reporting turnaround time, and help clinicians identify complex abnormalities with greater precision across areas such as oncology, neurology, and cardiology.

Government initiatives aimed at digital healthcare transformation are further strengthening adoption of imaging informatics technologies. In the United States, regulations such as the 21st Century Cures Act and Health Information Technology for Economic and Clinical Health (HITECH) Act encourage healthcare providers to implement interoperable digital health systems. Similarly, the European Health Data Space initiative aims to improve cross-border healthcare data sharing and digital infrastructure across the European Union. In 2025, regulatory agencies including the U.S. Food and Drug Administration (FDA) continued approving new AI-enabled imaging software tools for clinical use, reflecting growing institutional support for AI-assisted diagnostics. These policy and regulatory developments continue to accelerate the adoption of advanced imaging informatics platforms globally.

High Implementation Costs and Complex Infrastructure Requirements

Despite growing adoption, the implementation of medical imaging informatics systems requires substantial capital investment. Deploying PACS, VNA, and enterprise imaging platforms involves hardware procurement, software licensing, system integration, and ongoing maintenance expenses. Hospital IT teams must also invest in secure storage infrastructure, high-performance servers, and network upgrades to manage large imaging datasets effectively. These requirements significantly increase the total cost of ownership for healthcare organizations planning to modernize imaging systems. As a result, many healthcare providers must carefully evaluate financial feasibility before implementing large-scale imaging informatics platforms.

Many small healthcare facilities in developing economies faced financial constraints that limited adoption of advanced imaging informatics solutions. Legacy systems often require costly upgrades to support interoperability with new platforms, further increasing investment requirements. Integration with electronic health records and other clinical systems can also extend project timelines and implementation costs. Financial pressure across hospitals remains significant as operating costs continue to rise and margins remain tight. Healthcare financial reports from major hospital associations indicate that rising labor, technology, and compliance costs are placing additional strain on hospital IT budgets, slowing large-scale digital infrastructure upgrades.

Cybersecurity Risks and Healthcare Data Privacy Concerns

Medical imaging systems store large volumes of sensitive patient data, making them attractive targets for cyberattacks. Healthcare organizations increasingly face data breaches and ransomware incidents affecting clinical IT infrastructure. According to publicly available data from the U.S. Department of Health and Human Services breach portal, tens of millions of individuals were affected by healthcare data breaches in 2025, with hundreds of incidents reported across hospitals and healthcare organizations. Imaging informatics platforms often connect with hospital networks, electronic health records, and cloud environments, expanding the potential attack surface for cyber threats.

Recent cybersecurity incidents further highlight these risks. In 2026, a major cyberattack disrupted the global IT systems of medical technology company Stryker, forcing the organization to investigate the breach and restore internal systems after significant operational disruptions. Similarly, healthcare providers continue to experience ransomware attacks targeting clinical infrastructure and patient databases, underscoring vulnerabilities within connected healthcare systems. As imaging informatics platforms increasingly rely on cloud connectivity and multi-institutional data sharing, healthcare organizations must invest heavily in cybersecurity frameworks and regulatory compliance, which can slow adoption in cost-sensitive healthcare environments.

Expansion of Cloud-Based Imaging Platforms and Tele-Radiology Services

Cloud computing represents one of the most promising opportunities for the medical imaging informatics market. Cloud-based platforms enable healthcare providers to store and access imaging data remotely while reducing the need for expensive on-premise infrastructure. Healthcare organizations are increasingly adopting cloud architectures to support growing imaging volumes and enable scalable data management. Cloud imaging platforms also simplify system upgrades and reduce long-term IT maintenance requirements. As hospitals continue modernizing digital infrastructure, cloud deployment models are becoming an attractive option for improving operational efficiency and managing large imaging datasets.

Cloud imaging platforms enable multi-site collaboration, tele-radiology services, and improved disaster recovery capabilities. These benefits are particularly valuable for large healthcare networks and diagnostic chains operating across multiple locations. Recent industry developments illustrate this trend. For example, in 2026 several hospital networks in Canada began transitioning their imaging infrastructure to cloud-based enterprise imaging platforms, enabling centralized management of millions of annual imaging examinations across multiple hospitals. Such deployments demonstrate how cloud platforms can improve data accessibility, streamline clinical collaboration, and support growing diagnostic imaging workloads across large healthcare systems.

Growing Demand for Remote Diagnostics and Digital Healthcare Expansion in Emerging Markets

Tele-radiology services have expanded significantly following the global digital health transformation accelerated by the COVID-19 pandemic. Remote radiology platforms allow radiologists to interpret imaging studies from different geographic locations, enabling healthcare providers to address radiologist shortages and improve service accessibility. Imaging informatics platforms that support remote access, secure image sharing, and integrated workflow management are becoming critical components of telemedicine infrastructure. As diagnostic imaging volumes increase globally, tele-radiology solutions are helping hospitals maintain 24-hour diagnostic coverage and reduce reporting delays.

Industry developments in 2025–2026 further highlight the strong opportunity created by remote diagnostics and digital health expansion. For example, GE HealthCare announced the acquisition of imaging software provider Intelerad in 2025, aiming to expand cloud-based enterprise imaging and remote diagnostic capabilities across outpatient and hospital networks. Additionally, healthcare systems worldwide continue investing in digital imaging infrastructure and tele-radiology networks to address growing imaging demand and shortages of radiology specialists. These developments are expected to accelerate adoption of advanced imaging informatics platforms capable of supporting distributed healthcare environments and large-scale digital imaging ecosystems.

Category-wise Analysis

Product Type Insights

The PACS segment is expected to account for approximately 32% of the medical imaging informatics market revenue share in 2026. PACS platforms enable healthcare providers to digitally store, retrieve, and distribute medical images across departments, replacing traditional film-based workflows. These systems significantly improve operational efficiency in radiology by enabling instant access to imaging data from modalities such as CT, MRI, ultrasound, and X-ray. Hospitals and large healthcare networks rely on PACS to centralize imaging records and facilitate collaboration among clinicians. The integration of PACS with electronic health records further enhances clinical decision-making. In 2025, Fujifilm expanded its partnership with Hackensack Meridian Health to deploy its Synapse Cardiology PACS platform across an 18-hospital network, reflecting continued investment in enterprise imaging infrastructure.

The imaging analytics & AI segment is projected to be the fastest-growing product category, projected to expand at a CAGR of around 9.1% during 2026–2033. AI-enabled imaging software assists radiologists in detecting abnormalities, prioritizing critical cases, and improving diagnostic accuracy through advanced image analysis. These solutions also automate time-consuming tasks such as image segmentation and reporting, improving workflow efficiency in radiology departments. Healthcare providers increasingly integrate AI analytics to support early disease detection in oncology, neurology, and cardiovascular diagnostics. In 2025, the U.S. Food and Drug Administration (FDA) reported that radiology accounted for the largest share of AI-enabled medical device approvals, highlighting strong technological momentum. Growing clinical adoption of AI tools continues to accelerate innovation in imaging informatics platforms.

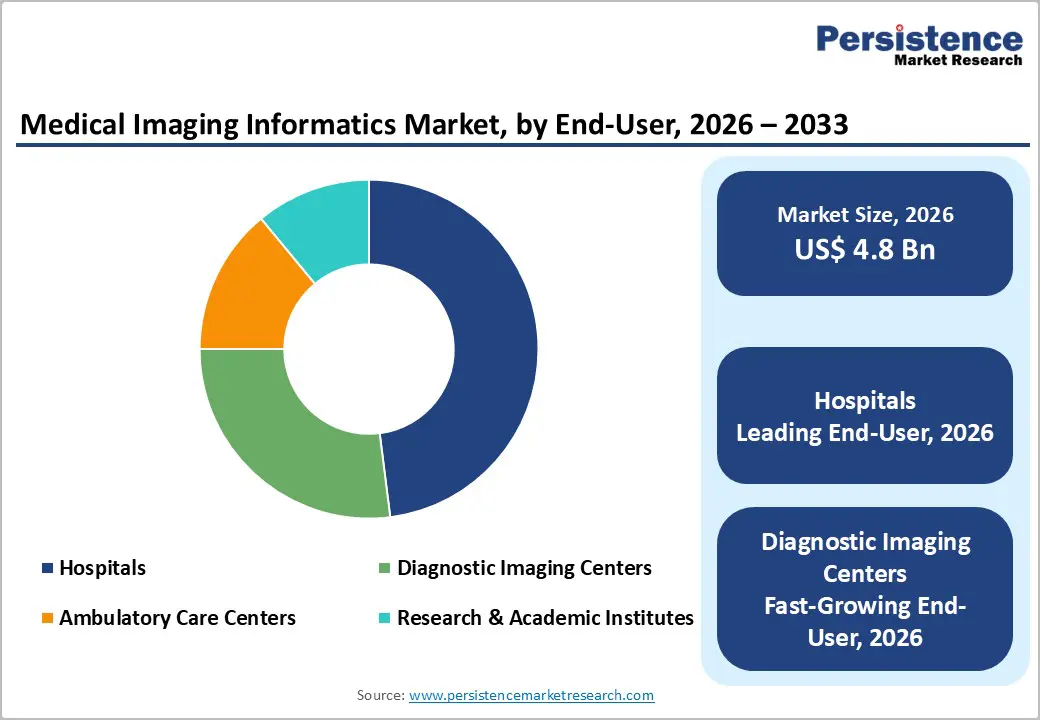

End-User Insights

Hospitals are likely to represent the largest end-user, projected to account for approximately 48% of the revenue share in 2026 due to their high imaging volumes and complex clinical workflows. Large hospitals operate multiple imaging departments such as radiology, cardiology, and oncology that generate substantial diagnostic data. Imaging informatics platforms help hospitals manage this data efficiently while providing clinicians with centralized access to patient imaging records. Enterprise imaging systems also support multidisciplinary collaboration by allowing physicians to review diagnostic images across departments. These platforms improve clinical efficiency, reduce duplication of imaging procedures, and support faster diagnosis. In 2025, several major hospital networks expanded enterprise imaging systems to unify imaging data across multiple facilities, demonstrating growing reliance on integrated imaging infrastructure.

Diagnostic imaging centers are anticipated as the fastest-growing end-user, expected to display a CAGR of approximately 8.5% between 2026 and 2033. These specialized facilities perform high volumes of outpatient imaging procedures, including CT scans, MRIs, mammography, and ultrasound examinations. Rising demand for preventive diagnostics and early disease detection is increasing patient visits to imaging centers worldwide. To manage this demand, providers are adopting PACS platforms, cloud-based imaging systems, and tele-radiology solutions that enable efficient workflow management. Multi-location diagnostic chains rely on centralized imaging informatics platforms for remote reporting and image sharing. In 2025, GE HealthCare announced plans to acquire imaging software company Intelerad, highlighting growing investment in imaging solutions designed for outpatient and diagnostic networks.

Regional Insights

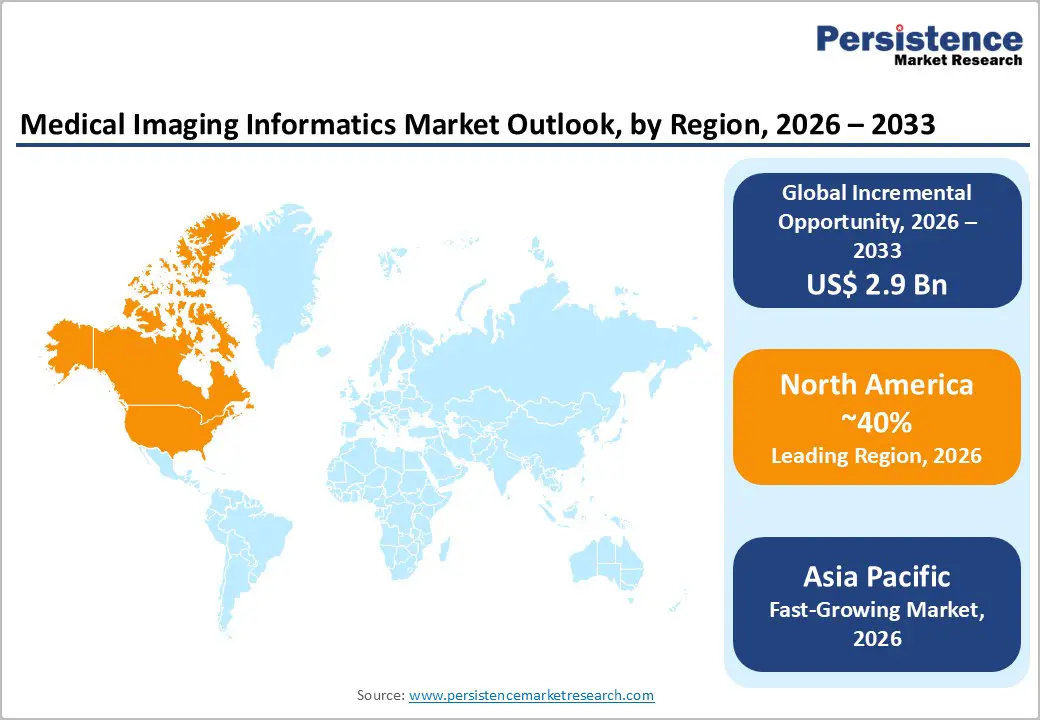

North America Medical Imaging Informatics Market Trends

North America is anticipated to capture around 40% of the medical imaging informatics market share in 2026. The region’s dominance is driven by highly advanced healthcare infrastructure, early adoption of digital health technologies, and the strong presence of leading medical technology companies. Hospitals and diagnostic centers across the United States and Canada increasingly deploy enterprise imaging platforms to manage growing volumes of radiology and diagnostic imaging data. The widespread use of integrated PACS, vendor-neutral archives, and AI-enabled analytics supports faster image interpretation and improved clinical decision-making. In addition, strong investments in healthcare IT modernization and precision medicine initiatives continue to drive demand for advanced imaging informatics platforms across the region.

The region also benefits from an active innovation ecosystem and continuous industry collaboration. Regulatory support for digital health interoperability and increasing adoption of AI-powered imaging analysis tools further accelerate market expansion. For instance, in 2025, Fujifilm partnered with Hackensack Meridian Health to implement its Synapse Cardiology PACS platform across 18 hospitals in the United States, enabling integrated cardiovascular imaging workflows and improved clinical collaboration across the healthcare network. Such large-scale deployments highlight the increasing integration of cloud-based imaging management systems within hospital networks. Furthermore, strong investments in imaging infrastructure and tele-radiology services continue to strengthen regional demand. As a result, North America is expected to maintain steady expansion during the forecast period.

Europe Medical Imaging Informatics Market Trends

Europe represents a mature and steadily expanding market for medical imaging informatics. The regional market benefits from well-established healthcare systems, advanced diagnostic infrastructure, and a strong focus on digital transformation in clinical environments. Germany, the United Kingdom, France, and Italy play a significant role in driving adoption of healthcare IT solutions. Healthcare providers across the region are increasingly deploying enterprise imaging systems that integrate radiology, cardiology, and pathology imaging data into unified platforms. These solutions improve interoperability across hospital departments while enabling clinicians to access patient imaging records more efficiently.

Regional growth is also supported by increasing investment in artificial intelligence and cloud-based imaging technologies. European healthcare organizations are focusing on improving clinical efficiency, managing large imaging datasets, and enhancing diagnostic accuracy through digital imaging platforms. A notable development occurred in 2025 when DeepHealth introduced a new generation of AI-powered radiology informatics and population screening solutions at the European Congress of Radiology (ECR 2025), designed to integrate clinical imaging workflows and improve operational efficiency for healthcare providers. The platform integrates AI-driven detection, advanced visualization, and scalable cloud infrastructure to support modern radiology operations. Such technological advancements demonstrate the region’s growing focus on digital healthcare innovation.

Asia Pacific Medical Imaging Informatics Market Trends

Asia Pacific is projected to be the fastest-growing market for medical imaging informatics through 2033. Rapid healthcare infrastructure development, increasing healthcare spending, and rising demand for diagnostic imaging services are key factors driving regional market growth. Countries such as China, Japan, South Korea, and Australia are actively investing in healthcare modernization and digital hospital initiatives. Hospitals and diagnostic centers across the region are adopting advanced imaging informatics systems to manage growing imaging volumes and improve diagnostic efficiency. In addition, expanding private healthcare networks and rising awareness of early disease detection are further increasing the demand for integrated imaging management solutions.

Government-led healthcare digitalization programs and strong technological development are also accelerating regional adoption of imaging informatics platforms. Healthcare providers are increasingly implementing enterprise imaging systems that enable centralized image storage, remote access, and collaboration among clinicians. For example, in 2025, a fully digital PACS integrated with hospital information systems was deployed at the Institute of Medical Sciences at Banaras Hindu University, enabling real-time access to medical imaging data and supporting digital radiology workflows for a large patient population. Such initiatives demonstrate the growing emphasis on digital healthcare infrastructure across emerging markets in the region. With continued investments in healthcare IT and diagnostic imaging capabilities, the Asia Pacific market is also set to expand at a CAGR of approximately 8.8% during the 2026-2033 forecast period, making it the most dynamic regional market globally.

Competitive Landscape

The global medical imaging informatics market structure is moderately consolidated, with key companies such as GE HealthCare, Siemens Healthineers, Philips Healthcare, and Fujifilm Holdings holding a major share of the market. These players leverage strong hospital partnerships and integrated portfolios including PACS, vendor-neutral archives, and enterprise imaging platforms. Their solutions enable efficient management of large imaging datasets and improved clinical workflows. Continuous investment in AI-driven diagnostics, cloud imaging, and interoperability strengthens their technological leadership. This innovation-driven approach helps them maintain a strong competitive position globally.

Other companies such as Agfa-Gevaert Group, Canon Medical Systems, and Carestream Health focus on specialized imaging informatics solutions and regional markets. These firms emphasize enterprise imaging software, advanced visualization, and workflow optimization tools. While regulatory compliance and system integration create entry barriers, the growth of cloud computing and AI is enabling software-focused firms to enter the market. Strategic collaborations between healthcare providers and technology vendors are increasing. Gradual consolidation is expected as major players expand through acquisitions and partnerships.

Key Industry Developments

- In January 2026, Google launched an updated version of its MedGemma open-source medical AI model, enhancing capabilities for interpreting complex medical data such as 3D CT, MRI, and histopathology scans. The update also introduces improved clinical reasoning, longitudinal image analysis, and a new medical speech-to-text model (MedASR), enabling more advanced, multimodal healthcare AI applications for developers and clinical workflows.

- In December 2025, Royal Philips showcased new AI-driven visualization tools and enterprise imaging solutions at Radiological Society of North America Annual Meeting 2025 and European Congress of Radiology 2026. The innovations include a cloud-based Advanced Visualization Workspace and AI-powered MRI and CT systems designed to improve diagnostic accuracy and radiology workflow efficiency.

- In November 2025, GE HealthCare announced the US$ 2.3 billion acquisition of Intelerad to expand its enterprise imaging and cloud-based informatics capabilities. The move strengthens GE HealthCare’s presence in imaging software and outpatient imaging networks.

Companies Covered in Medical Imaging Informatics Market

- GE HealthCare

- Siemens Healthineers

- Philips Healthcare

- Fujifilm Holdings Corporation

- Agfa-Gevaert Group

- Sectra AB

- Carestream Health

- Merge Healthcare

- Intelerad Medical Systems

- RamSoft

- INFINITT Healthcare

- Novarad Corporation

- Koninklijke Philips NV

Frequently Asked Questions

The global medical imaging informatics market is projected to reach US$ 4.8 billion in 2026.

Increasing diagnostic imaging volumes, growing adoption of digital healthcare systems, and rising integration of AI-based imaging analytics are key market drivers.

The market is poised to witness a CAGR of 7% from 2026 to 2033.

Expansion of cloud-based imaging platforms, enterprise imaging adoption, and AI-powered diagnostic analytics present significant growth opportunities.

Some of the major companies in the market include GE HealthCare, Siemens Healthineers, Philips Healthcare, and Fujifilm Holdings.