- Healthcare Services

- Medical Wigs Market

Medical Wigs Market Size, Share, and Growth Forecast, 2026 - 2033

Medical Wigs Market by Product Type (Full Wigs, Partial Wigs, Lace Wigs, Medical-grade Wigs), Material Type (Human Hair Wigs, Synthetic Fiber Wigs, Blended Wigs), Application (Cancer Patients, Alopecia Patients, Burn Victims, Others), and Regional Analysis for 2026 - 2033

Medical Wigs Market Share and Trends Analysis

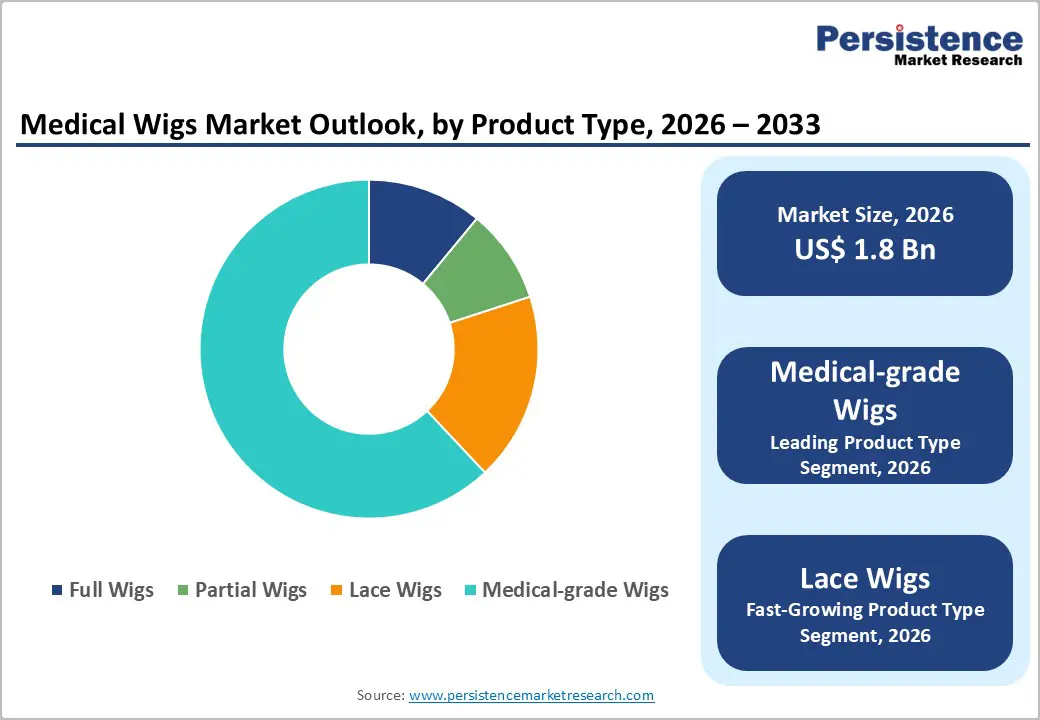

The global medical wigs market size is likely to be valued at US$1.8 billion in 2026 and is estimated to reach US$5.8 billion by 2033, growing at a CAGR of 6.3% during the forecast period 2026−2033, driven by the rising incidence of medically induced hair loss.

Oncology-related alopecia, autoimmune disorders, and burn-related scalp damage contribute to demand. Increasing clinical awareness in dermatology and oncology supports early adoption of prosthetic hair solutions. Expansion of healthcare access improves the availability of certified wig solutions in emerging economies. Insurance reimbursement frameworks enhance affordability and utilization. Technological advancements in medical-grade lace, breathable caps, and lightweight fibers improve comfort and usability.

Key Industry Highlights:

- Leading Product Type: Medical-grade wigs are set to hold around 62% revenue share in 2026, driven by clinical integration across oncology care systems.

- Fastest-Growing Product Type: Lace wigs are projected as the fastest-growing segment, supported by improved breathability and enhanced scalp realism.

- Leading Application: Cancer patients are estimated to hold roughly 55% revenue share in 2026, due to the high incidence of chemotherapy-induced hair loss.

- Fastest-Growing Application: Alopecia patients are forecast to record the fastest growth, driven by increasing autoimmune diagnosis rates and expanding dermatology treatment access.

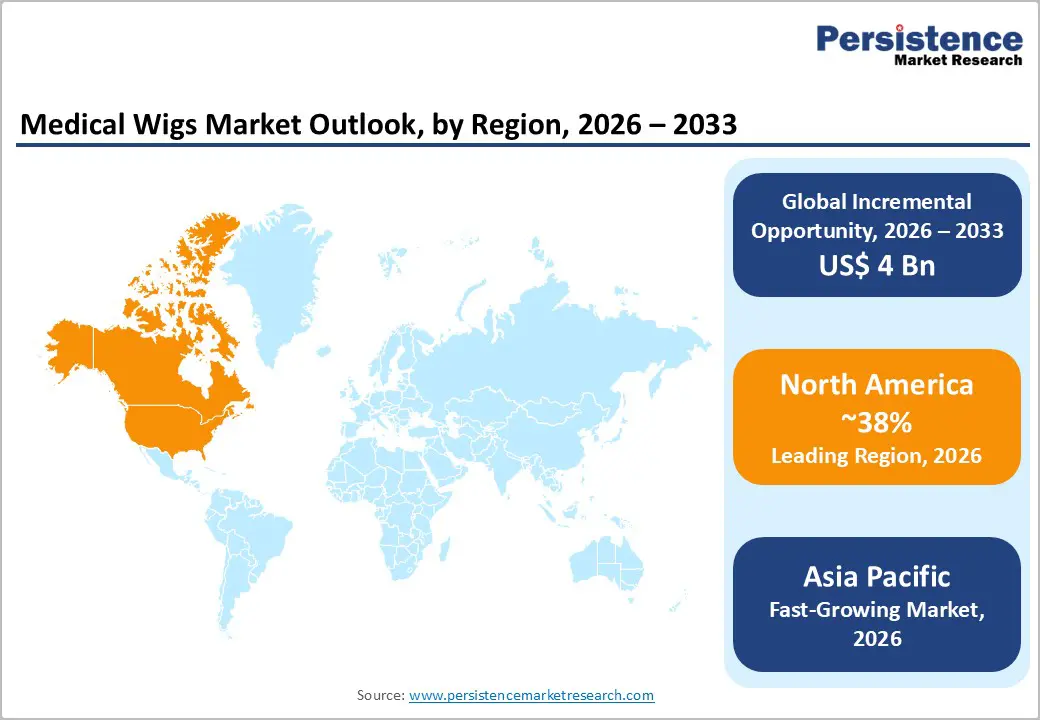

- Regional Leadership: North America is projected to capture roughly 38% of the market share by 2026, while Asia Pacific is forecast to record the fastest growth due to advanced healthcare infrastructure and reimbursement support frameworks.

- Competitive Environment: The market reflects a moderately fragmented structure, with key players focusing on product innovation and hospital integration to strengthen competitive positioning.

DRO Analysis

Driver - Rising Clinical Burden of Hair Loss Associated with Medical Treatments

Demand rises with increasing treatment-related hair loss across oncology and autoimmune care. The National Cancer Institute reported nearly 2 million new cancer cases in the U.S. in 2025, driving chemotherapy usage and visible hair loss, which directly stimulates consistent product demand across clinical support pathways.

Healthcare systems integrate appearance management into patient care protocols to improve treatment adherence and psychological stability. Medical providers recommend wigs as essential support solutions, strengthening procurement channels and institutional demand. Expanding treatment volumes increases recurring need, while standardization of supportive care services enhances product accessibility across hospitals and specialty clinics.

Restraint - High Cost Structure and Limited Reimbursement Coverage

High-cost structures create significant entry barriers for patients requiring medical wigs. Premium human hair units, customization processes, and clinical fittings raise pricing beyond affordability thresholds. Elevated upfront expenses reduce purchasing ability across large patient segments, limiting conversion rates and slowing overall demand expansion within healthcare-driven consumption channels.

Limited reimbursement coverage reduces financial support across healthcare systems, restricting access among middle and low-income groups. Insurance frameworks prioritize essential treatments, leaving supportive care products underfunded. This structure shifts full payment responsibility to patients, weakening adoption momentum, reducing volume scalability, and constraining manufacturer investment in innovation and distribution efficiency.

Opportunity - Expansion of Digital Customization and Tele-trichology Platforms

Digital customization tools enable precise fitting through 3D scalp mapping and virtual trials. This reduces product returns and inventory inefficiencies. Clinics and manufacturers gain operational cost control. In 2025, the Centers for Disease Control and Prevention reported that 37% of adults used telehealth services, indicating strong digital engagement in healthcare delivery.

Tele-trichology platforms expand patient access across remote and underserved regions. Virtual consultations support early intervention and faster product selection. This increases conversion rates and shortens sales cycles. Digital integration improves data collection on patient preferences, enabling targeted product development and scalable distribution strategies across healthcare networks.

Category-wise Analysis

Product Type Insights

Medical-grade wigs are expected to capture around 62% of the medical wigs market share in 2026, reflecting growing clinical preference for certified prosthetic hair solutions designed specifically for patients undergoing medical treatments. Adoption rises as hospitals standardize the procurement of supportive care, while organizations such as the World Health Organization (WHO) promote safe rehabilitation tools, ensuring consistent use across oncology treatment pathways.

Lace wigs are expected to be the fastest-growing segment during the 2026-2033 forecast period, propelled by improved scalp realism, lightweight construction, and enhanced breathability suitable for prolonged wear during medical recovery. Growth accelerates as clinics recommend lace variants for chemotherapy patients, while digital customization platforms enable precise fitting, supporting higher adoption across diverse patient demographics globally.

Application Insights

Cancer patients are likely to be the leading segment with a projected 55% of the medical wigs market share in 2026, due to the high prevalence of chemotherapy-induced hair loss and structured integration of supportive care in oncology treatment pathways. Hospitals standardize referrals, while organizations such as the National Cancer Institute support patient care frameworks, ensuring steady demand.

Alopecia patients are anticipated to be the fastest-growing segment from 2026 to 2033, fueled by rising diagnosis rates of autoimmune-related hair loss conditions and increasing awareness of dermatological treatment options. Growth strengthens as dermatology clinics expand referrals, while organizations such as the National Alopecia Areata Foundation promote awareness, improving adoption across diagnosed populations.

Regional Insights

North America Medical Wigs Market Trends

North America is expected to lead with an estimated 38% of the medical wigs market share in 2026, supported by advanced oncology infrastructure and structured supportive care integration. The Centers for Medicare & Medicaid Services reported healthcare spending reaching US$4.9 trillion in 2025, reflecting strong federal and private funding capacity for supportive care services. Companies such as Aderans Co., Ltd. and HairUWear Inc. maintain extensive clinical distribution networks.

Federal healthcare programs strengthen reimbursement pathways for medically certified wigs across oncology treatment settings. Institutional procurement systems prioritize compliant products, ensuring standardized supply across hospitals. Digital scalp mapping and teleconsultation tools improve fitting precision and service efficiency. Strong clinician awareness supports consistent prescription rates across integrated oncology and dermatology care frameworks.

Europe Medical Wigs Market Trends

Europe maintains a stable position supported by structured public healthcare systems and standardized clinical pathways for oncology and dermatology care. The European Commission promotes cross-border healthcare access, improving patient mobility for specialized treatments. Countries such as Germany and France show strong hospital procurement frameworks, ensuring consistent availability of certified prosthetic hair solutions.

Reimbursement alignment within national health systems improves affordability for patients undergoing long-term treatment. Companies such as Ellen Wille focus on premium medical-grade products, supporting quality standards. Aging population trends increase the incidence of hair loss conditions, strengthening demand. Digital consultation services expand access, improving patient engagement and customization efficiency across healthcare networks.

Asia Pacific Medical Wigs Market Trends

Asia Pacific is forecast to be the fastest-growing market for medical wigs, stimulated by the rapid expansion of healthcare infrastructure and rising integration of aesthetic rehabilitation within oncology care pathways. China records strong hospital expansion supported by the National Health Commission of China, improving treatment access. India benefits from schemes led by the Ministry of Health and Family Welfare, while companies such as Artnature Inc. expand regional distribution.

Digital health platforms and e-commerce channels improve direct-to-patient access, reducing dependence on clinical visits. Japan and South Korea lead innovation through companies such as Aderans Co., Ltd., enhancing product quality and comfort. Government-backed healthcare spending growth and outpatient care expansion improve early diagnosis and treatment access, strengthening demand across diverse patient populations.

Competitive Landscape

The global medical wigs market is structured with moderate fragmentation, where specialized manufacturers compete through clinically validated products and integrated healthcare distribution. Premium segment control remains concentrated among key players due to established hospital partnerships and certified supply chains. The key players are Aderan, Hairdreams Haarhandels GmbH, HairUWear, Raquel Welch Wigs, and Follea.

Competitive intensity is defined by advanced material engineering, precision customization, and compliance with dermatological safety standards. Regulatory certification and sourcing of high-quality hair fibers increase operational complexity. Market participants strengthen positioning through digital scalp mapping, direct clinical integration, and multi-channel distribution strategies, improving procurement efficiency and patient-specific product delivery across healthcare systems.

Key Industry Developments:

- In October 2025, Fortis Hospital Mulund expanded oncology infrastructure with the launch of advanced oncology services, strengthening supportive cancer care ecosystems that indirectly enhance access to adjunct solutions such as medical wigs for patients undergoing treatment.

- In February 2025, Aderans Co., Ltd. launched a new ready-made medical wig for men under the Rafra brand, featuring faster styling and delivery, multiple color options, and improved affordability to support patient comfort and accessibility in clinical care settings.

Companies Covered in Medical Wigs Market

- Aderans Co., Ltd.

- Hairdreams Haarhandels GmbH

- HairUWear Inc.

- Raquel Welch Wigs

- Follea

- Noriko Wigs (Amekor Industries)

- New Look Hair

- Louis Ferre

- Vivi Wigs

- Rebecca Fashion Wig Co.

- Lordhair

- UniWigs

Frequently Asked Questions

The medical wigs market is projected to reach US$1.8 billion in 2026.

Rising incidence of chemotherapy-induced and medical hair loss conditions drives demand for clinically approved wig solutions.

The medical wigs market is poised to witness a CAGR of 6.3% from 2026 to 2033.

Expansion of digital customization platforms and tele-trichology services creates scalable access and personalized solutions for patients in the medical wigs market.

Some of the key market players include Aderans, Hairdreams Haarhandels GmbH, HairUWear, Raquel Welch Wigs, and Follea.