- Medical Devices

- Medical Oxygen Cylinders Market

Medical Oxygen Cylinders Market Size, Trends, Share, Growth, and Regional Forecast, 2025 to 2032

Medical Oxygen Cylinders Market by Product (Fixed Medical Oxygen Cylinders and Portable Medical Oxygen Cylinders), by End-user (Hospitals, Specialty Clinics, Ambulatory Surgery Centers, and Home Care Settings and Others), and Regional Analysis from 2025 - 2032

Medical Oxygen Cylinders Market Share and Trends Analysis

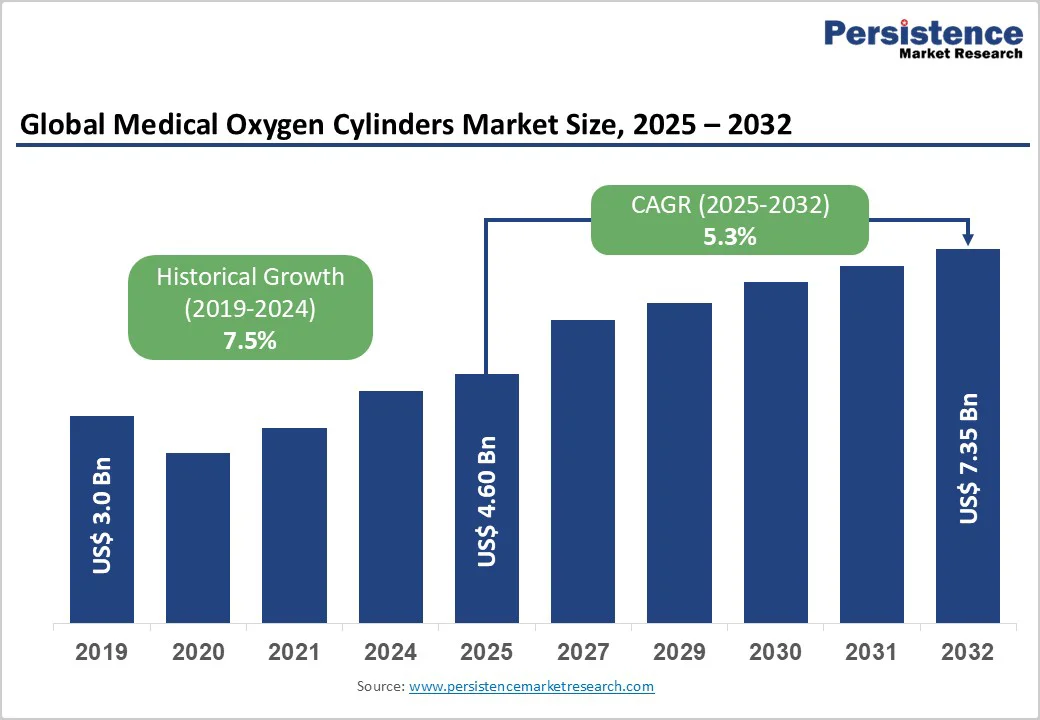

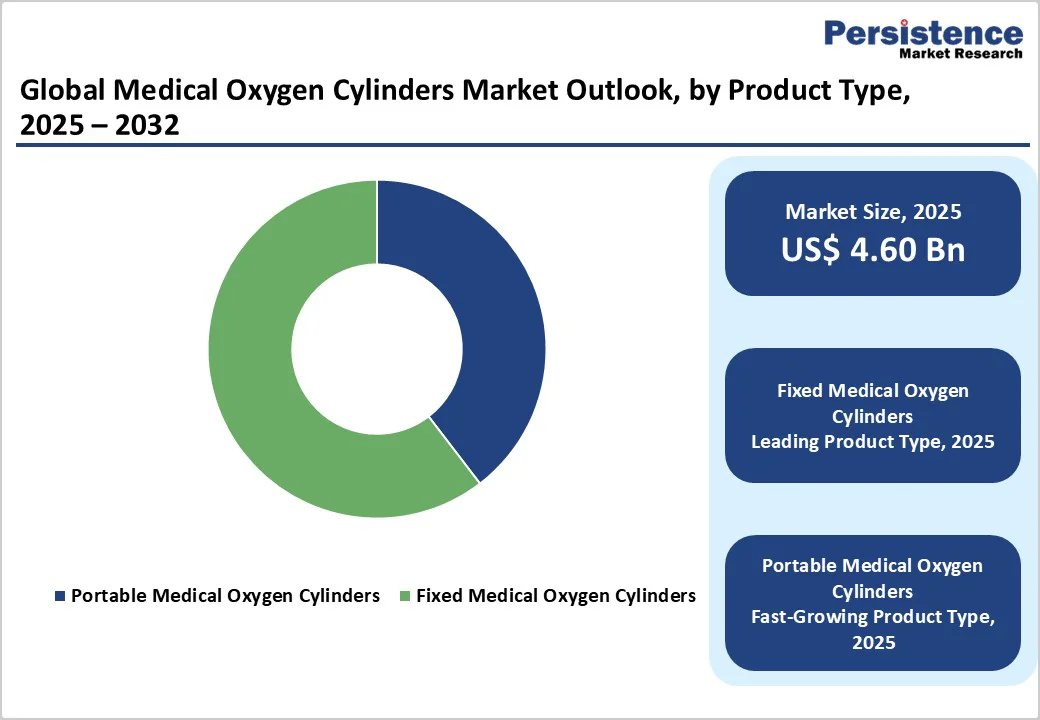

The global medical oxygen cylinders market size is valued at US$4.60 billion in 2025 and is projected to reach US$7.35 billion by 2032, growing at a CAGR of 5.4% from 2025 to 2032.

Global demand for medical oxygen cylinders is rising as the incidence of respiratory disorders, including chronic obstructive pulmonary disease (COPD), asthma, pneumonia, acute respiratory distress syndrome (ARDS), and post-COVID complications, continues to increase worldwide. Growing geriatric populations, higher hospitalization rates for respiratory distress, and expanding use of oxygen therapy in emergency and critical-care stabilization are driving broader clinical adoption.

Key Industry Highlights

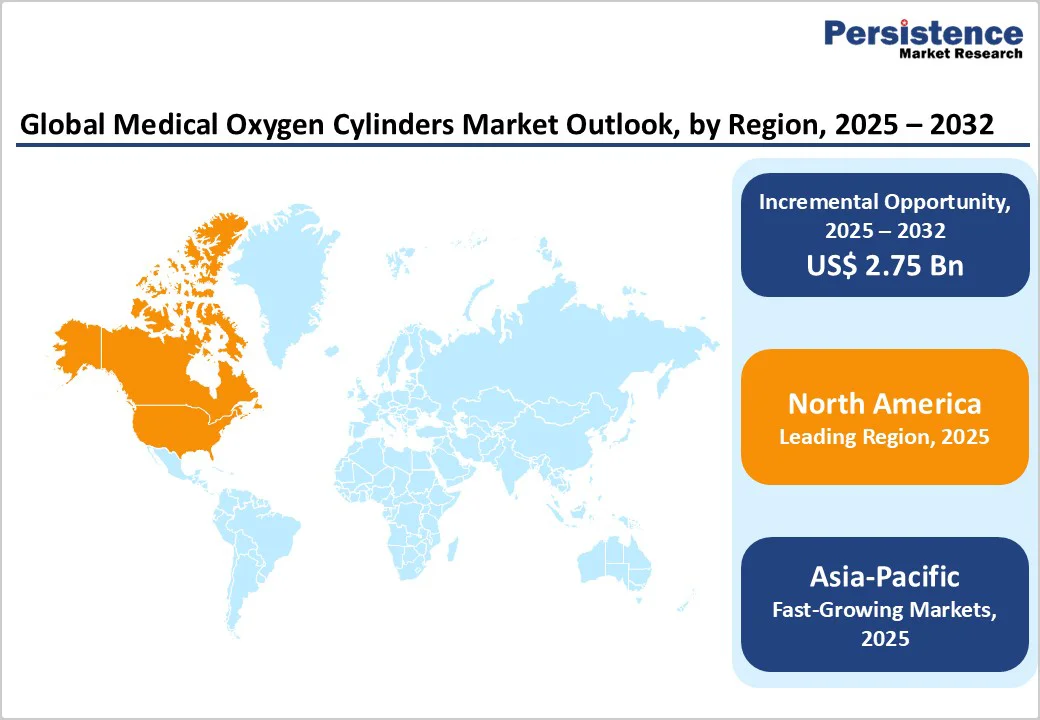

- Leading Region: North America dominates the global medical oxygen cylinders market, accounting for 40.2% of the market value, driven by the high prevalence of chronic respiratory diseases, extensive ICU and emergency care infrastructure, widespread adoption of home-based oxygen therapy, and advanced hospital systems integrating centralized oxygen pipelines and digital monitoring solutions.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, supported by the rising incidence of respiratory disorders, the rapid expansion of tertiary-care hospitals, increasing healthcare expenditure, and the growing adoption of portable oxygen cylinders for home-based and emergency respiratory care.

- Leading Product Type Segment: Fixed medical oxygen cylinders lead the market due to their high storage capacity, stable oxygen delivery, reliability during surgeries and ICU care, and strong hospital preference for uninterrupted supply in critical-care and emergency settings.

- Fastest-Growing Product Type Segment: Portable medical oxygen cylinders are the fastest-growing segment, supported by ease of mobility, lightweight composite designs, integration with digital monitoring systems, and increasing use in home-care therapy, ambulatory services, and emergency transport.

- Leading End-user Segment: Non-home care settings dominate the market, as hospitals, surgical centers, and emergency units require high-capacity oxygen cylinders to manage perioperative care, trauma cases, ventilator support, and critical respiratory interventions.

- Fastest-Growing End-user Segment: Home care settings represent the fastest-growing segment, driven by rising adoption of long-term oxygen therapy, increased prevalence of chronic respiratory diseases among aging populations, and demand for portable oxygen solutions that enable safe and convenient at-home management.

| Key Insights | Details |

|---|---|

|

Medical Oxygen Cylinders Market Size (2025E) |

US$4.60 Bn |

|

Market Value Forecast (2032F) |

US$7.35 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.3% |

|

Historical Market Growth (CAGR 2019 to 2024) |

7.5% |

Market Dynamics

Driver - Rising Prevalence of Respiratory Disorders Globally and Growing Need for Emergency Preparedness & Pandemic Readiness

Growing cases of chronic obstructive pulmonary disease (COPD), asthma, pneumonia, acute respiratory distress syndrome (ARDS), and post-COVID respiratory complications have significantly increased the demand for high-purity medical oxygen. Hospitals, emergency units, and home-care settings are adopting larger inventories of both portable and stationary cylinders to ensure an uninterrupted supply for oxygen-dependent patients. The rapid surge in geriatric populations and high smoking prevalence further accelerates long-term demand for medical oxygen delivery solutions. For instance, according to the American Lung Association (ALA) in 2022, about 44.2 million Americans had been diagnosed with asthma, highlighting the expanding patient base and sustained need for medical oxygen cylinders.

Governments worldwide are building long-term stockpiles of medical oxygen cylinders to strengthen disaster preparedness and pandemic readiness. Initiatives to establish oxygen banks in district hospitals, deploy mobile medical units, and establish rural health centers represent a major procurement opportunity. The focus on maintaining strategic medical oxygen reserves ensures recurring, large-volume orders from public health systems, supporting consistent demand across national emergency response programs and healthcare infrastructure expansion efforts.

Restraints - High Refill Costs and Growing Shift Toward On-Site Oxygen Generation

High-pressure medical oxygen cylinders are costly to transport and refill, particularly in rural, mountainous, and hard-to-access regions. The need for specialized transport vehicles, dedicated logistics partners, and frequent refill cycles substantially increases operational expenses for healthcare facilities. Refill delays or shortages during high-demand periods can disrupt patient care and discourage hospitals from relying solely on cylinder-based oxygen delivery, making these challenges especially prominent in low- and middle-income countries.

Moreover, healthcare systems are increasingly transitioning to on-site oxygen generation via pressure swing adsorption (PSA) oxygen plants and oxygen concentrators, which provide a more continuous and cost-efficient supply than refilled cylinders. Large tertiary hospitals, surgical centers, and newly developed healthcare facilities are investing in centralized oxygen systems to improve reliability and reduce dependency on high-capacity cylinders. Government-backed incentives and subsidies for PSA plant installations further boost this shift, creating a competitive restraint for traditional cylinder manufacturers.

Opportunity - Expansion of Home Healthcare Ecosystems and Advancements in Smart Cylinder Technologies

Urbanization, rising healthcare spending, and increased awareness of chronic respiratory diseases are accelerating the adoption of home-based oxygen therapy across Asia-Pacific, Latin America, and the Middle East. Demand for portable oxygen cylinders continues to grow as patients seek convenient, at-home respiratory support, supported by online medical equipment platforms and home-delivery refill services. This shift toward consumer-driven oxygen therapy is creating substantial growth opportunities for regional distributors and global manufacturers.

Furthermore, rapid advancements in cylinder valve design and digital monitoring technologies are transforming purchasing preferences across healthcare systems. Smart valves, digital pressure indicators, Internet of Things (IoT)-enabled tracking tools, and integrated flow-control mechanisms are helping hospitals minimize leakage risk, reduce operational errors, and maintain real-time visibility into oxygen levels. Manufacturers that introduce next-generation, safety-enhanced, and digitally monitored cylinders can strengthen product differentiation and capture premium demand from technologically advanced medical institutions.

Category-wise Analysis

By Product, Fixed Medical Oxygen Cylinders Dominate Globally Due to Their High Storage Capacity and Essential Role in Critical-Care Infrastructure

The fixed medical oxygen cylinders segment is projected to dominate the global medical oxygen cylinders market in 2025, accounting for 60.4% of revenue. The segment’s strong performance is primarily driven by the hospitals, surgical centers, and intensive care units (ICUs) relying heavily on high-capacity, stationary cylinders to maintain a stable and uninterrupted oxygen supply. Their ability to deliver consistent high-flow oxygen during surgeries, trauma care, ventilation support, and emergency stabilization makes them indispensable in clinical environments. In addition, fixed cylinders integrate seamlessly with centralized medical gas pipeline systems (MGPS), ensuring reliable oxygen availability during peak patient load, mass-casualty situations, and prolonged respiratory emergencies.

By End-user, Hospitals Lead the Market Globally Due to Advanced Infrastructure and Higher Adoption of Implantable PNS Procedures

The hospitals segment is projected to dominate the global medical oxygen cylinders market in 2025, accounting for 58.8% of revenue. This is due to the consistently high demand for medical oxygen across emergency departments, ICUs, operating rooms, and general wards, where continuous oxygen therapy is essential for critical and respiratory care. The high volume of inpatient and outpatient surgical procedures, the crucial need for continuous oxygen support in perioperative and emergency care, and the preference of hospitals and surgical centers for high-capacity, refillable cylinders to ensure uninterrupted supply further drive demand for medical oxygen cylinders in Hospitals.

Hospitals also maintain large inventories of fixed and portable cylinders to support surgical procedures, trauma management, and ventilator-dependent patients. Additionally, rising hospitalization rates for COPD, pneumonia, cardiac events, and postoperative complications further strengthen the segment’s dominance. Growing investments in oxygen infrastructure, including automated refilling stations and advanced cylinder-tracking systems, are further driving hospital procurement.

Region-wise Insights

North America Medical Oxygen Cylinders Market Analysis

The North America market is expected to dominate globally with a value share of 40.2% in 2025, with the U.S. leading the region due to its well-established healthcare infrastructure, high prevalence of chronic respiratory diseases such as chronic obstructive pulmonary disease (COPD), asthma, and pneumonia, and the widespread adoption of home-based oxygen therapy. Additionally, rising ICU admissions, trauma cases, and dependence on advanced respiratory management systems further strengthen the segment’s market leadership.

The expansion of multispecialty surgical centers and improved emergency transport infrastructure has further increased oxygen procurement. Growing investments in critical-care upgrades across public and private hospitals are also accelerating demand in this segment. The presence of advanced hospitals, critical-care units, and ambulatory surgical centers ensures a consistent demand for both fixed and portable medical oxygen cylinders. Furthermore, government initiatives and reimbursement policies promoting long-term oxygen therapy, rising geriatric populations, and increased awareness of respiratory health are driving higher consumption. The integration of smart oxygen delivery systems, IoT-enabled monitoring, and portable composite cylinders in emergency services and home healthcare further strengthens the market.

Europe Medical Oxygen Cylinders Market Trends

Europe is expected to achieve steady growth due to increasing investments in critical-care infrastructure and the expansion of surgical and emergency facilities across key countries such as Germany, France, and the UK. The region’s focus on hospital-acquired pneumonia prevention, enhanced ICU capabilities, and integration of centralized oxygen distribution systems is driving demand for high-capacity medical oxygen cylinders. Additionally, growing industrial collaborations, rising production of high-purity oxygen, and increasing adoption of portable cylinders in outpatient and home rehabilitation programs are supporting market growth in Europe. Favorable government reimbursement policies for long-term oxygen therapy and rising awareness about respiratory health among the aging population are further fueling demand. Moreover, advancements in digital monitoring and smart valve technologies are enhancing patient safety and operational efficiency, boosting the adoption of medical oxygen cylinders across hospitals and home-care settings.

Asia Pacific Medical Oxygen Cylinders Market Trends

The Asia Pacific market is expected to register a relatively higher CAGR of around 7.3% between 2025 and 2032, driven by rapid urbanization, rising healthcare expenditure, and growing prevalence of respiratory disorders such as chronic obstructive pulmonary disease (COPD), asthma, and pneumonia. Increasing government initiatives to improve rural healthcare infrastructure, the expansion of tertiary-care hospitals, and rising adoption of home-based oxygen therapy are further boosting demand.

Additionally, the surge in medical tourism, the expansion of emergency medical services, and rising awareness of critical-care respiratory management are driving strong growth across countries such as India, China, and Japan. The increasing availability of portable and composite oxygen cylinders, along with technological advancements in smart valves and digital monitoring systems, is further enhancing adoption. Moreover, collaborations between local manufacturers and global medical gas suppliers are facilitating broader distribution and access, thereby strengthening market growth in the region.

Competitive Landscape

The global medical oxygen cylinders market is highly competitive, with major players such as Drive Devilbiss International, Koninklijke Philips N.V., Nidek Medical India, CAIRE Inc., and Linde plc dominating through broad product portfolios, robust distribution networks, and long-standing expertise in medical gas solutions. These companies offer a wide range of fixed and portable oxygen cylinders, integrated oxygen delivery systems, pressure regulators, and digital monitoring devices widely used in hospitals, emergency care, surgical centers, and home-based respiratory therapy.

Manufacturers are increasingly focusing on lightweight, corrosion-resistant, and portable cylinder designs, alongside innovations in smart valves, integrated flow meters, IoT-enabled monitoring, and enhanced safety features. Strategic initiatives such as mergers and acquisitions, expansion of manufacturing capacities, partnerships with healthcare providers, and development of advanced portable oxygen generators are further strengthening competitive positioning across global markets.

Key Industry Developments:

- In February 2025, Nikkiso Co., Ltd. was selected to supply medical oxygen production plants under a regional health initiative led by Unitaid, aimed at improving access to medical oxygen in low- and middle-income countries. Three air separation units will be installed in Kenya and Tanzania to expand local oxygen production. The project, supported by a $7.3 million contribution from the Government of Japan, seeks to boost the availability of medical oxygen cylinders for surgery, emergency care, and treatment of severe respiratory conditions, addressing critical shortages across East Africa.

- In December 2023, the Ministry of Health of the Lao People’s Democratic Republic (Lao PDR), in collaboration with the World Health Organization (WHO), inaugurated the country’s third and fourth provincial medical oxygen plants at Luang Prabang and Oudomxay hospitals. Supported by WHO, these facilities will enable the provinces to produce medical oxygen locally for the first time, improving the availability of oxygen cylinders for critical care and strengthening the region’s capacity to deliver timely oxygen therapy in hospitals and emergency settings.

Region-wise Analysis

By Product

- Portable Medical Oxygen Cylinders

- Fixed Medical Oxygen Cylinders

By End-user

- Hospitals

- Specialty Clinics

- Ambulatory Surgery Centers

- Home Care Settings

- Others

By Region

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- Middle East and Africa

Companies Covered in Medical Oxygen Cylinders Market

- Drive Devilbiss International

- Koninklijke Philips N.V.

- Nidek Medical India

- CAIRE Inc

- Linde plc

- Air Liquide

- AMS Composite Cylinders

- Pune Air Products

- EKC (Everest Kanto Cylinder Limited)

- Rama Cylinders

- Lizer Cylinders Limited

- Euro Global Gas Cylinders LLP

- Others

Frequently Asked Questions

The global medical oxygen cylinders market is projected to be valued at US$ 4.60 Bn in 2025.

Rising prevalence of respiratory disorders, increasing hospitalizations, and growing adoption of home-based oxygen therapy. Additionally, expanding critical-care infrastructure and advancements in portable and smart oxygen delivery systems are driving the global medical oxygen cylinders market.

The global medical oxygen cylinders market is poised to witness a CAGR of 5.3% between 2025 and 2032.

Growing demand for portable and composite cylinders for home healthcare and emergency use are creating strong growth opportunities in the market.

Devilbiss International, Koninklijke Philips N.V., Nidek Medical India, CAIRE Inc., and Linde plc are some key players in the medical oxygen cylinders market.