Liquid Silicone Rubber Market

Industry: Chemicals and Materials

Published Date: November-2024

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 188

Report ID: PMRREP34915

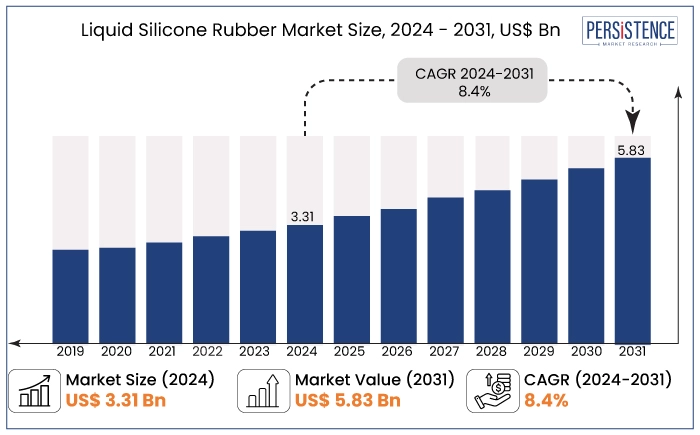

The liquid silicone rubber market is projected to witness a CAGR of 8.4% during the forecast period from 2024 to 2031. It is anticipated to increase from US$ 3.31 Bn recorded in 2024 to US$ 5.83 Bn by 2031.

Rising demand from healthcare and automotive industry is boosting the demand for silicone rubber. The ability to function efficiently at higher temperature, biocompatibility, having high chemical and electrical resistance, with transparency is attracting the manufacturers toward this rubber. These properties are creating an opportunity for electronic gadgets manufacturers to use the rubber.

Worldwide IT spending is expected to total $5.06 trillion in 2024, an increase of 8% from 2023. The spending of devices is around 14% of the total IT spending and is growing with the rate of 3.6%. The increasing use of devices, consumers are looking forward to more efficient, soft, and eco-friendly materials which leads to utilization of silicone rubber in manufacturing of the devices.

Key Highlights of the Market

|

Market Attributes |

Key Insights |

|

Liquid Silicone Rubber Market Size (2024E) |

US$ 3.31 Bn |

|

Projected Market Value (2031F) |

US$ 5.83 Bn |

|

Global Market Growth Rate (CAGR 2024 to 2031) |

8.4% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

7.7% |

In North America, the United States is anticipated to record a considerable CAGR of 8.4% through 2031. This expansion is largely driven by the automotive sector, where the increasing adoption of advanced materials is enhancing product performance and durability.

The demand for silicone rubber is being further amplified by the production trends in the automotive industry. According to the International Organization of Motor Vehicle Manufacturers, North America produced approximately 16,166,628 motor vehicles in 2023, reflecting a steady growth of around 10% over the past two years.

The upward trajectory in vehicle production underscores the automotive sector's reliance on innovative materials like liquid silicone rubber, which offers superior properties such as heat resistance, flexibility, and longevity.

As the automotive industry continues to evolve, particularly with the rise of electric vehicles and advanced manufacturing techniques, the need for high-performance materials like silicone rubber is expected to grow, positioning the market favorably in the coming years. This not only highlights the significant role of LSR in automotive applications but also indicates a broader shift toward materials that enhance the functionality and sustainability of vehicle components.

|

Category |

CAGR through 2031 |

|

Grade - Industrial Grade |

8.6% |

The industrial grade segment of the rubber market is expected to lead in the foreseeable future, with an anticipated CAGR of 8.6%. This growth is primarily driven by unprecedented demand from the automotive and healthcare sectors, which are increasingly relying on industrial-grade rubber for various applications.

The automotive industry, in particular, is experiencing a transformative phase. According to the World Trade Organization, the United States surpassed Japan in 2022 to become the second-largest automotive exporter globally. This shift underscores the robust growth potential within the U.S. automotive market.

China has also demonstrated significant export growth, with its automotive product exports increasing by 30% among the top ten exporters. China reported a 7% year-on-year increase in November 2023 in the value of its automotive product exports, further highlighting the competitive landscape in the sector.

The burgeoning demand for industrial-grade rubber in these industries is attributable to its excellent performance characteristics, including durability, heat resistance, and versatility. As manufacturers seek to enhance product quality and efficiency, the reliance on high-performance materials like industrial-grade rubber is expected to continue rising, driving market growth in the coming years.

|

Category |

CAGR through 2031 |

|

End-use Industry - Automotive |

8.6% |

The automotive end-use industry is projected to experience growth at a CAGR of 8.6% from 2024 to 2031. This growth is significantly influenced by the rising global market for electric vehicles (EVs), which has driven an increased demand for materials that exhibit high thermal resistance and excellent electrical insulation properties, such as silicone rubber.

The transition toward electric vehicles is particularly notable in Europe, where the European Hydrogen Observatory reports that EV registrations surged by approximately 450% from 2018 to 2022. This remarkable increase highlights the accelerating shift in consumer preferences and regulatory support for sustainable transportation solutions.

As automakers focus on enhancing the performance and safety of electric vehicles, the need for advanced materials that can withstand the unique demands of EV applications becomes critical. Liquid silicone rubber, with its superior thermal stability and electrical insulating capabilities, is increasingly being utilized in components such as battery seals, gaskets, and connectors.

The automotive industry's commitment to innovation and sustainability, particularly through the adoption of electric vehicles, is driving the demand for high-performance materials. As a result, the automotive sector is positioned for continued growth, reinforcing the importance of materials like liquid silicone rubber in meeting the evolving needs of modern transportation.

Liquid silicone rubber (LSR) has emerged as a significant player in various industries, particularly due to its unique properties that cater to a wide range of applications. The market introduction of LSR has been characterized by its high biocompatibility, making it suitable for parts that come into direct contact with humans. This includes critical applications such as organ components and prosthetics, where material safety and compatibility are paramount.

One of the key trends driving the adoption of LSR is its exceptional durability, which ensures long-term stability and chemical resistance. This resilience makes LSR an ideal choice for demanding environments, further expanding its utility across sectors such as healthcare, automotive, and consumer goods. Temperature resistance is another important attribute of LSR. It can maintain its high-performance mechanical properties across a wide temperature range, from -60 °C to +250 °C. This versatility allows manufacturers to utilize LSR in applications exposed to extreme conditions, enhancing its appeal in various industries.

The global liquid silicone rubber market recorded a decent CAGR of 7.7% in the historical period from 2019 to 2023. Key chemical companies invested a lot in liquid silicone rubber owing to its wide usage in several applications, including medical, automotive, electronics, and others.

In particular, the medical applications of LSR are anticipated to witness substantial growth in the coming years. The demand for biocompatible materials in healthcare continues to rise, as advancements in medical technology and an aging population increase the need for high-quality, durable components such as prosthetics, seals, and tubing.

In December 2022, Dow announced the launch of a new product named SILASTIC SA 994X Liquid Silicone Rubber series. The goal of the product launch was to maintain the emphasis on safer and more sustainable technologies. The product consists primerless, self-adhesive LSRs that are self-lubricating. They have a one-to-one mix ratio and are designed for two-component injection molding with thermoplastic substrates.

The LSR market is poised for continued expansion, driven by technological advancements and increasing demand across various industries. As manufacturers prioritize sustainability and safety, the development of innovative LSR formulations will play a crucial role in meeting market needs. The market is estimated to record a CAGR of 8.4% during the forecast period between 2024 and 2031.

Rising Demand from Healthcare Industry

The market is experiencing significant growth, largely driven by the rapid expansion of the healthcare sector, particularly in emerging markets like India. The growth in the healthcare sector is creating a massive demand for LSR among medical manufacturers. This demand is primarily attributed to LSR's exceptional properties, including its ability to perform efficiently at extreme temperatures and its inherent chemical resistance.

LSR's compliance with stringent regulatory standards, including FDA, ISO, and Class VI medical-compliant grades, enhances its reliability and safety for use in healthcare settings. This compliance is crucial as it reassures manufacturers and healthcare providers of the material's suitability for critical applications. These characteristics make LSR an ideal material for various medical applications.

Growing Demand from Automotive Industry

The demand for LSR in the automotive industry is on the rise, driven by several key factors. A significant driver of demand within the automotive sector is the growing emphasis on electric vehicles (EVs). As concerns about climate change and the need to reduce greenhouse gas emissions gain prominence, the shift toward EVs is accelerating.

Governments worldwide are promoting electric vehicle adoption through various incentives and subsidies, further increasing demand for EV components.

LSR is particularly well-suited for the fabrication of EV components due to its superior qualities, including high-temperature resistance, electrical insulation, and chemical resistance. These properties make LSR an ideal material for critical applications such as battery packs, charging cables, and connectors. For example,

Expensive Production Cost can Hamper Demand

One of the primary restraints affecting the LSR market is the high production cost associated with its manufacturing. The process of producing LSR is relatively time-consuming, which can create challenges during periods of extreme demand.

The extended manufacturing timelines can lead to potential shortages in supply, particularly when market demand surges rapidly. This situation can frustrate manufacturers and end-users alike, as the inability to meet demand can result in missed opportunities and lost revenue.

The costs associated with the raw materials and specialized equipment required for LSR production contribute to the overall expense, making it less accessible for some manufacturers, especially smaller enterprises.

Liquid silicone rubber prices can limit the adoption of LSR in price-sensitive markets, where alternative materials with lower costs may be preferred despite their inferior performance characteristics. As a result, while LSR offers numerous advantages in terms of performance and versatility, the expense associated with its production poses a significant challenge that could hinder its broad market penetration and growth.

High Demand for Electronic Gadgets Bolstering the LSR Market

The increasing demand for electronic gadgets, particularly driven by the growth of the Internet of Things (IoT), presents a significant opportunity for the liquid silicone rubber market. According to the Mobile Economy 2020 report released by the GSM Association, the number of devices connecting to the Internet specifically IoT connections is projected to reach 25 billion by 2025, up from 12 billion in 2019. This remarkable growth highlights the expanding ecosystem of interconnected devices that is poised to reshape industries and daily life.

The proliferation of IoT devices will facilitate the integration of computers with software, enhancing user connectivity to essential resources and streamlining corporate workflows. As electronic gadgets become increasingly sophisticated, the demand for high-performance materials that can withstand varying environmental conditions becomes critical.

LSR's excellent properties, such as high-temperature resistance, electrical insulation, and chemical stability, make it an ideal choice for use in a wide range of electronic applications, including protective housings, connectors, and seals.

Leading companies in the LSR market include leading chemical manufacturers such as Dow, Wacker Chemie AG, Momentive Performance Materials, and Elkem Silicones. These firms leverage their extensive research and development capabilities to innovate and enhance their product offerings. They often focus on developing specialized grades of LSR that meet specific industry requirements, such as medical, automotive, and electronics applications.

Geographical competition also plays a role in the LSR market. Regions such as North America, Europe, and Asia Pacific have distinct market dynamics influenced by local regulations, manufacturing capabilities, and demand trends. For instance, Asia Pacific is witnessing rapid growth due to the increasing automotive and electronics sectors, leading to intensified competition among local and international players.

Recent Industry Developments

|

Attributes |

Details |

|

Forecast Period |

2024 to 2031 |

|

Historical Data Available for |

2019 to 2023 |

|

Market Analysis |

US$ Billion for Value |

|

Key Regions Covered |

|

|

Key Market Segments Covered |

|

|

Key Companies Profiled in the Report |

|

|

Report Coverage |

|

|

Customization & Pricing |

Available upon request |

By Grade

By End-use Industry

By Region

To know more about delivery timeline for this report Contact Sales

Yes, the market is set to reach US$ 5.81 Bn by 2031.

Automotive sector is the main consumer that companies need to target.

Liquid silicone rubber materials are employed mainly in consumer products including electronics, appliances, healthcare application and baby products.

Dow is considered the leading player.

As of September 2024, Dow. has been dominant.