Industry: Healthcare

Published Date: December-2024

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 189

Report ID: PMRREP2822

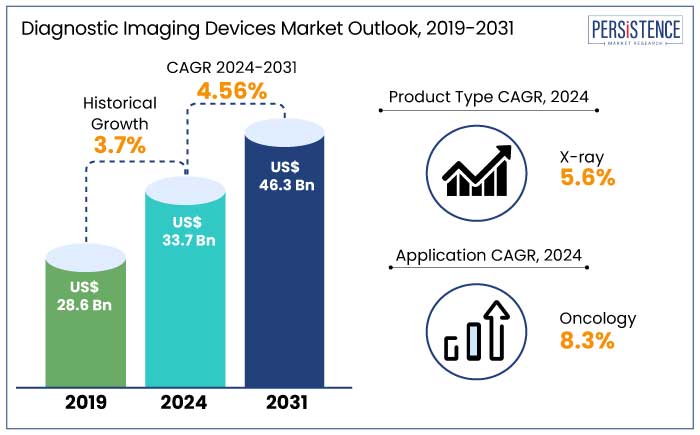

The diagnostic imaging devices market is anticipated to reach a size of US$ 33.7 Bn by 2024. It is predicted to witness a CAGR of 4.6% during the forecast period to reach the value of US$ 46.3 Bn by 2031. Government authorities in emerging countries are prioritizing the development of their healthcare infrastructure, including diagnostic facilities. Asia Pacific is projected to emerge as the leading region in the industry owing to the rising healthcare awareness, insurance coverage, and affordability.

Hybrid imaging systems that combine two or more imaging modalities to provide improved diagnostic accuracy are estimated to witness expansion. Manufacturers in the industry are working toward developing low-dose, portable, and efficient CT and X-ray systems to address radiation exposure concerns.

Portable X-ray and ultrasound devices are expected to account for a market share of 26% by the end of the forecast period. Handheld ultrasound devices like GE’s Vscan are gaining traction owing to their affordability, portability, and high-2quality imaging.

Key Highlights of the Industry

|

Market Attributes |

Key Insights |

|

Diagnostic Imaging Devices Market Size (2024E) |

US$ 33.7 Bn |

|

Projected Market Value (2031F) |

US$ 46.3 Bn |

|

Global Market Growth Rate (CAGR 2024 to 2031) |

4.6% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

3.7% |

Rapid economic expansion in countries like India and China are enabling high investments in healthcare infrastructure in Asia Pacific. Healthcare spending in the region grew by 8% annually in 2023. Asia Pacific alone records 50% of global diabetes cases with over 230 million people affected in 2023. The region is projected to hold a share of 22.3% in 2024.

Cancer and cardiovascular diseases are on the rise owing to the aging population and lifestyle changes. Diagnostic imaging modalities like MRI and CT scans are progressively being used for early detection and management of these conditions. The urban population in Asia Pacific is estimated to reach 3.5 billion by 2031, thereby boosting access to advanced diagnostic facilities.

Government authorities in the region are significantly investing in diagnostic imaging as a part of the national healthcare initiative. Policies like “Health China 2030” and Ayushman Bharat scheme aim at expanding imaging services to rural and underserves populations while providing affordable diagnostic services to over 500 million people.

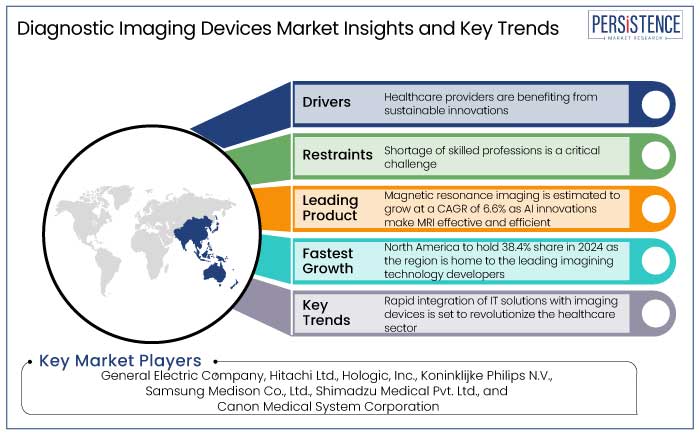

North America, especially the U.S., is consistently leading the global healthcare expenditure. In 2023, the country spent US$ 4.7 trillion on healthcare, accounting for nearly 18% of its GDP. This high expenditure supports investments in advanced diagnostic technologies like AI-powered imaging devices and hybrid systems like PET/CT. The region has a high demand for portable x-ray and ultrasound devices for use in emergency care and remote settings and accounts for 38.4% market share in 2024.

The U.S. is home to some of the leading imaging technology developers, including Hologic, GE Healthcare, and Siemens Healthineers. The region accounts for 45% of global medical imaging research and development, thereby driving advancements in imaging modalities.

Widespread awareness campaigns for diseases including breast cancers and cardiovascular conditions promote routine imaging. For instance, the U.S. conducts around 40 million mammograms conducted annually in the U.S., thereby making breast imaging one of the largest application segments.

By 2031, the number of X-ray procedures across the globe is estimated to exceed 5 billion annually, thereby reflecting their essential role in healthcare. The industry is witnessing a shift to digital technologies where analog systems are being replaced by digital radiography (DR) systems. These offer fast image processing and retrieval while decreasing radiation exposure by 30% compared to conventional methods.

X-rays are finding increasing use in preventive care where they are used in routine screenings like Chest X-rays for tuberculosis and lung cancer detection. Government authorities and healthcare providers across the globe are investing in preventive care programs, thereby boosting demand.

Compared to modalities like MRI and CT, X-ray systems are affordable and easy to maintain. This affordability makes X-rays preferred in emerging economies with limited healthcare budgets and rural areas where access to advanced imaging systems is constrained.

The number of new cancer cases is estimated to rise from 20 million in 2023 to 30 million annually by 2040, according to the statistics provided by the World Health Organization. Imaging modalities like CT, MRI, and PET scans are crucial for early detection, accurate staging of tumors, and treatment planning and monitoring.

Rising demand for early cancer detection as it substantially enhances survival rates and treatment outcomes. For instance, the 5-year survival rate for localized breast cancer detected early is 99% compared to 30% for late-stage detection. Diagnostic imaging plays a crucial role in early detection programs like mammography for breast cancer and low-dose CT scans for lung cancer.

The diagnostic imaging devices market is estimated to continue its growth trajectory throughout the forecast period as healthcare providers adopt advanced imaging solutions to cater to the rising demand for early and accurate diagnostics.

Significant contributions from AI integration, portable devices, and hybrid imaging systems are predicted to facilitate expansion. By 2023, 1 in 6 people worldwide will be aged 60 or older, thereby increasing vulnerability to chronic conditions needed for diagnostic imaging.

Adoption of AI in algorithms is likely to enable efficient and accurate image interpretation, thereby decreasing workloads for radiologists by 40%. Real-time decision making with the help of AI will assist in enhancing diagnostic accuracy in cancer detection, cardiovascular imaging, and neurological assessments. Rural areas and developing nations are expected to have a growing demand for point-of-care diagnostics in emergency care, thereby spiking demand.

The diagnostic imaging devices market growth experienced a robust CAGR of 3.7% during the historical period. Growing incidence of chronic conditions fueled the demand for advanced diagnostic imagining technologies during the period.

According to the Internation Agency for Research on Cancer (IARC), cancer cases across the globe witnessed an increase from 18 million in 2018 to approximately 20 million in 2023, thereby driving the need for CT, MRI, and PET imaging.

The COVID-19 pandemic further accelerated the use of diagnostic imaging, especially CT scans and chest C-rays, to detect lung-related complications in COVID-19 patients. Hospitals reported an increase of 30% to 40% in CT imaging volumes during the peak pandemic period. Breakthroughs in imaging modalities during the historical period enhanced diagnostic accuracy and patient safety.

Technological Advancements in Imaging Modalities to Enable Efficient and Cost-effective Diagnostics

Technological advancements in imaging modalities are revolutionizing diagnostic imaging devices to enable accurate, fast, and cost-effective diagnosis across a range of medical conditions. Recent advancements in MRI technologies focus on enhancing image resolutions and decreasing scanning times. MRI is estimated to hold a share of 28.2% for efficient and accurate diagnosing.

High-field MRI scanners, for instance 7T MRI, offer ultra-high-resolution images with great detail which is especially useful for detecting small lesions, neurological disorders, and tumors. Advances in computed tomography technology focus on decreasing exposure to radiation while enhancing image quality and scan speed.

New dual-energy CT and high-definition CT scanners enable swift and detailed imaging with lower radiation doses, that is especially important for pediatric and sensitive patient groups. Iterative reconstruction algorithms decrease the radiation dose needed for CT scans while maintaining superior image quality.

Diversification of Imaging Applications to Boost Expansion

Diagnostic imaging solutions are no longer limited to conventional uses as they are being applied to an increasingly diverse range of medical conditions and specialties. According to the World Health Organization (WHO), cancer is the second leading cause of death worldwide.

As the global incidence of cancer continues to rise, the demand for advanced imaging technologies to detect, diagnose, and monitor cancer is growing. By 2040, the number of cancer cases globally is estimated to reach 29.5 million. Diagnostic imaging techniques like MRI, PET-CT, and mammography are vital for early cancer detection, staging, and treatment monitoring.

A report by the WHO reported cardiovascular diseases to account for 17.9 million deaths globally, thereby representing 31% of all global deaths. Advances in cardiovascular imaging have substantially improved the diagnosis and management of heart diseases. CT Angiography has become a standard imaging technique for evaluating blood vessels, specifically in patients with suspected coronary artery disease.

Diagnostic imaging devices are finding application in dental imaging as well as veterinary imaging. 3D imaging and cone beam CT (CBCT) are a significant growth area in dental imaging applications. Advanced technologies like MRI, CT scans, and ultrasound are used for diagnosing animals, especially pets and livestock.

Shortage of Skilled Professionals to Emerge as a Critical Challenge

Shortage of skilled professionals, especially radiologists and imaging technicians is a critical challenge in the industry. This shortage not only limits the utilization of advanced imaging technologies but also delays diagnosis and treatment, thereby negatively impacting patient outcomes.

A survey conducted by the Royal College of Radiologists (RCR) in 2023 revealed that the U.K. faced a 34% shortfall in radiologists, with an estimated 2,000 additional radiologists required to meet the current demand. This shortage leads to patients facing delays in obtaining diagnostic imaging results. For instance,

The WHO pointed out that there is also a shortage of technicians, especially in low- and middle-income countries. In high income countries like the U.S., imaging technicians face high turnover rates owing to workload pressures and insufficient pay. A survey by the Bureau of Labor Statistics in 2022 noted a 7% decline in the number of new graduates entering imaging technician workforce compared to a decade ago.

Integration of Imaging Devices with IT Solutions

Integration of diagnostic imaging devices with IT solutions is a transformative trend that is revolutionizing the healthcare sector. This integration helps in improving efficiency, accuracy, and accessibility of diagnostic imaging by enabling seamless data management, supporting advanced analytics, and facilitating real-time sharing.

The increasing need for fast and accurate diagnostics along with the shift toward value-based care is becoming essential in enhancing healthcare delivery. Picture Archiving and Communication Systems (PACS) is one of the most significant IT integrations in diagnostic imaging as they store, retrieve, manage, and share medical images electronically.

Use of PACS enhances efficiency by minimizing the time spent on retrieving images and decreases costs related to storing physical films. Integration of imaging devices with Electronic Health Records (EHRs) enables real-time sharing of imaging results with other patient health data.

Sustainability and Eco-friendly Innovations to Benefit Healthcare Providers

Growth in environmental concerns has led healthcare systems to strive to decrease their carbon footprints, thereby increasing their focus on sustainability and eco-friendly innovations. Companies are adapting to regulatory pressures and market demands by creating energy-efficient and environmentally responsible imaging solutions. These innovations contribute to the global sustainability goals while benefiting healthcare providers by decreasing operational costs, increasing efficiency of diagnostic procedures, and enhancing patient safety.

Companies are decreasing energy consumption by creating energy-efficient models that consume less power and operate efficiently. For instance, GE Healthcare introduced an energy-efficient MRI scanner that decreases energy consumption by 40% compared to previous models. Philips also launched energy-efficient versions of their MRI and CT machines with a few systems using 30% less energy compared to old versions.

The broad trend toward sustainability has led diagnostic imaging companies to incorporate recyclable materials in their devices while decreasing the use of hazardous substances. According to Siemens Healthineers, approximately 70% of materials in their imaging devices are recyclable. Canon Medical Systems has implemented water-saving technologies in their manufacturing processes, including water recycling systems that decrease water consumption by 40%.

Companies in the industry are continuously investing in the development of modern technologies like AI-powered imaging, 3D imaging, and enhance MRI or CT scanners. Investment is made to provide precise diagnostics, efficient processing, and improved patient outcomes. Portable ultrasound devices, handheld imaging solutions, and small equipment for point-of-care diagnostics are gaining traction as companies are looking to cater to developing markets and hospitals having limited space.

Leading companies in the diagnostic imaging space market usually acquire small and innovative firms to gain access to new technologies to expand their product portfolios. Businesses are progressively partnering with hospitals, clinics, and research institutions to understand the requirements of their target audience and enhance their product design while boosting product adoption.

Recent Industry Developments

|

Attributes |

Details |

|

Forecast Period |

2024 to 2031 |

|

Historical Data Available for |

2019 to 2023 |

|

Market Analysis |

US$ Billion for Value |

|

Key Regions Covered |

|

|

Key Market Segments Covered |

|

|

Key Companies Profiled in the Report |

|

|

Report Coverage |

|

|

Customization and Pricing |

Available upon request |

By Product Type

By Application

By End Use

By Region

To know more about delivery timeline for this report Contact Sales

The market is predicted to reach a size of US$ 46.3 Bn by 2031.

Most popular diagnostic imaging types are CT scan, X-ray imaging, magnetic resonance imaging (MRI), and ultrasound.

These devices enable doctors to view through the body to find clues regarding medical conditions.

General Electric Company, Hitachi Ltd., and Hologic, Inc. are the leading companies in the market.