Industry: Healthcare

Published Date: April-2025

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 180

Report ID: PMRREP35187

The global cancer diagnostics market size is anticipated to reach a value of US$137.8 Bn in 2025 and witness a CAGR of 7.1% from 2025 to 2032. The market will likely attain a value of US$222.7 Bn by 2032.

According to Persistence Market Research, high cancer prevalence in the population and advancements in diagnostic technologies is encouraging the need for accurate cancer diagnostics. Besides, the early detection enhances patient outcomes is further driving demand for innovative diagnostic solutions such as liquid biopsy, next-generation sequencing (NGS), and AI-driven imaging technology.

Governments and healthcare organizations are investing heavily in cancer screening programs, further boosting market expansion. North America is a dominant market due to strong healthcare infrastructure and the high adoption of advanced diagnostics. However, Asia Pacific is poised to experience positive growth due to rise in healthcare investments.

Key Industry Highlights:

|

Global Market Attribute |

Key Insights |

|

Cancer Diagnostics Market Size (2025E) |

US$ 137.8 Bn |

|

Market Value Forecast (2032F) |

US$ 222.7 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

7.1% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.5% |

Biopsy is the leading diagnostic test category in the cancer diagnostics market and is projected to hold 35.3% market share in 2025. This dominance is attributed to its high accuracy and the increasing prevalence of cancer globally. Advancements in minimally invasive biopsy techniques, such as liquid and image-guided, perform diagnostic precision while reducing patient discomfort. Governments and healthcare organizations are investing heavily in cancer screening programs further strengthens the role of biopsy. With continued innovation and integration of AI-driven pathology, biopsy is set to remain the cornerstone of cancer diagnostics, ensuring early detection and improved patient outcomes.

The increasing prevalence of smoking continues to be a significant factor fueling the growth of the lung cancer segment. According to the World Health Organization (WHO), tobacco use is responsible for nearly 85% of all lung cancer cases globally. Despite awareness campaigns, smoking rates remain high in several regions, particularly in developing countries, where the adoption of tobacco products is rising.

Additionally, clinical research affirms that a significant correlation exists between smoking and lung cancer. The World Health Organization (WHO) states that smokers face a higher likelihood of developing lung cancer than non-smokers. Additionally, the risk increases with both the quantity of cigarettes consumed daily and smoking frequency. Moreover, governments and healthcare organizations invest in initiatives to enhance diagnostic accessibility further propelling the demand for diagnostic lung cancer solutions.

Hospitals continue to dominate largely due to the rising number of patients needing comprehensive diagnostic services and the increasing incorporation of advanced imaging technologies. The widespread adoption of in vitro diagnostics (IVD), along with imaging techniques, has played a significant role in enabling earlier and more accurate detection of various cancers, thereby enhancing clinical outcomes.

Diagnostic laboratories are witnessing growing demand, particularly in the consumables segment. Items such as antibodies, probes, and test kits are experiencing increased utilization, driven by the need for reliable, fast, and precise diagnostic tools. This segment commands a major portion of the market due to its efficiency in processing large sample volumes and supporting a wide range of cancer tests.

Cancer research institutes are placing a strong focus on emerging diagnostic approaches such as liquid biopsies and genomic profiling. These technologies provide critical molecular-level data to support the advancement of personalized medicine. The segment is expected to grow robust, aligning with the broader shift toward targeted therapies and individualized treatment plans. Additionally, ambulatory surgical centres embrace the point-of-care testing to improve diagnostic speed and decision-making. The development of compact, portable diagnostic equipment has facilitated quicker results and broader access, particularly in outpatient settings.

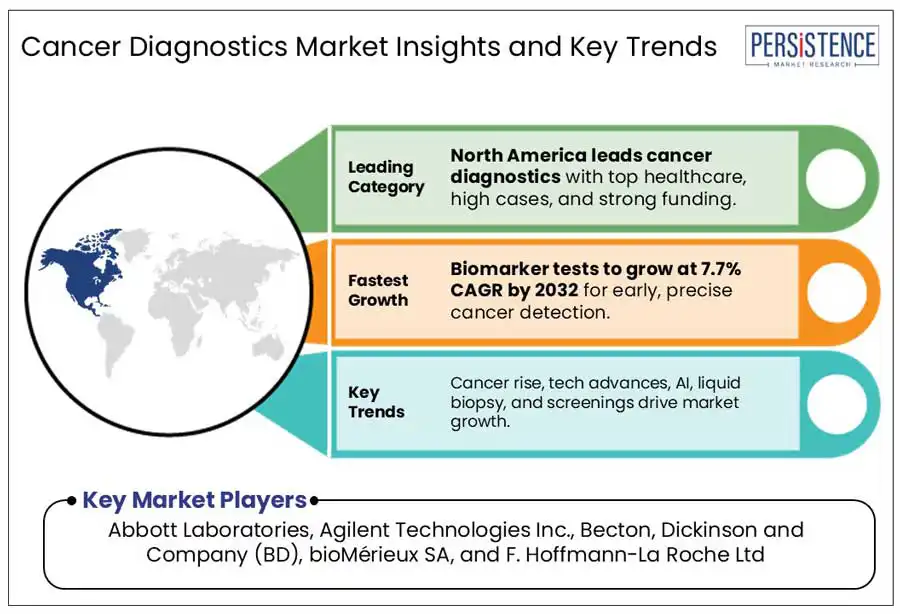

North America leads the global market, with a 42.3% share in 2025, driven by the advanced healthcare infrastructure, rising cancer cases, increased research funding, and an early adoption of innovative diagnostic technologies. The rise in the U.S. cancer cases and smoking-related fatalities in 2024 drives the need for advanced diagnostics. Innovations such as liquid biopsy and AI imaging enhance early detection. Increased healthcare spending and biotech collaborations further solidify North America’s advancement in cancer diagnostics.

Europe is poised to experience a significant growth, driven by advancements in biotechnology and increased investments in genomic sequencing, particularly in the U.K. and Germany. The U.K. cancer diagnostics market is expected to grow due to the rising collaborations among key players, increased adoption of biomarker tests, and government initiatives supporting early detection. Advancements in genomic sequencing and innovative product launches, such as Invitae’s LiquidPlex Dx further drive market expansion across the country.

Asia Pacific is expected to witness a robust growth driven by increasing healthcare reforms, urbanization, and economic expansion. Established players are expanding their regional footprint, further boosting market growth.

China’s cancer diagnostics market is projected to grow significantly due to the rise in cancer cases and advancements in early detection methods. According to the National Cancer Center China (NCCC), around 3.24 million new cases and 1.69 million deaths from cancer were reported in China in 2024. Companies are leveraging partnerships to expand multi-cancer early detection (MCED) test accessibility.

India is emerging as a key player in South Asia with an increasing focus on innovative technologies and early detection. According to the Indian Council of Medical Research (ICMR), India will witness over 1.57 million new cancer cases annually by 2025, a 12% increase from 2020. The demand for affordable and accessible diagnostic solutions drive investments in AI-based imaging, liquid biopsy, and biomarker testing.

The Middle East and Africa presents significant growth opportunities. For underdeveloped African countries, lack of clinical access and infrastructure results in the lack of organized cancer screening programs. Companies such as Guardant Health, Pathcare, and others are actively enhancing cancer diagnostics in the MEA through technological advancements, strategic partnerships, and tailored programs aim to improve early detection and treatment outcome for cancer patients.

The global cancer diagnostics market is highly competitive. Innovation, strategic alliances, and cutting-edge technologies are the strategies adopted by leading cancer diagnostics companies to improve early cancer detection. While Agilus Diagnostics has introduced sophisticated genome testing for quicker results, companies such as Bio-Rad Laboratories and Quidel Corporation are diversifying their molecular diagnostics offerings. To increase accuracy, businesses are also spending money on biomarker-based assays, liquid biopsy innovations, and AI-driven diagnostic tools. Their market presence is strengthened through partnerships with healthcare providers and research institutions.

|

Report Attribute |

Details |

|

Historical Data/Actuals |

2019 - 2024 |

|

Forecast Period |

2025 - 2032 |

|

Market Analysis Units |

Value: US$ Bn, Volume: As applicable |

|

Geographical Coverage |

|

|

Segmental Coverage |

|

|

Competitive Analysis |

|

|

Report Highlights |

|

|

Customization and Pricing |

Available upon request |

By Diagnostic Test

By Application

By End-Use

By Region

To know more about delivery timeline for this report Contact Sales

The global market is estimated to increase from US$137.8 billion in 2025 to US$222.7 billion in 2032.

The increasing demand for advanced diagnostic technologies and early screening programs drives the global market.

The market is projected to record a CAGR of 7.1% during the forecast period from 2025 to 2032.

Abbott Laboratories, Agilent Technologies Inc., Becton, Dickinson and Company (BD), bioMérieux SA, F. Hoffmann-La Roche Ltd, and Others.

Opportunities include AI-driven diagnostics, liquid biopsy advancements, biomarker-based testing, early screening programs, and global market expansion initiatives.