- Biotechnology

- Antimicrobial Resistance Diagnostics Market

Antimicrobial Resistance Diagnostics Market Size, Share, and Growth Forecast, 2026 – 2033

Antimicrobial Resistance Diagnostics Market by Pathogen Type (Methicillin-resistant Staphylococcus aureus (MRSA), Others), Technology (Polymerase Chain Reaction (PCR), Others), End-user (Hospitals & Clinics, Others), and Regional Analysis for 2026-2033

Antimicrobial Resistance Diagnostics Market Size and Trends Analysis

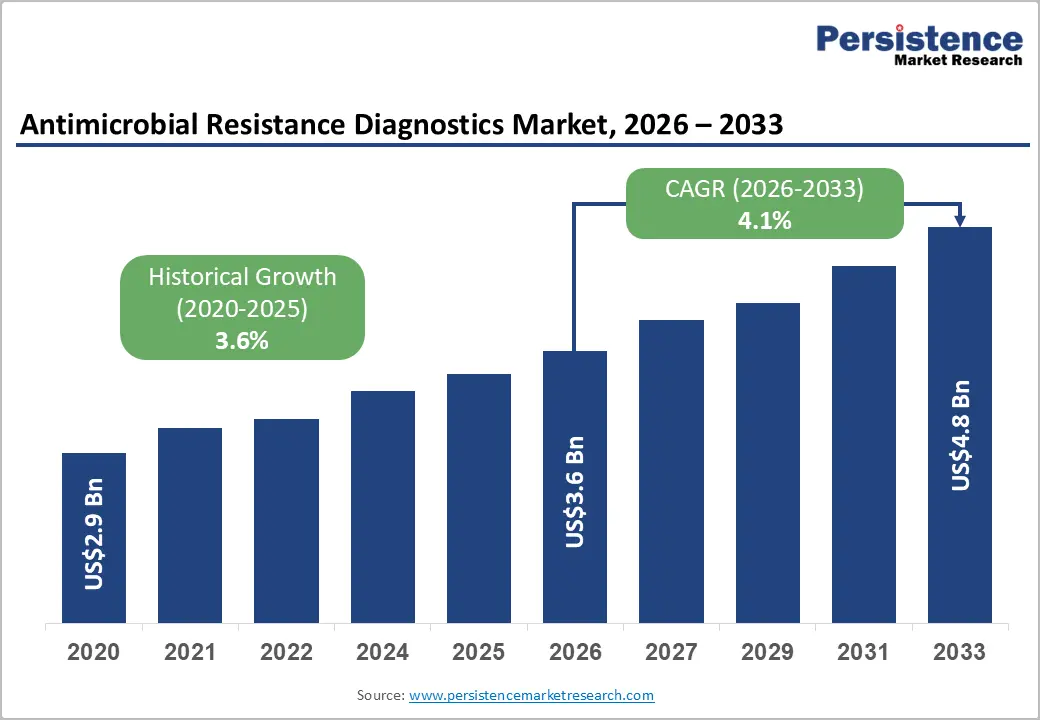

The global antimicrobial resistance diagnostics market size is likely to be valued at US$3.6 billion in 2026 and is estimated to reach US$4.8 billion by 2033, growing at a CAGR of 4.1% during the forecast period from 2026 to 2033, driven by demographic disease burden shifts, regulatory escalation in antimicrobial stewardship programs, expansion of molecular diagnostic infrastructure, and wider integration of rapid testing platforms in clinical workflows.

The rising incidence of drug-resistant infections across hospital and community settings is increasing demand for rapid identification tools that reduce empirical antibiotic use. Regulatory frameworks introduced by public health authorities are reinforcing mandatory resistance surveillance programs and strengthening the adoption of diagnostic systems.

Key Industry Highlights:

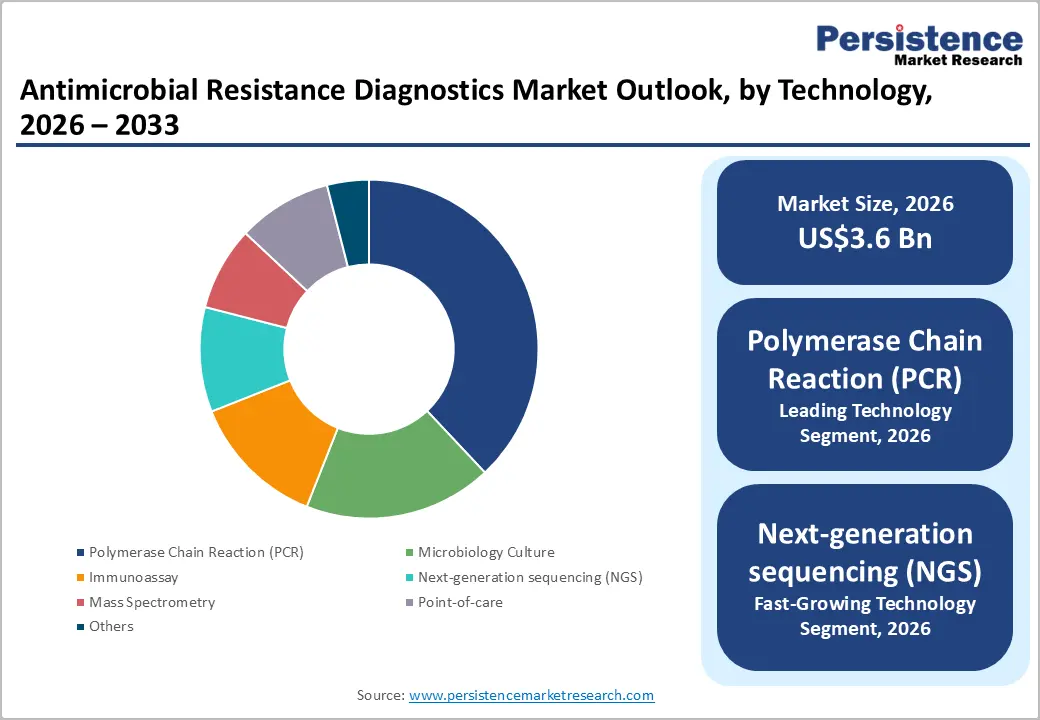

- Leading Technology: Polymerase chain reaction (PCR) is estimated to hold roughly 38% revenue share in 2026, due to established clinical validation, broad regulatory acceptance, and integration into near-patient testing workflows across acute care settings.

- Fastest-growing Technology: Next-generation sequencing (NGS) is forecast to record the fastest growth, driven by falling per-sample costs and the expanding clinical utility of whole-genome-based resistance gene detection.

- Leading Pathogen Type: MRSA is set to hold around 28% revenue share in 2026, driven by mandatory screening protocols in surgical and ICU settings across North America and Europe.

- Fastest-growing Pathogen Type: Drug-resistant Streptococcus pneumoniae diagnostics are projected as the fastest-growing segment, supported by rising respiratory infection incidence.

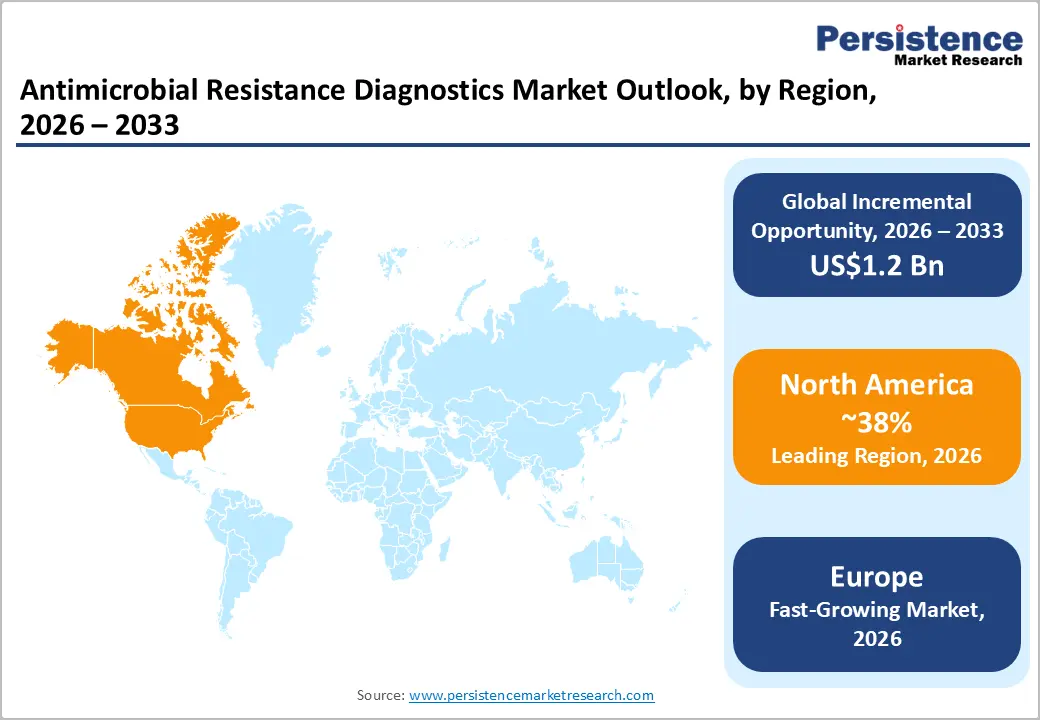

- Regional Leadership: North America is projected to capture roughly 38% of the market share in 2026, while Europe is forecast to record the fastest growth due to regulatory harmonization and genomic surveillance expansion.

- Competitive Environment: The market reflects a moderately consolidated structure, with key players BioMérieux, Cepheid, Becton Dickinson, Roche Diagnostics, and Thermo Fisher Scientific leveraging proprietary reagent ecosystems, global distribution scale, and regulatory pre-clearance portfolios to maintain competitive positioning.

- Innovation Trends: AI-driven resistance prediction integration, multiplex panel expansion for single-assay pathogen coverage, and miniaturized PoC molecular platforms are shaping long-term market evolution and directing capital allocation toward next-generation diagnostic architectures

DRO Analysis

Driver - Rapid Molecular Testing Integration in Clinical Workflows

The escalation of healthcare-associated infections caused by drug-resistant bacteria accelerates clinical deployment of rapid molecular diagnostics. Traditional culture methodologies require forty-eight to seventy-two hours for pathogen identification, creating dangerous therapeutic delays for critically ill patients. Implementing automated polymerase chain reaction systems reduces diagnostic turnaround times to less than one hour, allowing immediate optimization of targeted antibiotic regimens.

The Centers for Disease Control and Prevention reported in 2025 that antibiotic-resistant pathogens cause more than 2.8 million infections annually in the U.S. This substantial disease burden forces healthcare networks to standardize rapid diagnostic screening protocols upon patient admission. Early detection mitigates horizontal transmission risks within intensive care units, decreasing overall hospital stay lengths and operational liabilities.

Restraint - High Capital Acquisition Cost and Maintenance Liabilities

Procurement of sophisticated molecular platforms imposes severe capital budget strains on clinical institutions. Advanced instruments require substantial initial investments, specialized laboratory renovations, and recurring software licensing fees. These capital allocations create a severe barrier to entry for lower-volume laboratory networks, restricting overall tool utilization. High operational overhead ultimately compresses facility operating margins and restricts technology diffusion outside tier-one urban health systems.

The underlying technology architectures demand precise environmental conditions and complex calibration intervals to ensure regulatory compliance. Component replacements and unexpected service interventions represent continuing financial exposures that complicate short-term budgeting. Maintenance dependencies frequently strain facility resources, particularly when single-source supply agreements restrict competitive service bidding. This operational financial pressure limits the scalability of comprehensive diagnostic installations across fragmented healthcare regions.

Opportunity - Decentralization via Point-of-Care Microfluidic Platforms

Transitioning critical diagnostic capabilities from central laboratories to decentralized patient interfaces creates an actionable growth pathway. Near-patient testing configurations eliminate transit delays, allowing emergency departments to establish definitive isolation protocols within minutes of patient admission. The incorporation of microfluidic channels onto single-use testing cartridges minimizes manual sample processing requirements, reducing institutional labor dependencies. This decentralization strategy expands the clinical user base to include long-term care units and community health clinics.

Integrated microfluidic technology facilitates automated extraction and rapid amplification of target resistance genes directly from unprocessed patient samples. Immediate diagnostic confirmation allows healthcare providers to implement targeted narrow-spectrum interventions during initial consultations. This rapid capability reduces reliance on broad-spectrum alternatives, preventing community-acquired resistance development. Expanding into decentralized clinical nodes provides a durable avenue for consistent, high-volume consumable reagent utilization.

Category-wise Analysis

Pathogen Type Insights

Methicillin-resistant Staphylococcus aureus (MRSA) is anticipated to secure around 28% of the antimicrobial resistance diagnostics market share in 2026, reflecting its status as the most surveilled healthcare-associated pathogen globally. Cepheid's GeneXpert MRSA assay, widely deployed across U.S. and European hospitals, exemplifies the scale of molecular testing infrastructure built around this organism. Mandatory screening protocols in surgical and ICU settings sustain high diagnostic volumes independent of outbreak conditions.

Drug-resistant Streptococcus pneumoniae (DRSP) is expected to be the fastest-growing segment, propelled by rising respiratory infection burden and pediatric vulnerability patterns. Adoption of multiplex respiratory panels in emergency departments, identifying DRSP in pneumonia cases. Expansion of respiratory surveillance programs supports sustained growth momentum.

Technology Insights

Polymerase chain reaction (PCR) is poised to dominate with a forecast market share of over 38% in 2026, powered by their established clinical validation, regulatory acceptance, and compatibility with near-patient workflows. Roche's cobas Liat system, deployed at point-of-care in hospital emergency departments, demonstrates PCR's reach beyond central laboratories. Speed-to-result advantages over culture methods create a direct clinical justification for continued platform investment across acute care environments.

Next-generation sequencing (NGS) is estimated to be the fastest-growing segment, fueled by falling per-sample sequencing costs and the expanding menu of resistance genes detectable within a single run. Illumina's MiSeq DX platform, adopted in reference laboratory networks, represents the commercial translation of this capability into routine diagnostic use. Decreasing instrument costs and the availability of curated resistance gene databases are enabling a broader set of clinical microbiology laboratories to operationalize NGS workflows.

End-user Insights

Hospitals and clinics are likely to be the leading segment with a projected 47% of the antimicrobial resistance diagnostics market share in 2026 due to their central role in managing severe and drug-resistant infections under stewardship program requirements. Cedars-Sinai Medical Center's integrated AMR diagnostic program, linking rapid testing to antimicrobial prescribing dashboards, illustrates the institutional model driving sustained test volume. Mandatory infection control protocols create a structural baseline of diagnostic demand within acute care facilities.

Pharmaceutical and biotechnology companies are anticipated to be the fastest-growing segment. Due to the expansion of clinical trial pipelines for novel antibiotics and bacteriophage therapies, which require companion diagnostic validation. AstraZeneca's partnership with diagnostics firms to co-develop resistance biomarker panels for antibiotic trial enrollment represents an emerging commercial model.

Regional Insights

North America Antimicrobial Resistance Diagnostics Market Trends

North America is expected to lead with an estimated 38% share of the market in 2026, supported by advanced clinical laboratory infrastructure, strong surveillance systems, and high adoption of molecular diagnostic platforms. Expansion of automated hospital laboratories strengthens rapid pathogen detection and resistance profiling.

U.S. Antimicrobial Resistance Diagnostics Market Insights

The U.S. is projected to account for nearly 82% of regional demand share in 2026, driven by large-scale deployment of hospital-based molecular diagnostic systems and national resistance monitoring programs led by public health agencies. Expansion of antimicrobial stewardship initiatives increases diagnostic testing volumes across intensive care units.

Canada Antimicrobial Resistance Diagnostics Market Insights

Canada is expected to hold approximately 18% of the regional demand share in 2026, supported by centralized laboratory networks and provincial infection control programs. Expansion of diagnostic accessibility across remote healthcare facilities improves early detection of resistant pathogens.

Europe Antimicrobial Resistance Diagnostics Market Trends

Europe is forecast to be the fastest-growing market with an estimated 32% share in 2026, stimulated by harmonized regulatory frameworks, expanded genomic surveillance initiatives, and rising hospital infection control mandates. Strengthening cross-border resistance monitoring programs improves data standardization. Investment in automated microbiology systems enhances diagnostic throughput across clinical laboratories.

Germany Antimicrobial Resistance Diagnostics Market Insights

Germany is projected to account for approximately 28% of regional demand share in 2026, supported by advanced hospital laboratory automation and strong adoption of molecular diagnostic platforms. Expansion of sequencing integration in reference laboratories strengthens resistance gene mapping capabilities. Public health investment in infection surveillance systems enhances diagnostic consistency across healthcare networks.

U.K. Antimicrobial Resistance Diagnostics Market Insights

The U.K. is expected to hold nearly 22% of regional demand share in 2026, driven by national infection surveillance programs and the expansion of rapid molecular testing in hospital systems. Integration of antimicrobial resistance monitoring frameworks improves diagnostic standardization. Increased funding for diagnostic innovation supports the adoption of multiplex testing platforms.

Asia Pacific Antimicrobial Resistance Diagnostics Market Trends

Asia Pacific is anticipated to hold approximately 24% share of the market in 2026, driven by rising infectious disease burden, expanding hospital infrastructure, and increasing investment in diagnostic laboratory networks. Growth in urban healthcare facilities strengthens the adoption of molecular testing platforms.

China Antimicrobial Resistance Diagnostics Market Insights

China is projected to account for nearly 36% of regional demand share in 2026, supported by large-scale hospital infrastructure expansion and national antimicrobial resistance surveillance programs. Increased deployment of automated diagnostic platforms strengthens laboratory efficiency. Domestic manufacturing capacity reduces diagnostic system costs and improves accessibility across tiered healthcare systems.

India Antimicrobial Resistance Diagnostics Market Insights

India is expected to hold approximately 28% of the regional demand share in 2026, driven by the expansion of diagnostic laboratory networks and increasing hospital-based infection testing programs. Government-led public health initiatives strengthen resistance monitoring frameworks. Growth in private healthcare infrastructure increases the adoption of automated molecular diagnostic systems.

Competitive Landscape

The global antimicrobial resistance diagnostics market is moderately consolidated, with the top five players comprising BioMérieux, Cepheid (Danaher), Becton Dickinson, Roche Diagnostics, and Thermo Fisher Scientific accounting for a combined share estimated at approximately 55% of global revenues in 2026. Consolidation is driven by the high capital requirements for regulatory validation, proprietary reagent ecosystem development, and global distribution network buildout that limit the ability of smaller participants to compete across multiple technology formats simultaneously.

Mid-tier and emerging players occupy specialized niches, focusing on specific pathogen types, geographic markets, or technology modalities. Companies such as Oxford Nanopore Technologies in sequencing, Luminex in multiplex PCR, and Molbio Diagnostics in PoC platforms are carving differentiated positions within the broader competitive structure. The entry of genomics-native companies into clinical diagnostics is introducing new competitive pressure on legacy instrument manufacturers, compelling portfolio expansion through acquisition and co-development partnerships.

Key Industry Developments:

- In May 2026, Biotia launched clinically approved drug resistance reporting for complicated urinary tract infections, supported by its Critical Assessment of Massive Data Analysis (CAMDA) recognition, enhancing genomic-based antimicrobial resistance diagnostics and improving precision-guided treatment decisions for drug-resistant infections.

- In June 2025, a global collaboration led by the Global Antibiotic Research and Development Partnership (GARDP) was launched to strengthen antimicrobial resistance diagnostics through improved access to innovative testing solutions and coordinated international partnerships, supporting faster detection of drug-resistant infections and enhanced global surveillance frameworks.

Companies Covered in Antimicrobial Resistance Diagnostics Market

- BioMérieux SA

- Cepheid (Danaher Corp.)

- Becton, Dickinson and Co.

- Roche Diagnostics

- Thermo Fisher Scientific

- Luminex Corporation

- Hologic Inc.

- Qiagen N.V.

- Abbott Laboratories

- Bruker Corporation

- Oxford Nanopore Technologies

- Molbio Diagnostics

- Mindray Medical International

- Sysmex Corporation

- Siemens Healthineers

Frequently Asked Questions

The global antimicrobial resistance diagnostics market is projected to reach US$3.6 billion in 2026.

Rising prevalence of multidrug-resistant infections, expansion of molecular diagnostic technologies, and strengthening of antimicrobial stewardship regulations drive the antimicrobial resistance diagnostics market.

The antimicrobial resistance diagnostics market is poised to witness a CAGR of 4.1% from 2026 to 2033.

Expansion of point-of-care molecular testing, integration of next-generation sequencing in routine surveillance, and growth of decentralized laboratory infrastructure create key market opportunities in antimicrobial resistance diagnostics.

Some of the key market players include BioMérieux, Cepheid (Danaher), Becton Dickinson, Roche Diagnostics, and Thermo Fisher Scientific.