- Animal Health

- Bacterial Diagnostics in Aquaculture Market

Bacterial Diagnostics in Aquaculture Market Size, Share, and Growth Forecast 2026 - 2033

Bacterial Diagnostics in Aquaculture Market by Technology (PCR / Molecular Diagnostics, Immunoassays, Culture-Based Methods, Others), by Pathogen Type (Vibrio, Aeromonas, Streptococcus, Others), by Aquatic Animal Type (Fish, Crustaceans (Shrimp, Crab), Mollusks, Others), End-user (Aquaculture Farms, Diagnostic Laboratories, Research Institutes), and Regional Analysis, 2026 - 2033

Bacterial Diagnostics in Aquaculture Market Share and Trends Analysis

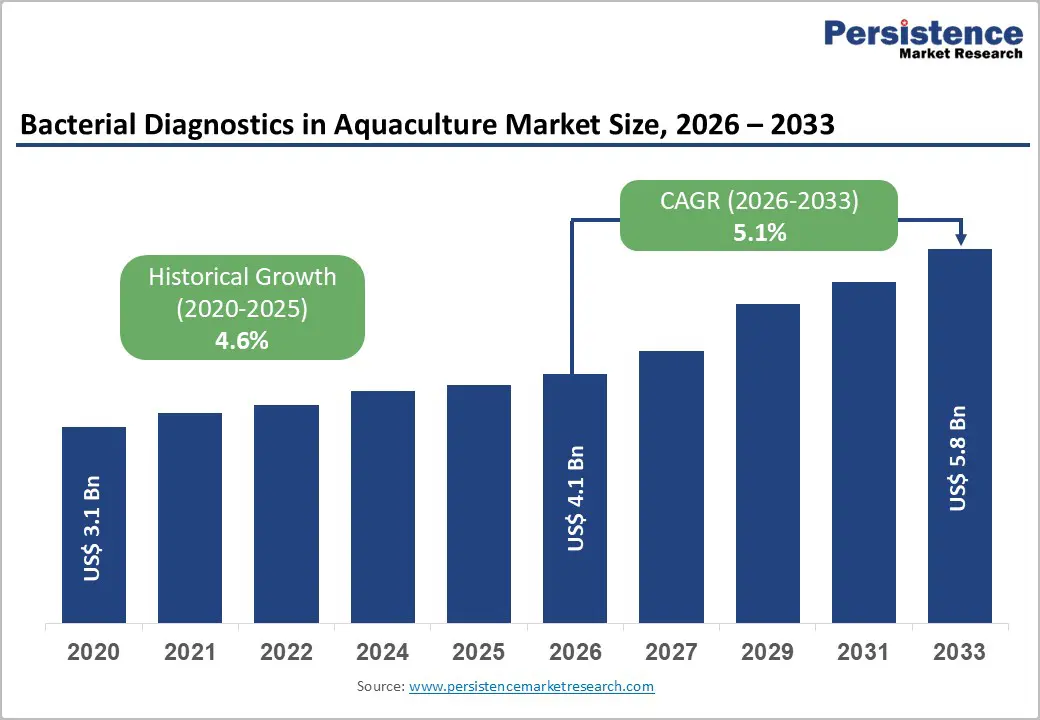

The global bacterial diagnostics in aquaculture market size is expected to be valued at US$ 4.1 billion in 2026 and projected to reach US$ 5.8 billion by 2033, growing at a CAGR of 5.1% between 2026 and 2033.

This outlook reflects intensifying disease pressure in aquaculture systems worldwide, rising economic losses from bacterial outbreaks, and greater reliance on rapid, sensitive diagnostics to protect stocks and ensure food security. As global aquaculture production has risen to about 130.9 million tonnes of output valued at roughly US$ 313 billion, surpassing capture fisheries for the first time, disease management, including rapid bacterial detection, has become a key strategic pillar for sustainable growth.

Key Market Highlights

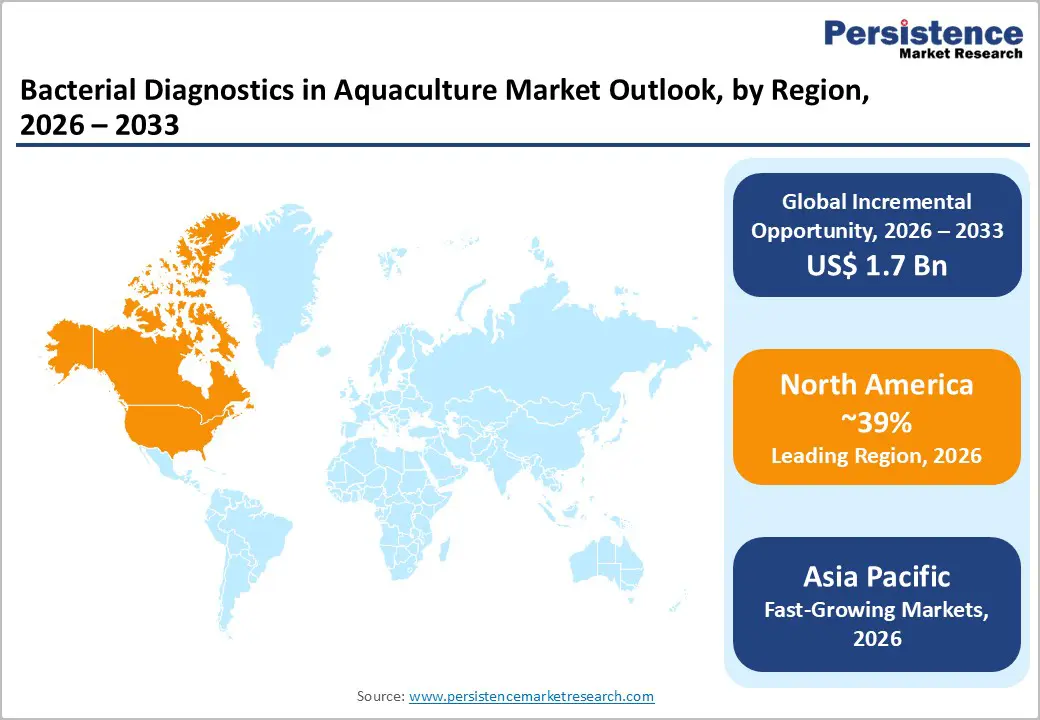

- North America is the leading region in the bacterial diagnostics in aquaculture market, with about 39% share in 2025, supported by stringent seafood safety regulations, advanced aquatic health infrastructures, and the presence of major diagnostics companies offering comprehensive bacterial testing solutions for fish and shellfish producers.

- Asia Pacific is the fastest-growing regional market, driven by its dominant share in global aquaculture production, increasing disease-related losses estimated at several billion US$ annually, and accelerating investments in laboratory and farm-level bacterial diagnostics for fish and shrimp value chains.

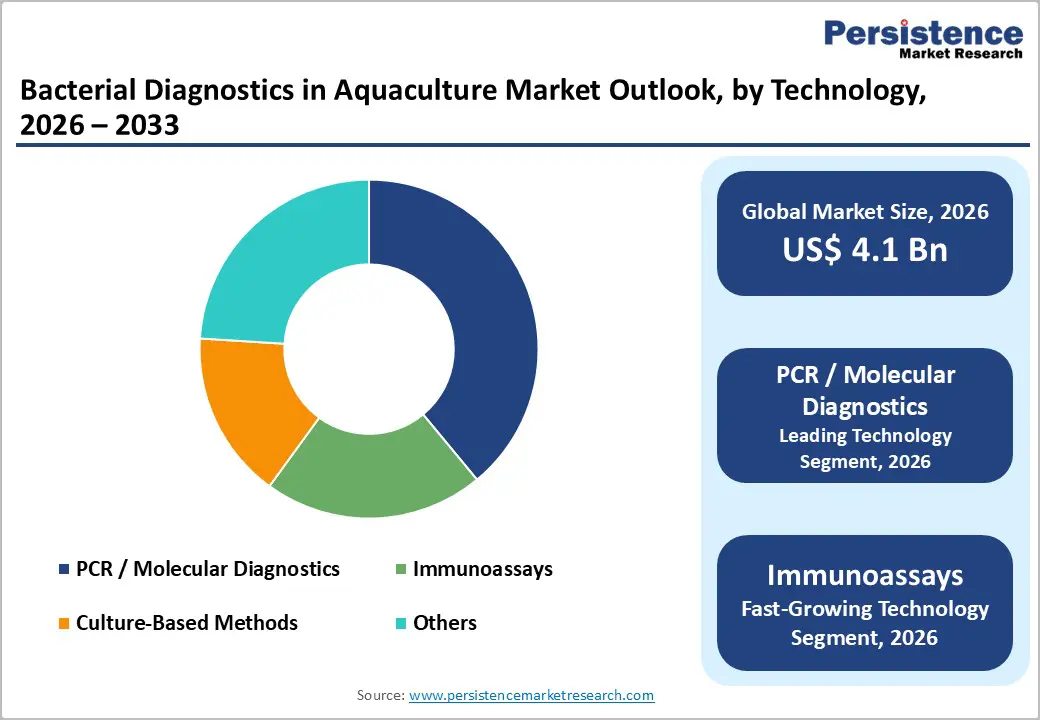

- By technology, PCR/Molecular diagnostics represent the dominant segment with around 39% share in 2025, reflecting the rapid adoption of multiplex and quantitative PCR assays for sensitive, specific detection of key bacterial pathogens such as Vibrio, Aeromonas, and Streptococcus in aquaculture systems.

- Among pathogen types, Vibrio diagnostics form the most prominent subsegment, as species such as Vibrio anguillarum, Vibrio harveyi, Vibrio parahaemolyticus, and Vibrio vulnificus drive recurrent disease outbreaks in marine and coastal aquaculture, prompting widespread use of targeted culture, immunoassay, and PCR-based detection kits.

| Key Insights | Details |

|---|---|

| Bacterial Diagnostics in Aquaculture Market Size (2026E) | US$ 4.1 billion |

| Market Value Forecast (2033F) | US$ 5.8 billion |

| Projected Growth CAGR (2026 - 2033) | 5.1% |

| Historical Market Growth (2020 - 2025) | 4.6% |

Market Dynamics

Drivers - Rise in Disease Burden and Economic Losses in Aquaculture

The substantial and rising economic burden of infectious diseases in farmed aquatic animals fuels more growth. Analyses presented to the Food and Agriculture Organization (FAO) and industry conferences estimate that aquatic animal diseases, including bacterial, viral, and parasitic infections, cost global aquaculture around US$ 6 billion annually, with shrimp alone having suffered losses of more than US$ 10 billion since the 90s. Regional studies in Asia report that diseases of multiple etiology and bacterial hemorrhagic septicemia account for hundreds of millions of US$ in annual production losses, and that expenses on prophylactics and therapeutics can exceed 50% of total disease-related costs. With aquaculture now providing more than 51% of aquatic animal products for human consumption, producers and regulators increasingly prioritize early detection of pathogens such as Vibrio, Aeromonas, and Streptococcus to reduce mortality, protect trade, and sustain rural livelihoods, directly stimulating demand for accurate, rapid diagnostic tools.

Shift Toward Intensive, High-value Production and Biosecurity Frameworks

The shift toward intensive, high-value aquaculture systems and the parallel strengthening of aquatic animal health governance. As aquaculture moves from extensive ponds to high-density cages, recirculating aquaculture systems, and integrated multi-trophic operations, stocking densities, stress, and exposure to opportunistic bacteria increase, raising the likelihood of outbreaks. The World Bank and global aquaculture alliances highlight disease risk as the major constraint to investment, with disease-related risks contributing to high insurance loss ratios and deterring capital flows unless robust biosecurity and health monitoring are in place. In response, governments, veterinary authorities, and producer organizations are formalizing aquatic health strategies aligned with WOAH (OIE) and FAO guidance, which emphasize surveillance, laboratory capacity, and diagnostics for listed and emerging bacterial pathogens. This policy emphasizes surveillance and certification, which directly boost the adoption of PCR / Molecular Diagnostics, Immunoassays, and standardized culture-based methods across farms and laboratories.

Restraints - Limited Diagnostic Capacity and Infrastructure in Low-Resource Settings

A key restraint for the bacterial diagnostics in the aquaculture market is the uneven distribution of laboratory infrastructure and trained personnel, particularly in low- and middle-income countries where over 90% of aquaculture production occurs. Many small-scale farmers lack affordable access to accredited laboratories capable of performing advanced tests, such as multiplex PCR, quantitative PCR (qPCR), or serological assays, and instead rely on empirical treatment and visual diagnosis, which can miss subclinical infections. This diagnostic gap means that a large share of disease events remains undocumented or mischaracterized, undermining both farm-level demand and public-sector investments in bacterial diagnostics.

Cost and Complexity of Advanced Molecular Platforms

Another restraint is the perceived cost and complexity of implementing advanced molecular diagnostic platforms in routine aquaculture operations. While PCR / Molecular diagnostics offer high sensitivity and specificity, they require cold-chain reagents, precision thermocyclers, and skilled technicians, which can be challenging for smaller laboratories or remote regions. Even as companies such as Thermo Fisher Scientific, Bio-Rad Laboratories, and others market streamlined real-time PCR assays for seafood and aquaculture-related bacteria, capital expenditure and operating costs remain barriers to widespread deployment at the farm level. Without financing mechanisms, training programs, and scalable service models, many producers may continue to underutilize formal bacterial diagnostics despite recognizing their value.

Opportunities - Rapid expansion of PCR-based and multiplex molecular diagnostics

One of the most attractive opportunities lies in the rapid expansion and diversification of PCR / Molecular diagnostics for aquatic pathogens. Research has demonstrated that multiplex PCR assays can simultaneously detect several major fish pathogens, such as Aeromonas salmonicida, Flavobacterium psychrophilum, Yersinia ruckeri and multiple Streptococcus species, with detection limits in the range of a few colony-forming units or picograms of DNA. Studies from intensive fish-farming regions such as Brazil show that direct colony PCR coupled with 16S rRNA sequencing enables rapid, cost-effective identification of bacterial pathogens across dozens of isolates, significantly shortening turnaround time compared with conventional culture. Building on such science, companies including Thermo Fisher Scientific, Bio-Rad Laboratories, and specialist providers are commercializing validated real-time PCR kits for Vibrio species and other aquaculture-relevant pathogens, offering results in less than 9-24 hours for seafood and environmental samples. As multiplex and panel-based assays tailored to fish, shrimp, and mollusk pathogens proliferate, they create strong growth prospects for molecular diagnostics in farm, hatchery, and reference-lab settings.

Rising focus on farm-level monitoring and One Health risk management

A second opportunity emerges from the convergence of aquaculture health management, food safety, and One Health antimicrobial resistance (AMR) agendas. FAO, WHO, and WOAH (OIE) jointly highlight the contribution of aquaculture to antimicrobial use and the emergence of resistant bacteria, including Vibrio and Aeromonas species with zoonotic potential. At the same time, reviews of global disease impacts emphasize that early detection and targeted control of bacterial pathogens can potentially reduce the estimated US$ 6 billion annual losses to aquaculture and mitigate risks to human health from contaminated seafood. These concerns are driving investment in routine water and stock monitoring, on-site rapid tests, and integrated laboratory services for farms, particularly in high-value finfish, shrimp, and salmon sectors. Diagnostic suppliers that design user-friendly kits for farm personnel, integrate results into digital farm-management platforms, and align assays with regulatory monitoring programs can capture significant new demand.

Category-wise Analysis

Technology Insights

PCR / Molecular diagnostics is the leading segment, accounting for approximately 39% share in 2025. Molecular assays offer unmatched sensitivity and specificity, allowing detection of low levels of pathogens such as Aeromonas, Vibrio, Yersinia, and Streptococcus directly from fish tissues, water, or biofilms without prior culture. Multiplex and quantitative PCR assays have been validated for simultaneous detection of several major fish pathogens, enabling comprehensive surveillance from a single sample and reducing time to decision from days to hours. Building on this evidence, companies such as Thermo Fisher Scientific, Bio-Rad Laboratories, and others supply dedicated real-time PCR food safety and aquaculture pathogen panels, including kits for Vibrio cholerae, Vibrio parahaemolyticus, Vibrio vulnificus, and other key bacteria affecting seafood value chains. These performance advantages and workflow efficiencies explain the strong market share and sustained growth trajectory of molecular diagnostics.

Pathogen Type Insights

By pathogen type, Vibrio is expected to be the leading diagnostic target, representing an estimated 40% share of the Bacterial Diagnostics in Aquaculture market in 2025. Species such as Vibrio anguillarum, Vibrio harveyi, Vibrio parahaemolyticus, and Vibrio vulnificus are widely recognized as major causes of vibriosis in marine and brackish aquaculture systems, affecting more than 50 fish species and numerous shellfish worldwide. These pathogens can cause high mortality, skin ulcerations, internal hemorrhages, and significant economic losses in finfish and shrimp culture, and some strains also pose public health risks through seafood-borne infections or wound exposure in humans. Diagnostics developers have responded with targeted culture media, ELISA kits, and, increasingly, multiplex and real-time PCR assays designed to rapidly detect V. cholerae, V. parahaemolyticus, and V. vulnificus in seafood and environmental samples, making Vibrio testing a central component of aquaculture and seafood safety programs.

End-user Insights

By end-user, aquaculture farms are projected to hold the largest share of around 50% of the bacterial diagnostics in the aquaculture market in 2025, ahead of Diagnostic Laboratories and Research Institutes. Farms are the first line of defense against disease outbreaks and bear the direct economic consequences of bacterial infections, which can account for nearly 24% of disease-related production losses and require significant expenditure on prophylactics and therapeutics. As mortality events in shrimp, tilapia, pangasius, and marine finfish systems have highlighted the value of early detection, more producers are adopting routine water quality checks, on-site rapid tests, and integrated farm-lab diagnostic services. At the same time, specialized veterinary diagnostic laboratories and contract research organizations, often supported by companies such as IDEXX Laboratories, Neogen Corporation, Eurofins Scientific, and others, provide high-complexity molecular and microbiological testing and represent the fastest-growing end user group as health certification and surveillance programs expand.

Regional Insights

North America Bacterial Diagnostics in Aquaculture Market Trends and Insights

North America holds a leading position in the bacterial diagnostics in aquaculture Market due to the region’s well-established aquaculture industry, strong regulatory oversight, and advanced diagnostic infrastructure. The growing need to control bacterial diseases in farmed fish and shellfish has encouraged aquaculture producers to adopt rapid and accurate diagnostic solutions. Increasing awareness regarding aquatic animal health and biosecurity measures has further supported the use of molecular diagnostic technologies such as PCR and other rapid detection methods. Government agencies and research institutions across the United States and Canada are actively promoting disease surveillance programs and monitoring systems to reduce the risk of large-scale disease outbreaks in aquaculture farms. In addition, the presence of leading biotechnology and diagnostic companies in the region supports continuous innovation and availability of advanced testing kits and instruments. Rising investments in aquaculture research, coupled with the growing demand for sustainable seafood production, are also contributing to the widespread adoption of bacterial diagnostic tools. These factors collectively strengthen North America’s leadership in the global market while encouraging the development of more efficient and reliable diagnostic technologies.

Asia Pacific Bacterial Diagnostics in Aquaculture Market Trends and Insights

Asia Pacific is emerging as a rapidly growing region in the bacterial diagnostics in aquaculture market, driven by the strong expansion of aquaculture production and rising concerns over disease outbreaks in farmed aquatic species. Countries such as China, India, Vietnam, Thailand, and Indonesia have large aquaculture industries that produce fish, shrimp, and other seafood on a commercial scale. Frequent bacterial infections in these intensive farming systems have increased the demand for reliable diagnostic solutions to ensure early disease detection and effective farm management. Governments and aquaculture authorities in the region are increasingly promoting disease monitoring programs, biosecurity practices, and the use of advanced diagnostic technologies to improve aquatic animal health. In addition, the growing export demand for high-quality seafood is encouraging producers to adopt better health surveillance systems to meet international safety standards. The expansion of aquaculture research centers and increased collaboration between diagnostic companies and aquaculture farms are also supporting market growth. As a result, the adoption of molecular diagnostics, rapid testing kits, and laboratory-based bacterial detection methods is steadily increasing across the Asia Pacific region.

Competitive Landscape

The bacterial diagnostics in aquaculture market is highly competitive, driven by the presence of global and regional players offering advanced diagnostic solutions for fish and shrimp diseases. Companies compete through technological innovation, product portfolio expansion, and strategic collaborations with aquaculture farms and research institutes. Key focus areas include molecular diagnostics, rapid immunoassays, and culture-based testing solutions that ensure accurate and timely pathogen detection. Firms are also investing in portable and user-friendly devices to cater to on-site farm testing.

Key Developments:

- In 2024, Thermo Fisher introduced a PCR-based diagnostic kit aimed at the rapid detection of bacterial pathogens in aquaculture, with a particular focus on Vibrio species. In 2025, the company intends to broaden its diagnostic offerings by adding more multiplex testing solutions to enable the detection of a wider range of pathogens.

Companies Covered in Bacterial Diagnostics in Aquaculture Market

- Thermo Fisher Scientific

- Bio-Rad Laboratories

- QIAGEN

- Neogen Corporation

- IDEXX Laboratories

- Agilent Technologies

- bioMérieux

- Zoetis

- Merck KGaA

- Eurofins Scientific

- Aquatic Diagnostics Ltd

- Mologic

- Hygiena

- PHARMAQ Analytiq

- WellFish Diagnostics

Frequently Asked Questions

The global Bacterial Diagnostics in Aquaculture market size is expected to reach approximately US$ 4.1 billion in 2026, supported by intensifying aquaculture production, increasing disease-related economic losses, and greater reliance on rapid bacterial detection to safeguard aquatic animal health and seafood value chains.

Key demand drivers include the rising economic burden of aquatic animal diseases estimated at around US$ 6 billion annually alongside rapid intensification of aquaculture, stricter aquatic health and food safety regulations, and the proven advantages of PCR / Molecular Diagnostics and immunoassays for early, accurate detection of pathogens such as Vibrio, Aeromonas, and Streptococcus.

North America currently leads the Bacterial Diagnostics in Aquaculture market, with roughly 39% share in 2025, reflecting its high-value salmon and shellfish sectors, robust regulatory oversight of seafood safety and aquatic health, and concentration of major diagnostics companies offering advanced laboratory and on‑site bacterial testing solutions.

The most significant opportunity lies in expanding affordable, user-friendly bacterial diagnostics across rapidly growing aquaculture hubs in the Asia Pacific, where disease and environment-related problems can cause annual losses exceeding US$ 3 billion, and where scaling molecular and rapid tests can materially reduce mortality, improve biosecurity, and support One Health objectives.

Key players include Thermo Fisher Scientific, Bio Rad Laboratories, QIAGEN, Neogen Corporation, IDEXX Laboratories, Agilent Technologies, bioMérieux, Zoetis, Merck KGaA, Eurofins Scientific, Aquatic Diagnostics Ltd, and Mologic, which collectively provide a wide portfolio of culture-based, immunoassay, and PCR / Molecular Diagnostic solutions tailored to aquaculture and seafood safety applications.