- Biotechnology

- Guillain-Barre Syndrome Diagnostics Market

Guillain-Barre Syndrome Diagnostics Market Size, Share, and Growth Forecast, 2026 - 2033

Guillain-Barre Syndrome Diagnostics Market by Diagnostic Test (Lumbar Puncture, Nerve Conduction, Other), Syndrome Type (Acute Inflammatory Demyelinating Polyneuropathy (AIDP), Others), End-user (Hospitals and Clinics, Diagnostic Laboratories, Others), and Regional Analysis for 2026 - 2033

Guillain-Barre Syndrome Diagnostics Market Share and Trends Analysis

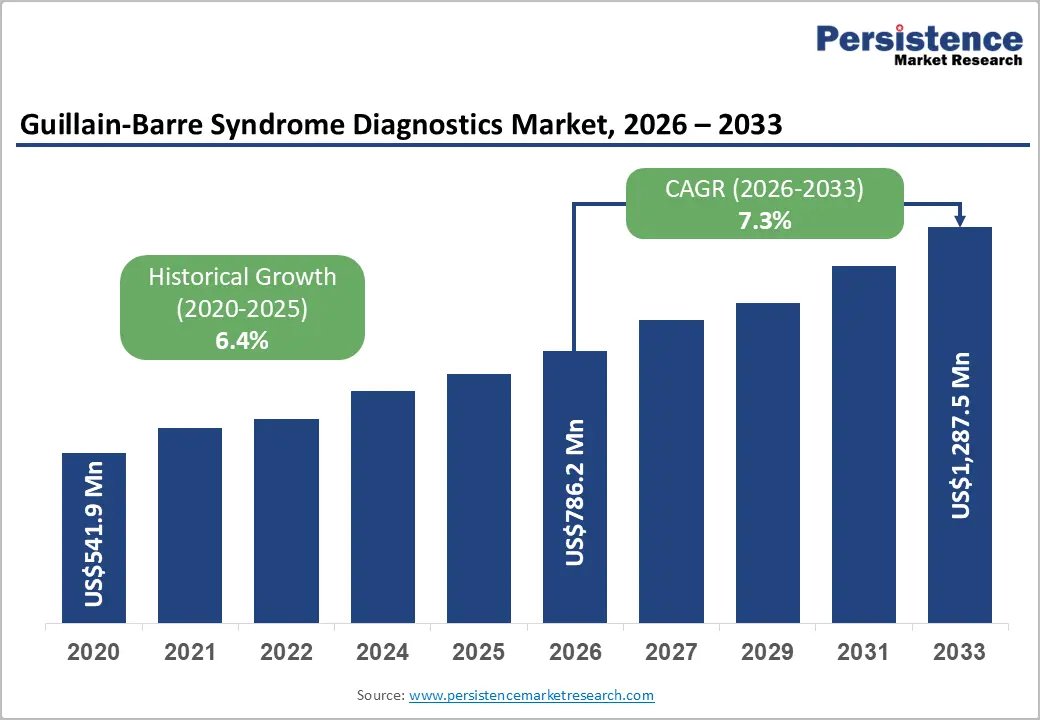

The global guillain-barre syndrome diagnostics market size is likely to be valued at US$786.2 million in 2026 and is estimated to reach US$1,287.5 million by 2033, growing at a CAGR of 7.3% during the forecast period from 2026 to 2033, driven by the rising burden of neurological disorders, increased clinical awareness, and wider access to neurodiagnostic infrastructure across emerging and developed healthcare systems.

Growth is reinforced by demographic aging, higher incidence of autoimmune neuropathies, and expansion of hospital-based diagnostic pathways. Regulatory emphasis on early disease detection and standardized neurological testing protocols is increasing adoption. Technology adoption in nerve conduction systems, molecular testing, and electromyography platforms is improving diagnostic precision.

Key Industry Highlights:

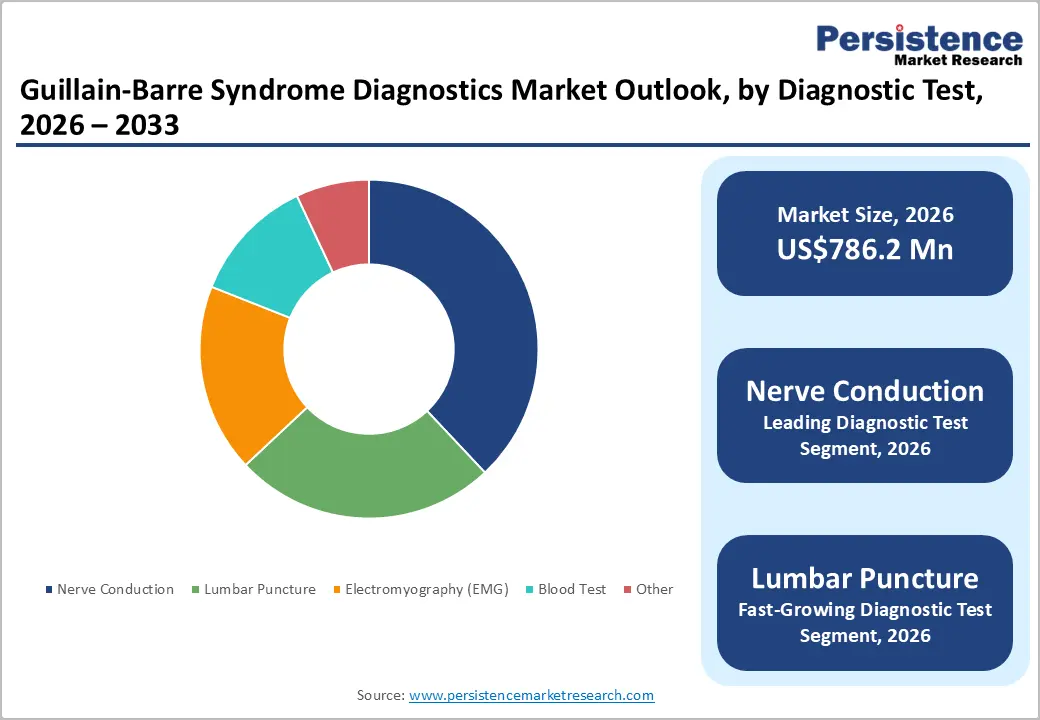

- Leading Diagnostic Test: Nerve conduction study is set to hold approximately 38% revenue share in 2026, driven by its clinical primacy as the first-line electrodiagnostic tool for GBS subtype differentiation in standard hospital neurology protocols.

- Fastest-Growing Diagnostic Test: Lumbar puncture (CSF Analysis) is projected as the fastest-growing segment, supported by the emergence of validated NfL protein biomarker assays enabling simultaneous GBS subtype confirmation and differential diagnosis exclusion.

- Leading End-user: Hospitals and clinics are estimated to hold approximately 47% revenue share in 2026, due to the concentration of multidisciplinary neurology teams and integrated GBS diagnostic pathway protocols within institutional settings.

- Fastest-Growing End-user: Diagnostic laboratories are forecast to record the fastest growth, driven by the outsourcing of specialized neurodiagnostic testing.

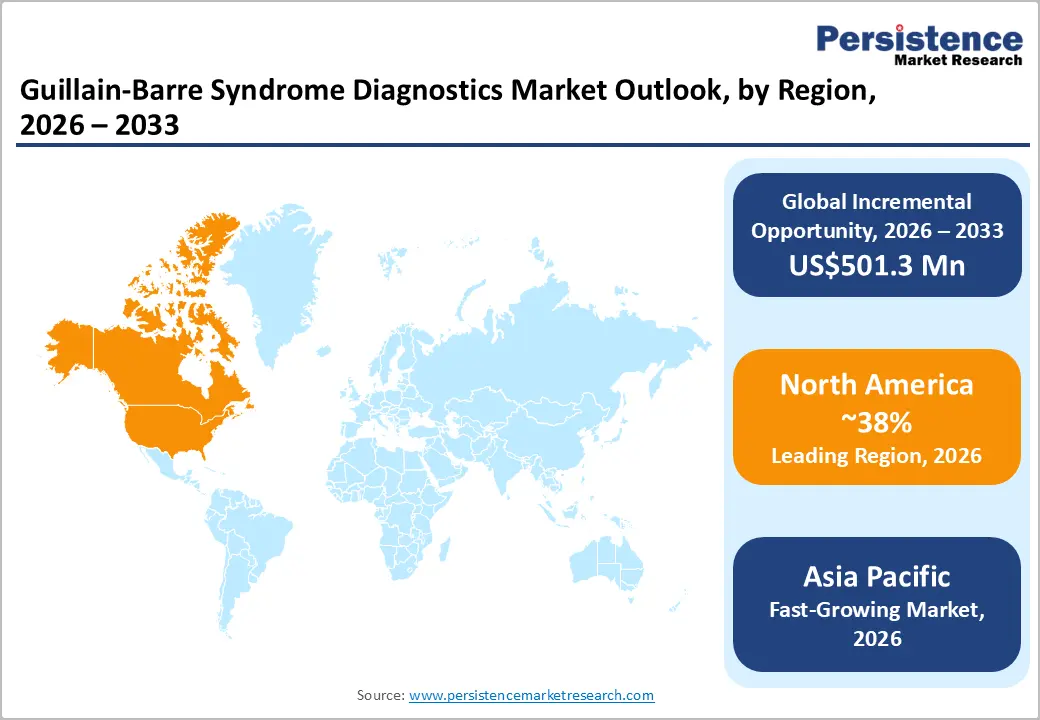

- Regional Leadership: North America is projected to capture roughly 38% of the market share by 2026, while the U.S. is anticipated to capture 82% of the regional segment, driven by extensive healthcare infrastructure automation.

- Competitive Environment: The market is moderately fragmented, with Natus Medical, Siemens Healthineers, and Nihon Kohden Corporation among the leading players, competing across electrophysiology platforms, CSF analysis systems, and AI-integrated diagnostic software.

- Key Opportunity: AI integration in electrodiagnostic platforms holds the highest near-term growth potential, accounting for an estimated 15-20% premium pricing uplift for AI-enabled devices, driven by the urgent need to reduce specialist dependency in fast-growing Asia Pacific markets.

DRO Analysis

Driver - Rising Burden of Autoimmune Neurological Disorders

Increased incidence of immune-mediated neuropathies is strengthening diagnostic demand across acute care systems. Guillain-Barre syndrome requires rapid confirmation through electrophysiological and cerebrospinal fluid testing. Expansion of neurology departments in tertiary hospitals is improving early case identification rates.

A 2025 surveillance update from national health authorities in India reported a measurable rise in acute flaccid paralysis investigations linked to post-infectious neuropathic conditions. This rise in diagnostic investigations is accelerating the adoption of nerve conduction and lumbar puncture testing frameworks across hospitals.

Restraint - Prohibitive Capital Equipment Costs and Specialized Technical Infrastructure Requirements

The high acquisition cost of advanced electrodiagnostic systems restricts the adoption within resource-constrained medical facilities. Specialized neurophysiology equipment requires significant capital expenditure, lowering profit margins for small-scale diagnostic laboratories operating under fixed reimbursement caps. This economic barrier limits the availability of comprehensive testing matrices outside metropolitan healthcare ecosystems, directly hindering market scalability.

These specialized instruments demand continuous calibration and technical oversight by certified clinical neurophysiologists. The lack of standardized training infrastructure in developing healthcare models creates operational bottlenecks, as uncalibrated systems yield high rates of false negatives. Regional diagnostic deficits persist, lowering overall diagnostic testing volumes and delaying therapeutic intervention schemas.

Opportunity - Expansion of Point-of-Care and Portable Diagnostic Technologies

The development and commercialization of portable nerve conduction study devices and point-of-care Cerebrospinal Fluid (CSF) biomarker assays present a structurally significant growth pathway for the Guillain-Barré Syndrome (GBS) diagnostics market. Compact, battery-operated electrodiagnostic tools that function without permanent laboratory infrastructure enable diagnostic capability deployment in community hospitals, rural neurology outposts, and emergency medicine settings previously outside the reach of traditional GBS workup protocols.

The U.S. National Institutes of Health (NIH) and European research consortia have funded biomarker discovery programs specifically targeting GBS-associated neurofilament light chain (NfL) proteins that are detectable via lateral flow assay platforms, enabling near-patient testing. If validated and cleared by regulatory authorities, these assay formats could substantially reduce diagnostic delays in underserved markets while expanding addressable patient volumes for diagnostic tool manufacturers operating in decentralized care models.

Category-wise Analysis

Diagnostic Test Insights

Nerve conduction study (NCS) is expected to lead the Guillain-Barré syndrome diagnostics market, accounting for approximately 38% of the revenue share in 2026. The clinical primacy of NCS in differentiating demyelinating from axonal GBS subtypes makes it the first-line electrodiagnostic tool in most hospital neurology protocols. Standardized electrodiagnostic pathways across tertiary care settings reinforce early case stratification, supporting timely therapeutic intervention and prognostic assessment.

Lumbar puncture is likely to represent the fastest-growing segment, propelled by expanding CSF biomarker panels that enable simultaneous GBS subtype confirmation and differential diagnosis exclusion. The emergence of validated NfL protein assay kits from companies such as Quanterix has accelerated adoption in high-complexity diagnostic laboratories. Expanded cerebrospinal fluid biomarker utilization enhances diagnostic precision across acute neuropathy evaluation, supporting improved subtype resolution and earlier exclusion of alternative inflammatory or infectious etiologies.

Syndrome Type Insights

Acute inflammatory demyelinating polyneuropathy (AIDP) is projected to lead the market, capturing around 62% of the revenue share in 2026. AIDP constitutes the predominant GBS variant in Western clinical populations, driving the bulk of nerve conduction study and CSF diagnostic procedure volumes. The Erasmus GBS Classification Tool, widely deployed in European neurology centers, specifically prioritizes AIDP diagnostic criteria, reinforcing clinical infrastructure investment toward this subtype.

Acute motor axonal neuropathy (AMAN) is likely to be the fastest-growing segment, fueled by rising incidence documentation in East and South Asian populations where AMAN prevalence exceeds Western demographic baselines. Expanding electrodiagnostic infrastructure in China and India is enabling clinicians to differentiate AMAN from AIDP more precisely.

End-user Insights

Hospitals and clinics are likely to be the leading segment with a projected 47% of the Guillain-Barré syndrome diagnostics market share in 2026. Specialized nerve conduction studies allow clinicians to measure the precise velocity of electrical impulses across peripheral nerves to confirm demyelination. A major healthcare network integrated automated electromyography systems to expedite critical neurological assessments. This structural adoption ensures sustained volume growth across diagnostic facilities.

Diagnostic laboratories are anticipated to be the fastest-growing segment, fueled by the outsourcing of specialized neurodiagnostic testing. Growth is supported by rising demand for centralized high-precision testing services. Examples include independent laboratories expanding electromyography partnerships with hospital networks. Increased referral-based testing improves utilization rates of advanced diagnostic platforms.

Regional Insights

North America Guillain-Barre Syndrome Diagnostics Market Trends

North America is anticipated to be the leading region, accounting for a market share of 38% in 2026, driven by a high concentration of advanced neurological care centers, established reimbursement frameworks, and widespread adoption of automated diagnostic technologies. The presence of key biotechnology industry participants facilitates rapid commercialization of novel serological assays.

U.S. Guillain-Barre Syndrome Diagnostics Market Insights

The U.S. is projected to capture a market share of 82% within the regional market in 2026, driven by rising investment in digital neurophysiology infrastructure across large hospital networks. Regulatory clearances from the Food and Drug Administration for multiplex autoantibody panels accelerate clinical deployment. Increased domestic incidence of post-bacterial autoimmune complications drives continuous utilization of high-complexity laboratory testing.

Canada Guillain-Barre Syndrome Diagnostics Market Insights

Canada is expected to account for a market share of 18% within the regional ecosystem in 2026, with steady growth stimulated by provincial healthcare investments aimed at upgrading rural diagnostic laboratory capabilities. Public health initiatives focus on standardizing neuromuscular evaluation protocols to reduce regional disparities in critical care access.

Europe Guillain-Barre Syndrome Diagnostics Market Trends

Europe is anticipated to be a major revenue contributor, accounting for a market share of 31% in 2026, supported by highly integrated public healthcare systems and rigid clinical guidelines recommending early electrodiagnostic intervention. Universal reimbursement policies for specialized cerebrospinal fluid analyses support stable testing volumes across public hospitals.

Germany Guillain-Barre Syndrome Diagnostics Market Insights

Germany is forecast to command a market share of 24% within the European sector in 2026, resulting in significant revenue contribution due to a high concentration of specialized medical instrumentation manufacturers. Cleanroom expansions and automated assay production lines within domestic biotechnology hubs lower localized procurement costs.

U.K. Guillain-Barre Syndrome Diagnostics Market Insights

The U.K. is likely to represent a market share of 19% within the European domain in 2026, driven by National Health Service procurement frameworks favoring consolidated diagnostic testing matrices. Centralized laboratory models optimize sample processing efficiency for rare autoantibody profiles, lowering per-test operational costs.

Asia Pacific Guillain-Barre Syndrome Diagnostics Market Trends

Asia Pacific is forecast to be the fastest-growing market, stimulated by rapid healthcare infrastructure modernization, expanding healthcare expenditure, and rising clinical awareness across developing economies. Government-led rural healthcare initiatives expand the reach of basic neurodiagnostic services into previously underserved geographic zones. The growing establishment of specialized neurology clinics increases the regional capacity for nerve conduction testing.

China Guillain-Barre Syndrome Diagnostics Market Insights

China is expected to achieve a dominant regional market share of 41% in 2026, driven by domestic production of cost-effective electrodiagnostic machinery. Rising healthcare access under national insurance schemes increases the volume of patients receiving definitive neurological assessments. Large-scale hospital expansions in tier-two and tier-three cities create sustained demand for foundational neurodiagnostic laboratory installations.

India Guillain-Barre Syndrome Diagnostics Market Insights

India is anticipated to record a market share of 22% within the regional framework in 2026, expanding rapidly due to rising private investments in multi-specialty tertiary care networks. Increased clinical focus on tracking post-infectious neurological syndromes drives the adoption of advanced serological testing panels in urban diagnostic centers. Medical tourism expansion further stimulates the procurement of international-standard neurodiagnostic equipment.

Competitive Landscape

The global Guillain-Barré syndrome diagnostics market is moderately fragmented, characterized by the coexistence of large multinational medical device and diagnostics corporations alongside specialized neurophysiology equipment manufacturers. Leading players, including Natus Medical (Natus Neurology), Siemens Healthineers, Nihon Kohden Corporation, Cadwell Industries, and Bio-Techne Corporation, collectively hold significant revenue share through diversified product portfolios spanning electrophysiology platforms, CSF analysis systems, and serology testing kits.

The moderate fragmentation reflects the multi-modality nature of GBS diagnostics, where no single technology platform covers the full diagnostic workup. This creates competitive space for specialized reagent and assay developers alongside hardware platform leaders. Competitive differentiation is increasingly driven by software integration, AI-assisted interpretation, and service contract bundling rather than hardware specification alone, reshaping competitive dynamics in favor of companies with strong digital health and data analytics capabilities.

Key Industry Developments:

- In January 2026, a Pune hospital launched a dedicated Guillain-Barre Syndrome clinic to strengthen neurological care and improve early diagnosis and coordinated management of patients with acute neuropathic conditions.

Companies Covered in Guillain-Barre Syndrome Diagnostics Market

- Natus Medical

- Siemens Healthineers

- Nihon Kohden Corporation

- Cadwell Industries

- Bio-Techne Corporation

- Quanterix Corporation

- Neusoft Medical Systems

- Roper Technologies (Verathon)

- Abbott Laboratories

- Thermo Fisher Scientific

- Bio-Rad Laboratories

- Beckman Coulter (Danaher)

- EUROIMMUN AG (PerkinElmer)

- Medtronic plc

- Compumedics Limited

Frequently Asked Questions

The global Guillain-Barre syndrome diagnostics market is projected to reach US$786.2 million in 2026.

Rising incidence of autoimmune neuropathies, expansion of neurodiagnostic infrastructure, and increased adoption of electrophysiology and cerebrospinal fluid testing drive the Guillain-Barre syndrome diagnostics market.

The Guillain-Barre syndrome diagnostics market is poised to witness a CAGR of 7.3% from 2026 to 2033.

Integration of automated neurodiagnostic systems, expansion of decentralized testing access, and adoption of biomarker-based cerebrospinal fluid assays create key growth opportunities in the Guillain-Barre syndrome diagnostics market.

Some The key market players include Natus Medical (Natus Neurology), Siemens Healthineers, Nihon Kohden Corporation, Cadwell Industries, and Bio-Techne Corporation.