- Inks, Coatings, Adhesives & Sealants (ICAS)

- Organic Pigments Market

Organic Pigments Market Size, Share, and Growth Forecast 2026 - 2033

Organic Pigments Market by Source (Synthetic, Natural), Product Type (Azo, Phthalocyanine, HPPs, Others), Application (Paints and Coatings, Inks, Plastics, Others), and Regional Analysis, 2026 - 2033

Organic Pigments Market Size and Trend Analysis

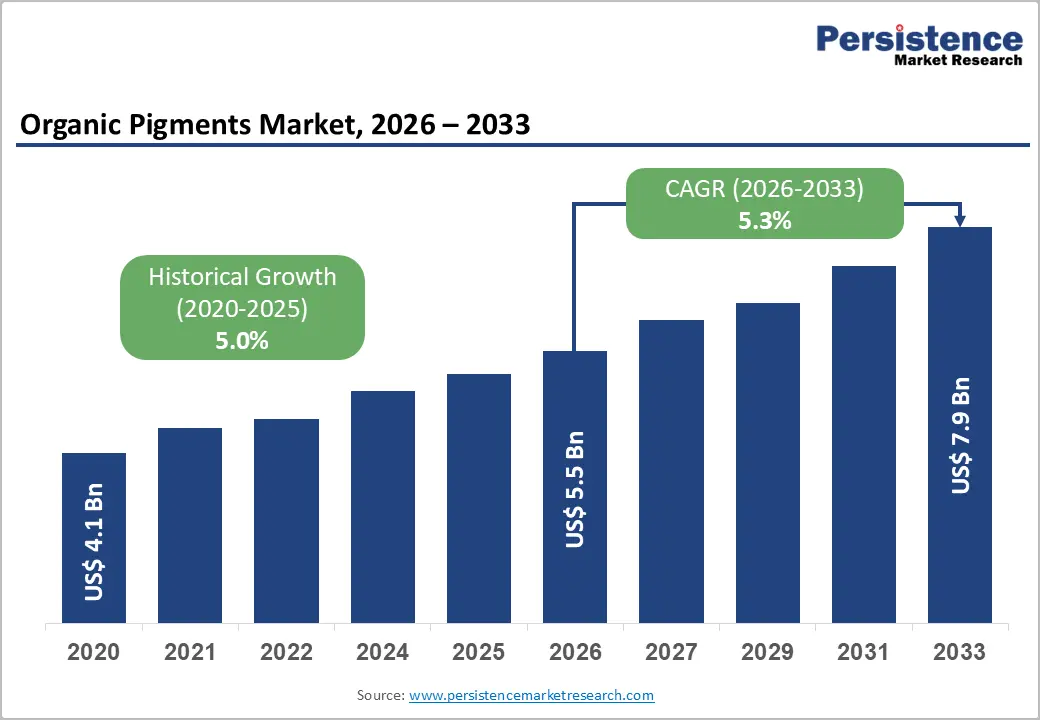

The global organic pigments market size is expected to be valued at US$ 5.9 billion in 2026 and projected to reach US$ 8.6 billion by 2033, growing at a CAGR of 5.5% between 2026 and 2033.

Organic pigments' superior colour strength, transparency, and regulatory compliance credentials versus inorganic alternatives make them the preferred colorant choice across increasingly stringent application environments. The European Chemicals Agency (ECHA) and U.S. Environmental Protection Agency (EPA) regulations restricting heavy metal-based inorganic pigments are further redirecting formulator demand toward high-performance organic pigment solutions, reinforcing the market's structural growth outlook across Asia Pacific, North America, and Europe.

Key Industry Highlights

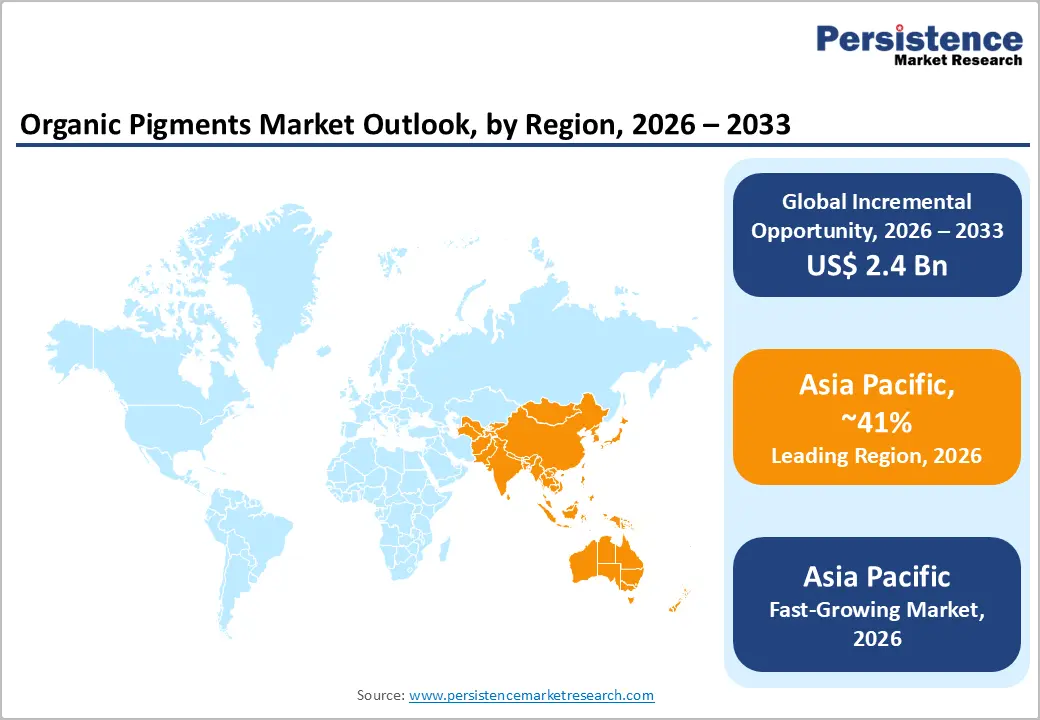

- Leading Region: Asia Pacific dominates the global Organic Pigments market with approximately 60% revenue share in 2026, anchored by China's position as the world's largest pigment producer, accounting for over 40% of global volumes, and India's rapidly growing export-oriented pigment manufacturing sector.

- Fastest Growing Region: Middle East & Africa is the fastest-growing organic pigments regional market, driven by Saudi Arabia's Vision 2030 construction investment surge exceeding US$ 1 trillion), rapid urbanisation, and expanding domestic manufacturing capacity across GCC nations and major African economies.

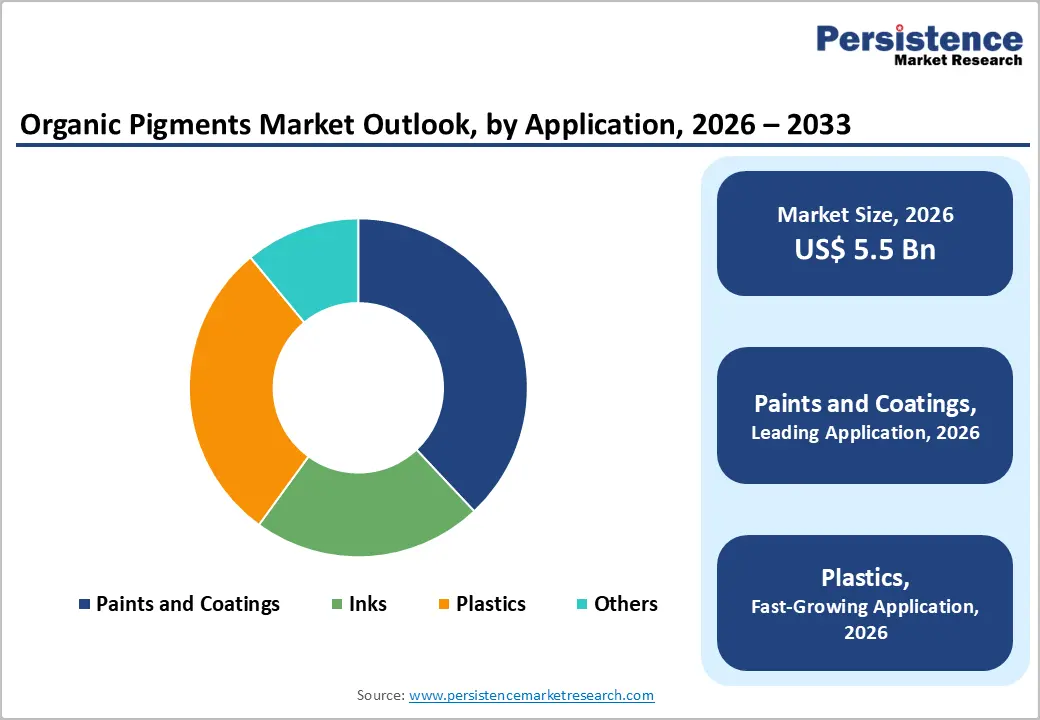

- Dominant Segment: Paints and Coatings is the leading application segment with approximately 36% global market share in 2026, driven by global construction activity, automotive OEM coatings demand, and regulatory-driven substitution of heavy metal inorganic pigments with high-performance organic colorants.

- Fastest Growing Segment: Plastics is the fastest-growing application at a projected CAGR of approximately 7%), fueled by growing demand for coloured flexible packaging, electric vehicle interior components, and consumer electronics housings requiring heat-stable, migration-resistant high-performance organic pigments.

- Key Opportunity: Significant revenue opportunities exist in MEA market penetration aligned with Vision 2030 infrastructure investment, and in bio-based and sustainable organic pigment R&D meeting EU Green Deal and REACH clean-chemistry mandates across coatings, inks, and packaging applications.

DRO Analysis

Drivers - Expanding Paints and Coatings Industry Fueled by Global Construction Boom

The paints and coatings industry, the largest end-use sector for organic pigments, is experiencing robust growth globally, driven by unprecedented levels of residential, commercial, and infrastructure construction activity, particularly across the Asia Pacific and the Middle East. The Global Construction Perspectives and Oxford Economics research forecasts global construction output to reach US$ 15.5 trillion by 2030, creating sustained demand for architectural coating.

Simultaneously, the automotive coatings segment is expanding, with the International Organization of Motor Vehicle Manufacturers (OICA) reporting global vehicle production recovering to over 93 million units in 2023. Organic pigments, particularly phthalocyanine blues and greens and high-performance HPP pigments, are specified in automotive OEM and refinish coatings for their superior heat stability, lightfastness, and gloss retention, ensuring consistent institutional demand from major coatings manufacturers, including PPG Industries, AkzoNobel, and Sherwin-Williams.

Regulatory Restrictions on Heavy Metal and Inorganic Pigments Driving Organic Substitution

Tightening global regulatory frameworks governing hazardous substances in colorant formulations is creating a sustained substitution tailwind for organic pigments. The EU's REACH Regulation and the RoHS Directive impose strict restrictions on lead chromate, cadmium, and other heavy metal-based inorganic pigments widely used in industrial and decorative coatings, compelling formulators to qualify organic pigment alternatives.

In the United States), the EPA has progressively tightened standards on cadmium and lead pigment use under TSCA. The Society of Dyers and Colourists (SDC) estimates that organic pigments now account for approximately 25-30% of global pigment volumes but over 50% of value, reflecting their premium positioning driven by both performance attributes and regulatory necessity across coatings, inks, and plastics applications.

Restraints - Volatile Raw Material Prices and Petrochemical Feedstock Dependence

Synthetic organic pigments are predominantly derived from aromatic amines and petrochemical feedstocks, including benzene, toluene, and naphthalene, whose prices exhibit significant volatility linked to crude oil market fluctuations. The International Energy Agency (IEA) reported crude oil price swings of over 60% between 2020 and 2023, directly impacting organic pigment manufacturing economics and compressing margins across the value chain.

This feedstock price volatility makes long-term contract pricing difficult, creates margin pressure for pigment producers, and may incentivize end-use formulators to seek lower-cost inorganic alternatives during periods of high feedstock costs.

Environmental and Wastewater Compliance Costs in Manufacturing

Organic pigment synthesis, particularly for azo and phthalocyanine classes, involves multi-step chemical processes that generate aromatic amine intermediates and heavy metal catalyst residues requiring sophisticated wastewater treatment and industrial effluent management. Compliance with EU Industrial Emissions Directive (IED), India's Environment Protection Act, and China's Water Pollution Prevention and Control Law imposes significant capital and operational expenditure on pigment manufacturers. Smaller producers, particularly in India and China, face disproportionate compliance burdens, which can limit capacity expansion and suppress competitive pricing, ultimately constraining market volume growth in cost-sensitive application segments.

Opportunities - High-Growth Plastics Segment - Fastest Growing Application at 7% CAGR

The plastics application segment is the fastest-growing end-use market for organic pigments, projected to expand at a CAGR of approximately 7% between 2026 and 2033. Surging demand for colored plastics in packaging, consumer electronics, automotive interior components, and construction materials is driving robust organic pigment offtake. The global flexible packaging market, a major organic pigment consumer, is growing at over 4% annually according to the Flexible Packaging Association (FPA), while the boom in colored polymer applications for electric vehicle (EV) interiors and lightweight components is opening premium HPP pigment demand.

The European Plastics Converters (EuPC) reports that color is the most frequently cited attributes driving plastic material specification decisions in consumer-facing applications, reinforcing the structural demand foundation for high-performance organic pigments in the plastics industry.

Middle East & Africa - Fastest Growing Regional Market

The Middle East & Africa (MEA) region represents the fastest-growing market for organic pigments, driven by an unprecedented infrastructure investment wave, rapid urbanization, and the expansion of domestic manufacturing capacity across Gulf Cooperation Council (GCC) states and major African economies. Saudi Arabia's Vision 2030 programme, which earmarks over US$ 1 trillion in construction and industrial investment, is creating structural demand for architectural coatings, construction materials, and packaging, all of which are significant organic pigment consumers.

The African Development Bank identifies manufacturing sector expansion, particularly in Nigeria), Ethiopia and South Africa, as a priority investment area, further broaden the MEA organic pigment addressable market. Producers, including BASF SE, and Sudarshan Chemical Industries, are investing in distribution network expansion and regional technical service capabilities to capitalize on this high-growth frontier market.

Category-wise Analysis

Application Insights

Paints and coatings is the dominant application segment for organic pigments, accounting for approximately 36% of the total global market share in 2026. This leadership position is underpinned by the paints and coatings industry's status as the largest and most technically demanding consumer of high-performance organic colorants. Architectural coatings require pigments with exceptional lightfastness, alkali resistance, and weather durability, performance attributes uniquely offered by phthalocyanine, azo, and HPP organic pigment classes.

The American Coatings Association (ACA) reports that the U.S. coatings industry shipments exceeded US$ 30 billion in 2023, with architectural coatings representing the largest sub-segment. Industrial coatings for automotive, marine, and protective applications additionally drive significant organic pigment consumption. The plastics segment is the fastest-growing application at a CAGR of approximately 7%, driven by packaging, electronics, and EV component coloration demand.

Product Type Insights

Azo pigments dominate the global Organic Pigments market by product type, accounting for approximately 55% of total market volume in 2026. Azo pigments, characterized by their nitrogen-nitrogen double bond (-N=N-) chromophore, represent the largest and most commercially diverse class of organic colorants, encompassing monoazo, diazo, and condensed azo varieties spanning the full visible color spectrum.

Their dominance reflects their cost competitiveness relative to HPPs, established large-scale manufacturing infrastructure, and broad application compatibility across inks, paints, plastics, and textiles. BASF SE), DIC Corporation, and Sudarshan Chemical Industries are leading azo pigment producers. Phthalocyanine pigments, particularly Pigment Blue 15 and Pigment Green 7, represent the second-largest segment, valued for their outstanding lightfastness and heat stability in demanding industrial applications.

Source Analysis

Synthetic organic pigments represent the overwhelmingly dominant source category, accounting for approximately 92% of total market revenue in 2026. The supremacy of synthetic pigments reflects their unmatched color consistency, high tinctorial strength, scalable industrial production, and ability to be precisely engineered to meet specific performance specifications, including lightfastness, heat resistance, migration fastness, and transparency, that are critical in professional coatings, inks, and plastics applications.

Leading synthetic organic pigment producers maintain extensive intellectual property portfolios around crystal form stabilization and surface treatment technologies that differentiate product performance. The natural pigment segment, while small in volume, is the fastest-growing source category, driven by clean-label and bio-based sustainability mandates in cosmetics, food contact packaging, and natural textile dyeing applications.

Regional Insights

North America Organic Pigments Market Trends and Insights

North America represents a mature but steadily growing organic pigments market, characterized by strong demand from high-value coatings, specialty inks, and engineering plastics sectors. Regulatory drivers, particularly EPA restrictions on heavy metal pigments and TSCA compliance requirements, are systematically redirecting formulator demand toward high-performance organic alternatives. Growing investment in sustainable packaging and waterborne coating reformulations are additional demand tailwinds for premium organic pigment grades.

U.S. Organic Pigments Market Size

The U.S. accounts for approximately 78-80% of North American organic pigment revenues, driven by its large coatings industry, with shipments exceeding US$ 30 billion annually per the American Coatings Association, and a sophisticated printing inks sector. Strong demand from automotive OEMs and refinish coatings, flexible packaging inks, and engineering polymer applications sustains consistent premium organic pigment consumption from producers, including Sun Chemical and Vibrantz.

Europe Organic Pigments Market Trends and Insights

Europe is a high-value organic pigments market shaped by stringent REACH and RoHS chemical regulations that drive substitution of hazardous inorganic pigments with organic alternatives. The region's strong automotive coatings, specialty printing inks, and high-performance plastics industries create consistent demand for premium HPP and phthalocyanine grades. Sustainability-driven reformulation toward waterborne and UV-cure systems is further expanding the technical specification of organic pigments.

Germany Organic Pigments Market Size

Germany is the largest European organic pigments market, accounting for approximately 22-24% of regional revenues. Germany's world-class automotive industry, producing over 4 million vehicles annually according to the Verband der Automobilindustrie (VDA), creates extensive demand for premium automotive coating pigments, while its chemical and plastics manufacturing sectors provide additional offtake. BASF SE and Lanxess AG, both headquartered in Germany, maintain strong domestic market presence.

U.K. Organic Pigments Market Size

The U.K. accounts for approximately 11-13% of European organic pigment revenues. According to the British Printing Industries Federation (BPIF), the British printing and packaging industry is the fourth largest in Europe which is a key organic pigment consumer, particularly for high-brightness azo and phthalocyanine pigments in specialty inks. Post-Brexit regulatory alignment with UK REACH requirements continues to shape chemical compliance investment among domestic pigment distributors and formulators.

France Organic Pigments Market Size

France contributes approximately 10-12% of European organic pigment market revenues, driven by its automotive coatings, luxury goods packaging, and cosmetics sectors. The French cosmetics industry, valued at over €14 billion according to the Fédération des Entreprises de la Beauté (FEBEA), is an important niche market for cosmetic-grade organic pigments, particularly for high-purity lake pigments in makeup and personal care formulations compliant with EU Cosmetics Regulation 1223/2009.

Asia Pacific Organic Pigments Market Trends and Insights

Asia Pacific dominates the global Organic Pigments market with approximately 60% of total revenue share in 2026), anchored by the region's status as the world's manufacturing hub for coatings, inks, plastics, and textiles. China accounts for the largest share of both organic pigment production and consumption globally, the China Dyestuff Industry Association (CDIA) estimates China produces over 40% of global organic pigment volumes, with major producers concentrated in Zhejiang) and Jiangsu provinces. India is the second-largest production hub, with companies including Sudarshan Chemical) and Kiri Industries competing globally.

India Organic Pigments Market Size

India is the world's second-largest organic pigment producer and a fast-growing domestic consumer, accounting for approximately 14-16% of Asia Pacific regional revenues. India's pigment exports, valued at over US$ 900 million annually according to CHEMEXCIL (the Basic Chemicals, Cosmetics & Dyes Export Promotion Council), reflect strong global competitiveness. Domestic demand is expanding from the rapidly growing Indian construction, automotive, and flexible packaging sectors, with the Ministry of Housing and Urban Affairs overseeing large-scale infrastructure programmes driving architectural coatings consumption.

Japan Organic Pigments Market Size

Japan accounts for approximately 10% of Asia Pacific organic pigment revenues, characterized by strong demand for ultra-high-performance pigments in automotive coatings, electronics, and specialty printing inks. DIC Corporation), one of the world's largest organic pigment and printing ink producers, maintains global leadership from its Japanese headquarters. Japan's sophisticated automotive and electronics industries set exacting pigment performance standards, creating a premium niche for high-value HPP and phthalocyanine grades.

Southeast Asia Organic Pigments Market Size

Southeast Asia is a growing organic pigment market, contributing approximately 6-8% of Asia Pacific revenues and expanding rapidly on the back of manufacturing sector growth in Vietnam), Thailand), Indonesia), and Malaysia). The region's expanding textiles, packaging, and automotive assembly industries create consistent demand for decorative and functional organic pigments. FDI-driven manufacturing relocation from China is further stimulating pigment consumption growth across the sub-region.

Competitive Landscape

The global organic pigments market is moderately consolidated, with multinational leaders BASF SE, DIC Corporation, Sun Chemical, and Heubach Group commanding significant revenue share through broad product portfolios, global manufacturing networks, and deep technical service relationships with major coating and inks companies. Indian producers, notably Sudarshan Chemical Industries, Kiri Industries, and Meghmani Organics, compete aggressively on cost and volume in azo and phthalocyanine grades.

Strategic priorities include sustainability certifications, bio-based pigment R&D, M&A consolidation (exemplified by Heubach's acquisition of Clariant's pigment business), and geographic expansion in MEA and Latin America.

Key Developments

- In March 2025, Sudarshan Chemical Industries announced a capacity expansion investment of INR 500 crore at its Roha manufacturing facility to scale high-performance pigment production for automotive coatings and plastics applications, targeting European and North American export markets.

- In October 2024, BASF SE launched a new range of bio-based organic pigment dispersions developed under its sustainability programme, targeting waterborne architectural coatings and packaging ink formulators seeking lower-carbon colorant solutions compliant with EU Green Deal objectives.

- In June 2023, Heubach Group completed the integration of Clariant's pigment business acquired in 2023, creating one of the world's largest dedicated organic pigment producers with combined revenues exceeding EUR 1 billion and operations across 20+ countries.

Organic Pigments Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 4.4 Billion |

| Current Market Value (2026) | US$ 5.9 Billion |

| Projected Market Value (2033) | US$ 8.6 Billion |

| CAGR (2026 - 2033) | 5.5% |

| Leading Region | Asia Pacific, 60% market share (2026) |

| Dominant Category (Application) | Paints and Coatings, 36% market share (2026) |

| Top-ranking Category (Product Type) | Azo Pigments, 55% market share (2026) |

| Incremental Opportunity | US$ 2.7 Billion (2026 - 2033) |

Companies Covered in Organic Pigments Market

- Clariant AG

- BASF SE

- DIC Corporation

- Sudarshan Chemical Industries Ltd.

- Atul Ltd.

- Huntsman Corporation

- Kronos Worldwide Inc.

- Lanxess AG

- Kiri Industries Ltd.

- Vibrantz

- Heubach Group

- Sun Chemical

- Meghmani Organics Ltd.

- Vipul Organics Ltd.

- Navpad Pigments Pvt. Ltd.

Frequently Asked Questions

The global organic pigments market is estimated to be valued at US$ 5.9 billion in 2026, growing from US$ 4.4 billion in 2020 at a historical CAGR of 5.1%. The market is projected to reach US$ 8.6 billion by 2033.

The primary demand drivers include global construction and automotive production growth stimulating paints and coatings demand, regulatory restrictions on hazardous inorganic pigments under EU REACH), RoHS), and U.S. TSCA compelling organic pigment substitution, and accelerating demand from the plastics sector for heat-stable, migration-resistant organic colorants in packaging, electric vehicle components, and consumer electronics applications.

Asia Pacific leads with approximately 60% of global Organic Pigments market share in 2026). China accounts for over 40% of global organic pigment production volumes per the China Dyestuff Industry Association), while India, the second-largest producer, generates over US$ 900 million in annual pigment exports through industry leaders including Sudarshan Chemical Industries and Kiri Industries.

The near-term growth opportunities are in the plastics application segment is driven by packaging, EV, and electronics demand, and in the Middle East & Africa regional market.

The leading companies include BASF SE), DIC Corporation), Heubach Group), Sun Chemical), Sudarshan Chemical Industries Ltd.), Lanxess AG), Kiri Industries Ltd.), Vibrantz), Meghmani Organics Ltd.), and Huntsman Corporation).