- Beauty & Personal Care

- Organic Deodorant Market

Organic Deodorant Market Size, Share, and Growth Forecast 2026 - 2033

Organic Deodorant Market by Product Type (Stick Deodorants, Roll-on Deodorants, Spray Deodorants, Balm Deodorants), Fragrance Type (Floral, Citrus, Herbal, Woody), End-user (Men, Women), Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Pharmacies, Online), and Regional Analysis, 2026 - 2033

Organic Deodorant Market Size and Trend Analysis

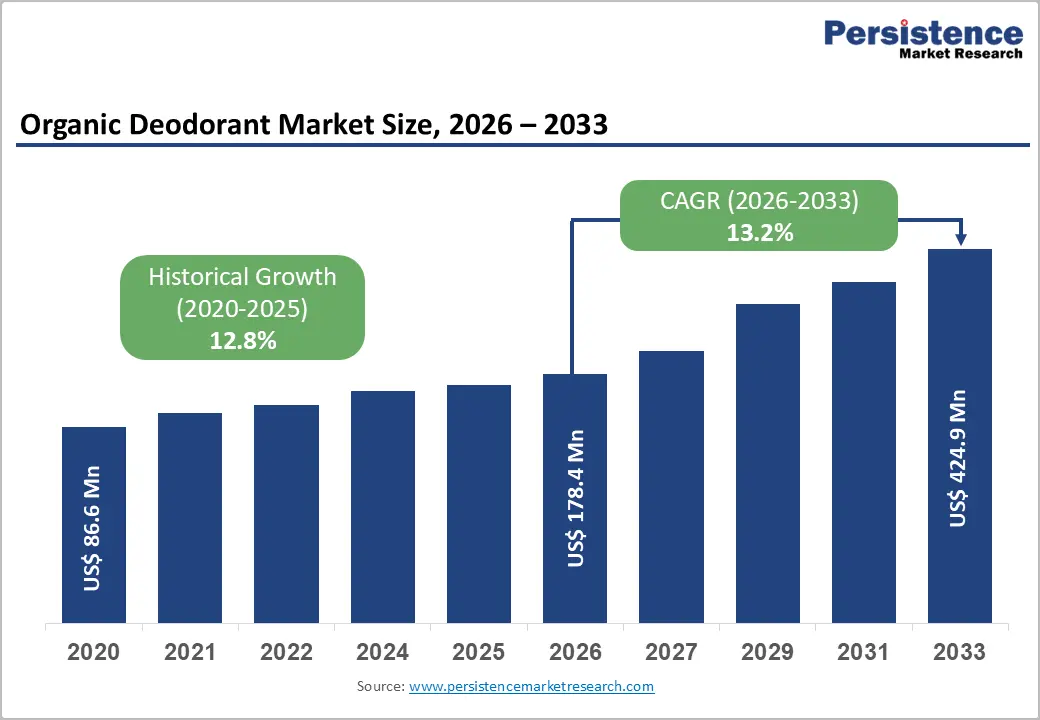

The global organic deodorant market size is expected to be valued at US$ 178.4 million in 2026 and projected to reach US$ 424.9 million by 2033, growing at a CAGR of 13.2% between 2026 and 2033.

Market expansion is primarily fueled by rising consumer awareness of long-term health risks linked to synthetic ingredients such as aluminum compounds, parabens, and phthalates. According to a 2023 Environmental Working Group (EWG) survey, nearly 74% of U.S. shoppers actively check product labels before purchase. Clean beauty movements, European Commission regulatory tightening, and surging demand for cruelty-free, vegan-certified products further reinforce growth.

Key Industry Highlights:

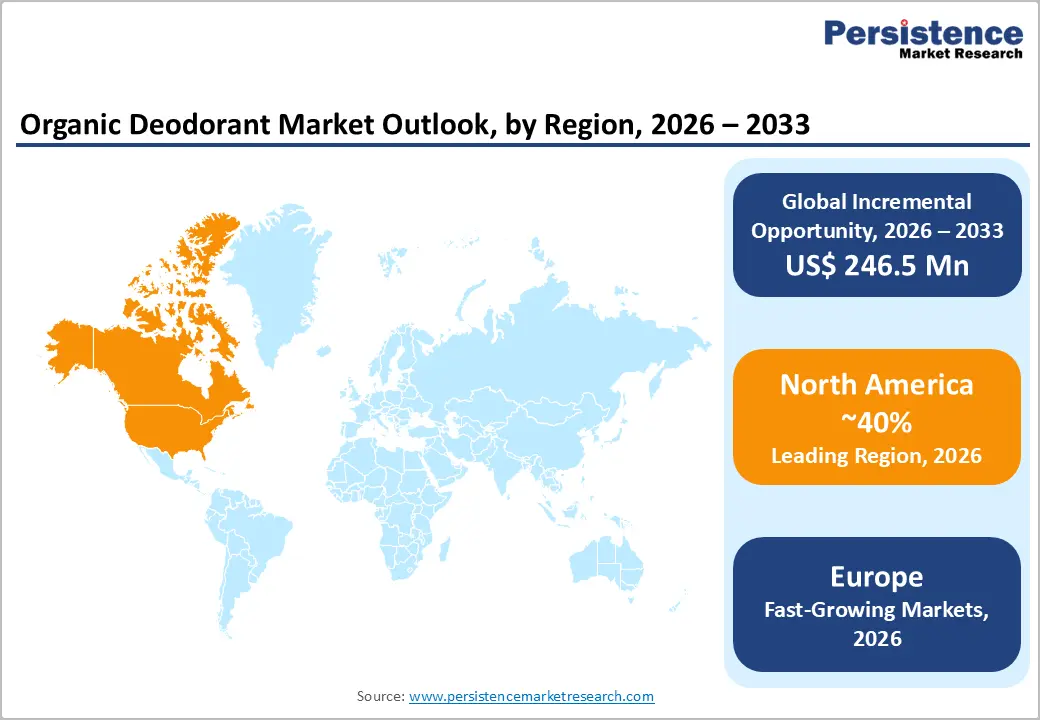

- Leading Region: North America dominates with nearly 40% share in 2025, driven by mature clean beauty adoption and well-established USDA Organic certification ecosystems.

- Fastest Growing Market: Europe leads growth at 14.1% CAGR during 2025-2032, fueled by the stringent EU Cosmetics Regulation and COSMOS-certified sustainable product expansion.

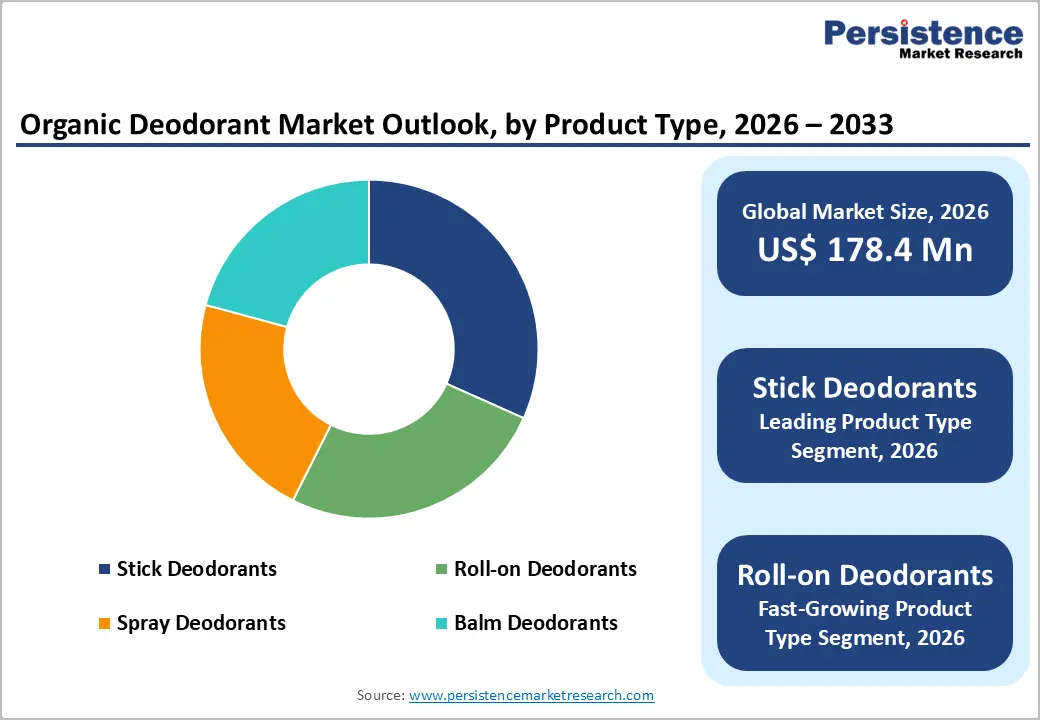

- Leading Category: Stick deodorants dominate product type with approximately 42% share in 2025, owing to mess-free application, portability, and balm-based formulation compatibility.

- Fastest Growing Distribution Channel: Online distribution is fast-growing at around 15% CAGR through 2032, driven by DTC subscriptions, marketplace expansion, and ingredient transparency-led decisions.

- Key Opportunity: Refillable and plastic-free packaging innovations present major upside, supported by EU PPWR 2024 mandates and Gen Z demand for sustainable cosmetics.

Market Dynamics

Drivers - Rising Consumer Awareness Around Aluminum-Free and Chemical-Free Formulations

A pronounced shift in consumer preferences toward aluminum-free, paraben-free, and phthalate-free personal care products is significantly driving the organic deodorant industry. According to the U.S. Food and Drug Administration (FDA), aluminum-based compounds in conventional antiperspirants have raised consumer concerns regarding skin sensitization and long-term exposure effects, prompting reformulation across the personal care market.

A 2024 report by the Organic Trade Association (OTA) noted that organic personal care product sales in the United States grew by approximately 9.7% year-on-year, outpacing the conventional segment. Millennials and Gen Z consumers are increasingly opting for plant-derived formulations, with the U.S. Environmental Protection Agency (EPA) also encouraging safer ingredient transparency, propelling demand within the organic skin care market and adjacent categories.

Expanding Retail Footprint of Clean Beauty and Sustainable Brands

The proliferation of dedicated natural and organic beauty retail chains, including Whole Foods Market, Sprouts Farmers Market, and Holland & Barrett, has substantially widened consumer access to organic deodorants. According to the U.S. Department of Commerce, retail sales of natural personal care products expanded notably during 2023-2024, supported by rising shelf-space allocation and dedicated clean beauty merchandising programs across major retailers.

Furthermore, e-commerce platforms such as Amazon, iHerb, and Thrive Market are dedicating expanded shelf space to certified-organic deodorants, with Amazon's Climate Pledge Friendly label covering thousands of personal care SKUs. This omnichannel availability, combined with influencer-driven marketing on TikTok and Instagram, accelerates penetration into mainstream households and enhances the green personal care market visibility globally.

Restraints - Higher Price Points Compared to Conventional Deodorants

Organic deodorants typically command a price premium of 30%-60% over conventional counterparts, owing to certified-organic raw materials, third-party certifications such as USDA Organic, COSMOS, and Ecocert, and small-batch manufacturing. These premium cost structures stem from rigorous supply chain audits, traceability mandates, and lower production volumes compared to mass-market chemical antiperspirants distributed by multinational personal care manufacturers.

According to a 2024 Statistics Canada household expenditure report, price sensitivity remains a key purchase barrier among middle-income consumers, particularly in inflationary economies. This premium positioning restricts adoption in price-conscious emerging markets and limits repeat purchases among value-seeking shoppers, creating a meaningful drag on volume-driven growth across the broader natural cosmetics market and constraining mass-market penetration globally.

Performance Concerns Around Odor and Sweat Control

A persistent challenge for the organic deodorant industry is consumer skepticism around the efficacy of natural formulations versus traditional antiperspirants. Since organic variants typically exclude aluminum chlorohydrate the active compound regulated by the U.S. Food and Drug Administration (FDA) that blocks sweat glands, many users report shorter wear time and inadequate odor protection in hot, humid environments and during prolonged physical activity.

A 2023 consumer satisfaction study published in the International Journal of Cosmetic Science found that nearly 38% of first-time organic deodorant users discontinued use within three months due to perceived underperformance, particularly in tropical climates. This efficacy perception gap continues to slow repeat purchase rates and constrains broader adoption among performance-driven consumers seeking all-day sweat protection.

Opportunities - Surging Demand for Refillable and Plastic-Free Packaging Innovations

Sustainable packaging is emerging as a high-impact opportunity for organic deodorant brands. According to the Ellen MacArthur Foundation, the global refillable beauty packaging segment is projected to expand at double-digit growth through 2030, with personal care among the fastest-adopting categories. Brands such as Wild, By Humankind, and Myro have pioneered refillable cases and compostable cardboard tubes, attracting climate-conscious millennials and Gen Z buyers.

The European Union's Packaging and Packaging Waste Regulation (PPWR), finalized in 2024, mandates significant reductions in single-use plastic by 2030. Combined with the U.S. Environmental Protection Agency's (EPA) sustainable materials initiatives, this regulatory momentum is accelerating reformulation of packaging across the natural deodorant ecosystem and creating commercial whitespace for early movers in the sustainable cosmetics market.

Rising Penetration in Men's Grooming and Gender-Neutral Categories

Men's organic personal care is rapidly emerging as an underpenetrated, high-growth opportunity. According to the U.S. Bureau of Labor Statistics Consumer Expenditure Survey (2023), male consumers increased spending on personal grooming products by approximately 11% year-on-year, with natural and organic SKUs gaining a disproportionate share within the broader men's toiletries category across North American and European markets.

Brands like Native, Schmidt's (owned by Unilever), and Each & Every are launching unisex and male-targeted organic deodorants with woody, citrus, and clean musk profiles. Combined with the rise of gender-neutral SKUs preferred by Gen Z and supported by the Personal Care Products Council (PCPC), this opportunity is reshaping product development pipelines and creating a strong tailwind for innovation across the organic men's grooming market.

Category-wise Analysis

Product Type Insights

Stick deodorants represent the leading product type, accounting for an estimated 42% market share in 2025 within the organic deodorant industry. According to the Personal Care Products Council (PCPC), stick formats remain the most preferred deodorant delivery system in North America and Europe combined, owing to consumer familiarity, mess-free application, longer wear time, and compatibility with solid balm-based natural formulations widely retailed across mainstream channels.

Roll-on deodorants are emerging as the fastest-growing product type within the organic deodorant landscape. The format's lightweight feel, quick-drying finish, and travel-friendly compliance with International Air Transport Association (IATA) liquid restrictions resonate strongly with younger consumers. Brands such as Weleda, Salt of the Earth, and Schmidt's are expanding aluminum-free roll-on portfolios with botanical actives, accelerating adoption across European pharmacies and Asia Pacific e-commerce platforms.

Fragrance Type Insights

The citrus fragrance segment leads the organic deodorant market with an approximate 34% share in 2025, driven by its universal appeal across genders and age demographics. Citrus-based essential oils such as bergamot, lemon, grapefruit, and orange are widely recognized for their natural antibacterial and odor-neutralizing properties, supported by research published in the Journal of Essential Oil Research and adopted broadly across unisex organic deodorant SKUs.

Herbal fragrances are emerging as the fastest-growing segment, fueled by rising consumer interest in botanical wellness and aromatherapy-inspired personal care. According to the International Federation of Essential Oils and Aroma Trades (IFEAT), demand for lavender, eucalyptus, sage, and tea tree oils has expanded steadily, supported by clean-label preferences. Brands such as Tom's of Maine and Weleda are leveraging herbal blends to differentiate within the natural fragrance market.

End-user Insights

Women constitute the leading end-user segment, holding approximately 58% market share in 2025 within the organic deodorant landscape. Female consumers traditionally exhibit higher engagement with clean beauty trends, sustainability messaging, and ingredient transparency. The proliferation of female-led indie brands such as Kosas, Megababe, and Salt & Stone, alongside dermatologically endorsed pregnancy-safe and breastfeeding-safe lines, has further deepened category penetration across the women's organic personal care market.

The men's segment is emerging as the fastest-growing end-user category, fueled by rising male engagement with grooming, wellness, and clean-label personal care. According to the U.S. Bureau of Labor Statistics, male spending on grooming products has expanded notably, with brands such as Native, Each & Every, and Hume Supernatural launching woody, musky, and aluminum-free organic deodorants targeted at millennial and Gen Z male consumers globally.

Distribution Channel Insights

The online distribution channel is the leading segment, capturing nearly 38% market share in 2025 within the organic deodorant industry. According to the U.S. Census Bureau, online retail sales of health and personal care products grew by approximately 12% year-on-year in 2024. Marketplaces such as Amazon, iHerb, and brand-owned Shopify storefronts dominate digital sales, supported by subscription-based DTC models from Native and Hume Supernatural.

Specialty stores, particularly natural and organic retail chains, are emerging as the fastest-growing distribution channel. Retailers such as Whole Foods Market, Sprouts Farmers Market, and Holland & Barrett are expanding dedicated clean beauty sections with curated organic deodorant assortments. Consumer preference for in-store ingredient verification, certified-organic merchandising, and trained staff guidance is accelerating footfall across the specialty natural personal care retail landscape globally.

Regional Insights

North America Organic Deodorant Market Trends and Insights

North America holds the leading position with an estimated 40% share of the global organic deodorant market in 2025, propelled by mature clean beauty adoption, well-established certification ecosystems such as USDA Organic, and high consumer willingness to pay premium prices. Increasing concerns regarding aluminum exposure, ingredient transparency, and plastic-free packaging continue to fuel category expansion across the region.

- U.S. Organic Deodorant Market Size

The United States dominates North America, accounting for nearly 85% of the regional market in 2025. Strong retail penetration through Whole Foods Market, Target's Clean Beauty assortment, and Sephora's Clean at Sephora program supports growth. Rising sales of indie organic brands and sustained demand for aluminum-free SKUs across millennial and Gen Z cohorts further reinforce U.S. leadership in the natural deodorant ecosystem.

Europe Organic Deodorant Market Trends and Insights

Europe is the fastest-growing region with a forecast CAGR of approximately 14.1% during 2025-2032. Stringent regulatory frameworks under the EU Cosmetics Regulation (EC) No 1223/2009, expanding COSMOS and Ecocert certified product portfolios, and strong sustainability-driven consumer attitudes are major regional growth catalysts driving organic personal care adoption.

- Germany Organic Deodorant Market Size

Germany captures nearly 24% of the European organic deodorant market in 2025. The country's mature natural cosmetics retail network, including dm-drogerie markt and Rossmann, alongside flagship local brands such as Weleda, anchors strong demand. Rising consumer preference for NATRUE-certified personal care reinforces Germany's regional dominance.

- U.K. Organic Deodorant Market Size

The United Kingdom holds approximately 18% share of the European organic deodorant market in 2025. Strong sustainability movements, retail leadership by Holland & Barrett and Boots, and the rapid rise of refillable brands such as Wild are propelling growth. Growing vegan-certified product launches further support consumer adoption.

- France Organic Deodorant Market Size

France accounts for around 15% of the European market in 2025, supported by the country's deeply rooted natural beauty heritage and the influence of pharmacy-led personal care retailing. Brands such as Sanoflore and Cattier, available across Pharmacie networks, drive premium organic deodorant adoption among health-conscious consumers.

Asia Pacific Organic Deodorant Market Trends and Insights

Asia Pacific is an emerging high-potential region, with China projected to register strong double-digit growth driven by rising disposable income, expanding cross-border e-commerce via Tmall Global and JD.com, and growing influence of K-beauty and clean beauty trends across Tier-1 and Tier-2 cities, supporting organic deodorant penetration.

- India Organic Deodorant Market Size

India represents one of the fastest-growing Asia Pacific markets, contributing nearly 12% regional share in 2025. The rise of homegrown ayurvedic and organic personal care brands such as Forest Essentials, Mamaearth, and Khadi Naturals, supported by Ministry of AYUSH endorsements, is accelerating organic deodorant adoption in metro consumer pockets.

- Japan Organic Deodorant Market Size

Japan accounts for approximately 18% of the Asia Pacific organic deodorant market in 2025. High consumer awareness of dermatologically safe formulations, growing demand for fragrance-light products, and strong distribution through Matsumoto Kiyoshi and Welcia drugstore chains support steady premium organic deodorant growth.

- Southeast Asia Organic Deodorant Market Size

Southeast Asia contributes nearly 15% regional share in 2025, led by Indonesia, Thailand, and the Philippines. Tropical climate conditions drive frequent deodorant usage, while platforms such as Shopee and Lazada enable accelerated penetration of indie organic brands and global imports across urban millennial consumers.

Competitive Landscape

The global organic deodorant market is moderately fragmented, with a competitive mix of multinational personal care giants and agile indie clean beauty brands vying for shelf and digital share. Established players are leveraging strategic acquisitions, sustained R&D investments in aluminum-free actives, magnesium-based formulations, and refillable packaging innovations to consolidate leadership across mature North American and European markets.

Indie brands are intensifying competitive pressure through differentiated positioning around vegan certification, plastic-free packaging, and minimalist clean-label branding. Direct-to-consumer subscription models, influencer-led marketing collaborations, and transparent ingredient disclosures have emerged as key strategic differentiators, reshaping consumer engagement patterns and accelerating challenger brand growth across the competitive organic personal care landscape globally.

Key Developments:

- In March 2025, Unilever expanded its Schmidt's Naturals lineup with a new sensitive-skin magnesium stick deodorant range, targeting consumers with reactive skin and reinforcing its leadership in the aluminum-free organic deodorant segment across the U.S. and U.K. markets.

- In November 2024, Native (a Procter & Gamble brand) launched a plastic-free paper-based deodorant tube line, marking a major sustainability milestone and aligning with retailer pledges from Target and Walmart on packaging waste reduction.

- In July 2024, Wild Cosmetics announced a multi-million-pound investment to scale its refillable deodorant manufacturing capacity in the U.K., supporting expansion into European markets including Germany and France.

Global Organic Deodorant Market - Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 86.6 million |

|

Current Market Value (2026) |

US$ 178.4 million |

|

Projected Market Value (2033) |

US$ 424.9 million |

|

CAGR (2026-2033) |

13.2% |

|

Leading Region |

North America, 40% |

|

Dominant Category-1 |

Stick Deodorants, US$ 74.9 million |

|

Top-ranking Category-2 |

Citrus Fragrance, US$ 60.7 million |

|

Incremental Opportunity |

US$ 246.5 million |

Companies Covered in Organic Deodorant Market

- Unilever PLC

- The Procter & Gamble Company

- L'Oréal S.A.

- Tom's of Maine

- Weleda AG

- Burt's Bees

- Dr. Bronner's

- Wild Cosmetics Ltd.

- By Humankind, Inc.

- Each & Every Co.

- Megababe Beauty

- Salt & Stone

- Hume Supernatural

- Kopari Beauty

- Pretty Frank

Frequently Asked Questions

The global organic deodorant market is projected to be valued at US$ 178.4 million in 2026, growing at a CAGR of 13.2% through 2033 to reach US$ 424.9 million.

Rising consumer awareness of aluminum-free, paraben-free, and phthalate-free personal care, combined with clean beauty movements and sustainability trends, is driving strong global demand for certified-organic deodorants.

North America leads the global organic deodorant market with nearly 40% share in 2025, supported by mature clean beauty retail networks, USDA Organic certification adoption, and premium consumer spending behavior.

Refillable and plastic-free packaging innovations represent a major growth opportunity, supported by EU PPWR 2024 regulations and rising Gen Z demand for sustainable, low-waste personal care alternatives globally.

Key market players include Unilever PLC, The Procter & Gamble Company, L'Oréal S.A., Tom's of Maine, Weleda AG, Burt's Bees, Dr. Bronner's, Wild Cosmetics, and By Humankind.