- Transportation & Logistics

- North America Mobility as a Service Market

North America Mobility as a Service Market Size, Share, and Growth Forecast 2026 - 2033

North America Mobility as a Service Market by Service Type (Ride Hailing Services, Ride Sharing Services, Public Transport Services, Micro Mobility Services, Car Sharing Services), Transportation Type (Public Transportation, Private Transportation, Shared Transportation), Payment Type (On-demand, Subscription-based), Business Model (Business-to-Consumer, Business-to-Business, Peer-to-Peer), and Regional Analysis, 2026 - 2033

North America Mobility as a Service Market Size and Trend Analysis

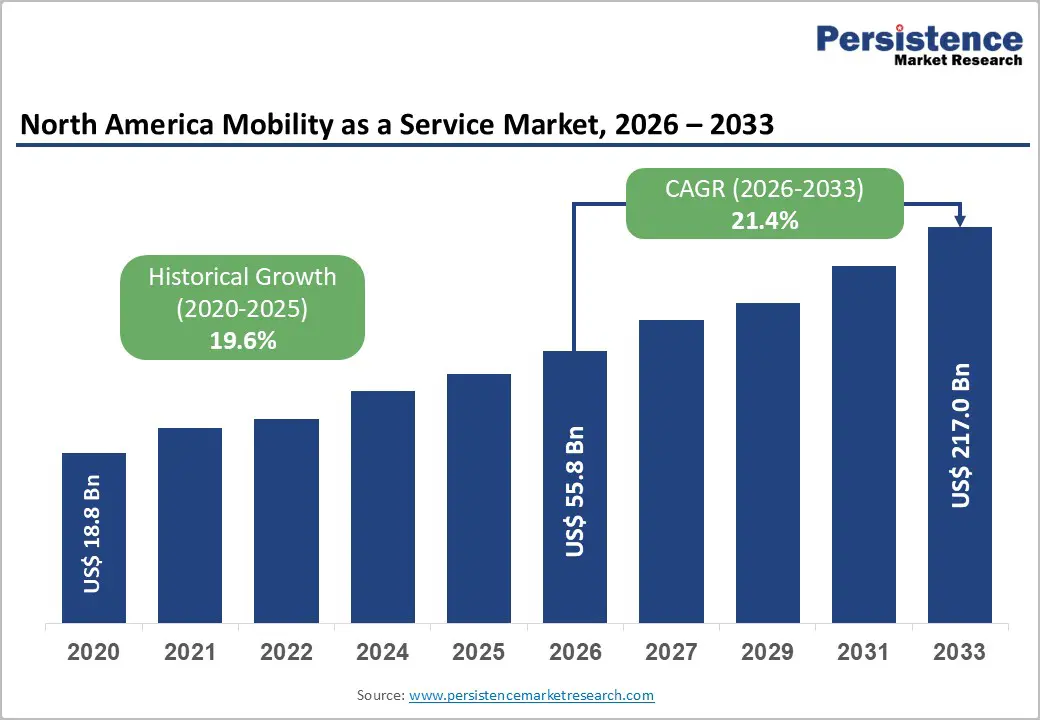

The North America mobility as a service market size is expected to reach US$55.8 billion in 2026 and is projected to reach US$217.0 billion by 2033, growing at a CAGR of 21.4% between 2026 and 2033. The North American Mobility as a Service (MaaS) market is experiencing accelerated growth, driven by rapid urbanisation, escalating traffic congestion, and a structural shift in consumer preferences from ownership to access-based transportation.

According to the U.S. Census Bureau, more than 83% of the U.S. population lived in urban areas in 2024, intensifying the demand for integrated digital mobility platforms. Additionally, large-scale deployment of autonomous ride-hailing services by Waymo, Uber, and Lyft, combined with supportive federal initiatives such as the U.S. Department of Transportation's Smart Mobility programs, is reinforcing market expansion across U.S. and Canadian metropolitan corridors.

Key Industry Highlights:

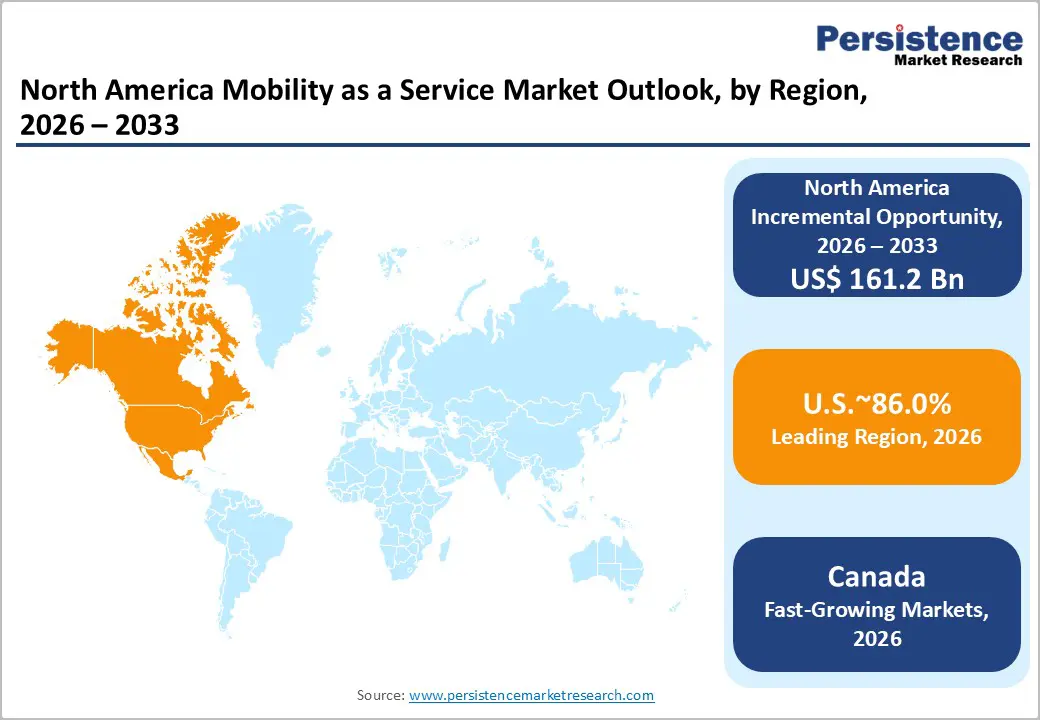

- Leading Region: The U.S. dominates the North America MaaS market with over 89% regional share in 2025, supported by ride-hailing penetration, autonomous vehicle commercialization, and advanced digital infrastructure across major metropolitan corridors.

- Fast- Growing Country: Canada is a fast-growing country, registering a double-digit CAGR, supported by smart-city investments in Toronto, Montreal, and Vancouver, and rapid uptake of multimodal commuter platforms across urban populations.

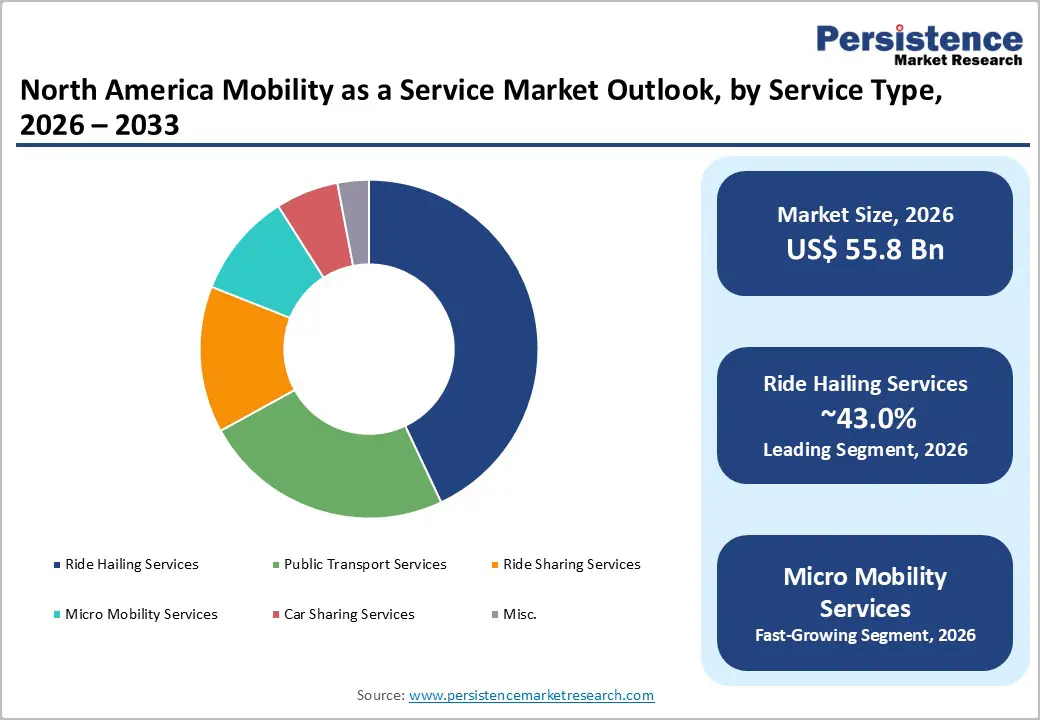

- Dominant Service Type: Ride-hailing services lead with approximately 43% share in 2025, propelled by the strong presence of Uber and Lyft, robust app-based ecosystems, and rising integration of autonomous robotaxi fleets.

- Fast-Growing Service Type: Micro mobility services is the fast-growing segment, expanding at 21% CAGR through 2032, driven by demand for last-mile connectivity, expanding e-scooter fleets, and dedicated urban cycling infrastructure across U.S. and Canadian cities.

- Key Opportunity: Rapid adoption of subscription-based multimodal platforms presents major growth potential, enabling MaaS operators to unlock recurring revenue, deepen customer loyalty, and integrate ride-hailing, transit, and micro mobility into unified mobility wallets.

DRO Analysis

Drivers - Rising Urban Congestion and Shift Toward Shared Mobility Solutions

Mounting urban traffic congestion across North America is a primary catalyst for accelerating Mobility as a Service adoption. According to the U.S. Department of Transportation's Federal Highway Administration, U.S. drivers collectively wasted over 8.7 billion hours in traffic in 2024, equating to approximately US$ 88 billion in lost productivity. Cities such as New York, Los Angeles, Chicago, and Toronto are experiencing severe pressure on transportation networks, prompting commuters to seek multimodal alternatives.

The American Public Transportation Association (APTA) reported that ridership on integrated mobility platforms grew nearly 16% in 2024 alone. This shift is reinforced by digital-first consumer behavior, with Pew Research Center noting that 76% of urban U.S. adults use ride-hailing or app-based mobility services. The growing intersection of shared mobility and the broader connected car market is further amplifying demand for seamless, app-based commuting.

Expansion of Autonomous Vehicle Deployments Across MaaS Platforms

The accelerated commercialisation of autonomous vehicles is significantly strengthening North America's MaaS ecosystem. The National Highway Traffic Safety Administration (NHTSA) authorized expanded autonomous testing across 29 U.S. states in 2025, enabling operators, including Waymo, Cruise, Zoox, and May Mobility, to scale robotaxi fleets.

Waymo reported delivering over 150,000 fully autonomous rides per week by mid-2025, while Lyft's partnership with BENTELER Mobility and HOLON GmbH is enabling autonomous shuttle rollouts beginning in 2026. The integration of AI-driven fleet management is reducing per-mile operational costs by an estimated 35-40%, according to the U.S. Department of Energy's Argonne National Laboratory. This convergence of automation, electrification, and platform-based mobility is reshaping the competitive landscape of the autonomous vehicle market within the MaaS framework.

Restraints - Regulatory Fragmentation Across U.S. States and Canadian Provinces

The North American MaaS market faces persistent regulatory inconsistency, with each U.S. state and Canadian province enforcing distinct licensing, insurance, and operational mandates. The National Conference of State Legislatures (NCSL) reported that 41 U.S. states introduced revised ride-hailing or autonomous vehicle legislation between 2023 and 2025, often creating compliance complexity for cross-state operators.

In Canada, Transport Canada maintains separate provincial frameworks for ride-sharing, public transit integration, and autonomous testing. Such fragmentation increases legal overhead, slows multi-city expansion, and constrains data-sharing initiatives essential for unified mobility ecosystems, ultimately limiting platform scalability and discouraging smaller operators from entering high-potential metropolitan markets.

Data Privacy and Cybersecurity Vulnerabilities in Connected Mobility Ecosystems

The expansion of digital, app-based mobility platforms has heightened concerns regarding consumer data privacy and cybersecurity. According to the Federal Trade Commission (FTC), complaints related to ride-hailing and connected mobility data breaches rose nearly 22% in 2024. The Cybersecurity and Infrastructure Security Agency (CISA) has flagged shared mobility platforms among critical sectors vulnerable to ransomware and identity theft attacks.

Compliance with frameworks such as the California Consumer Privacy Act (CCPA) and Canada's PIPEDA adds substantial cost burdens. These vulnerabilities undermine consumer trust, particularly for subscription-based and multimodal services, restraining adoption among privacy-sensitive demographics and enterprise users.

Opportunities - Rapid Growth of Micro Mobility and Last-Mile Connectivity Solutions

Micro mobility represents one of the most lucrative opportunities in North America's MaaS landscape, growing at a forecast CAGR of 21% between 2025 and 2032. The North American Bikeshare and Scootershare Association (NABSA) reported that shared micromobility trips exceeded 180 million in 2024, marking a 27% year-on-year increase.

Major U.S. cities, including Washington D.C., San Francisco, Austin, and Denver, have expanded protected bike lanes and integrated docking infrastructure under the U.S. Department of Transportation's Safe Streets and Roads for All (SS4A) program, which allocated US$ 1.7 billion in 2024 for safer urban mobility. Operators including Lime, Bird Global, and Spin are leveraging electric bicycles and e-scooters to bridge first- and last-mile gaps, opening pathways for deeper integration with the broader electric vehicle market and transit agencies.

Adoption of Subscription-Based and Multimodal Mobility Platforms

The shift toward subscription-based MaaS offerings is unlocking new revenue streams for operators across North America. The American Public Transportation Association (APTA) noted that pilot programs integrating transit passes, ride-hailing credits, and bike-share access generated over US$ 420 million in subscription revenue in 2024. Platforms such as Uber One, Lyft Pink, and Transit App Royale are reporting double-digit subscriber growth, with Uber disclosing more than 30 million active members globally by Q1 2025.

Cities including Toronto, Vancouver, and Seattle are piloting unified mobility wallets enabling seamless multimodal payments. This trend aligns with growth in the smart transportation market, where bundled service models are reshaping commuter economics and operator profitability.

Category-wise Analysis

Service Type Insights

Ride hailing services constitute the dominant segment within the North America Mobility as a Service market, accounting for nearly 43% share in 2026. The leadership of this segment is underpinned by the widespread penetration of platforms such as Uber Technologies, Inc. and Lyft, Inc., which together serve over 150 million monthly active users across the U.S. and Canada, according to company filings.

The U.S. Bureau of Transportation Statistics indicates that ride-hailing trips accounted for over 6.8 billion total annual rides in 2024. The integration of autonomous vehicles into ride-hailing networks, exemplified by Uber's partnership with May Mobility and Lyft's alliance with Waymo, is further consolidating segment dominance, supported by AI-driven dispatch, dynamic pricing, and large urban customer bases.

Transportation Type Insights

Shared transportation leads the North America MaaS market, holding approximately 48% share in 2026. The growth trajectory is driven by widespread adoption of pooled ride-hailing, carpooling, and shared micro mobility services across major North American metros.

According to the U.S. Department of Transportation, shared mobility trips surpassed 8.4 billion in 2024, representing a substantial year-on-year increase. Platforms such as BlaBlaCar, Uber Pool, Lyft Shared, and Via Transportation are leveraging AI route-optimisation to maximise fleet utilisation and reduce per-trip emissions. The U.S. Environmental Protection Agency (EPA) reports shared transportation reduces urban transport emissions by approximately 30%, reinforcing both environmental and economic justifications for sustained adoption across U.S. and Canadian metropolitan corridors.

Payment Type Insights

The on-demand payment model dominates the North America MaaS market, capturing nearly 71% market share in 2026. Consumers across the U.S. and Canada strongly favor pay-per-trip flexibility for ride-hailing, car-sharing, and micro mobility services, supported by digital wallet penetration exceeding 89% among urban smartphone users, per Statistics Canada and U.S. Federal Reserve Payment Studies.

Real-time fare estimation, surge pricing algorithms, and instant settlement systems used by Uber, Lyft, and Lime make on-demand models the default consumer experience. The Federal Reserve Bank of Atlanta reports that contactless mobility payments grew nearly 24% in 2024, further cementing the dominance of transaction-based engagement over subscription alternatives, particularly among occasional and tourist-driven commuter segments.

Business Model Insights

The Business-to-Consumer (B2C) model leads the North America MaaS market, accounting for approximately 62% share in 2026. The model's dominance is reinforced by direct app-based engagement with millions of urban commuters across the U.S. and Canada. According to industry filings of Uber and Lyft, North American B2C ride-hailing users surpassed 130 million in 2024. The model offers superior monetisation through dynamic pricing, loyalty programs, and bundled subscription add-ons.

Investments in user-experience platforms, AI-personalized recommendations, and integration of micro mobility options under unified B2C apps continue to expand customer retention. Uber One and Lyft Pink programs have collectively driven over 40 million premium subscriptions, anchoring the segment's sustained leadership.

Regional Insights

North America Mobility as a Service Market Trends and Insights

North America holds a commanding regional share of approximately 27% of the global MaaS market in 2025, driven by mature digital infrastructure, dense metropolitan populations, and aggressive autonomous vehicle commercialisation. The region benefits from strong public-private collaboration through initiatives like the U.S. DOT's Smart City Challenge and Canada's Smart Cities Challenge, alongside rapid integration of micro mobility and ride-hailing under unified mobility platforms across major urban centres.

U.S. Mobility as a Service Market Size

The U.S. mobility as a service market value stood at approximately US$39.6 billion in 2026, driven by the deep penetration of ride-hailing giants Uber and Lyft, accelerated robotaxi rollouts by Waymo, and growing adoption of multimodal commuter platforms. According to the U.S. Bureau of Transportation Statistics, more than 42 million Americans use shared mobility weekly. Robust 5G network coverage and FHWA-funded smart corridors in Texas, California, and Arizona are reinforcing accelerated commercial expansion.

Competitive Landscape

North America mobility as a service market exhibits a moderately consolidated competitive structure, with the top five players collectively holding nearly 60% of the total revenue share. Market leaders such as Uber Technologies, Inc., Lyft, Inc., and Waymo LLC are aggressively pursuing autonomous fleet expansion, AI-powered dispatch optimisation, and strategic partnerships with OEMs such as Hyundai, General Motors, and Toyota.

Key differentiators include proprietary routing algorithms, multimodal integrations, and exclusive autonomous vehicle alliances. Emerging trends include subscription-based super apps, B2B fleet-as-a-service offerings, and integration of vehicle-to-grid charging models, signalling a shift toward integrated and intelligent shared mobility ecosystems.

Key Developments:

- In July, 2025, Lyft partnered with BENTELER Mobility to introduce next-generation autonomous shuttles across the Lyft network starting in 2026, leveraging HOLON GmbH autonomous vehicles to expand autonomous Mobility as a Service (MaaS) offerings and enhance scalable, cost-efficient shared transportation solutions in the U.S. market.

- In September 2025, Lyft and Waymo announced a partnership to expand autonomous Mobility as a Service (MaaS) operations to Nashville in 2026, integrating Waymo’s fully autonomous ride-hailing vehicles with Lyft’s Flexdrive fleet management services to enhance fleet utilisation, operational efficiency, and scalable autonomous transportation across shared mobility networks.

Companies Covered in North America Mobility as a Service Market

- Lyft, Inc.

- Intel Corporation (Moovit)

- Uber Technologies, Inc.

- BlaBlaCar

- Grab Holdings Limited

- Free Now

- SkedGo

- moovel North America, LLC.

- Fluidtime

- Cubic Transportation Systems, Inc.

- Citymapper

- MaaS Global

- FOD Mobility UK Ltd.

Frequently Asked Questions

The North America Mobility as a Service market is expected to be valued at US$55.8 billion in 2026, growing at a CAGR of 21.4% to reach US$217.0 billion by 2033.

Rising urban congestion, accelerated autonomous vehicle deployment, growing smartphone penetration, and shifting consumer preference from ownership to access-based shared mobility are key demand drivers, supported by federal smart-city and transportation infrastructure investments.

The U.S. leads the North America MaaS market, holding nearly 89% regional share in 2025, supported by strong ride-hailing penetration, autonomous fleet expansion, and advanced 5G-enabled urban infrastructure.

Subscription-based multimodal mobility platforms and rapid expansion of micro mobility services growing at 21% CAGR offer the most significant opportunities for operators seeking recurring revenue, customer loyalty, and integrated last-mile connectivity solutions.

Major participants include Uber Technologies, Inc., Lyft, Inc., Waymo LLC, Cruise LLC, May Mobility, Inc., BlaBlaCar, Hertz North America Holdings, Inc., Lime, Bird Global, Inc., Via Transportation, Inc., and Moovit (Intel Corporation).