- Processed Food

- North America Bakery Products Market

North America Bakery Products Market Size, Share, and Growth Forecast 2026 - 2033

North America Bakery Products Market by Product Type (Cakes and Pastries, Biscuits, Bread, Morning Goods, Others), Distribution Channel (Hypermarkets/Supermarkets, Convenience Stores, Specialty Stores, Online Retailers, Others), Country Analysis, 2026 - 2033

North America Bakery Products Market Size and Trend Analysis

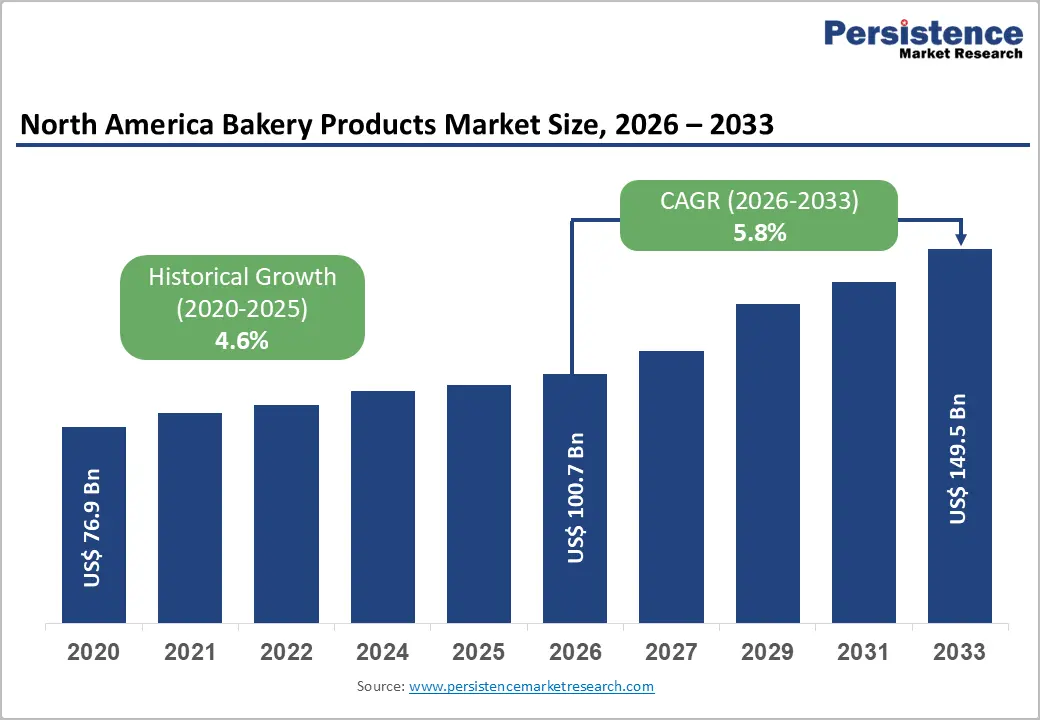

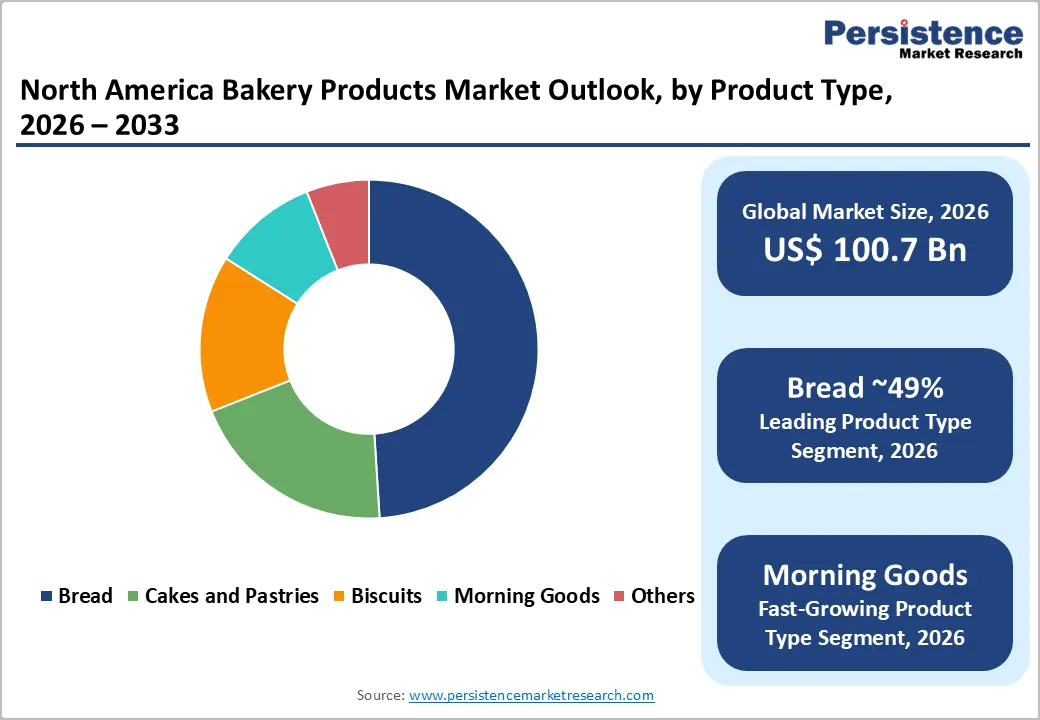

The North America bakery products market size is expected to be valued at US$ 100.7 billion in 2026 and projected to reach US$ 149.5 billion by 2033, growing at a CAGR of 5.8% between 2026 and 2033. As the market is evolving steadily, driven by changing consumer preferences toward healthier and more transparent food choices.

Growing awareness around ingredient quality and nutrition has encouraged consumers to seek clean-label, natural, and minimally processed bakery items. This shift is prompting manufacturers to reformulate products by reducing artificial additives and incorporating plant-based and functional ingredients.

The demand for convenience foods continues to support sales of packaged bakery products across busy urban populations. Innovation in artisanal, gluten-free, and specialty offerings is further expanding the market landscape. Strong retail infrastructure, along with increasing online grocery adoption, is enhancing product accessibility and supporting sustained market growth across the region.

Key Industry Highlights:

- Leading Country - The U.S. dominates the North America market, supported by a strong baking industry, extensive retail networks, and a highly advanced ecosystem for bakery innovation.

- Fastest Growing Country - Canada is the fastest-growing market, driven by rising population diversity, evolving consumer preferences, and increasing demand for premium, specialty, and organic bakery offerings.

- Dominant Segment - Bread remains the dominant segment, reflecting its role as a daily staple, with growing consumer interest in artisanal, whole grain, and health-focused varieties.

- Fastest Growing Segment - Morning goods are the fastest-growing category, fueled by busy lifestyles, expanding café culture, social media influence, and demand for convenient yet indulgent breakfast options.

- Key Opportunity - Rapid growth of e-commerce and direct-to-consumer models offers a significant opportunity, enabling brands to improve margins, strengthen customer relationships, and cater to health-conscious buyers.

Market Dynamics

Drivers - Expanding Health and Wellness Consciousness, Reshaping Bakery Product Formulations

Consumer health awareness is profoundly reshaping bakery product formulations across North America, creating a powerful and sustained demand uplift for functional, clean-label, and specialty dietary offerings. According to the International Food Information Council (IFIC) Foundation's Food & Health Survey, over 52% of American consumers actively seek to limit or avoid certain ingredients, including refined sugars, artificial additives, and trans fats, when purchasing food products. This behavioral shift has prompted major manufacturers and artisan producers alike to reformulate bread, biscuit, and pastry offerings with whole grains, plant-based proteins, probiotics, and natural sweeteners.

The Whole Grains Council reports that whole grain product availability in North America has grown by over 2,000% since 2003, illustrating the depth of this market transformation. Health-positioned bakery products command premium price points, supporting both revenue growth and margin improvement for market participants through the forecast period.

Rising Demand for Convenience Foods and On-the-Go Consumption Formats

The accelerating pace of modern lifestyles across North America is fueling strong and growing demand for convenient, ready-to-eat bakery formats, particularly in the Morning Goods and Bread categories. According to the U.S. Bureau of Labor Statistics (BLS), American workers average only 37 minutes per day on food preparation and cleanup a figure that underscores the structural appeal of portable bakery products as time-efficient meal solutions. Breakfast pastries, grab-and-go muffins, single-serve wraps, and pre-sliced specialty breads are experiencing accelerating shelf velocity across convenience stores, supermarkets, and online channels.

The Food Marketing Institute (FMI) notes that ready-to-eat and convenience food categories consistently rank among the highest-growth segments in U.S. grocery retail, validating the strategic importance of convenient bakery formats. Manufacturers investing in extended shelf-life technology and innovative packaging formats are capturing a disproportionate share of this high-velocity segment.

Restraints - Commodity Input Cost Volatility Squeezing Manufacturer Margins

Fluctuating prices of key bakery inputs, including wheat flour, sugar, butter, and vegetable oils represent a persistent and significant margin pressure for North American bakery manufacturers. The U.S. Department of Agriculture (USDA) reports that wheat prices experienced a 40%+ surge in 2022 due to supply disruptions linked to the Russia-Ukraine conflict, and while prices have partially normalized, structural volatility remains elevated. For mid-size and smaller bakery producers with limited hedging capabilities and fixed-price retail contracts, raw material cost spikes directly compress operating margins and constrain investment in innovation and distribution expansion, creating a durable competitive disadvantage relative to large-scale players.

Opportunities - Emergence of Artisan Bakeries Providing Premium Products

Increasing consumer preference for artisan bakery products is anticipated to create new opportunities in North America. Artisan bakeries are using various healthy ingredients such as natural sweeteners and whole grains to develop products appealing to younger consumers seeking premium and authentic bakery items. The American Bakers Association, for instance, revealed that about 90% of millennials and Gen Z customers have bought artisanal products such as tortillas, wraps, flatbreads, and pizzas.

Artisan bakeries often employ sustainable practices and source their ingredients locally, which lines up with rising interest of consumers in supporting homegrown businesses. These bakeries are now focusing on differentiating themselves from their competitors by delivering creative items and unique flavors that are otherwise difficult to find in mass-market bakeries. They are also adding nutrient-rich ingredients such as nuts, seeds, spelt, amaranth, and quinoa to improve the nutritional profile of their products.

Category-wise Analysis

Product Type Insights

Bread dominates the Product Type category with a commanding 49% market share in 2025, reflecting its status as a daily staple food consumed across all household demographics in both the U.S. and Canada. The category encompasses white bread, whole wheat, multigrain, sourdough, artisan loaves, and specialty dietary breads, including gluten-free and keto-certified variants. According to the American Bakers Association, bread is the most universally purchased bakery item in U.S. grocery retail, with consumption spanning all income levels and age groups.

The premiumization of the bread segment, evidenced by double-digit growth in sourdough, ancient grain, and organic bread varieties, is supporting above-average revenue growth within the category. Morning Goods is the fastest-growing product segment, driven by shifting breakfast habits, café culture, and rising consumer preference for indulgent yet convenient morning occasions.

Distribution Channel Analysis

Hypermarkets and supermarkets lead the distribution channel category with an estimated 48% share in 2025. Major grocery chains, including Walmart, Kroger, Costco, and Loblaw Companies in Canada, serve as the primary purchase point for bakery products, offering broad SKU variety, in-store bakery departments, and promotional pricing that drives volume.

According to the Food Marketing Institute (FMI), bakery is one of the highest-traffic destination categories in U.S. grocery stores, generating consistent repeat visits. The in-store bakery experience offering fresh-baked bread, artisan pastries, and custom cakes is increasingly used as a key footfall and differentiation driver by major supermarket operators. Online Retailers represent the fastest-growing distribution channel, propelled by e-commerce food growth and DTC subscription models expanding bakery accessibility.

Regional Insights

The U.S. leads the North America Bakery Products market with ~87% of regional market share in 2025. Canada accounts for the remaining ~13% and is the fastest-growing country market, expanding at an estimated CAGR of approximately 6.5% through 2033, outpacing the regional average due to strong demographic-driven demand and premiumization trends.

U.S. Bakery Products Market Trends and Insights

The U.S. dominates the North America Bakery Products market, underpinned by its scale, innovation ecosystem, and the structural depth of its retail and foodservice infrastructure. The American Bakers Association (ABA) reports that the U.S. baking industry supports over 800,000 jobs and encompasses more than 3,000 commercial baking facilities nationwide. Key market trends include the rapid premiumization of everyday bakery categories, particularly bread and morning goods, alongside a decisive consumer pivot toward health-positioned offerings.

The U.S. Food and Drug Administration (FDA)'s updated Nutrition Facts panel requirements have heightened consumer awareness of sugar and fiber content, incentivizing manufacturers to reformulate products with cleaner profiles.

The U.S. also leads in bakery product innovation, with companies like Grupo Bimbo, Flowers Foods, and General Mills investing heavily in R&D for functional, high-protein, and free-from bakery lines. The USDA's National School Lunch Program which mandates whole-grain-rich bread products in school cafeterias continues to drive institutional demand for compliant bakery formulations. E-commerce penetration in food retail, which surpassed 12% of total U.S. grocery sales in 2023 per the U.S. Census Bureau, is further reshaping distribution strategies for both established brands and DTC bakery entrants.

Competitive Landscape

The North America Bakery Products market is moderately consolidated at the top, with a small number of multinational and large regional players including Grupo Bimbo, Flowers Foods, General Mills, and Mondelez International commanding significant share, while a large and vibrant cohort of regional, artisan, and specialty bakeries competes at the local and premium segment level. Key competitive differentiators include product innovation and reformulation speed, distribution network depth, private-label manufacturing capabilities, and brand investment.

The market is witnessing an accelerating trend of M&A activity as large players acquire specialty and health-positioned brands to broaden portfolio reach and access premium consumer segments.

Key Developments:

- In January 2026, Eshbal Functional Food Inc. announced a partnership with Queen St Gluten Free Inc. to manufacture its products for the North American market.

- In January 2025, Kinderini, the Ferrero-owned brand, announced that its crunchy shortbread cookies with the taste of Kinder was made available in the U.S. The product has no artificial preservatives or colors. It comes with convenient packaging as the company aims to make the product ideal for after-school snacking, car rides, or lunchboxes.

- In January 2025, OREO launched OREO Cakesters in Canada in partnership with Toronto Maple Leafs player William Nylander. The brand plans to open a playful cake shop in Toronto, providing the exclusive OREO Cakesters for a limited time for free.

- In October 2024, Vandemoortele, based in Belgium, introduced its new Pistachio Filled Croissant in North America. The product was inspired by current flavor trends and consumer requests. It was exhibited at the National Association of Convenience Stores show held in Las Vegas.

North America Bakery Products Market - Key Insights

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 76.9 Billion |

| Projected Market Value (2026) | US$ 100.7 Billion |

| Projected Market Value (2033) | US$ 149.5 Billion |

| CAGR (2026 - 2033) | 5.8% |

| Leading Country | U.S., 34% share |

| Dominant Product Type | Product Type, 49% share |

| Top-ranking Distribution Channel | Hypermarkets/Supermarkets, 51% share |

| Incremental Opportunity | US$ 48.8 Billion |

Companies Covered in North America Bakery Products Market

- Mondelez International, Inc.

- The Kellogg Company

- The J.M. Smucker Company (Hostess Brands)

- Campbell Soup Company

- GRUMA S.A.B. de C.V.

- General Mills Inc.

- Grupo Bimbo S.A.B. de C.V.

- Alpha Baking Company Inc.

- Sara Lee Frozen Bakery

- Flowers Foods Inc.

- Others

Frequently Asked Questions

The North America bakery products market is estimated to be valued at US$ 100.7 billion in 2026.

Increasing demand for clean-label products and surging number of artisan bakeries are the key market drivers.

The U.S. leads the North America Bakery Products market with approximately 87% of regional market share in 2025.

Emergence of frozen baked goods and inclusion of healthy ingredients in existing products are the key market opportunities.

Mondelez International, Inc., The Kellogg Company, and The J.M. Smucker Company (Hostess Brands) are a few key players.