- Medical Devices

- North America Medical Wellness Devices Market

North America Medical Wellness Devices Market Size, Share, and Growth Forecast, 2026 - 2033

North America Medical Wellness Devices Market by Product Type (Blood Pressure Monitors, Diabetic Monitoring Devices, Thermometers, Pulse Oximeters, and Sleep Trackers), End-user (Institutional Sales and Retail Sales), and Country Analysis for 2026 - 2033

North America Medical Wellness Devices Market Size and Trends Analysis

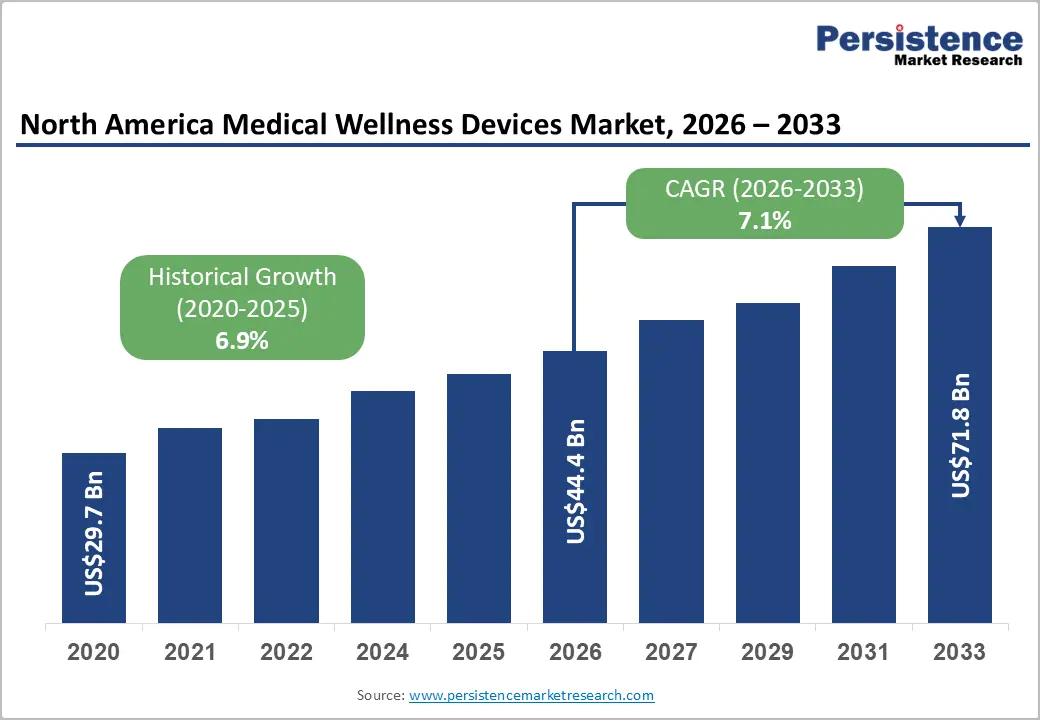

The North America medical wellness devices market size is likely to be valued at US$44.4 billion in 2026 and is expected to reach US$71.8 billion by 2033, growing at a CAGR of 7.1% during the forecast period from 2026 to 2033, driven by rising chronic disease prevalence, increasing adoption of wearable health technologies, and growing demand for remote patient monitoring solutions.

According to the U.S. Centers for Disease Control and Prevention (CDC), nearly 40.1 million Americans were living with diabetes in 2023, representing about 12% of the U.S. population, significantly increasing demand for continuous glucose monitors, pulse oximeters, and connected wellness devices. The region benefits from advanced healthcare infrastructure, high digital health adoption, and expanding telehealth integration. AI-enabled wearables, smart sleep trackers, and home-based monitoring devices are gaining traction as consumers increasingly prioritize preventive and personalized healthcare solutions.

Key Industry Highlights:

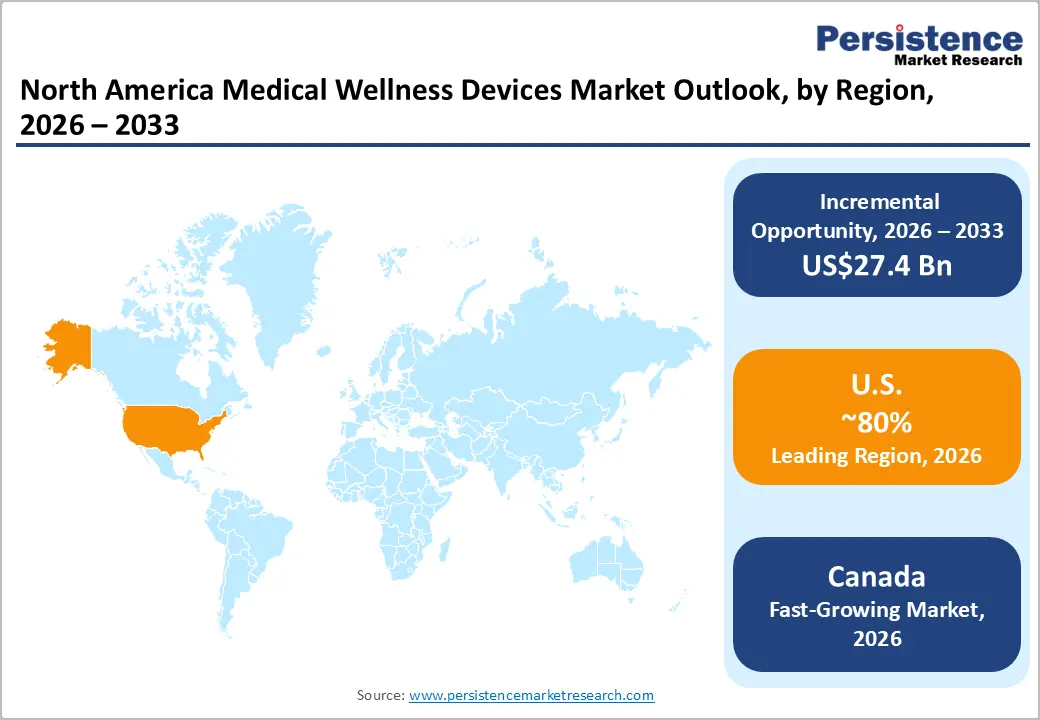

- Leading Region: The U.S. is anticipated to be the leading region, accounting for a market share of 80% in 2026, driven by strong digital health adoption, advanced healthcare infrastructure, and high demand for wearable monitoring devices.

- Fastest-growing Region: Canada is likely to be the fastest-growing region, supported by growing preventive healthcare adoption and increasing demand for remote wellness monitoring solutions.

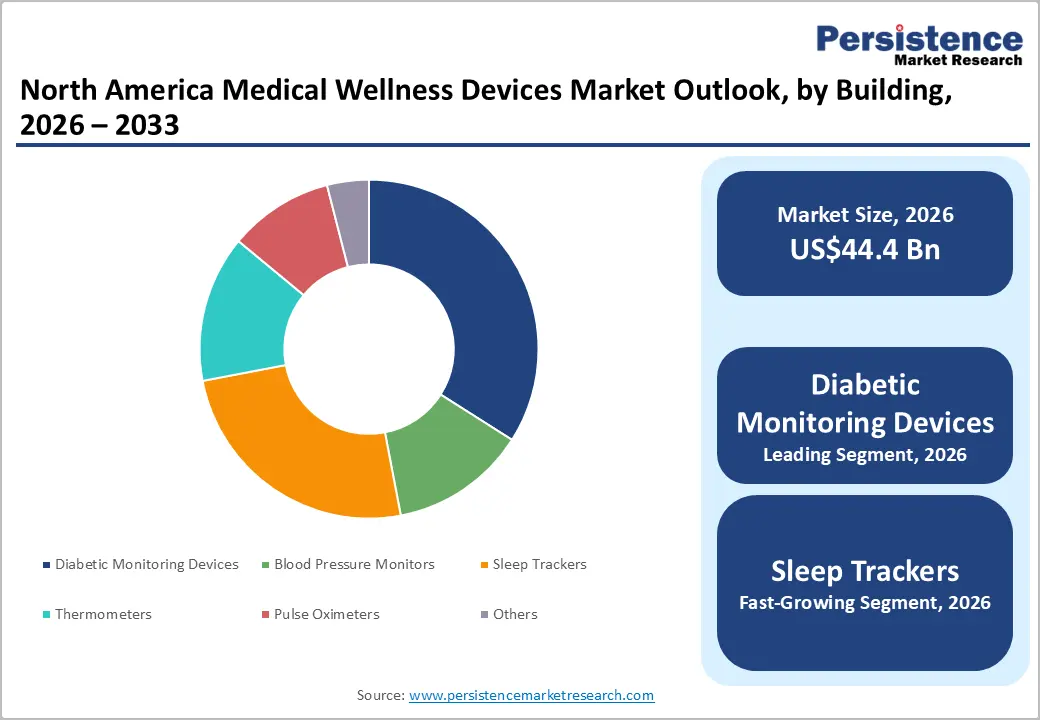

- Leading Product Type: Diabetic monitoring devices are projected to represent the leading product type in 2026, accounting for 37% of the revenue share, driven by rising diabetes prevalence and increasing adoption of continuous glucose monitoring technologies.

- Leading End-user: Retail sales are anticipated to be the leading end-user, accounting for over 62% of the revenue share in 2026, supported by strong consumer preference for self-monitoring devices through pharmacies, retail stores, and e-commerce channels.

- Key Opportunity: The rising integration of AI-powered wearable wellness devices with remote patient monitoring and telehealth platforms is creating significant growth opportunities across the North America medical wellness devices market.

DRO Analysis

Driver - Rising Prevalence of Chronic Diseases and Aging Population

The increasing prevalence of chronic diseases such as diabetes, hypertension, cardiovascular disorders, and respiratory illnesses is driving the market. Growing demand for continuous health monitoring has accelerated the adoption of blood pressure monitors, diabetic monitoring devices, pulse oximeters, and connected wearable technologies across the U.S. and Canada. According to the U.S. Centers for Disease Control and Prevention (CDC), more than 38 million Americans were living with diabetes in 2024, while hypertension affects nearly half of the adult population.

These conditions require long-term monitoring, encouraging consumers and healthcare providers to increasingly utilize remote patient monitoring and home-based wellness devices daily. The rapidly aging population across North America strengthens demand for medical wellness devices designed for preventive healthcare and chronic disease management. Older adults increasingly require continuous monitoring solutions for heart health, glucose levels, sleep quality, oxygen saturation, and mobility assistance, increasing demand for user-friendly wearable technologies and connected monitoring platforms.

Healthcare providers are also promoting home-based care to reduce hospitalization costs and improve patient outcomes. Advances in wireless connectivity, cloud integration, AI-enabled analytics, and smartphone-compatible devices are enhancing accessibility and convenience for elderly users. This demographic trend continues encouraging manufacturers to develop personalized, easy-to-use, and clinically reliable wellness monitoring devices for long-term healthcare support.

Restraint - Data Privacy, Accuracy Concerns, and Regulatory Hurdles

Data privacy and cybersecurity concerns remain significant restraints for the North America medical wellness devices market as connected health devices increasingly collect sensitive patient information. Wearable devices, cloud-based monitoring systems, and smartphone-connected wellness applications continuously transmit health data, creating risks related to unauthorized access, data breaches, and misuse of personal medical records. Consumers are becoming more cautious regarding digital health privacy, especially with the growing integration of AI and remote patient monitoring platforms.

Regulatory agencies such as the U.S. Food and Drug Administration (FDA) and Health Canada continue strengthening compliance standards related to cybersecurity, interoperability, and patient data protection, increasing operational complexity for manufacturers and software developers significantly. Accuracy limitations and regulatory approval challenges also restrict the broader adoption of certain medical wellness devices in North America.

Consumer-grade wellness devices occasionally face criticism for inconsistent readings, inaccurate monitoring, and a lack of clinical validation compared to hospital-grade equipment. Variations in sensor quality, calibration issues, and software reliability can affect trust among healthcare professionals and consumers. Obtaining regulatory approvals for AI-enabled monitoring technologies requires extensive testing, documentation, and compliance with evolving healthcare standards.

Opportunity - Expansion of AI-Powered Personalized Wellness and RPM

The growing adoption of AI-powered personalized wellness solutions and remote patient monitoring (RPM) platforms presents a major opportunity for the North America medical wellness devices market. Artificial intelligence is increasingly integrated into wearable devices, diabetic monitoring systems, sleep trackers, and cardiovascular monitoring platforms to provide predictive insights, personalized recommendations, and real-time health analytics. Consumers are seeking proactive healthcare solutions that support fitness tracking, chronic disease prevention, stress management, and early diagnosis.

AI-enabled wellness devices can analyze continuous health data patterns and deliver individualized alerts through connected applications. This technological advancement is encouraging healthcare providers and consumers to adopt smarter, more responsive wellness monitoring ecosystems across North America rapidly. Remote patient monitoring expansion is creating substantial growth opportunities for hospitals, healthcare providers, and medical device manufacturers throughout North America.

Government reimbursement support for RPM services in the United States is encouraging institutional adoption of connected wellness technologies. Healthcare systems increasingly utilize remote monitoring tools to reduce hospital admissions, improve patient engagement, and lower healthcare costs. Continuous innovation in AI algorithms, cloud computing, biosensors, and IoT connectivity is expected to enhance accuracy, interoperability, and long-term scalability within personalized wellness and RPM solutions.

Category-wise Analysis

Product Type Insights

Diabetic monitoring devices are expected to lead, accounting for approximately 37% of revenue in 2026, due to the growing prevalence of diabetes and increasing adoption of continuous glucose monitoring technologies. Rising awareness regarding preventive healthcare and long-term diabetes management has significantly increased consumer demand for connected glucose monitoring systems across the U.S. and Canada. A notable example includes Dexcom Inc., which continues expanding its continuous glucose monitoring portfolio through advanced wearable technologies.

Sleep trackers are likely to represent the fastest-growing segment, supported by increasing consumer focus on wellness monitoring, sleep quality improvement, and preventive healthcare management. The growing prevalence of sleep disorders, stress-related conditions, obesity, and mental health concerns has accelerated the adoption of wearable sleep monitoring devices among health-conscious consumers. For instance, Fitbit, Inc., which offers advanced wearable sleep tracking solutions integrated with health analytics and wellness insights.

End-user Insights

Retail sales are projected to lead the market, capturing around 62% of the revenue share in 2026, supported by increasing consumer preference for self-monitoring devices and expanding product accessibility across retail channels. Pharmacies, supermarkets, specialty healthcare stores, and e-commerce platforms have significantly improved the availability of wellness monitoring products, including blood pressure monitors, thermometers, diabetic monitoring devices, and wearable trackers. For example, Abbott, which distributes connected glucose monitoring and wellness monitoring products extensively through retail pharmacies.

Institutional sales are likely to be the fastest-growing end-user, driven by increasing adoption of remote patient monitoring and telehealth solutions by hospitals and healthcare providers. Healthcare institutions are investing heavily in connected monitoring technologies to improve chronic disease management, reduce hospital readmissions, and enhance patient outcomes through real-time data tracking. For instance, Koninklijke Philips N.V., which provides advanced remote patient monitoring and connected healthcare solutions widely adopted by hospitals and healthcare institutions.

Country Insights

U.S. Medical Wellness Devices Market Trends

The U.S. is anticipated to be the leading region, accounting for a market share of 80% in 2026, driven by increasing adoption of wearable health technologies, remote patient monitoring solutions, and AI-enabled wellness platforms. The rising prevalence of chronic diseases such as diabetes, hypertension, obesity, and cardiovascular disorders continues to accelerate demand for connected monitoring devices, including blood pressure monitors, diabetic monitoring systems, pulse oximeters, and sleep trackers. Consumers are increasingly prioritizing preventive healthcare and personalized wellness management, encouraging rapid integration of smartphone-connected and cloud-based health monitoring devices.

Expansion of telehealth services and favorable reimbursement policies for remote patient monitoring are strengthening market demand across hospitals, clinics, and home healthcare settings. Technology companies and healthcare manufacturers are focusing heavily on AI-powered analytics, predictive health insights, and real-time patient tracking capabilities to improve healthcare outcomes. A notable example includes Masimo Corporation, which continues expanding advanced remote patient monitoring and wearable health technologies.

Canada Medical Wellness Devices Market Trends

Canada is likely to be the fastest-growing region, driven by growing emphasis on preventive healthcare, aging population management, and increasing digital healthcare adoption across the country. Rising consumer awareness regarding chronic disease prevention and wellness tracking is driving demand for wearable monitoring devices, connected thermometers, diabetic monitoring systems, and sleep tracking technologies. Rural healthcare accessibility challenges are further promoting demand for remote patient monitoring technologies capable of supporting long-distance health management and virtual consultations.

Canadian consumers are increasingly adopting fitness-focused and AI-enabled wellness devices integrated with mobile applications and cloud-based health analytics platforms. Manufacturers are prioritizing user-friendly product designs, data security features, and interoperability with digital healthcare systems. For example, Garmin Ltd. continues strengthening its wearable wellness portfolio with advanced health tracking features, including sleep monitoring, heart rate tracking, stress monitoring, and connected fitness analytics solutions.

Competitive Landscape

The North America medical wellness devices market exhibits a moderately fragmented structure, driven by rapid technological advancements, rising consumer demand for connected wellness solutions, and increasing adoption of remote patient monitoring technologies across healthcare and homecare settings. Market participants are focusing heavily on wearable innovation, AI-powered analytics, cloud-based health monitoring platforms, and integration with telehealth ecosystems to strengthen market positioning.

Growing demand for diabetic monitoring devices, blood pressure monitors, pulse oximeters, and sleep tracking solutions has intensified competition among medical device manufacturers, digital health companies, and consumer wellness technology providers.

With key leaders including Abbott, Dexcom, Inc., Koninklijke Philips N.V., Masimo Corporation, Fitbit, Inc., and Garmin Ltd., the market continues witnessing strong strategic competition and product innovation activities. These players compete through advanced wearable technologies, AI-enabled wellness tracking, continuous product launches, strategic partnerships, telehealth integration, and expansion of connected healthcare ecosystems. Several companies are investing in research and development to improve sensor accuracy, predictive analytics, battery efficiency, and interoperability with mobile health applications.

Key Industry Developments:

- In May 2026, Johnson & Johnson launched the Shockwave C2 Aero Coronary IVL Catheter globally to improve the treatment of calcified coronary artery disease, featuring enhanced lesion crossing, deliverability, and repositioning capabilities for complex cardiovascular procedures.

- In March 2026, Abbott received U.S. FDA approval for its updated CardioMEMS HERO heart failure monitoring device, featuring a smaller and lighter design with enhanced remote monitoring capabilities to support early detection and management of worsening heart failure conditions.

Companies Covered in North America Medical Wellness Devices Market

- Abbott

- 3M Company

- Dexcom, Inc.

- F. Hoffmann-La Roche AG

- Koninklijke Philips N.V.

- Fossil Group, Inc.

- Garmin Ltd

- LifeScan, Inc.

- Tandem Diabetes Care

- Masimo Corporation

- Fitbit, Inc.

- Garmin Ltd.

Frequently Asked Questions

The North America medical wellness devices market is projected to reach US$44.4 billion in 2026.

The North America medical wellness devices market is driven by rising chronic disease prevalence, growing adoption of wearable health technologies, expanding remote patient monitoring, and increasing demand for preventive healthcare solutions.

The North America medical wellness devices market is expected to grow at a CAGR of 7.1% from 2026 to 2033.

Key opportunities lie in AI-powered personalized wellness devices, telehealth integration, connected remote patient monitoring platforms, and expansion of home-based digital healthcare solutions.

Abbott, 3M Company, Dexcom, Inc., F. Hoffmann-La Roche AG, and Koninklijke Philips N.V are the leading players.