- Metalworking & Fabrication

- Metal Sanding Machines Market

Metal Sanding Machines Market Size, Share and Growth Forecast, 2026 - 2033

Metal Sanding Machines Market by Machine Type (Belt Sanders, Orbital Sanders, Disc Sanders, Others), Power Source (Electric, Pneumatic, Hydraulic), Application (Automotive, Aerospace, Others), and Regional Analysis 2026 - 2033

Metal Sanding Machines Market Share and Trends Analysis

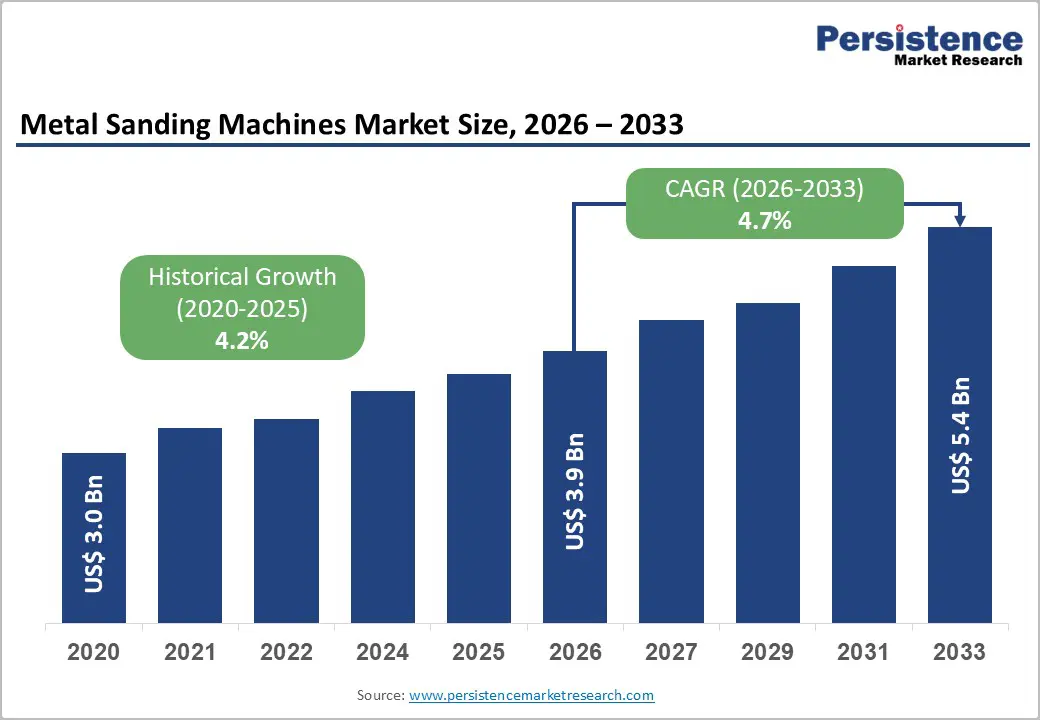

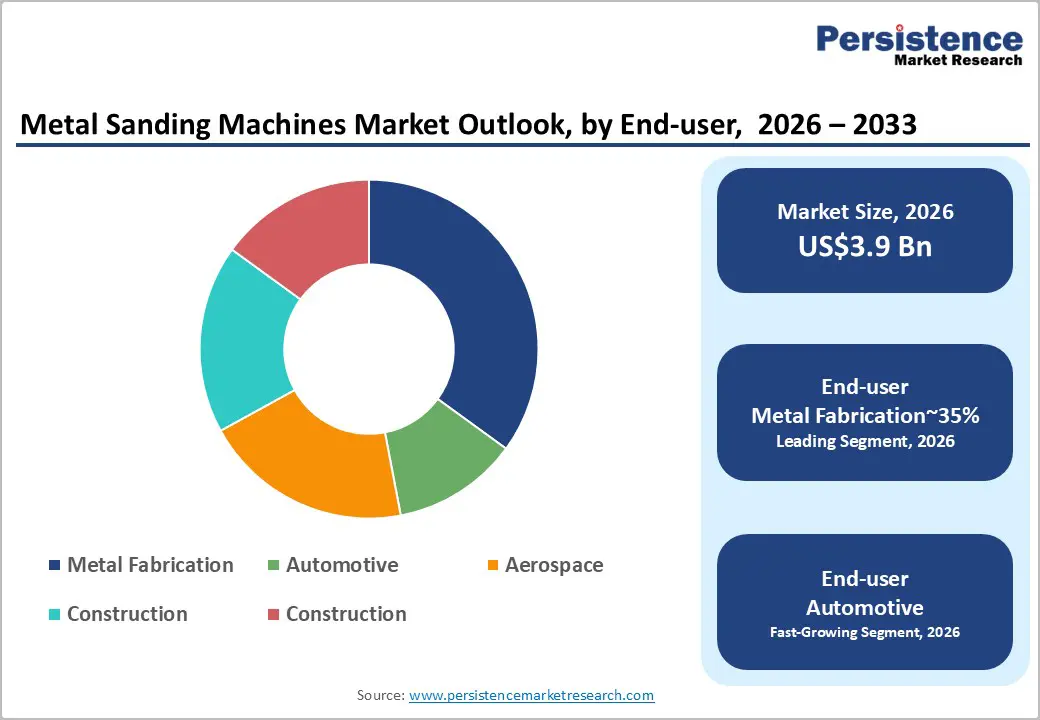

The global metal sanding machines market is likely to be valued at US$3.9 billion in 2026 and is anticipated to reach US$5.4 billion by 2033, growing at a CAGR of 4.7% during the forecast period from 2026 to 2033, driven by the essential role of metal sanding machines in smoothing and finishing surfaces for fabrication and assembly processes.

Increasing global metal fabrication activities are boosting equipment procurement, while the recovery in automotive production is further driving demand for high-precision sanding in component manufacturing. Stringent workplace safety and ventilation regulations are also encouraging the adoption of advanced dust-controlled systems. The integration of automation and robotic sanding solutions is enhancing operational efficiency, supporting steady market expansion over the forecast period.

Key Industry Highlights:

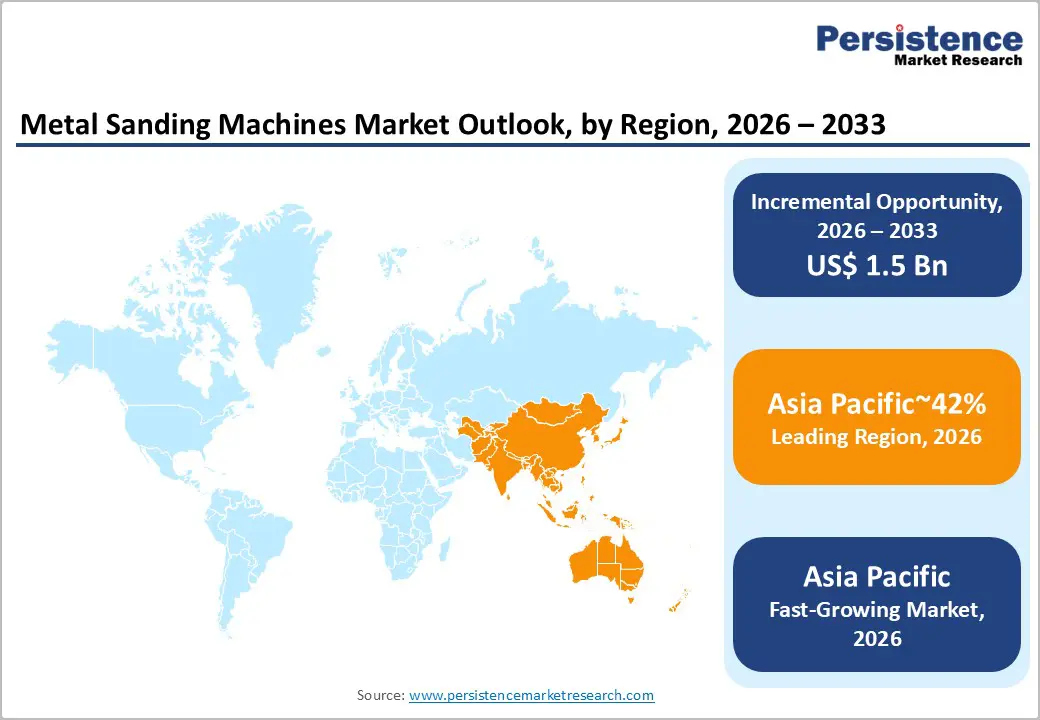

- Leading Region: Asia Pacific is projected to lead due to massive infrastructure investments and manufacturing corridor expansion, accounting for approximately 42% share in 2026, supported by strong industrial ecosystems and capital-intensive production capacity.

- Fastest-growing Region: Asia Pacific is anticipated to grow the fastest due to sustained manufacturing output expansion, policy alignment, and increasing automotive component demand across domestic and export markets.

- Leading Application: Metal fabrication is expected to lead, accounting for approximately 35% in 2026, through high industrial adoption, enhanced throughput efficiency, superior surface quality, and integration across high-value structural applications.

- Leading Machine Type: Belt sanders are projected to dominate for operational simplicity, cost-efficiency, and broad industrial usability, holding approximately 42% in 2026.

- Leading Power Source: Electric power sources are projected to dominate, due to operational versatility, cost-efficiency, and compatibility across industrial use-cases, with approximately 63% in 2026.

- Competitive Environment: Major vendors actively pursue strategic acquisitions to consolidate advanced abrasive technology portfolios. Geographic expansion into emerging manufacturing hubs remains a primary focus for established providers, ensuring localized supply chains.

DRO Analysis

Driver - Aerospace Component Precision Requirements

Aircraft manufacturing demands uncompromising surface integrity to ensure structural reliability. Consequently, procurement patterns favor specialized equipment capable of achieving micro-level finish tolerances. Regulatory bodies continuously update certification criteria for aviation components, necessitating upgraded workshop technology. This regulatory pressure sustains a consistent upgrade cycle across international aviation supply chains.

Bosch's Professional Orbital Sander provides an example of enhanced vibration control targeting precise applications. Market participants increasingly tailor their engineering to meet these strict aerospace specifications. High-tolerance requirements establish a lucrative niche for advanced tool providers. The segment is set to expand alongside global fleet modernization efforts.

Industrial Infrastructure Expansion

Global investment in heavy industry pipelines directly accelerates tool utilization. Structural steel processing requires heavy-duty material removal before welding and coating phases. International labor organizations emphasize hazard reduction in these demanding environments, driving the transition toward ergonomic machinery. These dynamic anchors baseline consumption across rapidly developing construction markets.

Makita with 9403 Belt Sander illustrates the focus on high-capacity material removal under continuous load. Vendors strategically align their portfolios to address rigorous site conditions. Consistent urbanization programs provide a reliable foundation for long-term equipment orders. This trend continues to solidify the market's commercial baseline.

Restraint - High Capital Expenditure for Automated Systems

Implementing fully integrated robotic finishing cells requires substantial initial capital deployment. Small and medium enterprises frequently lack the financial flexibility to transition away from manual units. This economic reality limits the total addressable market for high-end automated solutions. Financing constraints restrict broader adoption across developing manufacturing regions globally.

Dynabrade's Robotic Sanding Head represents the advanced tier of equipment that remains inaccessible to smaller fabricators. Value-focused consumers delay upgrades, extending the lifecycle of existing manual inventories. This financial barrier bifurcates the industry into premium and economy tiers. Widespread automation adoption is likely to proceed gradually.

Transition to Cordless Power Tools

Advancements in lithium-ion battery density unlock unprecedented mobility for industrial users. Worksite safety initiatives encourage the elimination of trip hazards associated with traditional pneumatic or corded electric systems. This technology inflection point generates a massive replacement cycle opportunity. Contractors increasingly prioritize untethered operation for complex structural installations.

DeWalt with FlexVolt Sander captures this exact shift toward high-capacity mobile performance. Providers capturing early market share in industrial-grade battery platforms secure long-term ecosystem lock-in. The convenience factor drives premium pricing acceptance among commercial buyers. This technological transition is anticipated to redefine baseline expectations.

Opportunity - Integration of IoT in Metal Fabrication

Industry 4.0 principles present a transformative pathway for preventative maintenance in heavy usage scenarios. Sensor-equipped machinery can transmit real-time wear data, minimizing unexpected operational downtime. Facility managers actively seek these diagnostic capabilities to optimize total asset lifecycle costs. This digital opening creates new recurring revenue models for manufacturers.

Festool's Connected Sander Interface points toward the future of data-driven workshop management. Software integration allows vendors to differentiate beyond mere mechanical specifications. Smart tools represent a highly lucrative frontier for established engineering firms. This digital evolution is projected to attract significant research funding.

Category-wise Analysis

Machine Type Insights

Belt sanders are projected to lead, accounting for approximately 42% share in 2026, underpinned by their unparalleled material removal rates and ability to process large surface areas efficiently. These machines are the workhorses of metal fabrication shops, providing the necessary power for initial surface preparation and stock removal. Makita's 9911 belt sanders demonstrate the versatility of these tools through their compatibility with stationary mounting for precision bench work. Their established presence in heavy industrial settings sustains their primary market position.

Orbital sanders are expected to be the fastest-growing segment, driven by the increasing demand for swirl-free, high-quality finishes in aerospace and decorative metalwork. These machines offer superior control for fine finishing and surface blending, which is increasingly required for modern architectural metals. The utilization of 3M with Trizact abrasive discs highlights how orbital motion paired with structured minerals delivers predictable, high-gloss results. This trend reflects a broader market shift toward precision and aesthetics in metal finishing.

Power Source Insights

Electric power sources are expected to dominate, accounting for approximately 63% share in 2026, anchored by the reliability and constant torque provided by corded industrial equipment. Most stationary metal finishing workstations are designed around electric power to ensure uninterrupted operation during high-volume production cycles. Bosch's GCD18V-14 dry cut saws showcase how electric motor technology is evolving to handle heavy metalworking tasks with extreme precision. The ubiquity of electrical infrastructure in factories reinforces this segment's long-term dominance.

Electric power is anticipated to be the fastest-growing segment, driven by significant advancements in brushless motor efficiency and lithium-ion battery density. The ability to perform heavy-duty metal finishing without the restrictions of a power cord is transforming maintenance and onsite fabrication workflows. Makita's brushless XGT platforms provide performance comparable to corded counterparts, enabling mobile professional use. This growth is fueled by the industrial sector's need for greater mobility and the elimination of workplace tripping hazards.

Application Insights

Metal fabrication is projected to lead, accounting for approximately 35% share in 2026, supported by the continuous expansion of structural steel projects and heavy equipment manufacturing. This segment relies heavily on high-torque machines for deburring and surface leveling in demanding industrial environments. The performance of 3M with Scotch-Brite PSG products illustrates how specialized abrasives integrated into fabrication workflows enhance finishing consistency. Such dominance is anchored by the sheer volume of metal processing required in global infrastructure development.

The automotive segment is anticipated to be the fastest-growing segment, driven by the rising production of electric vehicles and the widespread use of lightweight aluminum components. Precision finishing is crucial in this sector to ensure the structural integrity of battery enclosures and complex body panels. The introduction of Makita's XGT metalworking tools provides the high-voltage performance needed for rapid material removal on assembly lines. This growth trajectory is further accelerated by the automotive industry's pivot toward highly automated, battery-powered production tools.

Regional Analysis

Asia Pacific Metal Sanding Machines Market Trends

Asia Pacific is expected to be the leading market region, accounting for approximately 42% share in 2026, supported by rapid industrialization and the presence of the world's largest automotive and electronics manufacturing hubs. The region is also anticipated to be the fastest-growing market, driven by massive infrastructure investments and 0.7% quarterly growth in regional manufacturing production as reported by UNIDO in 2025. Large-scale infrastructure investments accelerate demand for advanced metal finishing equipment across industrial hubs.

Manufacturing growth momentum strengthens the adoption of automated and high-efficiency Sanding machines. Market dynamics reflect the integration of precision tooling within high-volume production environments.

China Metal Sanding Machines Market Trends

China is expected to dominate, driven by the expanding metal fabrication industry and rising electric vehicle production capacity. 3M Company strengthens its presence through precision abrasives used in advanced finishing applications. Increasing adoption of robotic automation enhances production efficiency across industrial facilities. Demand for high-performance finishing systems continues to rise within large-scale manufacturing clusters. The trend of robotic automation continues to accelerate industrial output.

India Metal Sanding Machines Market Trends

India is anticipated to lead, supported by national manufacturing initiatives and tightening industrial safety regulations. Makita Corporation expands cordless tool adoption within the shipbuilding and heavy fabrication sectors. Growing focus on worker safety increases demand for advanced and mobile finishing equipment. Market trends emphasize scalable solutions aligned with expanding industrial corridors.

North America Metal Sanding Machines Market Trends

North America is projected to remain a structurally stable market, with demand anchored in the aerospace and defense sectors. The region's focus on high-precision manufacturing and strict environmental standards sustains the adoption of premium, dust-controlled finishing systems.

U.S. Metal Sanding Machines Market Trends

The U.S. is expected to dominate, driven by manufacturing resurgence and the expansion of semiconductor and battery facilities. Stanley Black & Decker Inc. strengthens professional metalworking solutions through strategic investments. Reshoring trends accelerate demand for automated sanding and finishing equipment. Integration of advanced machinery enhances productivity across industrial manufacturing sectors.

Canada Metal Sanding Machines Market Trends

Canada is anticipated to maintain a stable share of the North American market, driven by the robust mining and aerospace industries in Ontario and Quebec. Bosch's 18V cordless platforms are increasingly utilized in remote maintenance operations within the Canadian energy sector. Growing demand for lightweight metals in transportation fuels the uptake of specialized finishing machines.

Europe Metal Sanding Machines Market Trends

Europe is projected to remain a technologically advanced market, where demand is anchored in the high-end automotive industry and stringent EU environmental mandates. The market is increasingly focused on energy efficiency and low-vibration machinery to comply with regional labor protection laws.

Germany Metal Sanding Machines Market Trends

Germany is expected to dominate, driven by strong mechanical engineering output and industrial innovation capabilities. Robert Bosch GmbH advances safety-focused tooling technologies widely adopted in metalworking applications. Transition toward carbon-neutral manufacturing influences the design of energy-efficient machines. Industrial demand remains anchored in high-precision automotive and engineering sectors. The shift toward carbon-neutral manufacturing processes continues to influence machine design.

U.K. Sanding Machines Market Trends

The U.K. is anticipated to lead, supported by the modernization of aerospace and maritime manufacturing infrastructure. Makita Corporation enhances productivity through advanced brushless motor technologies. Investment in offshore wind fabrication increases demand for heavy-duty metal finishing equipment. Market trends emphasize compliance with safety standards and efficiency in industrial operations.

Competitive Landscape

The global metal sanding machines market remains moderately fragmented, with leading manufacturers leveraging automation depth and established procurement networks across industrial sectors. TRUMPF expands capabilities through Flex Cell automation, enabling integrated sheet metal processing workflows. Amada Co., Ltd. strengthens precision engineering standards across complex fabrication applications. Schuler Group aligns investments with electric vehicle manufacturing requirements, enhancing forming efficiency and system reliability.

Value-oriented manufacturers focus on hydraulic and pneumatic systems, addressing cost-sensitive fabrication environments. Mayville Engineering Company accelerates expansion through acquisitions, strengthening regional market access and service capabilities. Innovation centers on predictive maintenance, digital twins, and real-time production analytics.

Key Industry Developments:

- In April 2026, 3M Company announced the deployment of an AI-powered assistant, "Ask 3M," to accelerate industrial customer innovation in material selection for metal finishing. This digital transformation allows metal fabricators to simulate sanding performance and material durability in real-time, drastically reducing the trial-and-error phase in high-precision finishing.

Companies Covered in Metal Sanding Machines Market

- TRUMPF Group

- Amada Co., Ltd.

- Schuler AG

- DMG Mori

- JIER Machine-Tool Group

- Bosch Professional

- Stanley Black & Decker

- Makita Corporation

- 3M

- Dynabrade Inc.

- Mayville Engineering Company

- Bystronic Group

- Prima Industrie S.p.A.

- Salvagnini Group

- LVD Group

- Durma Machinery

Frequently Asked Questions

The global metal sanding machines market is likely to be valued at US$3.9 billion in 2026 and is anticipated to reach US$5.4 billion by 2033.

As machines become more complex with digital controls and automated features, a lack of certified personnel limits effective utilization of high-end equipment, leading to underperformance, higher maintenance costs, and hindered full-scale adoption globally.

The metal sanding machines market is forecast to grow at a CAGR of 4.7% from 2026 to 2033.

Asia Pacific leads with approximately 42% share and is also the fastest-growing region, driven by rapid industrialization in 2026, massive infrastructure investments, and steady manufacturing output expansion.

Key players include TRUMPF Group, Amada Co., Ltd., Schuler AG, DMG Mori, Bosch Professional, Stanley Black & Decker, Makita Corporation, 3M, Dynabrade Inc., and Mayville Engineering Company.