- Metals & Minerals

- Metal Injection Molding Market

Metal Injection Molding Market Size, Share, and Growth Forecast 2026 - 2033

Metal Injection Molding Market by Material Type (Stainless Steel, Low Alloy Steel / Carbon Steel, Soft Magnetic Materials, Titanium Alloys, Cobalt Alloys, Tungsten Alloys, Ceramics, and Others), End-user (Automotive, Electrical & Electronics, Medical & Orthodontics, Consumer Products, Industrial, Firearms & Defence, Aerospace, and Others), and Regional Analysis, 2026 - 2033

Metal Injection Molding Market Size and Trend Analysis

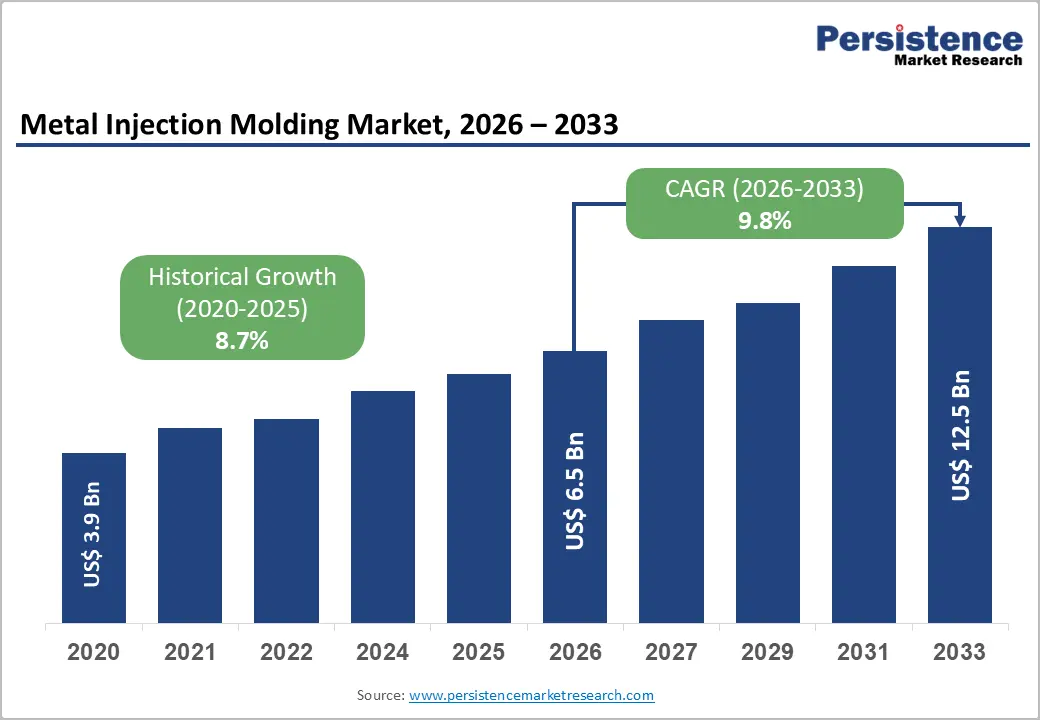

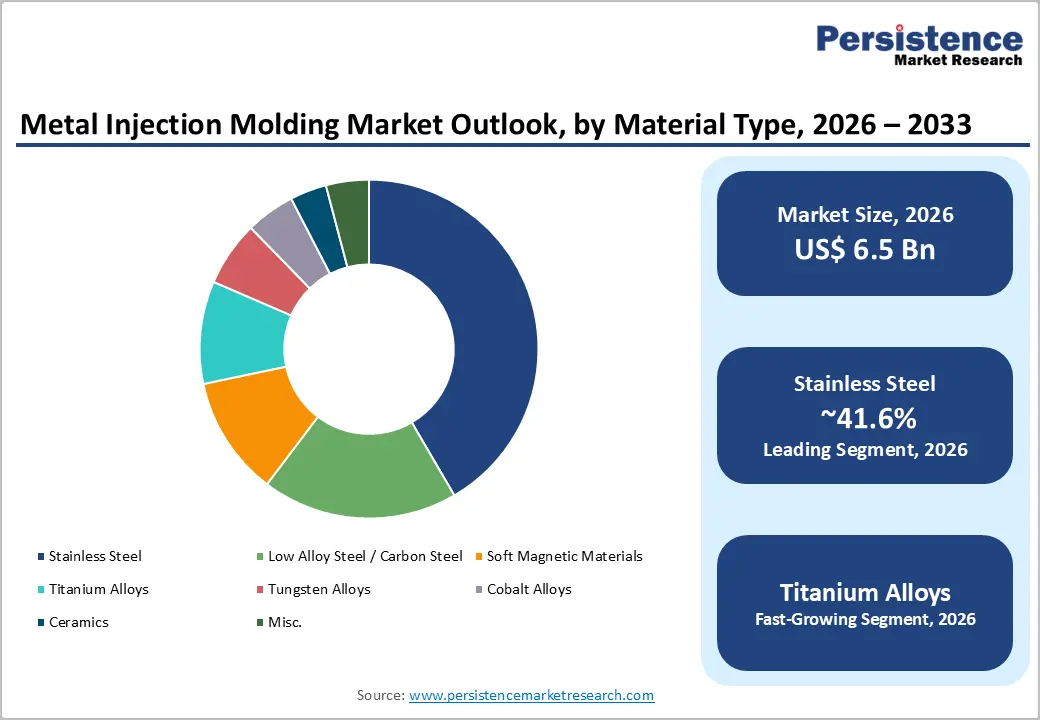

The global metal injection molding (MIM) market size is expected to be valued at US$ 6.5 billion in 2026 and projected to reach US$ 12.5 billion by 2033, growing at a CAGR of 9.8% between 2026 and 2033.

Demand acceleration is primarily driven by the convergence of miniaturisation in consumer electronics, lightweighting mandates in mobility, and the substitution of conventional machining with net-shape manufacturing for complex small components.

According to the International Energy Agency (IEA), global electric car sales surpassed 17 million units in 2024, intensifying requirements for high-precision metallic parts in actuators, sensors and battery enclosures. Simultaneously, the U.S. Food and Drug Administration (FDA) has cleared a record number of orthopaedic and dental devices, where MIM-grade titanium and stainless-steel components offer the geometrical complexity and biocompatibility that traditional fabrication cannot economically deliver.

Key Industry Highlights:

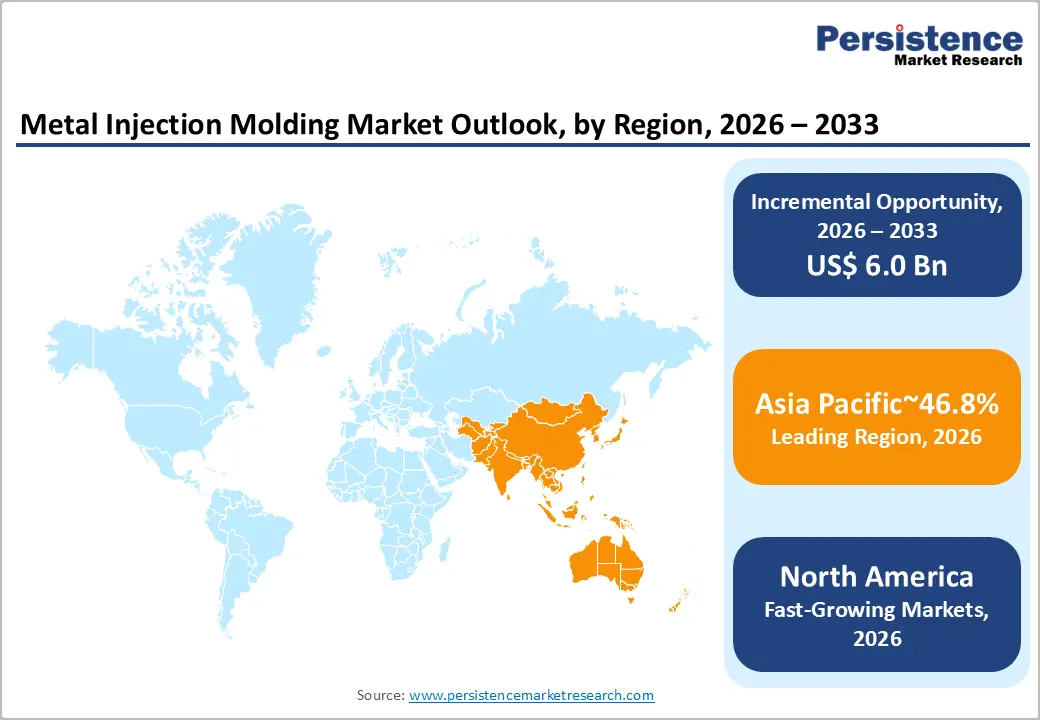

- Leading Region: Asia Pacific dominates the global metal injection molding market with a 46.8% share in 2025, supported by China's vehicle production scale, India's electronics push under the PLI scheme and Japan's precision manufacturing base.

- Fast-Growing Market: Asia Pacific is also the fastest-growing region through 2033, propelled by India's PLI-led US$ 17 billion electronics investment, EV adoption in China, and rising defence outlays across the broader region.

- Dominant Material Type: Stainless steel led the material category with a 42% share in 2025, driven by 316L and 17-4 PH adoption in medical, firearms, and automotive applications certified to U.S. FDA and ISO 5832-1 standards.

- Fast-Growing Material Type: Titanium alloys are the fastest-growing material with a CAGR of 10% between 2026 and 2033, propelled by aerospace lightweighting and orthopedic implant volumes from AIA, ASD and FDA-aligned demand.

- Key Opportunity: Soft magnetic MIM components for EV motors and inverters represent a high-value opportunity, supported by the U.S. CHIPS Act's US$ 52 billion and India's PLI funding for next-generation electrification platforms.

DRO Analysis

Drivers - Electrification of Mobility Intensifying Demand for Net-shape Metallic Components

The shift toward electrified powertrains are reshaping component sourcing in the automotive industry, where MIM is replacing machining and casting for small, intricate parts inside e-motors, sensors, and battery management systems. Per the IEA Global EV Outlook 2024, electric car sales reached 17 million units globally in 2024, with China alone contributing close to 11 million plug-in vehicles.

European Automobile Manufacturers' Association (ACEA) data shows battery-electric vehicles captured a 13.6% share of new EU registrations in 2024, surpassing diesel for the first time. Each EV typically integrates 35-50% more high-precision metal micro-components than an internal combustion vehicle, directly enlarging the addressable opportunity for tungsten, soft magnetic and stainless steel MIM parts.

Medical Device Innovation Reinforcing the Adoption of Biocompatible MIM Alloys

Growth in implantable devices, surgical instruments, and orthodontic hardware is firmly anchoring demand for titanium and 316L stainless steel MIM components. According to the U.S. FDA, more than 3,200 510(k) device clearances were granted in 2024, with orthopedic and dental subcategories being among the most active.

The Organisation for Economic Co-operation and Development (OECD) reports that healthcare expenditure across member states averaged 9.2% of GDP in 2023, with a clear shift toward minimally invasive procedures requiring micro-scale components. MIM enables sub-millimetre wall thicknesses and complex undercuts, helping medical OEMs cut machining cycle times by 40-60% while maintaining the surface integrity required for ISO 13485 compliance.

Restraints - High Capital Intensity and Feedstock Cost Volatility

The MIM process demands significant upfront investment in debinding furnaces, sintering equipment and tooling, with greenfield production lines often requiring US$ 8-15 million in capex before reaching nameplate capacity.

According to the London Metal Exchange (LME), nickel prices fluctuated by over 35% during 2024, while cobalt and tungsten APT prices remained structurally elevated due to concentrated supply from the Democratic Republic of Congo and China. Such feedstock volatility compresses converter margins and discourages smaller fabricators from scaling. Long qualification cycles, often 18-24 months for automotive and aerospace approvals, further extend payback horizons, particularly for first-time MIM adopters.

Geometric and dimensional limitations versus alternative processes

Despite its strengths, MIM is constrained to component weights typically below 100 grams and wall thicknesses under 10 mm, limiting its applicability for larger structural parts. Sintering shrinkage of 15-20% also introduces dimensional tolerance challenges, with achievable accuracy generally bounded at ±0.3-0.5% of nominal, tighter than casting but looser than precision machining.

Competition from metal additive manufacturing (binder jetting and laser powder bed fusion), which the ASTM International F42 Committee notes is achieving comparable density at falling unit costs, is gradually eroding MIM's exclusivity in low-volume complex geometries, particularly in aerospace prototyping and customised medical implants.

Opportunities - Titanium MIM unlocking high-value aerospace and orthopaedic platforms

Titanium-based MIM, identified as the fastest-growing material segment with a projected CAGR of 10% between 2026 and 2033, presents a substantial whitespace for converters investing in low-oxygen processing capability.

The Aerospace Industries Association (AIA) 2025 Facts & Figures report records the U.S. A&D industry generating US$ 995 billion in business activity with exports of US$ 138.6 billion in 2024, much of it tied to lightweight titanium content. The ASD reports European A&D turnover at €325.7 billion in 2024, up 10.1% year-on-year. Concurrent demand from orthopaedic implant makers, where Ti-6Al-4V ELI is the standard, creates dual-use scale economics for MIM houses able to certify to AS9100 and ISO 13485 simultaneously.

Soft magnetic MIM components powering next-generation electrification

The pivot toward higher-efficiency motors, EV inverters and inductive charging is generating an attractive runway for soft magnetic MIM parts based on Fe-Si, Fe-Ni and Fe-Co systems. The International Renewable Energy Agency (IRENA) projects that global electric motor stock for industrial and mobility applications will need to be substantially upgraded to meet IEC IE4/IE5 efficiency classes by 2030.

India's Production Linked Incentive (PLI) scheme, with US$ 17 billion allocated across semiconductor and electronics components, and the U.S. CHIPS and Science Act's US$ 52 billion commitment, are channelling investment into domestic component ecosystems where MIM stators, rotor laminates and EMI shielding parts deliver superior magnetic performance versus stamped laminations, particularly in compact axial-flux topologies.

Category-wise Analysis

Material Type Insights

Stainless steel retains the dominant position within the material mix, and is likely to account for an estimated 42% share of the global metal injection molding market in 2026. Its leadership reflects the alloy family's unmatched balance of corrosion resistance, mechanical strength, biocompatibility, and feedstock availability. Grades such as 316L, 17-4 PH, and 420 are widely qualified across medical, firearms, consumer electronics, and automotive fuel-system components.

The World Steel Association reports global stainless steel melt production reached 58.4 million tonnes in 2023, ensuring a stable feedstock supply. In addition, U.S. FDA and ISO 5832-1 certifications for 316L have made it the default choice for surgical staplers, orthodontic brackets and laparoscopic tooling, where MIM offers consistent metallurgy at scale.

End-user Insights

Automotive stands as the leading end-use vertical, accounting for an estimated 27% share of the global MIM market in 2025. The segment's dominance is anchored in the high parts-per-vehicle intensity of MIM components, turbocharger vanes, fuel injector parts, transmission shifter elements, airbag components, and seat-belt locks.

According to the International Organisation of Motor Vehicle Manufacturers (OICA), global vehicle production exceeded 75.5 million units in 2024, while the IEA reports EV sales of 17 million in the same year. Each modern vehicle contains 80-150 MIM parts on average, with electrified platforms pushing the upper end. Tier-1 supplier consolidation around precision powertrain and ADAS subsystems further entrenches MIM as the cost-efficient process for sub-50-gram steel and tungsten parts.

Regional Insights

North America Metal Injection Molding Market Trends and Insights

North America holds a share of 21.6% in 2025, supported by a deeply embedded medical device manufacturing base in the U.S., defence procurement under the U.S. Department of Defence, and ongoing reshoring of precision component production. Trends include accelerating qualification of MIM titanium for orthopaedic implants, integration with hybrid additive workflows, and Mexico's rise as a near-shore MIM cluster serving North American Tier-1 automotive suppliers.

U.S. Metal Injection Molding Market Size

The U.S. Metal Injection Molding market is valued at US$ 1,101.1 Mn in 2025, driven by concentrated demand from medical device OEMs in Massachusetts and Minnesota, defence small-arms procurement supporting firearms MIM volumes, and the orthopaedic implant cluster in Warsaw, Indiana.

The AIA 2025 Facts & Figures report's US$ 138.6 billion in A&D exports and FDA clearances of over 3,200 510(k) devices in 2024 directly translate into sustained MIM specification on critical-application components.

Europe Metal Injection Molding Market Trends and Insights

Europe holds a share of 24.1% in 2025, anchored by Germany's automotive Tier-1 ecosystem, Switzerland's watch and precision instruments base, and pan-European defence expansion. Per ASD, the European A&D industry generated €325.7 billion in 2024, with defence turnover up 13.8% year-on-year to €183.4 billion, sustaining demand for MIM components in firearms, missile sub-assemblies, and military aero-engine accessories.

Germany Metal Injection Molding Market Size

Germany's Metal Injection Molding market is valued at US$ 386.8 Mn in 2025, driven by its powertrain and chassis component supply chain serving Volkswagen Group, BMW and Mercedes-Benz, alongside its dental implant cluster. According to the VDA, German vehicle production reached 4.1 million units in 2024, while VDMA highlights mechanical engineering as a €260 billion sector, both directly underwriting MIM consumption in transmission, fuel and actuator parts.

U.K. Metal Injection Molding Market Size

The U.K. Metal Injection Molding market is valued at US$ 211.9 Mn in 2025, driven by aerospace primes such as Rolls-Royce and BAE Systems, the country's medical-technology corridor across Cambridge and Oxford, and consumer electronics OEMs. The ADS Group reports U.K. aerospace turnover of £40 billion in 2024, sustaining MIM demand for fuel-system, cabin and actuator components.

Asia Pacific Metal Injection Molding Market Trends and Insights

Asia Pacific holds a share of 46.8% in 2025, the largest of any region, anchored by China's dominance as the global hub for MIM tonnage, Japan's precision component base, and rising clusters in South Korea, India and Southeast Asia. Per OICA, China produced over 31 million vehicles in 2024, while the region accounted for nearly 46 million units of total automotive output, driving MIM demand across powertrain, electronics and consumer goods.

China Metal Injection Molding Market Size

China's metal injection molding market size is likely to be valued at US$ 1,349 Mn in 2026, driven by its 23 million units of car sales, 31% of global volume per IEA/OICA and its position as the world's largest smartphone and consumer electronics manufacturing base. Concentrated MIM clusters in Guangdong, Jiangsu, and Zhejiang serve Apple, Huawei, and BYD supply chains, with hinge, frame, and connector components leading in volume.

India Metal Injection Molding Market Size

India's metal injection molding market size is valued at US$ 472.2 Mn in 2026, driven by the PLI scheme's US$ 17 billion allocation across semiconductors and electronics, 21-fold growth in mobile phone production to US$ 49.3 billion, and 4.8% growth in car sales in 2024. The Make in India programme and the Defence Production and Export Promotion Policy 2020, targeting US$ 23.49 billion in revenue underpin MIM demand in firearms, electronics and automotive.

Competitive Landscape

The global Metal Injection Molding market is moderately fragmented, with the top 10 players accounting for an estimated 35-40% of revenue while regional and application-specialist converters hold the balance. Leading players differentiate via proprietary feedstock chemistry, in-house tooling, multi-alloy capability and certifications spanning AS9100, ISO 13485, and IATF 16949.

Strategic moves cluster around capacity additions in India and Mexico, vertical integration into binder formulation, M&A targeting niche titanium specialists, and hybrid platforms combining MIM with metal additive printing. R&D priorities include reducing sintering energy intensity, expanding tungsten-heavy alloy portfolios for defence, and qualifying new soft magnetic compositions for EV traction motors.

Key Developments:

- In 2024, INDO-MIM Pvt. Ltd. partnered with HP Inc. to deploy advanced HP Metal Jet S100 3D printers at its Bengaluru, India and Texas, U.S. facilities to enhance large-scale production of high-precision metal parts

- April 30, 2025, The Schunk Group strengthened its position in the Metal Injection Molding (MIM) market by highlighting its advanced MIM capabilities for producing highly complex and precision-engineered metal components at scale, leveraging over 100 years of material expertise and state-of-the-art injection molding technology to deliver end-to-end solutions from material development to heat treatment and quality assurance, with a strong focus on high-performance applications in sectors such as power electronics where copper-based MIM components enhance conductivity and thermal efficiency.

Metal Injection Molding Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 3.9 Billion |

| Current Market Value (2026) | US$ 6.5 Billion |

| Projected Market Value (2033) | US$ 12.5 Billion |

| CAGR (2026 - 2033) | 9.8% |

| Leading Region | Asia Pacific, 46.8% |

| Dominant Material Type | Stainless Steel, 42% |

| Top-ranking End-user | Automotive, 27% |

| Incremental Opportunity | US$ 6.0 Billion (2026 - 2033) |

Companies Covered in Metal Injection Molding Market

- INDO-MIM

- Dynacast (Form Technologies)

- GKN Automotive Limited (GKN Powder Metallurgy)

- Schunk Mobility (Schunk Sinter Metals)

- CMG Technologies

- Sintex

- ARC Group Worldwide

- Epson Atmix Corporation

- NIPPON PISTON RING Co., Ltd.

- Phillips-Medisize

- Rockleigh Industries

- Robert Bosch GmbH

Frequently Asked Questions

The global Metal Injection Molding market is expected to be valued at US$ 6.5 billion in 2026, on track to reach US$ 12.5 billion by 2033 at a CAGR of 9.8%.

Demand is driven by the electrification of mobility 17 million EV sales in 2024 per IEA rising medical device clearances by the U.S. FDA, and substitution of conventional machining with net-shape MIM for complex small components.

Asia Pacific leads with a 46.8% share in 2025, anchored by China's MIM tonnage, India's PLI-driven electronics expansion, and Japan's precision manufacturing ecosystem serving automotive, electronics and medical OEMs.

Soft magnetic and titanium MIM components for EV motors, inverters and aerospace/orthopedic platforms represent the most significant opportunities, supported by the U.S. CHIPS Act's US$ 52 billion and India's PLI funding.

Key players include Indo-MIM, Form Technologies (Optimim, Dynacast), ARC Group Worldwide, Sintex a.s., NIPPON PISTON RING, Schunk Sinter Metals, Epson Atmix, Sandvik AB, and Phillips-Medisize.