Industry: Chemicals and Materials

Published Date: January-2025

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 189

Report ID: PMRREP35114

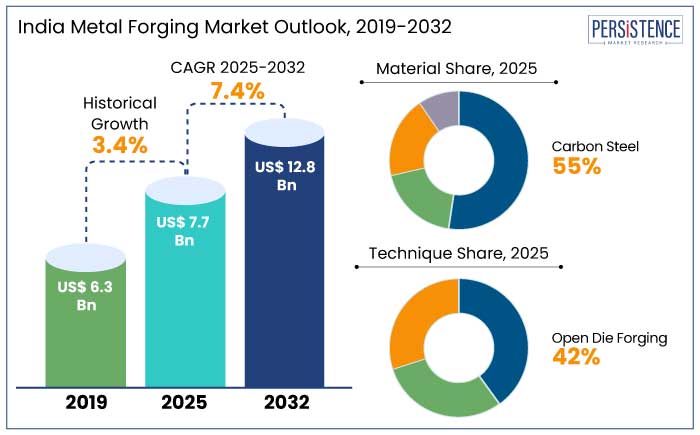

The India metal forging market is estimated to increase from US$ 7.7 Bn in 2025 to US$ 12.8 Bn by 2032. The market is projected to record a CAGR of 7.4% during the forecast period from 2025 to 2032.

The India metal forging industry is anticipated to surge due to rising demand from key industries, such as automotive and aerospace. The automotive industry in India is projected to rise at a CAGR of 10 to 12%. It is anticipated to fuel demand for forged components such as engine parts, transmission systems, and chassis parts.

Automotive and aerospace industries increasingly demand lighter yet stronger forged materials like aluminum and titanium to improve fuel efficiency and performance. The use of aluminum in vehicles has grown significantly, with aluminum parts making up about 10 to 12% of the average vehicle weight.

Key Highlights of the Market

|

Market Attributes |

Key Insights |

|

India Metal Forging Market Size (2025E) |

US$ 7.7 Bn |

|

Projected Market Value (2032F) |

US$ 12.8 Bn |

|

India Market Growth Rate (CAGR 2025 to 2032) |

7.4% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

3.4% |

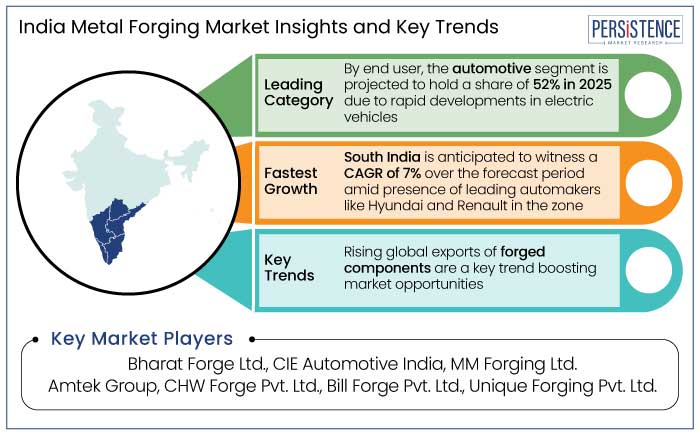

South India is projected to dominate by accounting for around 40% of the India metal forging market share in 2025. It is estimated to rise at a CAGR of 7% over the forecast period. It is a key industrial hub mainly due to its strong automotive sector, which is the largest consumer of forged components.

South India, especially Tamil Nadu, is known for its robust automotive manufacturing base. Global companies like Hyundai, Ford, and Renault operate their factories from the state. The automotive sector requires high-quality forged components for engines, transmission systems, and chassis parts, which significantly boosts the demand for metal forging.

South India also has a high concentration of forging units and suppliers, primarily in states like Tamil Nadu and Karnataka. These states have well-established forging clusters serving various industries, including automotive, defense, aerospace, and heavy machinery.

South India has a well-developed infrastructure, with a robust transportation network, ports, and logistical facilities, which support the smooth flow of raw materials and finished products for the metal forging industry. The zone benefits from favorable government policies under initiatives like Make in India and Atmanirbhar Bharat. Such policies encourage the growth of manufacturing and industrial sectors and drive demand for forged components.

Based on material, the market is divided into carbon steel, alloy steel, and stainless steel. Out of these, the carbon steel segment is projected to lead with 55% of the market share in 2025. This is due to its widespread use across various sectors, especially automotive, industrial machinery, and construction.

Carbon steel is one of the most cost-effective materials for forging. Its affordability, strength, and durability make it the preferred choice in industries looking for a balance between performance and cost. Carbon steel can be easily forged into complex shapes and sizes. It is highly versatile and suitable for various applications, from automotive parts to industrial machinery.

Carbon steel provides an excellent strength-to-weight ratio, making it ideal for parts that need to withstand high loads without adding excessive weight, which is particularly valuable in the automotive and industrial sectors. Growth of the automotive industry in India is a significant driver of demand for carbon steel.

As vehicle production increases, especially for commercial vehicles and two-wheelers, demand for carbon steel forged components is likely to rise. India’s focus on infrastructure projects like smart cities, highways, and railways drives demand for carbon steel components in construction machinery and infrastructure equipment. Sectors like mining, energy, and manufacturing require forged carbon steel parts that can endure extreme conditions, driving steady demand from these industries.

Based on technique, the market is segmented into close die forging, open die forging, and ring forging. Among these, the open die forging segment is projected to dominate the market with 42% of share in 2025. This dominance can be attributed to its versatility, cost-effectiveness, and the types of components it produces.

Open die forging allows for the production of a wide range of parts in terms of size, shape, and material. It is especially suitable for large and heavy components, which is why it is extensively adopted for the automotive, aerospace, defense, and heavy machinery sectors.

The open die forging technique can be used for various materials, including carbon steel, alloy steel, stainless steel, and titanium. Such broad material compatibility is crucial for industries that require specific performance attributes.

Open die forging is also well-suited for large components such as shafts, crankshafts, flanges, axles, and rollers, which are commonly used in the automotive, mining, and construction industries. Significant demand for large-scale components, along with cost-effective tooling and material flexibility, ensures that open die forging will continue leading the market over the forecast period.

The India metal forging market is a cornerstone of the country's manufacturing and industrial sectors, serving as a vital link in producing robust and durable components for diverse industries. Forging, a process that involves shaping metal through compressive forces, enhances materials' strength, reliability, and performance.

With India emerging as a global manufacturing hub, demand for forged components has witnessed a significant surge in the automotive, aerospace and defense, railways, industrial machinery, and marine industries. For example,

The market is bolstered by India's booming manufacturing base, government initiatives promoting the Make in India campaign and increasing foreign direct investments (FDIs). Such factors, coupled with developments in forging technology, are transforming the sector, making it a critical contributor to the country's economic growth.

As the country continues strengthening its position as a global manufacturing hub, the forging sector is set to play a pivotal role in shaping India's industrial landscape. With evolving trends such as lightweight materials, automation, and sustainability, the market presents abundant opportunities for innovation and growth, making it a critical component of India's industrial future. For example,

The India metal forging market experienced steady growth from 2019 to 2023, driven by the country's industrial developments and robust demand across key sectors. It witnessed a CAGR of 3.4% in the historical period.

The market steadily evolved from 2019 to 2023, supported by rapid growth of the automotive industry, which accounted for most of the demand for forged components like crankshafts, axles, and transmission parts. Increasing infrastructure development and government initiatives like Make in India further strengthened the manufacturing base, enabling growth. Challenges such as fluctuating raw material prices and limited adoption of unique technologies slowed the pace of growth in certain segments.

The market is set to accelerate significantly over the forecast period, with a projected CAGR of 7.4% from 2025 to 2032. The growth will likely be fueled by developments in forging technologies, such as precision and automation, which enhance efficiency and reduce material wastage.

Rising demand for lightweight and high-strength materials, like aluminum and titanium, from the automotive and aerospace sectors is also set to play a key role. India's rising prominence as a global manufacturing hub and increasing exports of forged components to Europe and North America create lucrative opportunities.

Rising Demand from Automotive Industry to Propel Market Growth

The automotive industry is India's largest consumer of forged components, making it a key growth driver for the India metal forging market. Components like crankshafts, axles, gears, and connecting rods are critical for vehicle performance and durability, driving consistent demand. With India emerging as one of the world's most prominent automotive manufacturing hubs, the production of passenger cars, commercial vehicles, and electric vehicles (EVs) has surged. For example,

The transition toward lightweight vehicles to improve fuel efficiency has increased adoption of forged aluminum components. The ‘Make in India’ initiative and production-linked incentives (PLI) for the automotive sector are further boosting local manufacturing and exports, positioning the forging industry for substantial growth.

Innovations in Forging Technologies to Reshape Growth Trajectories

Technological innovation is reshaping the metal forging industry in India, driving efficiency and productivity. Adoption of precision forging, computer-aided design (CAD), and automation reduces material wastage and enhances the production of high-strength, defect-free components. For example,

Investments in environmentally friendly technologies, such as energy-efficient furnaces, align with global sustainability goals. These developments make India-based forging firms globally competitive, enabling them to meet rising demand from the aerospace, defense, and industrial machinery sectors. Such trends are anticipated to unlock new growth opportunities in the next ten years. For example,

Raw Material Price Volatility to Hamper Market Growth

Volatility in raw material prices, particularly for steel, aluminum, and other forging materials, poses a significant growth restraint for the India metal forging industry. Global market fluctuations, supply chain disruptions, and geopolitical tensions often lead to unpredictable cost variations.

Steel prices have experienced over 30 to 40% surges in specific periods, squeezing profit margins for forging companies. The lack of long-term contracts with suppliers intensifies these challenges, leaving manufacturers vulnerable to sudden price hikes.

Small-scale firms are significantly impacted, as they often lack the financial buffer to absorb increased costs. Rising energy costs also contribute to production expenses, making it challenging for local forging companies to remain competitive in global markets. Addressing this issue requires better supply chain management and strategic sourcing agreements to stabilize raw material costs.

Rising Global Exports of Forged Components to Create New Opportunities

India’s forging industry is rapidly positioning itself as a leading global exporter of high-quality forged components. With competitive production costs and developments in automation, India’s forging firms are catering to rising demand from automotive, industrial machinery, and aerospace sectors in Europe, North America, and Asia Pacific.

Exports have already contributed over 30% to the sector’s total revenue, and this figure is set to rise as manufacturers adopt precision forging technologies and meet international sustainability standards. India’s focus on energy-efficient production methods aligns with global trends, enhancing its attractiveness as a sourcing hub.

India-based firms are now producing forged aluminum components for lightweight vehicles and aircraft in high demand worldwide. By building robust supply chains and fostering partnerships with global OEMs, leading forging firms are projected to further solidify their reputation as key players in the international market.

The India metal forging industry is highly competitive, with several key players focusing on technological developments, quality enhancement, and cost-effectiveness. Companies like Bharat Forge, MandM Ltd., and Ramkrishna Forgings dominate the sector, leveraging state-of-the-art precision forging technologies and automation.

With rising global demand for lightweight forged components, key industry players invest heavily in forged aluminum production. They are set to align their operations with energy-efficient and sustainable manufacturing practices.

Strategic partnerships with global OEMs and focus on global market development are key strategies for leading market players. Broadening in Europe, North America, and Asia Pacific are a few other strategies for securing market share and enhancing competitiveness in the international market.

Recent Industry Developments

|

Attributes |

Details |

|

Forecast Period |

2025 to 2032 |

|

Historical Data Available for |

2019 to 2023 |

|

Market Analysis |

US$ Billion for Value |

|

Key Zones Covered |

|

|

Key Market Segments Covered |

|

|

Key Companies Profiled in the Report |

|

|

Report Coverage |

|

|

Customization and Pricing |

Available upon request |

By Material

By Technique

By End User

By Zone

To know more about delivery timeline for this report Contact Sales

The metal forging industry in India is set to be valued at US$ 12.8 Bn in 2025.

India has an installed forging capacity of around 38.5 lakh MT.

The market is estimated to exhibit a CAGR of 7.4% over the forecast period.

Bharat Forge Ltd., CIE Automotive India, and MM Forging Ltd. are a few key players.

South India is the dominant zone in the India metal forging industry.