- Medical Devices

- Clinical Rollators Market

Clinical Rollators Market Size, Share, and Growth Forecast, 2026 - 2033

Clinical Rollators Market by Product Type (3-Wheeler Rollators, 4-Wheeler Rollators, Others), Material Type (Aluminum Rollators, Others), Application (Mobility Assistance, Rehabilitation, Post-Surgical Recovery, Elderly Care), and Regional Analysis for 2026 – 2033

Clinical Rollators Market Size and Trends Analysis

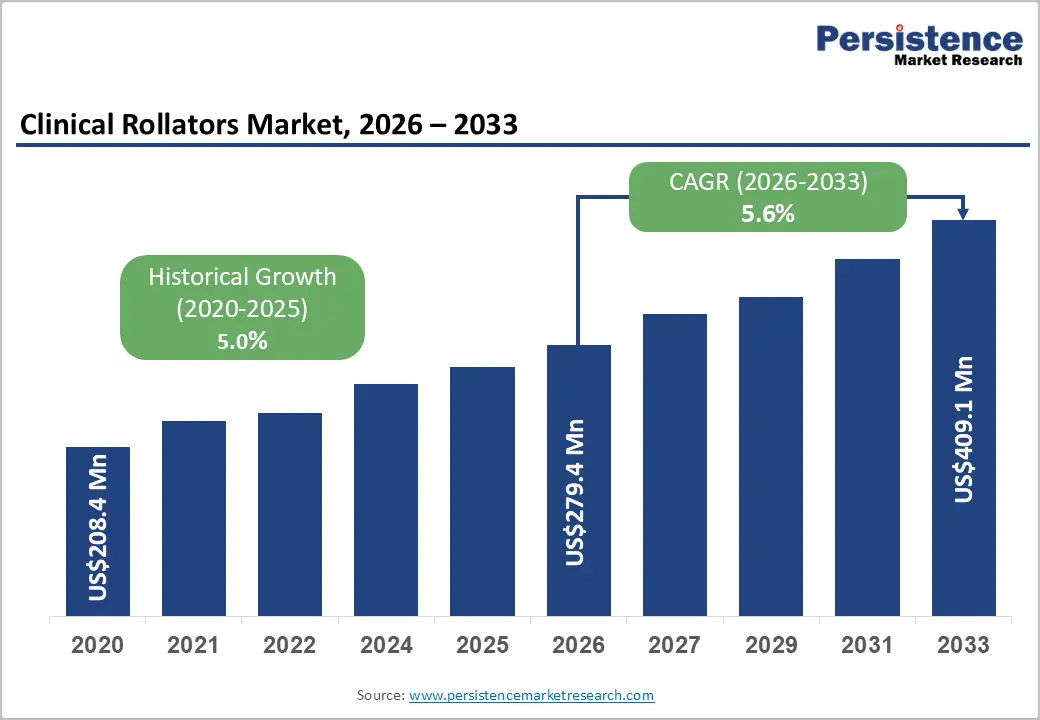

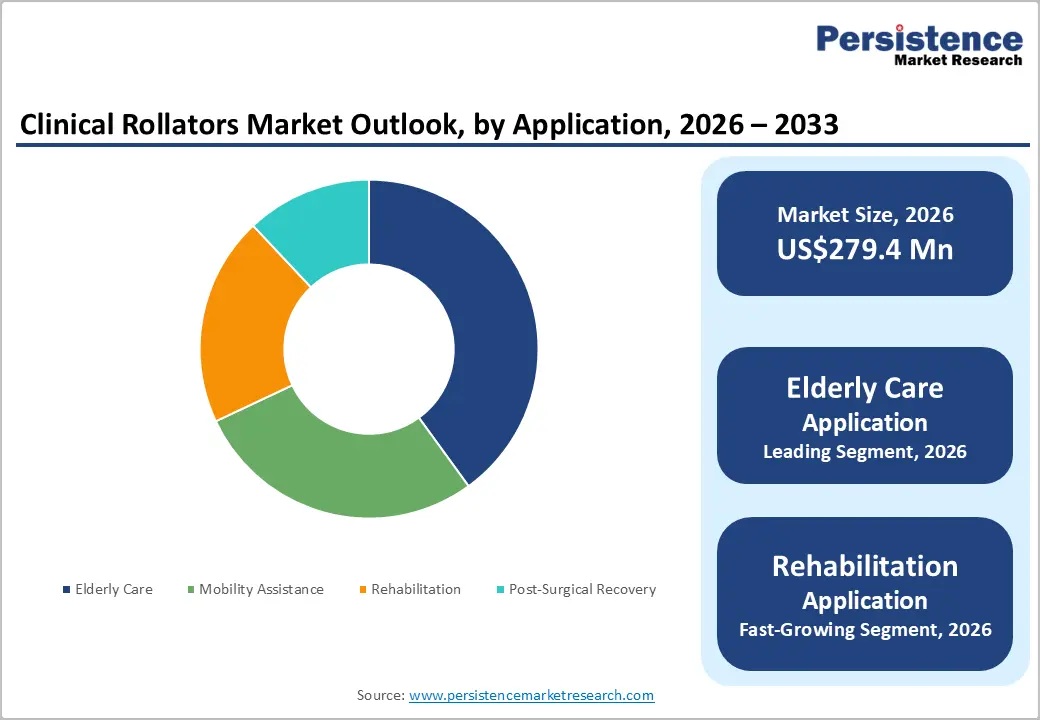

The global clinical rollators market size is likely to be valued at US$279.4 million in 2026, and is expected to reach US$409.1 million by 2033, growing at a CAGR of 5.6% during the forecast period from 2026 to 2033, driven by the intersection of aging global demographics, a rising burden of chronic musculoskeletal and neurological conditions, and growing healthcare system emphasis on mobility-assisted rehabilitation and community-based elderly care that collectively sustain durable structural demand for clinically engineered rolling walker solutions.

Key Industry Highlights:

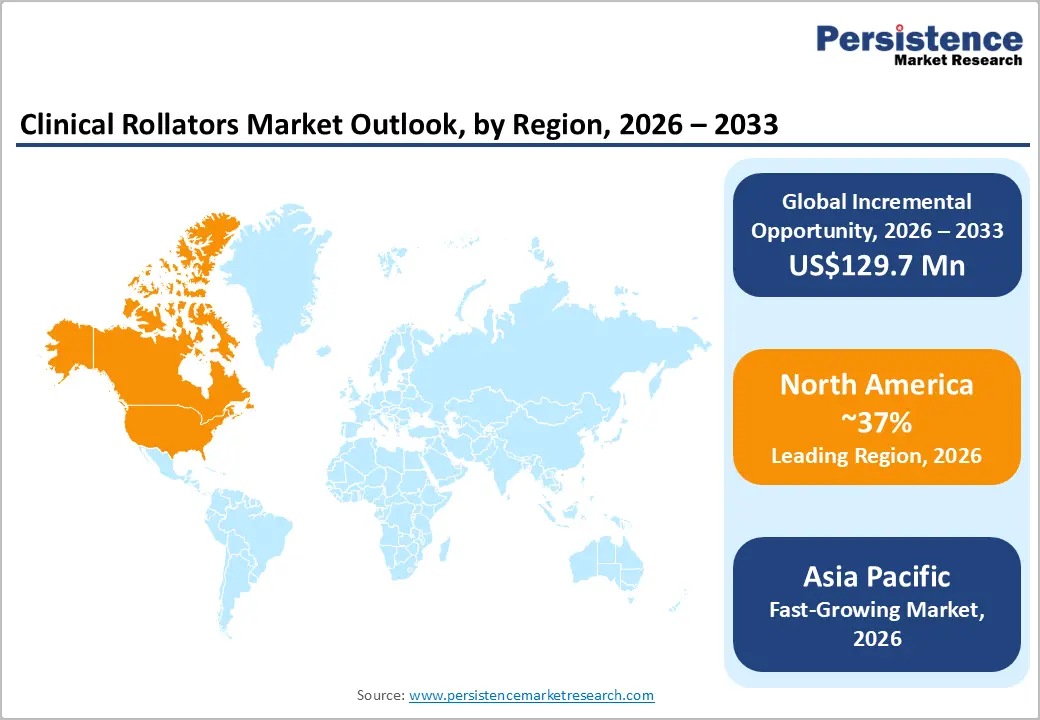

- Dominant Region: North America is expected to dominate the market with approximately 37% revenue share in 2026, supported by the region's large aging population, well-established Medicare and private insurance reimbursement frameworks for durable medical equipment (DME), and the concentrated commercial presence of leading rollator manufacturers in the U.S.

- Fastest-growing Region: Asia Pacific is projected to be the fastest-growing regional market, advancing at a CAGR of approximately 7.1% through 2033, driven by the rapid aging of populations in China and Japan, expanding geriatric healthcare infrastructure, and growing awareness of mobility-assisted rehabilitation in developing healthcare systems across India and Southeast Asia.

- Leading Product Type: 4-wheeler rollators are expected to dominate with approximately 65% share in 2026, reflecting their superior stability, integrated seat and basket functionality, and broad clinical recommendation across mobility assistance, rehabilitation, and elderly care applications.

- Dominant Material Type: Aluminum rollators lead with approximately 58% of material segment revenue in 2026, preferred for their optimal strength-to-weight ratio, rust resistance, and cost-effective manufacturing that supports broad clinical adoption across healthcare settings.

DRO Analysis

Driver - Healthcare System Emphasis on Rehabilitation, Fall Prevention, and Value-based Care

The structural shift of healthcare systems toward value-based care models emphasizing preventive intervention, reduced hospital readmission, shorter acute care length of stay, and patient functional outcome optimization is creating a favorable clinical and reimbursement environment for rollator prescription as a mobility rehabilitation intervention that demonstrably reduces fall incidence, supports faster post-surgical functional recovery, and enables earlier hospital discharge for orthopedic surgery patients.

The growing clinical evidence base linking adequate mobility aid provision to improved rehabilitation outcomes, reduced fall-related injury costs, and extended community living duration for elderly patients provides health technology assessment bodies and insurance reimbursement decision-makers with compelling economic justification for maintaining and expanding coverage for clinical rollator prescription.

Restraint - Patient Stigma and Low Awareness of Rollator Clinical Benefits

Patient reluctance to adopt rollator mobility aids, driven by social stigma associated with visible disability or aging, resistance to acknowledging functional decline, and limited patient and caregiver awareness of the clinical fall prevention and rehabilitation benefits of rollator-assisted ambulation, remains a meaningful barrier to market penetration, particularly in culturally conservative markets where assistive device use carries negative social connotations.

Under-prescription by primary care physicians and general practitioners with limited geriatric mobility assessment training, combined with patient refusal of prescribed rollator aids, creates a persistent gap between clinical need and actual rollator adoption that constrains market growth relative to the scale of the underlying mobility impairment population.

Opportunity - Smart Rollator Technology and Digital Health Integration

The integration of sensor technology, connectivity features, and digital health monitoring capabilities into clinical rollator design represents a transformational innovation opportunity for rollator manufacturers seeking to differentiate premium products, capture value-based care reimbursement positioning, and address growing healthcare provider demand for objective patient mobility monitoring and rehabilitation progress data.

Smart rollator concepts incorporating inertial measurement units, GPS tracking, step counting, gait analysis sensors, and connectivity to clinical electronic health record systems are advancing from research prototype to early commercial development, with academic medical centers and mobility technology companies collaborating on evidence-based smart rollator development programs.

The clinical value proposition of smart rollators enabling remote patient monitoring for fall risk assessment, rehabilitation progress quantification, and early detection of functional decline in community-dwelling elderly patients aligns with digital health infrastructure investment priorities in North American and European healthcare systems, supporting reimbursement pathway development for technology-enhanced rollator devices.

Category-wise Analysis

Product Type Insights

4-wheeler rollators are expected to dominate by product type, commanding approximately 65% of global revenue in 2026. The 4-wheel configuration leads the market due to its superior stability, four-point ground contact, and enhanced safety for patients with balance impairments. Its popularity is further supported by features such as a padded seat, storage basket, ergonomic hand brakes, and adjustable height settings for improved comfort and usability. Drive Medical Nitro Sprint Rollator, a 4-wheel rollator designed with large wheels for stability, an integrated seat for resting, ergonomic hand brakes, and adjustable handle heights.

3-Wheeler rollators represent the fastest-growing product type, gaining clinical and consumer adoption for their compact turning radius and enhanced maneuverability in confined indoor spaces, narrow hospital corridors, small apartment bathrooms, and commercial building environments relative to 4-wheel designs. NOVA Medical Products Traveler 3-Wheel Rollator is specifically designed for users who need greater maneuverability in tight indoor spaces.

Material Type Insights

Aluminum rollators are expected to be the dominant material segment, capturing approximately 58% of the market revenue in 2026. Aluminum dominates rollator frame construction due to its high strength-to-weight ratio, corrosion resistance, cost-effective manufacturing, and recyclability. These properties provide durable, lightweight, and affordable mobility solutions while supporting sustainability goals. Nitro Rollator from Drive Medical. The rollator features a lightweight aluminum frame, combining durability, corrosion resistance, and ease of use for elderly and mobility-impaired users.

Carbon fiber rollators represent the fastest-growing material type, driven by growing demand for ultra-lightweight, premium-positioned clinical rollators from active elderly users and rehabilitation patients prioritizing minimal device weight for ease of transport and independent management. Carbon Ultralight Rollator from byACRE. The product is constructed from carbon fiber, making it one of the lightest rollators on the market while maintaining high strength and durability.

Application Insights

Elderly care is the leading application in the clinical rollators market, commanding approximately 40% of the global market revenue in 2026. The elderly population dominates rollator demand, driven by the growing aging population and the high prevalence of age-related mobility impairments requiring daily mobility support for independent living and outdoor activities. TOPRO Troja Original Rollator from TOPRO. The rollator is specifically designed for older adults, offering stability, ergonomic handles, a built-in seat, and easy maneuverability to support independent daily living and outdoor mobility.

The rehabilitation segment represents the fastest-growing application segment, fueled by the expanding global hospital rehabilitation sector, growing surgical volumes generating post-operative rehabilitation rollator demand, and healthcare system investment in structured outpatient rehabilitation programs incorporating rollator-assisted progressive ambulation protocols. Gemino 30 Walker Rollator from Sunrise Medical. The rollator is commonly used in rehabilitation settings due to its lightweight design, stability, and adjustable features that support progressive mobility training for patients recovering from surgery, injury, or neurological conditions.

Regional Insights

North America Clinical Rollators Market Trends

North America is projected to dominate, holding approximately 37% of the total revenue in 2026. The regional market's growth is propelled by an aging population, broad insurance reimbursement coverage for rollators, and a well-established healthcare infrastructure that supports rollator prescriptions through hospitals, physical therapy centers, and geriatric care programs.

U.S. Clinical Rollators Market Insights

The U.S. represents the largest clinical rollator market globally, driven by the world's highest per-capita healthcare expenditure, Medicare Part B's established coverage of rollators as durable medical equipment with physician prescription, and the large and growing U.S. elderly population, which drives both institutional procurement and individual consumer rollator purchases.

Canada Clinical Rollators Market Insights

Canada's market benefits from provincial health program funding support for assistive devices through programs, including Ontario's Assistive Devices Program (ADP) and equivalent provincial frameworks that provide eligible elderly and disabled individuals with funding contributions toward prescribed rollator purchases. Canadian physical therapy and occupational therapy practice standards align closely with U.S. clinical guidelines for rollator prescription, creating consistent clinical demand patterns for 4-wheel rollators across Canadian hospital, community health, and long-term care settings.

Europe Clinical Rollators Market Trends

Europe represents the second-largest regional clinical rollators market. The region's market position reflects Europe's advanced aging demographic profile, with the European Commission projecting that over 25% of the EU population will be aged 65 or over by 2030. Comprehensive National Health Service and statutory health insurance reimbursement frameworks support rollator prescription in major European markets, and a strong clinical physical therapy culture emphasizing mobility aid prescription for fall prevention and rehabilitation.

Germany Clinical Rollators Market Trends

Germany is the leading European market, underpinned by the country's large elderly population, the German statutory health insurance (GKV) system's established coverage for prescribed rollators as Hilfsmittel (aids and appliances) for eligible patients with mobility impairment, and Germany's strong rehabilitation medicine and physical therapy infrastructure that generates consistent clinical rollator demand across hospital, outpatient rehabilitation, and community care settings.

U.K. Clinical Rollators Market Trends

The U.K. clinical rollators market is shaped by NHS England community equipment service provision, the NHS wheelchair and walking aids service commissioning framework, and the growing private pay market for premium rollator products among the U.K.'s active elderly and mobility-conscious consumer segments. NHS community equipment services and social care departments provide rollators to eligible elderly and disabled individuals through local authority assistive technology provision programs, creating an institutional demand channel complemented by private retail purchasing of premium rollators through mobility equipment retailers and e-commerce channels.

Asia Pacific Clinical Rollators Market Trends

Asia Pacific is likely to be the fastest-growing regional market, driven by the rapid aging of populations in China, Japan, and South Korea, expanding geriatric healthcare and long-term care infrastructure investment across the region, and growing awareness of rollator-assisted mobility support as a clinical fall prevention and rehabilitation tool in both advanced and developing Asian healthcare systems.

Japan Clinical Rollators Market Trends

The Japan market is experiencing steady growth due to the country's rapidly aging population and increasing prevalence of mobility-related conditions among older adults. Demand is rising for lightweight, foldable, and ergonomically designed rollators that support independent living and community mobility. Healthcare providers and long-term care facilities are increasingly incorporating rollators into elderly care programs to reduce fall risks and improve patient mobility.

India Clinical Rollators Market Trends

The India market is witnessing growth due to the rising elderly population, increasing incidence of mobility impairments, and greater awareness of assistive mobility devices. Demand is expanding across hospitals, rehabilitation centers, and home healthcare settings as patients seek improved mobility and independence. Manufacturers are focusing on affordable, lightweight, and foldable rollator designs suited to diverse user needs.

Competitive Landscape

The global clinical rollators market is characterized by a moderately concentrated competitive landscape anchored by established durable medical equipment and assistive mobility device manufacturers with multi-decade market presence, alongside a diverse tier of regional manufacturers and specialists serving specific geographic or clinical market segments. The market is driven by competition in product quality, clinical compliance, portfolio diversity, distribution networks, reimbursement approvals, and the ability to offer cost-effective rollators with advanced ergonomic and safety features.

Invacare Corporation maintains a leading global position in the clinical rollators market through its comprehensive durable medical equipment portfolio, established multi-regional DME distribution relationships spanning North America, Europe, and Asia Pacific, and a broad rollator product line addressing institutional and consumer market segments.

Key Industry Developments:

- In December 2025, Signature Products Ltd. announced the launch of its Signature Series “Out and About” 4-Wheel Rollator, a lightweight and feature-rich mobility aid. The product was introduced through the company’s distribution network across Canada, expanding access to advanced mobility support solutions for users seeking enhanced independence and comfort.

- In May 2023, Drive Medical launched the Nitro Sprint Rollator, featuring an upgraded Euro-style frame, enhanced braking system, and integrated slow-down brake to improve user safety, control, and convenience.

Companies Covered in Clinical Rollators Market

- Invacare Corporation

- GF Health Products

- Human Care HC AB

- Karman Healthcare

- Briggs Healthcare

- Evolution Technologies Inc.

Frequently Asked Questions

The global clinical rollators market is projected to reach US$279.4 million in 2026.

The growing focus on rehabilitation, fall prevention, and value-based care is driving rollator adoption by improving patient mobility outcomes, reducing healthcare costs, and supporting broader reimbursement coverage.

The clinical rollators market is poised to witness a CAGR of 5.6% from 2026 to 2033.

Smart rollator technologies with sensors, connectivity, and remote monitoring capabilities are creating growth opportunities by enhancing patient mobility tracking, fall prevention, and digital health integration.

Key players include Invacare Corporation, GF Health Products, Human Care HC AB, Karman Healthcare, Briggs Healthcare, and Evolution Technologies Inc.