- Medical Devices

- Breast Implants Market

Breast Implants Market Size, Share, and Growth Forecast 2026 – 2033

Breast Implants Market by Product Type (Silicone Breast Implants, Saline Breast Implants), Application (Cosmetic Surgery, Reconstructive Surgery), Shape (Round Breast Implants, Anatomical Breast Implants), by End-user (Hospitals, Cosmetology Clinics), and Regional Analysis, 2026–2033

Breast Implants Market Size and Trend Analysis

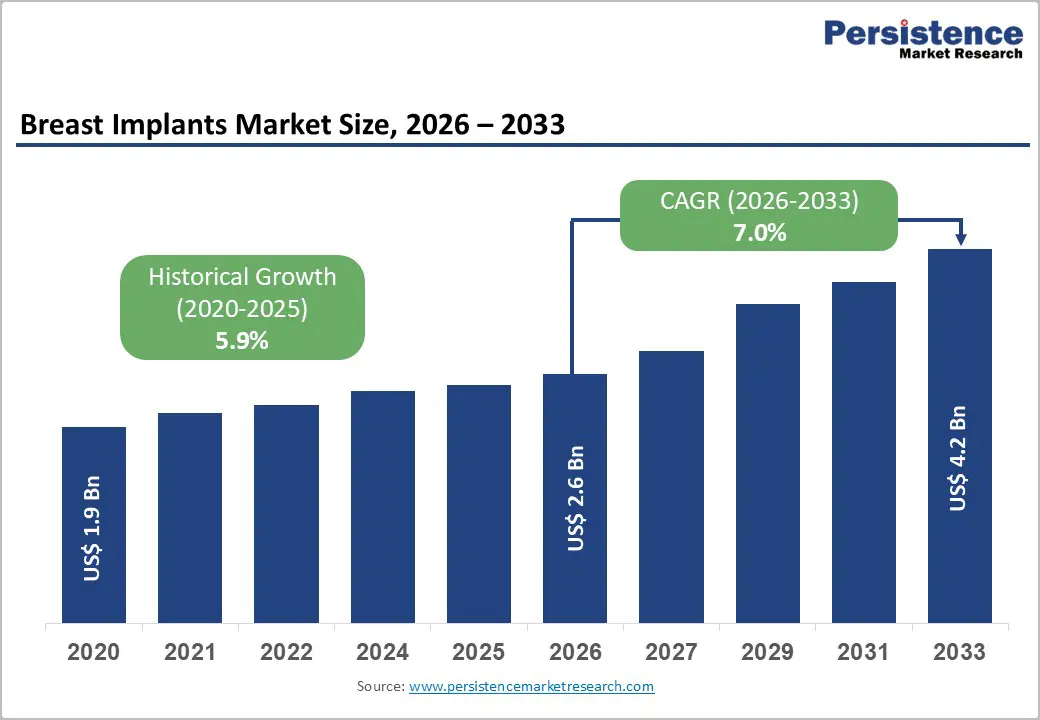

The global breast implants market size is expected to be valued at US$ 2.6 billion in 2026 and projected to reach US$ 4.2 billion by 2033, growing at a CAGR of 7.0% between 2026 and 2033. Breast implants are widely used for breast augmentation and reconstruction procedures to improve breast shape, size, and symmetry. The market is growing steadily due to rising demand for cosmetic enhancement and post-mastectomy reconstruction. According to the International Society of Aesthetic Plastic Surgery (ISAPS), more than 1.89 million breast augmentation procedures were performed globally in 2023, making it one of the top aesthetic surgical procedures worldwide.

Additionally, the World Health Organization (WHO) reported that approximately 2.3 million women were diagnosed with breast cancer in 2022, significantly increasing the need for reconstructive breast surgeries. Advancements in cohesive silicone gel implants, improved safety profiles, and growing awareness of aesthetic procedures in emerging economies are further supporting market expansion. Increasing healthcare expenditure and wider access to plastic surgery services continue to strengthen global demand for breast implants.

Key Industry Highlights

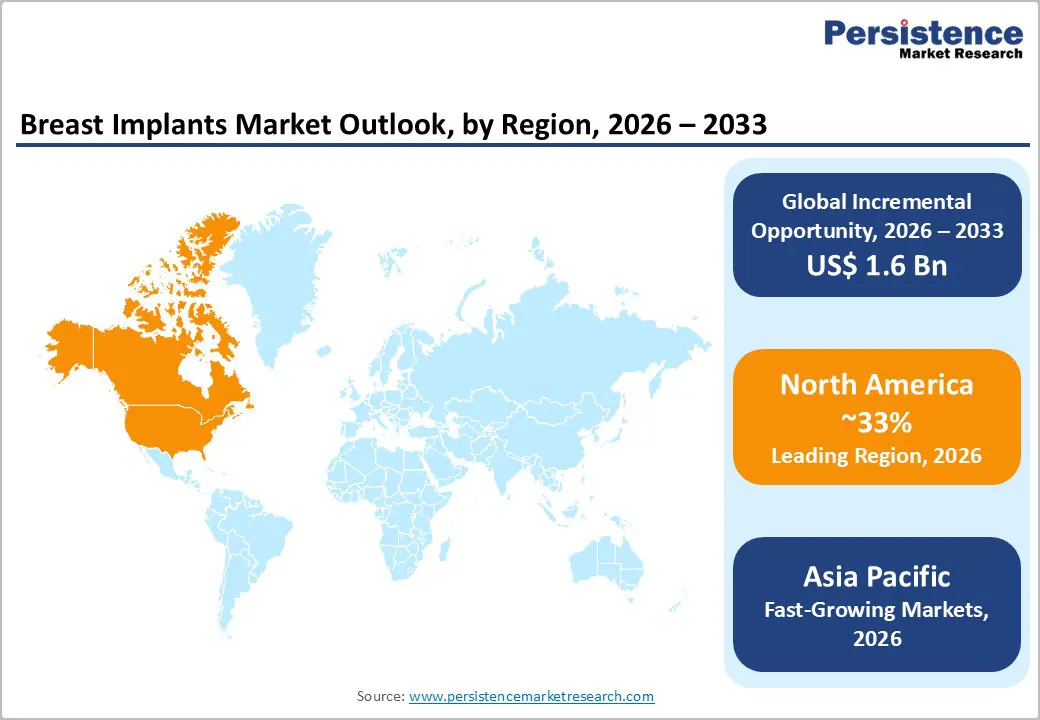

- Leading Region – North America holds ~33% of the global breast implants in 2026, driven by the world's highest cosmetic surgery volume per ASPS data, WHCRA-mandated insurance coverage for post-mastectomy reconstruction, and premium implant technology adoption.

- Fastest Growing Region – Asia Pacific is the fastest-growing breast implants region through 2033, propelled by rapidly expanding aesthetic surgery markets in China, South Korea, and India, rising disposable incomes, and Thailand's globally ranked medical tourism infrastructure attracting international cosmetic surgery patients.

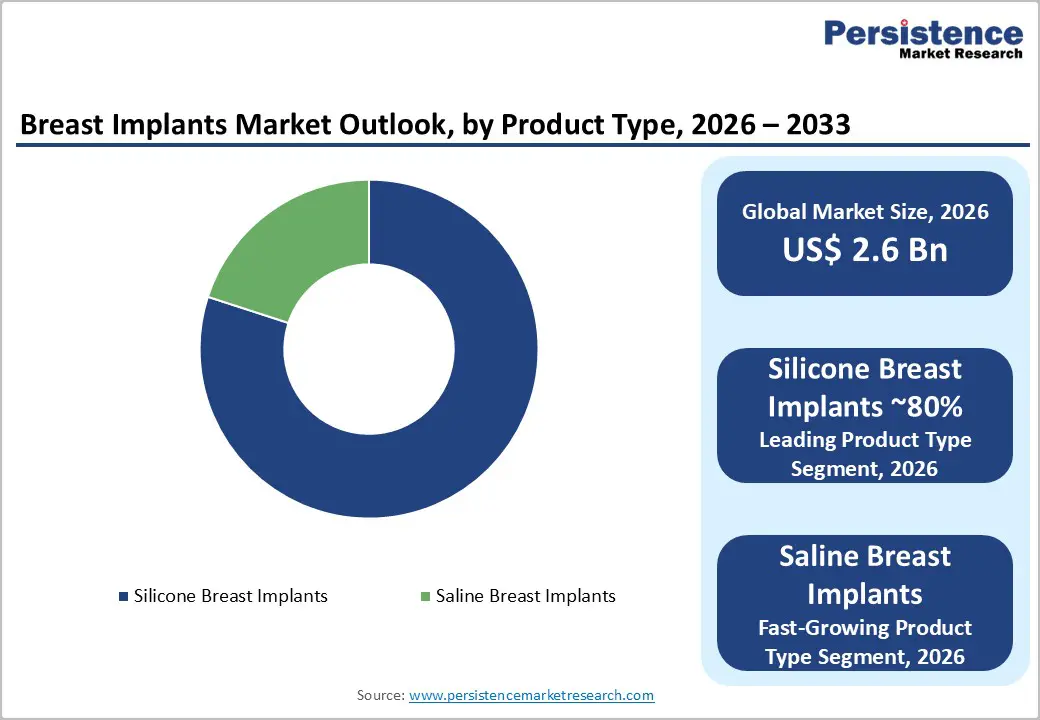

- Dominant Segment – Silicone Breast Implants dominate the Product Type category with ~80% market share in 2025, backed by superior aesthetic outcomes, broad FDA and global regulatory approval, and strong surgeon preference accounting for 84% of U.S. breast augmentations per ASPS data.

- Fast-Growing Segment – Saline Breast Implants are the fastest-growing product type through 2033, benefiting from renewed interest following BIA-ALCL safety concerns around textured silicone devices and growing demand for the FDA-cleared IDEAL IMPLANT® structured saline technology offering improved aesthetic outcomes.

- Key Opportunity: Asia Pacific's aesthetic surgery boom, particularly China's double-digit growth medical aesthetics sector and India's expanding medical tourism infrastructure, represents the most transformative revenue opportunity for breast implant manufacturers pursuing volume growth.

Market Dynamics

Drivers - Rising Demand for Post-Mastectomy Breast Reconstruction Driving Clinical Volume

Breast reconstruction following mastectomy represents an increasingly important and fast-growing demand driver for the breast implants market. The American Cancer Society estimates that ~300,000 new breast cancer cases are diagnosed annually in the U.S. alone, with the National Cancer Institute (NCI) reporting that 40–50% of mastectomy patients in the U.S. now opt for breast reconstruction a proportion that has increased significantly following the enactment of the Women's Health and Cancer Rights Act (WHCRA), which mandates insurance coverage for reconstructive procedures post-mastectomy.

Global breast cancer incidence has similarly risen, with the WHO's Global Cancer Observatory (GLOBOCAN) reporting 2.3 million new breast cancer diagnoses worldwide in 2022. This structural demand is further amplified by increasing surgeon advocacy for immediate implant-based reconstruction, elevating breast implant utilization in oncology-linked procedures globally.

Technological Innovation in Implant Design and Material Safety Expanding Patient Confidence

Continuous technological advancement in breast implant design and material science is a significant market driver, expanding both patient acceptance and the addressable procedural volume. The development of form-stable cohesive silicone gel implants marketed under brands including Allergan's Natrelle® and Mentor's MemoryGel® has substantially improved shape retention and rupture resistance compared to earlier liquid silicone designs.

The FDA's 2020 updated safety requirements for breast implants, mandating standardized labeling, a boxed warning, and patient decision checklists, while initially restrictive, have increased informed consent quality and long-term patient trust. More recently, the introduction of Motiva Implants® by Establishment Labs S.A., featuring nano-textured surfaces and BluSeal® integrity indicators, represents a new generation of safety-focused innovation attracting premium pricing and strong surgeon adoption globally.

Restraints - Safety Concerns and Regulatory Actions Around Breast Implant-Associated ALCL

The identification of Breast Implant-Associated Anaplastic Large Cell Lymphoma (BIA-ALCL), a rare but serious immune system cancer linked primarily to textured breast implants, has significantly impacted market sentiment and regulatory posture. The FDA has received over 1,100 reports of BIA-ALCL cases globally, leading to Allergan's voluntary recall of its Biocell® textured implants in 2019. Multiple countries, including France, Canada, and Australia, have enacted their own restrictions on textured implants. These events have structurally reduced the textured implant market and imposed heightened regulatory scrutiny on all manufacturers, increasing compliance costs and slowing the pace of new product approvals globally.

Opportunities - Reconstructive Surgery and Next-Generation Implant Technologies Creating Premium Revenue Corridors

The increasing prevalence of breast cancer has led to a significant rise in mastectomy procedures, subsequently boosting the demand for breast reconstruction surgeries. For instance, in 2023, breast reconstruction was among the top three reconstructive procedures performed in the U.S. In the U.S., approximately 75% of breast reconstruction patients opt for immediate reconstruction, making it the most common approach.

Globally, immediate reconstruction remains the preferred choice, accounting for 55.4% of cases, followed by delayed two-stage reconstruction. This preference highlights the impact of factors such as the need for additional therapies, patient health, and personal choices in determining the timing of reconstruction. The increasing number of breast reconstruction surgeries contributes significantly to this market expansion, presenting substantial opportunities for manufacturers and healthcare providers specializing in breast implants.

Category-wise Analysis

Product Type Insights

Silicone breast implants dominate the global breast implants market, accounting for ~80% share in 2026. This overwhelming dominance reflects silicone gel's superior aesthetic outcomes, natural feel, shape retention, and lower risk of visible rippling compared to saline alternatives that align with both cosmetic and reconstructive patient preferences.

The FDA approved cohesive silicone gel implants for cosmetic augmentation in patients aged 22 and older in 2006, and the expanded regulatory acceptance of next-generation form-stable silicone devices has further reinforced clinical preference. According to the ASPS, silicone implants accounted for ~84% of all breast augmentation procedures in the U.S. in 2022. The segment's dominance is further reinforced by ongoing R&D investment from major manufacturers in silicone gel chemistry refinement, surface engineering, and safety biomarker technologies.

Breast Implants market

Hospitals represent the leading end-user segment in the breast implants market ~48% total share in 2026. Hospitals' dominance is rooted in their role as the primary setting for medically indicated reconstructive breast surgery, as a fast-growing application. Complex post-mastectomy reconstruction procedures, often requiring general anesthesia, multi-stage surgery, and oncology team coordination, necessitate full hospital infrastructure.

According to the ASPS, virtually all implant-based breast reconstruction procedures following mastectomy are performed in hospital inpatient or outpatient surgical settings. Large academic medical centers and cancer institutes, particularly in North America and Europe, are major procurement hubs for premium silicone implants, driving high average selling price realization and sustaining hospitals' dominant revenue contribution to the overall breast implants market.

Regional Insights

North America Breast Implants Market Trends and Insights

North America leads the global market with ~33% of total share in 2026, anchored by the U.S.' world-leading aesthetic surgery volume, robust insurance-supported reconstructive surgery infrastructure, and a highly developed surgeon training and implant technology ecosystem. The region is characterized by premium product preference, high adoption of next-generation silicone implants, and active FDA regulatory engagement, driving continuous product safety innovation.

U.S. Breast Implants Market Size

The U.S. dominates the North American market, representing ~90% of regional revenue in 2026. The ASPS reported over 350,000 breast augmentation procedures and ~100,000 reconstruction procedures annually in recent years, collectively establishing the U.S. as the single largest national market globally. Strong private insurance coverage for reconstructive procedures under WHCRA and high cosmetic procedure volumes sustain exceptional implant demand.

Europe Breast Implants Market Trends and Insights

Europe is the second-largest Breast Implants market, characterized by stringent regulatory oversight under the European Union Medical Device Regulation (EU MDR 2017/745), which has significantly elevated clinical evidence and post-market surveillance requirements for breast implants since 2021. The region has strong reconstructive surgery programs linked to organized national breast cancer screening initiatives, particularly in Germany, France, and the UK, sustaining consistent institutional demand.

Germany Breast Implants Market Size

Germany leads the European Breast Implants market, contributing ~22% of regional revenue in 2026. Germany's robust private health insurance system supports both cosmetic and reconstructive procedures, and its world-class oncology infrastructure, with leading cancer centers including the German Cancer Research Center (DKFZ), drives high reconstructive surgery volumes and consistent premium implant procurement.

UK Breast Implants Market Size

The UK accounts for ~19% of European market revenue, underpinned by significant NHS-funded breast reconstruction activity following mastectomy and a large private cosmetic surgery sector. The Medicines and Healthcare Products Regulatory Agency (MHRA) actively monitors breast implant safety, and the UK's organized breast cancer screening program sustains a large population with reconstructive surgery needs.

Asia Pacific Breast Implants Market Trends and Insights

Asia Pacific is the fastest-growing regional market for Breast Implants, propelled by rapidly expanding aesthetic surgery markets in South Korea, Japan, China, India, and Thailand. China represents the region's largest national market in its medical aesthetics sector, estimated by the Chinese Society of Plastic Surgery to be experiencing double-digit annual growth, and is driving massive implant volume expansion. Rising disposable incomes, social media influence, and growing infrastructure for medical tourism collectively accelerate the regional adoption.

India Breast Implants Market Size

India accounts for ~12% of the regional share in 2026 and is among the fast-growing markets. A rapidly expanding private cosmetic surgery sector supported by the Association of Plastic Surgeons of India (APSI) combined with growing medical tourism from South Asia and the Middle East, positions India as a significant emerging demand center for breast implant manufacturers.

Japan Breast Implants Market Size

Japan represents an analyst-estimated 22% of the Asia Pacific breast implants market. The Pharmaceuticals and Medical Devices Agency (PMDA) in Japan maintains one of the strictest post-market surveillance regimes in the Asia Pacific region, requiring annual safety reports for all implantable devices, which concentrates market share among manufacturers with robust clinical affairs infrastructure. Japan's ageing population and above-average breast cancer incidence rate, as per National Cancer Center Japan data, support a sustained reconstructive demand base independent of aesthetic volume cycles.

Competitive Landscape

The global breast implants market is moderately consolidated, with Allergan Plc (AbbVie) and Mentor Worldwide LLC (Johnson & Johnson) historically commanding dominant combined global market share through their extensive regulatory approvals, surgeon training programs, and brand recognition. Key competitive strategies include R&D investment in implant surface innovation and safety biomarker technologies, geographic expansion into high-growth Asia Pacific markets, and direct surgeon engagement through outcomes registries and clinical evidence programs.

Establishment Labs S.A. has emerged as a significant disruptor with its Motiva Implants® platform, capturing premium market positioning. Emerging business trends include digital patient engagement tools, outcome tracking platforms, and sustainability-focused packaging initiatives, differentiating leading brands.

Key Developments:

- In October 2025, Allergan Aesthetics, an AbbVie company, announced that Natrelle® had been selected as a supplier by Vizient, Inc., the nation’s largest provider-driven healthcare performance improvement organization. This agreement expanded Natrelle®’s access to Vizient’s broad network of academic medical centers, community hospitals, integrated delivery networks, and non-acute care providers, covering more than half of U.S. healthcare organizations.

- In February 2025, Establishment Labs S.A. received expanded market clearance for its Motiva Implants® SilkSurface® technology in additional Asia Pacific markets, accelerating the company's geographic footprint in the region's fastest-growing aesthetic surgery segment.

- In December 2024, Mentor Worldwide LLC, the number one global brand in breast aesthetics, and part of Johnson & Johnson MedTech, announced the U.S. Food and Drug Administration (FDA) approved MENTOR™ MemoryGel™ Enhance Breast Implants for primary and revision reconstruction breast surgery in post-mastectomy women.

- In December 2024, GC Aesthetics® (GCA), announced the initiation of a significant multi-center and prospective clinical study in Europe to evaluate and confirm the safety, effectiveness, and patient satisfaction associated with the innovative PERLE™ smooth opaque round breast implant.

- In September 2024, GC Aesthetics® (GCA) announced the launch of the YOUTHLY™ brand in China, featuring its latest breast implant innovations: PERLE™, Luna XT™, and the latest version of The Round Collection™, 100% filled.

Global Breast Implants Market – Key Insights and Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 1.9 billion |

|

Current Market Value (2026) |

US$ 2.6 billion |

|

Projected Market Value (2033) |

US$ 4.2 billion |

|

CAGR (2026–2033) |

7.0% |

|

Leading Region |

North America, ~33% market share in 2026 |

|

Dominant Product Type |

Silicone Breast Implants, ~80% market share in 2026 |

|

Top-ranking Application |

Cosmetic Surgery, ~72% market share in 2026 |

|

Incremental Opportunity |

US$ 1.6 billion (Absolute Dollar Opportunity, 2026–2033) |

Companies Covered in Breast Implants Market

- Allergan, Plc (Actavis Plc)

- Mentor Worldwide LLC. (Johnson & Johnson Services, Inc.)

- GC Aesthetics plc

- Sientra, Inc.,

- Groupe Sebbin SAS

- Polytech Health & Aesthetics GmbH

- Establishment Labs S.A.

- HansBiomed Co., Ltd

- CEREPLAS

- Silimed

- Laboratoires Arion

- Guangzhou Wanhe Plastic Materials Co., Ltd.

- Nagor Ltd.

- Implantech Associates Inc.

- Others

Frequently Asked Questions

The market is expected to reach US$ 3,934.3 Mn by 2032, growing at a CAGR of 7.0%.

Silicone breast implants dominate the market with an 80.2% share due to their natural feel and durability.

Increasing cosmetic surgeries, rising disposable income, and advancements in implant technology are key growth drivers.

North America holds the largest share (33.2% in 2025) due to high aesthetic demand and advanced healthcare infrastructure.

Risks include implant rupture, leakage, infection, chronic pain, and capsular contracture, affecting patient decisions.