Industry: Consumer Goods

Published Date: January-2025

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 187

Report ID: PMRREP34138

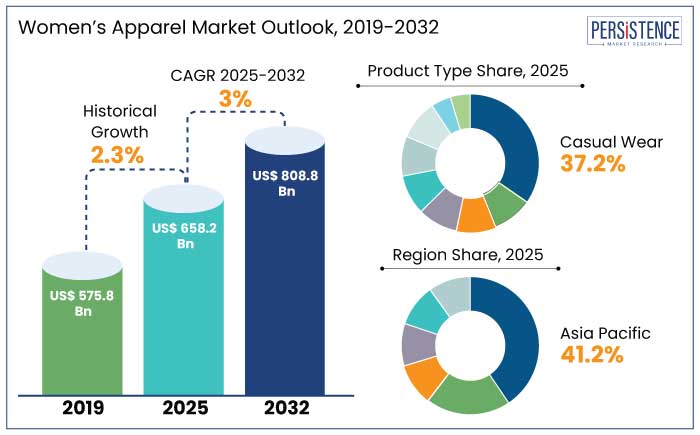

The global women’s apparel market is estimated to reach a size of US$ 658.2 Bn by 2025. It is anticipated to showcase a CAGR of 3% during the forecast period to attain a value of US$ 808.8 Bn by 2032.

By 2030, over 3.5 billion middle-class consumers will be concentrated in Asia Pacific, significantly contributing to apparel demand. Online sales of women’s apparel are set to account for 50% of the market by 2032. Consumers are increasingly seeking tailored clothing options, driving demand for tech-enabled customization.

Demand for sustainable fabrics like organic cotton, hemp, and recycled polyester is projected to witness exponential growth during the assessment period. Brands are likely to focus on recycling, upcycling, and take-back programs, appealing to eco-conscious consumers.

By 2030, 50% of global apparel companies are projected to adopt circular fashion practices. Leading brands aim to achieve net-zero emissions by 2030, further driving innovations in green manufacturing.

Key Highlights of the Industry

|

Market Attributes |

Key Insights |

|

Women’s Apparel Market Size (2025E) |

US$ 658.2 Bn |

|

Projected Market Value (2032F) |

US$ 808.8 Bn |

|

Global Market Growth Rate (CAGR 2025 to 2032) |

3% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

2.3% |

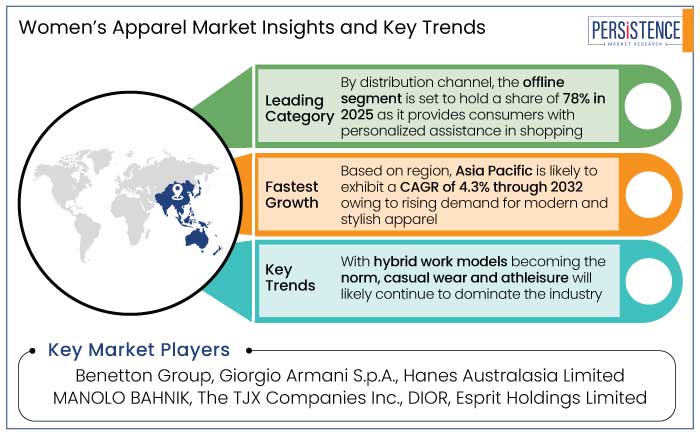

Asia Pacific is set to account for a share of 41.2% in 2025. The region is home to over 4.6 billion people with women comprising a significant portion of this demographic. Rapid urbanization is driving demand for modern and stylish apparel as urban women increasingly adopt global fashion trends.

Countries like China, India, and Southeast Asia’s nations are witnessing strong economic growth and increasing purchasing power. These are enabling women to spend on premium and branded apparel. With more women entering the workforce, there is a rising demand for professional attire, athleisure, and multifunctional clothing. In Southeast Asia, working women represent 40% of the total workforce in leading urban centers.

Asia Pacific is the most prominent e-commerce market globally, with countries like China and India leading online retail sales. The region has a high proportion of young consumers, especially in India and Southeast Asia, who are more inclined to experiment with fashion trends.

Casual wear is projected to hold a share of 37.2% in 2025. The rise of remote work and hybrid work models has led to a decreased demand for formal wear and an increased preference for comfortable yet stylish clothing. As more people prioritize comfort and practicality in their daily lives, casual wear like jeans, t-shirts, and athleisure has become a wardrobe staple.

Athleisure has witnessed significant growth due to its dual functionality for casual and active use. Brands like Lululemon, Nike, and Adidas have reported double-digit growth in their women’s casual and athleisure lines. Consumers seek multi-functional apparel that suits various occasions, right from running errands to social gatherings.

Casual wear caters to this need by being stylish yet adaptable. For instance,

Online platforms have made casual wear more accessible, offering a vast array of styles and price points. Casual wear is the most searched apparel category online. In 2023, casual wear accounted for nearly 45% of online women’s apparel sales.

Offline segment is anticipated to generate a share of 78% in 2025. Despite the rapid growth of e-commerce, offline channels remain a dominant force in the women's apparel market. Women often prefer to see, feel, and try on clothes before purchasing, especially for items like dresses, blouses, or fitted garments where texture, fit, and quality matter.

Offline shopping allows customers to purchase and take home items immediately without waiting for delivery. This is especially appealing for last-minute shopping needs or special occasions.

In-store staff provide personalized assistance, helping customers choose items based on their preferences and needs. A survey conducted in 2022 revealed that 75% of consumers value personalized in-store experiences when shopping for apparel.

Offline stores give a sense of reliability, particularly in regions where online fraud or delivery issues are prevalent. Several women view shopping as a leisure activity to enjoy with friends or family. Visiting malls or boutiques offers a complete experience that extends beyond just buying clothes. A survey revealed that 68% of women prefer in-person shopping for the social and recreational aspect.

Potential growth in the global women’s apparel industry is predicted to be driven by increasing demand for sustainable clothing and unique materials. By 2030, online channels are projected to contribute 50% of global women’s apparel sales.

Brands are predicted to integrate the latest technologies like AI, AR, and ML to improve consumer experiences. Leading apparel labels are progressively extending their offerings to cater to diverse consumer requirements, thereby driving growth.

The women’s apparel market growth was average at a CAGR of 2.3% during the historical period from 2019 to 2023. Key drivers of growth during this period were rapid urbanization and rising middle-class populations, especially in emerging markets. Fast fashion and celebrity endorsements were prominent influences in the industry.

Growth of online retail platforms offered convenience and competitive pricing, further spurring growth. For instance,

The COVID-19 pandemic increased focus on loungewear and casual wear, leading to a surge in women athleisure sales. Brands focused on inclusivity, offering diverse size ranges and styles to women across the globe.

The forecast period is predicted to witness an increasing penetration of hybrid retail models, blending offline and online shopping experiences. Significant investments in technology, such as virtual fitting rooms and AI-driven personalization are predicted to see increased adoption.

Increasing Shift toward Sustainability and Ethical Fashion to Spur Demand

Over 60% of millennials and 70% of Gen Z consumers consider sustainability as a key factor in their purchasing decisions. Consumers now expect brands to disclose supply chain details, with 73% of consumers stating they prefer brands with transparent and ethical practices. Producing a single cotton T-shirt requires 2,700 liters of water, prompting a shift toward recycled and organic materials.

The EU Green Deal and initiatives like the Fashion Pact aim to make the industry more sustainable by 2030. Innovations in plant-based and biodegradable materials like Tencel and Piñatex, made from pineapple fibers, offer eco-friendly alternatives and are hence gaining traction in the women’s apparel industry.

Brands like Patagonia and H&M are adopting take-back programs to recycle old clothing into new garments. Consumers are increasingly attracted to unique and upcycled products, thereby offering a way to decrease waste while creating value. Adidas and Nike are investing in low-impact production technologies to reduce carbon footprints.

Trends for Inclusivity and Adaptive Fashion to Augment Sales

Consumers increasingly demand clothing that celebrates diversity, including extended sizing and diverse fits. For example,

Brands increasingly recognize the importance of catering to cultural and religious needs, such as modest fashion or traditional wear for specific communities. Brands like Torrid, Universal Standard, and Good American are leading the charge by offering stylish and functional options in larger sizes for women.

Specialized sizing for shorter and taller consumers is an underexplored market with significant growth potential. Adaptive apparel includes designs that cater to physical limitations, such as Velcro closures, magnetic fastenings, or adjustable waists. A few notable examples of these are Tommy Hilfiger’s adaptive line and Zappos Adaptive collection.

Intense Competition in the Market to Hinder Sales

Rapid growth of e-commerce has levelled the global field, enabling online-only brands to challenge established players. Consumers now have access to a vast array of fashion choices at the click of a button, making it easier for new and niche brands to hold market share.

Online-only retailers like Shein, Boohoo, and ASOS have emerged as leading competitors to traditional stores like H&M and Zara. This is due to their ability to offer lower prices, faster fashion cycles, and direct-to-consumer models.

Fast fashion brands such as Zara, H&M, Forever 21, and Shein have intensified competition by offering low-cost, high-turnover products that reflect the latest trends. Shein, a fast-fashion giant, became the largest global fashion retailer by sales volume in 2023, surpassing brands like Zara and H&M. The business model of fast fashion enables companies to release new designs on a bi-weekly or monthly basis, often outpacing traditional fashion cycles.

Companies to Focus on Modest and Cultural Fashion to Gain Profit

Various communities prioritize traditional and modest clothing as part of their cultural identity. Extending diaspora populations in Western countries are driving demand for cultural and fusion wear. Social media platforms like Instagram, TikTok, and Pinterest have amplified the visibility of modest and cultural fashion, creating a global community of consumers and influencers.

Fusion wear, combining traditional elements with contemporary designs, is a surging trend across the globe. Brands offering custom options for weddings, festivals, and cultural celebrations can capture high-value markets. Luxury brands like Dolce & Gabbana and Oscar de la Renta have launched modest fashion lines, targeting affluent consumers in emerging markets.

Cultural and modest fashion brands are incorporating sustainable practices, appealing to environmentally conscious consumers. Online platforms dedicated to modest and cultural fashion are rising, offering worldwide shipping. E-commerce leaders like ASOS and Net-a-Porter have introduced modest sections on their websites.

Increasing Shift toward Events and Experiential Marketing to Spur Avenues

Consumers are increasingly seeking memorable and personalized experiences rather than just transactional interactions. For example,

Events often generate significant buzz on social media, amplifying brand exposure through user-generated content. Event-based content on platforms like Instagram, TikTok, and Facebook has been shown to boost engagement by 30% to 40%.

Consumers are increasingly looking for personalized experiences and events, enabling brands to cater to this demand through bespoke services or limited-edition offerings. Around 55% of consumers are more likely to make a purchase when their experience is personalized.

Hosting events creates an opportunity for brands to foster emotional connections with their target audience, leading to higher levels of brand loyalty. According to Event Marketer, 70% of consumers feel more connected to a brand after participating in an in-person or virtual event.

Companies in the women’s apparel market are leveraging data analytics to understand customer preferences, purchasing habits, and emerging trends. They are offering a wide range of sizes, styles, and designs to cater to diverse body types and demographics.

Businesses are using sustainable fabrics such as organic cotton, recycled polyester, and biodegradable textiles. They are also highlighting ethical production processes to appeal to environmentally conscious consumers.

Organizations are further offering personalized apparel or made-to-order options. They are progressively incorporating features like wrinkle-free materials, moisture-wicking fabrics, or multi-use clothing.

Brands are defining and communicating what makes their brand unique, such as affordability, luxury, or durability. They are also partnering with causes that resonate with their target audience, such as women’s empowerment.

Recent Industry Developments

|

Attributes |

Detail |

|

Forecast Period |

2025 to 2032 |

|

Historical Data Available for |

2019 to 2023 |

|

Market Analysis |

US$ Billion for Value |

|

Key Regions Covered |

|

|

Key Market Segments Covered |

|

|

Key Companies Profiled in the Report |

|

|

Report Coverage |

|

|

Customization and Pricing |

Available upon request |

By Type

By Category

By Distribution Channel

By Region

To know more about delivery timeline for this report Contact Sales

The market is anticipated to reach a value of US$ 658.2 Bn by 2025.

Casual wear is projected to hold a share of 37.2% in 2025.

Asia Pacific is predicted to hold a share of 41.2% in 2025.

Prominent players in the market include Benetton Group, Giorgio Armani S.p.A., and Hanes Australasia Limited.

The market is predicted to witness a CAGR of 3% through the forecast period.