- Medical Devices

- Tuberculosis Diagnostics Market

Tuberculosis Diagnostics Market Size, Share and Growth Forecast, 2026-2033

Tuberculosis Diagnostics Market by Test Type (Nucleic Acid Testing, SMEAR Microscopy, Radiography Tests), End-user (Hospitals & Clinics, Diagnostics Centers, Others), by Regional Analysis for 2026 - 2033

Tuberculosis Diagnostics Market Share and Trends Analysis

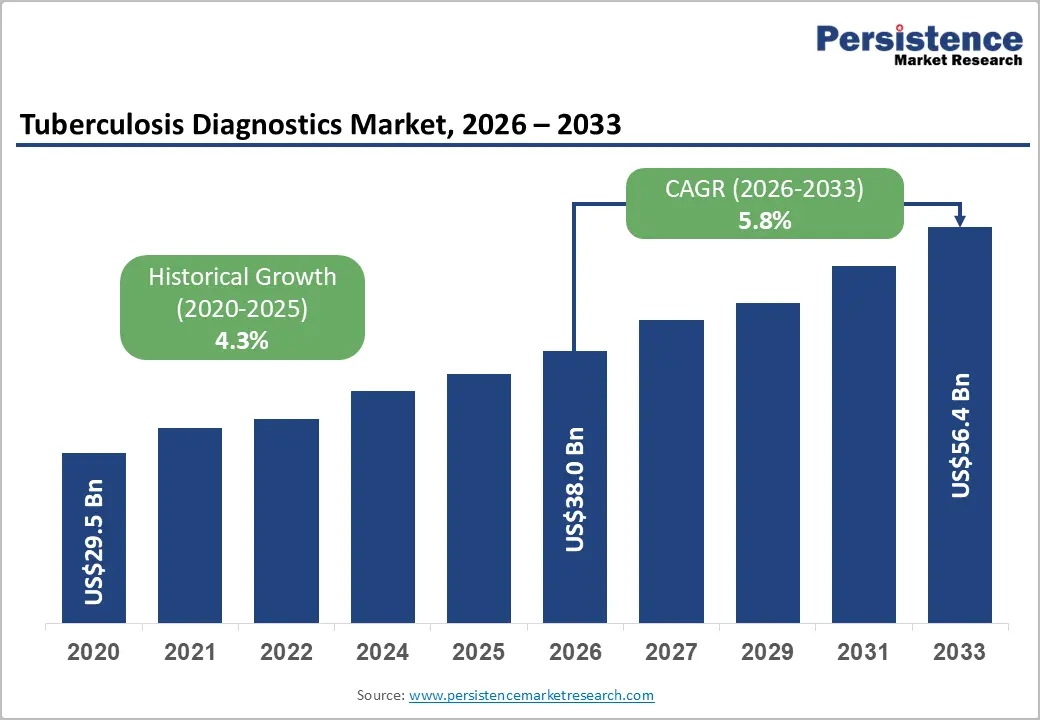

The global tuberculosis diagnostics market size is likely to be valued at US$38 billion in 2026 and is projected to reach US$56.4 billion by 2033, growing at a CAGR of 5.8% during the forecast period from 2026 to 2033, driven by the increasing global tuberculosis burden, rising adoption of molecular diagnostics, expanded government-funded screening programs, and broader deployment of rapid tuberculosis testing platforms. The World Health Organization (WHO) continues to prioritize early diagnosis through WHO-recommended rapid diagnostic tests, creating sustained demand for advanced diagnostic technologies. Growing investments in laboratory infrastructure, digital radiography, and drug-resistance detection are further strengthening long-term market expansion.

Key Industry Highlights:

- Dominant Test Type: Nucleic acid testing is expected to lead with 46% revenue share in 2026, while also emerging as the fastest-growing segment through 2033, driven by high diagnostic accuracy, rapid turnaround time, and expanding adoption of WHO-recommended molecular TB diagnostics.

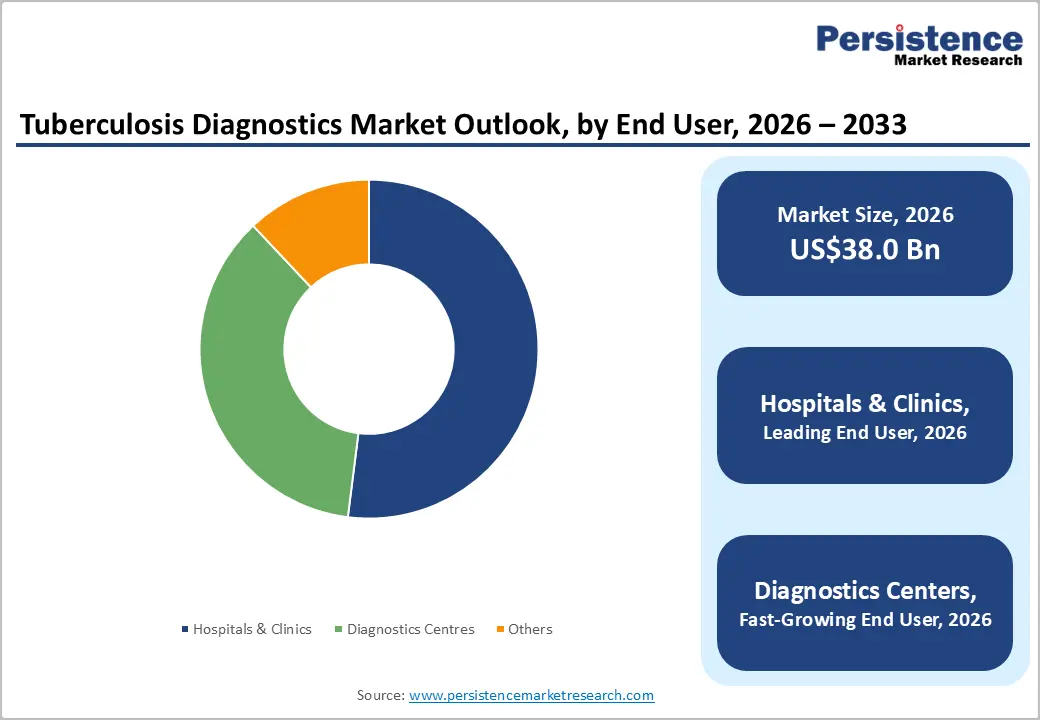

- Leading End-user: Hospitals & clinics are projected to dominate with a 52% share in 2026, while diagnostic centers are anticipated to be the fastest-growing segment through 2033, supported by rising molecular testing outsourcing and expansion of automated diagnostic networks.

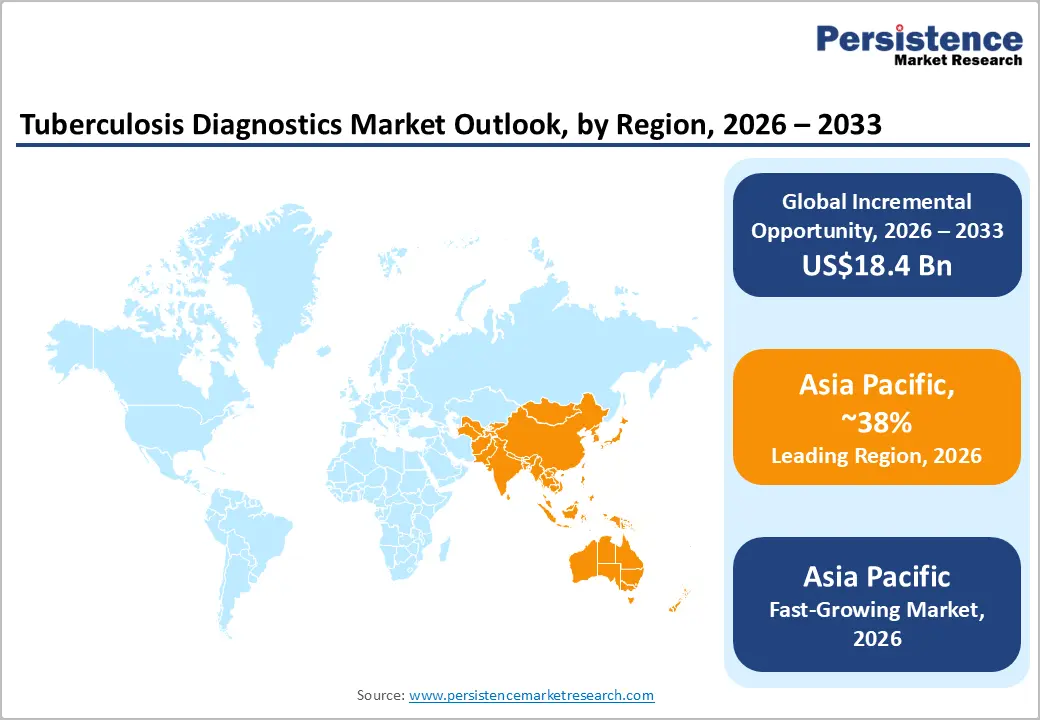

- Regional Leadership: Asia Pacific is set to lead with a 38% market share in 2026 and remain the fastest-growing region through 2033, driven by high TB burden, large-scale government screening programs, and expanding access to rapid molecular testing infrastructure.

- Innovation Landscape: The WHO reported nearly 100 tuberculosis diagnostic products under development as of August 2025, highlighting strong innovation activity across molecular diagnostics, AI-assisted imaging, and point-of-care testing technologies.

DRO Analysis

Driver - Expansion of WHO-Recommended Rapid Molecular Testing Programs

The global transition toward rapid molecular tuberculosis diagnostics remains the strongest growth driver for the market. According to the WHO Global Tuberculosis Report 2025, approximately 54% of newly diagnosed TB patients were initially tested using WHO-recommended rapid diagnostic tests (WRDs) in 2024, compared with 48% in 2023. WHO member states also adopted a target that 100% of diagnosed TB patients should receive an initial rapid diagnostic test by 2027, significantly accelerating investments in nucleic acid amplification technologies.

Rapid molecular platforms enable earlier detection of active tuberculosis and drug-resistant strains, reducing transmission risks and improving treatment outcomes. Expanding reimbursement support, procurement initiatives, and laboratory modernization programs across high-burden countries continues to increase the adoption of advanced TB diagnostic testing solutions.

Restraint - Infrastructure Gaps and Uneven Diagnostic Accessibility

According to the World Health Organization (WHO) Global Tuberculosis Report 2025, access to WHO-recommended rapid diagnostic tests remains uneven, with only 8 of 30 high-burden TB countries reporting that more than half of diagnostic sites had access to rapid molecular testing in 2024. This reflects persistent gaps in laboratory infrastructure, workforce availability, and diagnostic network coverage across resource-constrained regions.

In addition, WHO and the Stop TB Partnership report that global tuberculosis research funding stood at approximately US$1.2 billion in 2023, significantly below the US$5 billion annual target required to achieve End TB Strategy goals. These financial and infrastructure constraints continue to restrict the scale-up of advanced tuberculosis diagnostic testing solutions and slow adoption of next-generation technologies in emerging markets.

Opportunity - Emergence of AI-Enabled and Point-of-Care Diagnostic Platforms

A major growth opportunity lies in the advancement of point-of-care tuberculosis diagnostics, AI-enabled radiography technologies, and portable molecular testing platforms. According to the World Health Organization (WHO), nearly 100 tuberculosis diagnostic products were under development as of August 2025, highlighting strong innovation momentum within the industry. The development pipeline encompasses biomarker-based rapid diagnostic tests, simplified nucleic acid amplification technologies, next-generation sequencing platforms, and computer-aided detection software designed to enhance digital chest imaging and support earlier, more accurate tuberculosis diagnosis.

These technologies address critical unmet needs in rural and underserved populations where laboratory infrastructure remains limited. Governments across Asia Pacific and Africa are increasingly prioritizing decentralized testing models to improve case detection rates. The commercialization of affordable, near-patient diagnostic solutions is expected to create substantial revenue opportunities for manufacturers targeting high-burden tuberculosis regions.

Category-wise Analysis

Test Type Insight

Nucleic Acid Testing (NAT) is expected to hold the dominant position in the tuberculosis diagnostics market with an estimated 46% revenue share in 2026, driven by its high sensitivity, rapid turnaround time, and strong ability to detect drug-resistant TB strains. Its leadership is reinforced by WHO guidelines recommending molecular diagnostics as the preferred first-line testing method, along with large-scale adoption of platforms such as GeneXpert and Truenat under national TB elimination programs in countries like India and across Africa.

Nucleic Acid Testing (NAT) is also projected to be the fastest-growing segment at 7% CAGR through 2033, supported by increasing demand for decentralized testing, government-backed TB control initiatives, and continued technological advancements that are enabling portable, cost-effective molecular diagnostic systems for wider rural and district-level deployment.

End-user Insights

Hospitals & clinics are expected to dominate the tuberculosis diagnostics market, with around a 52% share in 2026, driven by strong diagnostic infrastructure, high patient inflow, and integration of molecular and radiography systems under national TB control programs. Their leadership is reinforced by widespread adoption of WHO-recommended rapid molecular testing such as GeneXpert, supported by government-funded initiatives in high-burden countries like India, Indonesia, and South Africa. Continuous upgrades in hospital laboratory networks and centralized diagnostic systems are further improving detection efficiency and strengthening their role as the primary hub for TB diagnosis and treatment initiation.

Diagnostic centers are anticipated to be the fastest-growing segment, expanding at an estimated 6.5% CAGR through 2033, driven by rising outsourcing of tuberculosis testing, rapid expansion of private laboratory networks, and increasing demand for faster and more accessible diagnostics. Growth is supported by investments in automated molecular platforms, digital reporting systems, and integrated lab chains. For instance, in countries like India, the National TB Elimination Programme (NTEP), Ministry of Health & Family Welfare, has formally integrated private diagnostic providers into TB screening and mandatory notification systems via the Nikshay platform and PPP models, strengthening their role in national TB detection efforts. This structured public-private integration is making diagnostic centres a key growth driver in the evolving tuberculosis diagnostics market.

Regional Insights

North America Tuberculosis Diagnostics Market Trends

North America is projected to account for about 27% of the global tuberculosis diagnostics market share in 2026, supported by advanced healthcare systems and strong adoption of NAAT-based molecular testing. The region benefits from well-established CDC-led surveillance programs, widespread use of automated laboratory workflows, and routine integration of digital radiography in hospitals. Continuous investments in infectious disease preparedness and drug-resistance monitoring are also reinforcing demand for high-precision diagnostic tools.

U.S. Tuberculosis Diagnostics Market Trends

The U.S. is expected to hold nearly 85% of the regional market share in 2026, driven by extensive deployment of GeneXpert and other NAAT platforms across hospitals and public health laboratories. TB diagnostics are closely embedded in CDC screening frameworks, enabling structured case detection and monitoring. In recent years, there has been a noticeable push to integrate real-time reporting systems and strengthen infectious disease preparedness networks, particularly in response to rising concerns about antimicrobial resistance and imported TB cases.

Canada Tuberculosis Diagnostics Market Trends

Canada is likely to contribute around 15% of the regional market share in 2026, supported by a centralized public healthcare system and strong provincial laboratory networks. Molecular testing and radiography remain key tools for targeted TB screening, especially in high-risk and remote populations. Recent efforts have focused on improving diagnostic access in northern regions through mobile and outreach-based testing models.

Europe Tuberculosis Diagnostics Market Trends

Europe is expected to account for close to 23% of the global market share, supported by structured healthcare systems and a strong reliance on molecular diagnostics and digital radiography. Countries such as Germany, the U.K., France, and Spain lead demand, though underdiagnosis in certain areas continues to drive the need for improved screening coverage and faster detection pathways.

Germany Tuberculosis Diagnostics Market Trends

Germany is anticipated to lead the Europe market with about a 32% share, supported by advanced laboratory infrastructure and high adoption of automated molecular testing systems. Hospitals are increasingly integrating digital and AI-enabled diagnostic tools to improve accuracy and workflow efficiency. Recent upgrades in lab networks are strengthening centralized infectious disease testing capabilities.

U.K. Tuberculosis Diagnostics Market Trends

The U.K. is projected to account for around 18% of the regional market share, driven by NHS-led TB screening and targeted testing in high-risk urban groups. Molecular diagnostics and centralized reporting systems are widely used to reduce diagnostic delays. Recent improvements in community-based testing models are enhancing early detection in metropolitan areas.

Asia Pacific Tuberculosis Diagnostics Market Trends

Asia Pacific is expected to dominate the global landscape with approximately a 38% share in 2026, largely due to its heavy tuberculosis burden and rapid expansion of diagnostic access. The region is undergoing a visible shift toward decentralized molecular testing, mobile screening initiatives, and AI-enabled radiography systems. Governments across the region are actively scaling up national TB elimination programs, while private diagnostic networks are increasingly complementing public health infrastructure. This combination of demand pressure and system expansion makes Asia Pacific the most dynamic region in the market.

India Tuberculosis Diagnostics Market Trends

India is expected to stand at the center of regional demand with roughly a 35% regional market share in 2026, driven by its large TB burden and aggressive national response under the National TB Elimination Programme (NTEP). Diagnostic expansion has been particularly strong in TrueNat and CBNAAT platforms, which are now widely deployed across district hospitals and public health centers. A key shift in recent years has been the deeper integration of private diagnostic providers through mandatory reporting systems and PPP models, alongside large-scale active case-finding campaigns aimed at improving early detection in both rural and urban settings.

China Tuberculosis Diagnostics Market Trends

China is set to contribute around 25% of the Asia Pacific market share in 2026, supported by the continuous modernization of its infectious disease diagnostic infrastructure. The country has been steadily upgrading its tuberculosis detection ecosystem through high-throughput molecular laboratories, digital imaging systems, and AI-supported screening tools in major hospitals. Recent public health efforts have focused on strengthening surveillance networks and improving early diagnosis capabilities, particularly through centralized lab upgrades and broader adoption of automated diagnostic platforms across provincial healthcare systems.

Competitive Landscape

The global tuberculosis diagnostics market is moderately consolidated, with key players such as Roche Diagnostics, Danaher (Cepheid), Abbott, Siemens Healthineers, and bioMérieux accounting for a major share of revenue. These companies maintain leadership through strong NAAT-based molecular diagnostic platforms, integrated laboratory solutions, and long-standing partnerships with public health systems and WHO-supported procurement programs. Continuous R&D investments in rapid testing, automation, and drug-resistance detection further strengthen their competitive position.

Alongside global leaders, regional players like Molbio Diagnostics and Trivitron Healthcare are expanding their presence through affordable point-of-care molecular testing and portable diagnostic systems, particularly in high-burden regions. While entry barriers remain high due to regulatory approvals and clinical validation requirements, growth in decentralized TB testing and AI-enabled diagnostic tools is opening space for niche technology providers. The market is gradually consolidating further through acquisitions and strategic partnerships, as companies focus on expanding geographic reach and strengthening diagnostic technology portfolios.

Key Industry Developments:

- In February 2025, QIAGEN received a favorable court ruling reaffirming a key QuantiFERON-TB patent. The decision, announced recently, upheld the validity of one of QIAGEN’s core patents related to its QuantiFERON-TB diagnostic technology.

- In April 2024, QIAGEN expanded its tuberculosis portfolio with a new NGS panel to support real-time surveillance and combat antimicrobial resistance. The company launched the panel as part of its ongoing efforts to enhance TB detection and resistance monitoring through next-generation sequencing technology.

Companies Covered in Tuberculosis Diagnostics Market

- Roche Diagnostics

- Danaher Corporation

- Abbott Laboratories

- Becton, Dickinson and Company

- Siemens Healthineers

- QIAGEN N.V.

- bioMérieux

- Hologic Inc.

- FUJIFILM Holdings Corporation

- Thermo Fisher Scientific

- Sysmex Corporation

- Agilent Technologies

- PerkinElmer Inc

- Trivitron Healthcare

- Molbio Diagnostics

Frequently Asked Questions

The global tuberculosis diagnostics market is projected to reach US$38.0 billion in 2026.

Rising TB burden, expansion of molecular diagnostics, and government-led screening programs drive the market.

The market is expected to grow at a CAGR of 5.8% from 2026 to 2033.

Growth is driven by decentralized molecular testing, AI-based radiography, and point-of-care diagnostic expansion in high-burden regions.

Key players include Roche Diagnostics, Danaher (Cepheid), Abbott, Siemens Healthineers, and bioMérieux.