- Medical Devices

- Surgical Drill Bits Market

Surgical Drill Bits Market Size, Share, and Growth Forecast, 2026 - 2033

Surgical Drill Bits Market by Product Type (Standard Solid Drill Bits, Others), Application (Orthopedic Surgery, Others), End-user (Hospitals, Specialty Clinics, Ambulatory Surgical Centers, Research Institutes & Academic Centers), and Regional Analysis for 2026 - 2033

Surgical Drill Bits Market Size and Trends Analysis

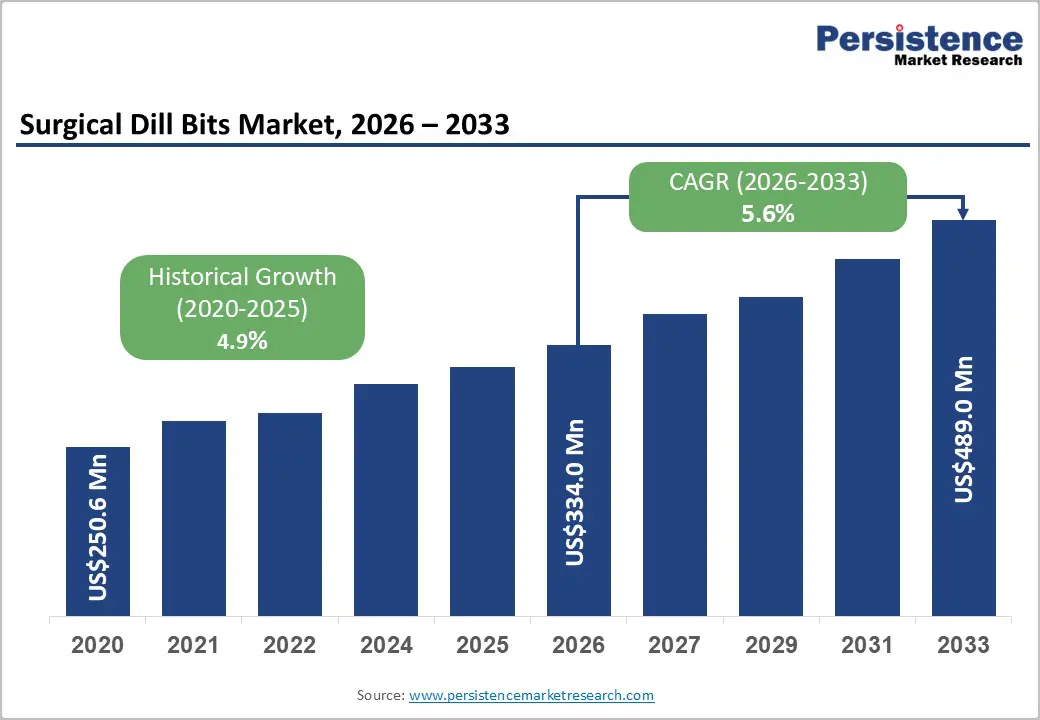

The global surgical drill bits market size is likely to be valued at US$ 334.0 million in 2026, and is expected to reach US$ 489.0 million by 2033, growing at a CAGR of 5.6% during the forecast period from 2026 to 2033, driven by rising global surgical volumes, accelerating adoption of minimally invasive surgical techniques, increasing joint replacement and spinal fixation procedure volumes driven by an aging global population, and continuous product innovation by leading medical device manufacturers.

Key Industry Highlights:

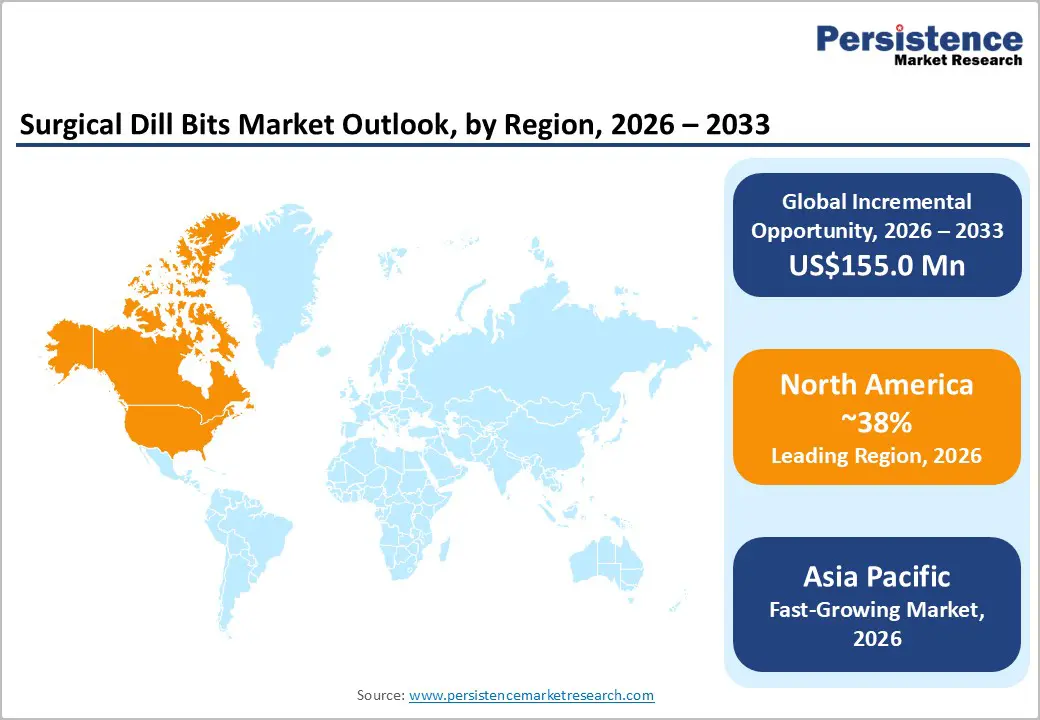

- Dominant Region: North America is expected to dominate with an estimated 38% revenue share in 2026, driven by the world's highest total joint arthroplasty procedure volumes, advanced hospital surgical infrastructure, comprehensive surgical reimbursement frameworks, and the concentrated presence of DePuy Synthes, Stryker, Zimmer Biomet, Arthrex, and Medtronic.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing market, driven by rapidly expanding surgical procedure volumes, growing orthopedic and dental implant market penetration, and healthcare infrastructure investment across China, India, and Southeast Asia.

- Leading Product Type: Cannulated drill bits are anticipated to dominate with approximately 42% share in 2026, reflecting their essential role in minimally invasive orthopedic fixation procedures, including hip fracture repair, ACL reconstruction, and percutaneous pedicle screw placement, where guidewire-over precision drilling is the clinical standard.

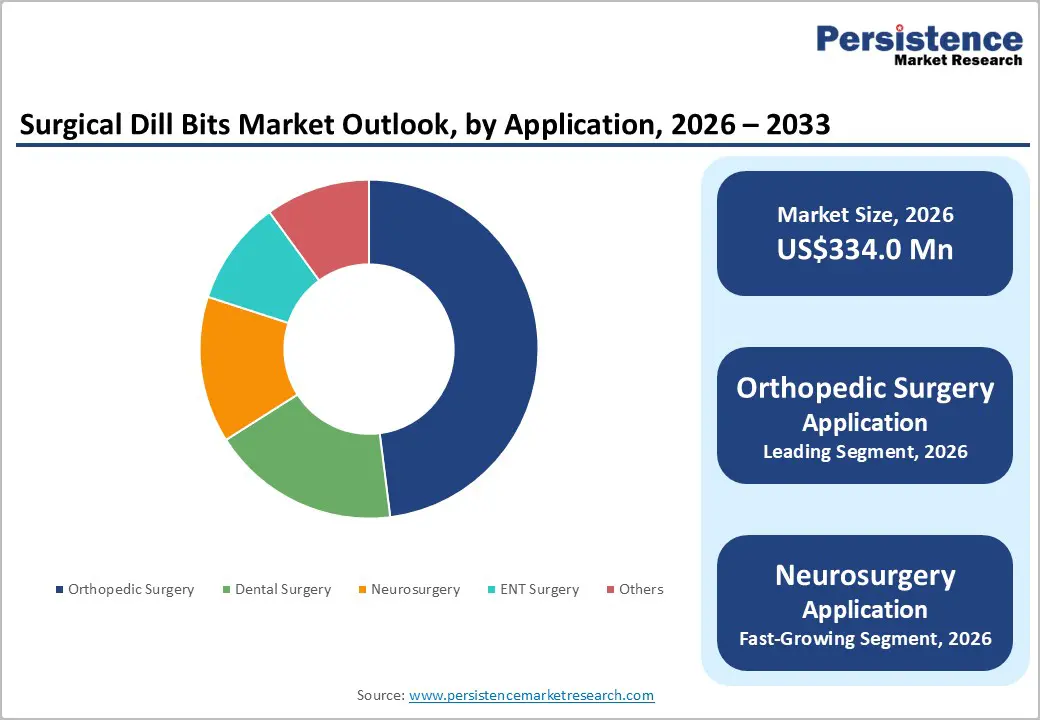

- Dominant End-use Industry: Orthopedic surgery is the leading application segment, accounting for approximately 48% of market value in 2026, driven by the enormous and growing global burden of joint degeneration, fracture fixation requirements, and spinal surgical procedures across aging patient populations.

DRO Analysis

Driver - Rising Global Orthopedic Procedure Volumes and Aging Population

The escalating global burden of musculoskeletal disease, driven by demographic aging, rising obesity rates, and increasing physical activity generating sports-related injuries, is a foundational demand driver for the market. Musculoskeletal conditions remain one of the leading causes of disability worldwide, significantly increasing the need for orthopedic interventions and reconstructive surgeries. Total hip and knee arthroplasty procedures, which require multiple surgical drill bit applications for bone canal preparation and fixation hardware placement, are among the fastest-growing elective surgical procedure categories globally.

Spinal surgical procedures, including spinal fusion, laminectomy, and disc replacement, represent another major surgical drill bit consumption category. The North American Spine Society reports approximately 500,000 spinal fusion procedures performed annually in the United States, each requiring multiple calibrated and cannulated drill bits for pedicle screw pilot hole preparation.

Restraint - Stringent Regulatory Requirements and Extended Product Development Timelines

Surgical drill bits are regulated as Class II medical devices in the United States (under FDA 21 CFR Part 880) and under the EU Medical Device Regulation (MDR, EU 2017/745) in Europe, regulatory frameworks imposing material qualification testing, biocompatibility assessment (ISO 10993), sterile packaging validation, and performance testing requirements that extend product development timelines and increase compliance costs.

ISO 5835 for powered medical equipment and ISO 7153-1 for surgical instrument materials establish baseline technical requirements that surgical drill bit manufacturers must satisfy across material selection, hardness specifications, and corrosion resistance. Sterilization cycle validation adds further burden for sterile-packed single-use drill bit manufacturers.

Opportunity - Single-Use Sterile Surgical Drill Bits and Infection Control Compliance

The global healthcare industry's heightened focus on surgical site infection (SSI) prevention, driven by the CDC's estimation that approximately 500,000 SSIs occur annually in U.S. healthcare facilities, generating an average additional cost of US$8,200-$42,000 per episode, is creating a significant and growing market opportunity for single-use, sterile-packed surgical drill bits that eliminate the cross-contamination risk associated with reusable instrument reprocessing. Hospitals implementing single-use surgical instrument programs report measurable reductions in SSI rates alongside reduced reprocessing labor and sterilization equipment maintenance costs.

Leading manufacturers, including MicroAire Surgical Instruments, B. Braun Melsungen AG, and Arthrex Inc., have developed sterile-packed single-use drill bit product lines targeting orthopedic and ENT surgical applications. The transition from reusable to single-use drill bits creates a structural volume multiplier, converting capital instrument purchases with multi-year depreciation cycles into recurring consumable purchases, potentially doubling or tripling annual drill bit procurement volumes in converted facilities.

Category-wise Analysis

Product Type Insights

Cannulated drill bits are expected to dominate the product type, commanding approximately 42% of total global revenue in 2026. Their market leadership is driven by their critical role in high-volume orthopedic procedures, including hip fracture fixation, ACL reconstruction, and minimally invasive spinal surgeries. Stryker offers the Asnis III Cannulated Screw System, which utilizes cannulated drill bits for femoral neck fracture fixation and other orthopedic trauma applications.

Calibrated drill bits are also projected to be the fastest-growing product type, driven by expanding adoption of depth-controlled drilling protocols in orthopedic implant surgery, where precise screw length determination requires exact drill depth measurement and integration into robotic-assisted bone preparation systems requiring instruments with tight dimensional specification and machine-readable depth markings. DePuy Synthes offers calibrated drill bits within its orthopedic trauma and spine instrumentation portfolio, designed with laser-marked depth graduations to support accurate screw placement and surgical precision in fixation procedures.

Application Insights

Orthopedic surgery is anticipated to dominate the application segment, accounting for approximately 48% of market revenue in 2026. The segment's leadership reflects the enormous and growing volume of bone drilling required across the full spectrum of orthopedic operative procedures, from simple cortical screw fixation of simple fractures through to complex multi-level spinal instrumentation and total joint arthroplasty revision surgery. Zimmer Biomet provides orthopedic drill systems widely used in trauma, spine, and joint reconstruction surgeries for bone preparation and implant fixation.

Neurosurgery is likely to be the fastest-growing application segment. The expansion of minimally invasive neurosurgical procedures, including endoscopic skull base surgery, MRI-guided stereotactic biopsy, deep-brain stimulation lead placement, and endoscopic third ventriculostomy, is driving growing demand for ultra-precision, low-thermal-injury neurosurgical drill bits compatible with navigation system guidance and narrow endoscopic access portals. Stryker offers the CORE 2 Neurosurgical High-Speed Drill System, designed for cranial and skull base procedures with precision drilling, reduced thermal injury, and compatibility with advanced surgical navigation technologies.

End-user Insights

Hospitals are estimated to dominate the end-user segment, capturing approximately 58% of the total share in 2026. Major academic medical centers and tertiary care hospitals, which perform the highest volumes of complex orthopedic, spinal, neurosurgical, and ENT procedures, generate the largest institutional demand for full-range surgical drill bit complement procurement, including premium cannulated and calibrated product lines. Cleveland Clinic is one of the leading U.S. tertiary care hospitals performing advanced orthopedic and neurosurgical procedures that require extensive use of surgical drill systems and precision drill bits.

Ambulatory surgical centers (ASCs) represent the fastest-growing end-user segment. The accelerating migration of elective orthopedic procedures, including outpatient total knee arthroplasty, outpatient total hip arthroplasty, ACL reconstruction, and rotator cuff repair from hospital inpatient settings to ASC environments, is driven by CMS reimbursement policy changes that have progressively added procedures to the ASC-approved payment list. Surgery Partners operates a large network of ASCs across the U.S. that perform outpatient orthopedic and sports medicine procedures requiring advanced surgical drilling and fixation systems.

Regional Insights

North America Surgical Drill Bits Market Trends

Market growth in North America is projected to dominate, holding approximately 38% of total revenue in 2026. The U.S. market value is driven by the world's highest total joint arthroplasty procedure volumes, the largest concentration of academic medical center robotic surgical programs, comprehensive CMS Medicare reimbursement frameworks for orthopedic and spinal surgical procedures, and the operational headquarters of multiple leading surgical drill bit manufacturers.

U.S. Surgical Drill Bits Market Insights

The U.S. surgical drill bits market is driven by the high volume of joint replacement, spinal fusion, and ACL reconstruction procedures performed across the country. CMS reimbursement policy changes, including the removal of total knee arthroplasty from the inpatient-only list and the addition of hip arthroplasty to the ASC-approved procedure list, have accelerated the shift of orthopedic surgeries toward outpatient ambulatory surgical center settings, increasing demand for surgical drill bits in ASCs.

Canada Surgical Drill Bits Market Insights

Canada’s market growth is being propelled by rising orthopedic surgical procedure volumes across provincial hospital networks, as tracked by Canada Health Infoway. In addition, the Canadian Joint Replacement Registry (CJRR) reports steady increases in hip and knee arthroplasty procedures, creating sustained demand for drill bits through hospital supply chain procurement systems.

Europe Surgical Drill Bits Market Trends

Europe market shows steady growth, driven by aging population demographics generating growing orthopedic and dental procedure volumes, strong hospital surgical infrastructure, EU MDR-aligned quality frameworks governing surgical instrument market access, and the commercial headquarters of B. Braun Melsungen AG, De Soutter Medical Ltd., and Adeor Medical AG.

Germany Surgical Drill Bits Market Trends

Germany is the leading European market, driven by world-class orthopedic and spine surgical programs at major university hospitals and the Berufsgenossenschaftliche (BG) trauma center network performing some of Europe's highest volumes of complex trauma and orthopedic reconstruction surgery. B. Braun Melsungen AG, headquartered in Melsungen, maintains significant domestic and European market presence through its comprehensive surgical instrument and orthopedic product portfolio.

U.K. Surgical Drill Bits Market Trends

The U.K. market is shaped by NHS surgical procedure commissioning frameworks and NHS Supply Chain procurement pathways, consolidating instrument purchasing across NHS trusts through national framework agreements. NHS England's elective recovery program, launched to address the surgical backlog accumulated during COVID-19, is generating above-trend orthopedic and ENT surgical procedure volume growth, directly increasing surgical drill bit consumption through NHS hospital and independent sector treatment center (ISTC) settings.

Asia Pacific Surgical Drill Bits Market Trends

Asia Pacific is likely to be the fastest-growing, driven by rapidly growing surgical procedure volumes, expanding hospital and ASC infrastructure, rising orthopedic and dental implant market penetration, and increasing adoption of advanced surgical techniques.

China Surgical Drill Bits Market Trends

The China market is experiencing strong growth due to the rapid expansion of orthopedic, spinal, and trauma surgery volumes supported by the country’s aging population and rising incidence of sports and road accident injuries. Domestic medical device manufacturers are expanding production capabilities, while international companies continue strengthening their presence through partnerships and local manufacturing.

India Surgical Drill Bits Market Trends

India is one of the fastest-growing surgical drill bits markets in Asia Pacific, driven by the rapidly expanding private hospital and specialty surgical center network, growing orthopedic implant market penetration, and increasing access to tertiary surgical care through the Ayushman Bharat PM-JAY insurance scheme, covering approximately 500 million beneficiaries. India's high rates of road traffic accident trauma, generating fracture fixation demand, and growing osteoarthritis prevalence sustain consistent and growing orthopedic and trauma surgery drill bit consumption.

Competitive Landscape

The global surgical drill bits market is moderately consolidated at the premium segment level, with Johnson & Johnson, Stryker Corporation, Zimmer Biomet Holdings Inc., and Smith & Nephew plc leading the market through their comprehensive implant system-matched drill bit portfolios and strong hospital system relationships. DePuy Synthes leads through the breadth and depth of its surgical trauma, joint reconstruction, and spine instrument portfolios, offering drill bit sets specifically engineered for each implant system that create system-locked procurement relationships sustaining predictable recurring revenue.

Specialty and mid-tier competitors serve distinct applications and market segments with focused product strategies. Arthrex Inc. commands strong positions in sports medicine and arthroscopic surgical drill bits, with its comprehensive ACL reconstruction and rotator cuff repair drill bit systems widely used across North American and European arthroscopic surgery markets. B. Braun Melsungen AG and De Soutter Medical Ltd. serve the European hospital market with quality-certified instrument portfolios.

Key Industry Developments:

- In March 2025, Stryker, a worldwide frontrunner in medical technologies, exhibited the cutting-edge research of Mako SmartRobotics™ in hip, knee, spine, and shoulder surgeries at the American Academy of Orthopaedic Surgeons’ (AAOS) 2025 Annual Meeting held in San Diego. Mako is a market-leading technology in orthopedics with more than 1.5 million Mako procedures done all over the world in 45 different countries.

Companies Covered in Surgical Drill Bits Market

- Johnson & Johnson

- Zimmer Biomet Holdings Inc.

- Stryker Corporation

- Medtronic plc

- CONMED Corporation

- Arthrex Inc.

- B. Braun Melsungen AG

- AlloTech Co. Ltd.

- Smith & Nephew plc

- De Soutter Medical Ltd.

- Brasseler USA

- MicroAire Surgical Instruments LLC

- ClearPoint Neuro Inc.

- Integra LifeSciences Holdings Corporation

- Adeor Medical AG

Frequently Asked Questions

The global surgical drill bits market is projected to reach US$334.0 million in 2026.

The rising volume of orthopedic, spinal, and trauma surgeries worldwide is driving strong demand for surgical drill bits used in bone drilling and implant fixation procedures.

The surgical drill bits market is poised to witness a CAGR of 5.6% from 2026 to 2033.

The rapid expansion of outpatient orthopedic procedures in ambulatory surgical centers (ASCs) is creating significant growth opportunities for compact and cost-efficient surgical drill systems.

Key players include Johnson & Johnson, Zimmer Biomet Holdings Inc., Stryker Corporation, Medtronic plc, CONMED Corporation, Arthrex Inc., B. Braun Melsungen AG, AlloTech Co. Ltd., Smith & Nephew plc, De Soutter Medical Ltd., Brasseler USA, MicroAire Surgical Instruments LLC, ClearPoint Neuro Inc., Integra LifeSciences Holdings Corporation, and Adeor Medical AG.