- Executive Summary

- Global Surgical Wound Matrix Market Snapshot, 2026 and 2033

- Market Opportunity Assessment, 2026 - 2033, US$ Bn

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Challenges

- Key Trends

- COVID-19 Impact Analysis

- Forecast Factors - Relevance and Impact

- Value Added Insights

- Value Chain Analysis

- Key Market Players

- Regulatory Landscape

- PESTLE Analysis

- Porter’s Five Force Analysis

- Consumer Behavior Analysis

- Price Trend Analysis, 2020-2025

- Key Factors Impacting Product Prices

- Pricing Analysis, By Product Type

- Regional Prices and Product Preferences

- Global Surgical Wound Matrix Market Outlook

- Market Size (US$ Bn) Analysis and Forecast

- Historical Market Size (US$ Bn) Analysis, 2020-2025

- Market Size (US$ Bn) Analysis and Forecast, 2026-2033

- Global Surgical Wound Matrix Market Outlook: Product Type

- Historical Market Size (US$ Bn) Analysis, By Product Type, 2020-2025

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2026-2033

- Foam Dressings

- Hydrocolloid Dressings

- Film Dressings

- Alginate Dressings

- Hydrogel Dressings

- Collagen Dressings

- Other

- Market Attractiveness Analysis: Product Type

- Global Surgical Wound Matrix Market Outlook: Application

- Historical Market Size (US$ Bn) Analysis, By Application, 2020-2025

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2026-2033

- Diabetic Foot Ulcers

- Pressure Ulcers

- Venous Ulcers

- Surgical & Traumatic Wounds

- Burns

- Others

- Market Attractiveness Analysis: Application

- Global Surgical Wound Matrix Market Outlook: End-user

- Historical Market Size (US$ Bn) Analysis, By End-user, 2020-2025

- Market Size (US$ Bn) Analysis and Forecast, By End-user, 2026-2033

- Hospitals

- Specialty Clinics

- Home Healthcare

- Others

- Market Attractiveness Analysis: End-user

- Market Size (US$ Bn) Analysis and Forecast

- Global Surgical Wound Matrix Market Outlook: Region

- Historical Market Size (US$ Bn) Analysis, By Region, 2020-2025

- Market Size (US$ Bn) Analysis and Forecast, By Region, 2026-2033

- North America

- Latin America

- Europe

- East Asia

- South Asia and Oceania

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Surgical Wound Matrix Market Outlook

- Historical Market Size (US$ Bn) Analysis, By Market, 2020-2025

- By Country

- By Product Type

- By Application

- By End-user

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026-2033

- U.S.

- Canada

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2026-2033

- Foam Dressings

- Hydrocolloid Dressings

- Film Dressings

- Alginate Dressings

- Hydrogel Dressings

- Collagen Dressings

- Other

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2026-2033

- Diabetic Foot Ulcers

- Pressure Ulcers

- Venous Ulcers

- Surgical & Traumatic Wounds

- Burns

- Others

- Market Size (US$ Bn) Analysis and Forecast, By End-user, 2026-2033

- Hospitals

- Specialty Clinics

- Home Healthcare

- Others

- Market Attractiveness Analysis

- Historical Market Size (US$ Bn) Analysis, By Market, 2020-2025

- Europe Surgical Wound Matrix Market Outlook

- Historical Market Size (US$ Bn) Analysis, By Market, 2020-2025

- By Country

- By Product Type

- By Application

- By End-user

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026-2033

- Germany

- France

- U.K.

- Italy

- Spain

- Russia

- Rest of Europe

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2026-2033

- Foam Dressings

- Hydrocolloid Dressings

- Film Dressings

- Alginate Dressings

- Hydrogel Dressings

- Collagen Dressings

- Other

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2026-2033

- Diabetic Foot Ulcers

- Pressure Ulcers

- Venous Ulcers

- Surgical & Traumatic Wounds

- Burns

- Others

- Market Size (US$ Bn) Analysis and Forecast, By End-user, 2026-2033

- Hospitals

- Specialty Clinics

- Home Healthcare

- Others

- Market Attractiveness Analysis

- Historical Market Size (US$ Bn) Analysis, By Market, 2020-2025

- East Asia Surgical Wound Matrix Market Outlook

- Historical Market Size (US$ Bn) Analysis, By Market, 2020-2025

- By Country

- By Product Type

- By Application

- By End-user

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026-2033

- China

- Japan

- South Korea

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2026-2033

- Foam Dressings

- Hydrocolloid Dressings

- Film Dressings

- Alginate Dressings

- Hydrogel Dressings

- Collagen Dressings

- Other

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2026-2033

- Diabetic Foot Ulcers

- Pressure Ulcers

- Venous Ulcers

- Surgical & Traumatic Wounds

- Burns

- Others

- Market Size (US$ Bn) Analysis and Forecast, By End-user, 2026-2033

- Hospitals

- Specialty Clinics

- Home Healthcare

- Others

- Market Attractiveness Analysis

- Historical Market Size (US$ Bn) Analysis, By Market, 2020-2025

- South Asia & Oceania Surgical Wound Matrix Market Outlook

- Historical Market Size (US$ Bn) Analysis, By Market, 2020-2025

- By Country

- By Product Type

- By Application

- By End-user

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026-2033

- India

- Indonesia

- Thailand

- Singapore

- ANZ

- Rest of South Asia & Oceania

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2026-2033

- Foam Dressings

- Hydrocolloid Dressings

- Film Dressings

- Alginate Dressings

- Hydrogel Dressings

- Collagen Dressings

- Other

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2026-2033

- Diabetic Foot Ulcers

- Pressure Ulcers

- Venous Ulcers

- Surgical & Traumatic Wounds

- Burns

- Others

- Market Size (US$ Bn) Analysis and Forecast, By End-user, 2026-2033

- Hospitals

- Specialty Clinics

- Home Healthcare

- Others

- Market Attractiveness Analysis

- Historical Market Size (US$ Bn) Analysis, By Market, 2020-2025

- Latin America Surgical Wound Matrix Market Outlook

- Historical Market Size (US$ Bn) Analysis, By Market, 2020-2025

- By Country

- By Product Type

- By Application

- By End-user

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026-2033

- Brazil

- Mexico

- Rest of Latin America

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2026-2033

- Foam Dressings

- Hydrocolloid Dressings

- Film Dressings

- Alginate Dressings

- Hydrogel Dressings

- Collagen Dressings

- Other

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2026-2033

- Diabetic Foot Ulcers

- Pressure Ulcers

- Venous Ulcers

- Surgical & Traumatic Wounds

- Burns

- Others

- Market Size (US$ Bn) Analysis and Forecast, By End-user, 2026-2033

- Hospitals

- Specialty Clinics

- Home Healthcare

- Others

- Market Attractiveness Analysis

- Historical Market Size (US$ Bn) Analysis, By Market, 2020-2025

- Middle East & Africa Surgical Wound Matrix Market Outlook

- Historical Market Size (US$ Bn) Analysis, By Market, 2020-2025

- By Country

- By Product Type

- By Application

- By End-user

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026-2033

- GCC Countries

- Egypt

- South Africa

- Northern Africa

- Rest of Middle East & Africa

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2026-2033

- Foam Dressings

- Hydrocolloid Dressings

- Film Dressings

- Alginate Dressings

- Hydrogel Dressings

- Collagen Dressings

- Other

- Market Size (US$ Bn) Analysis and Forecast, By Application, 2026-2033

- Diabetic Foot Ulcers

- Pressure Ulcers

- Venous Ulcers

- Surgical & Traumatic Wounds

- Burns

- Others

- Market Size (US$ Bn) Analysis and Forecast, By End-user, 2026-2033

- Hospitals

- Specialty Clinics

- Home Healthcare

- Others

- Market Attractiveness Analysis

- Historical Market Size (US$ Bn) Analysis, By Market, 2020-2025

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping By Market

- Competition Dashboard

- Company Profiles (Details - Overview, Financials, Strategy, Recent Developments)

- Mölnlycke Health Care Ab

- Overview

- Segments and Product Type

- Key Financials

- Market Developments

- Market Strategy

- 3M

- Convatec Group Plc

- Baxter

- Coloplast Corp.

- Medtronic

- Derma Sciences Inc.

- Medline Industries Inc.

- Smith & Nephew Plc.

- Mölnlycke Health Care Ab

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Medical Devices

- Surgical Wound Matrix Market

Surgical Wound Matrix Market Size, Share, and Growth Forecast, 2026 - 2033

Surgical Wound Matrix Market by Product Type (Foam Dressings, Hydrocolloid Dressings, Film Dressings, Alginate Dressings, Other), Application (Diabetic Foot Ulcers, Pressure Ulcers, Others), End-user, and Regional Analysis for 2026 - 2033

Surgical Wound Matrix Market Size and Trends Analysis

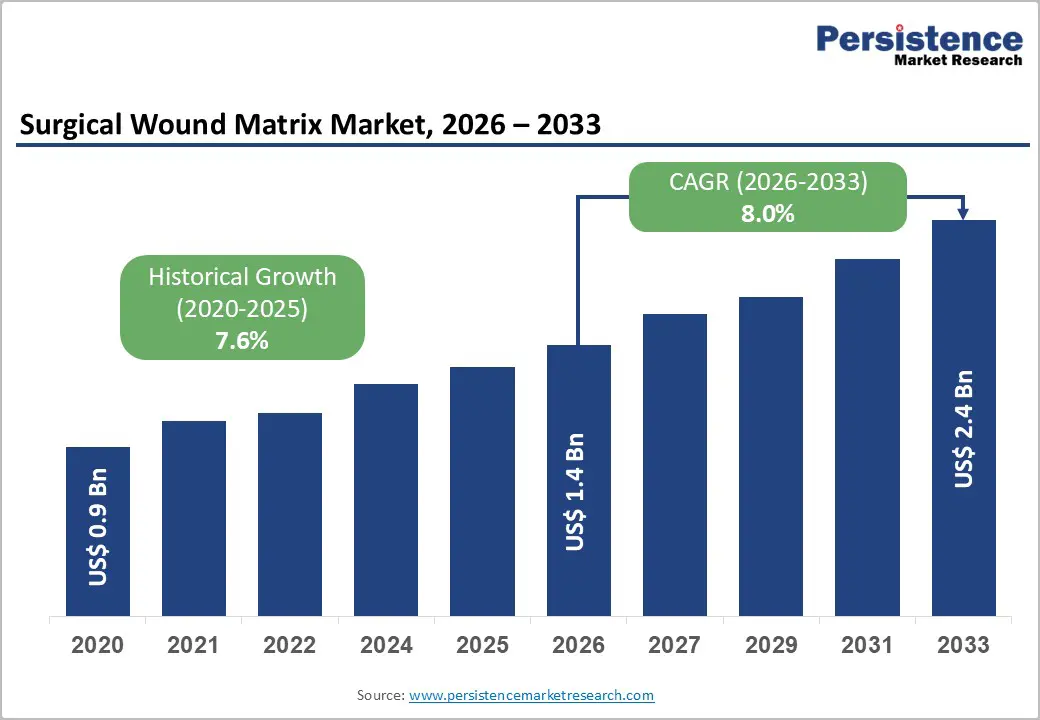

The global surgical wound matrix market size is likely to be valued at US$1.4 billion in 2026, and is expected to reach US$2.4 billion by 2033, growing at a CAGR of 8.0% during the forecast period from 2026 to 2033, driven by the increasing prevalence of chronic wounds and surgical site complications, rising demand for advanced wound care dressings that promote moist healing and reduce infection risk, and growing adoption of bioactive and antimicrobial matrices in hospitals and home healthcare settings.

The growing demand for foam dressings and collagen-based matrices, particularly for diabetic foot ulcers and surgical wounds, is driving adoption in hospitals and specialty clinics. Innovations such as silver-impregnated foams, bioactive collagen scaffolds, and negative-pressure compatible matrices are accelerating healing by promoting faster epithelialization and shorter recovery times. The increasing recognition of surgical wound matrices for reducing readmissions, improving patient outcomes, and cutting wound care costs is further fueling market growth, especially in emerging chronic wound and post-surgical sectors.

Key Industry Highlights:

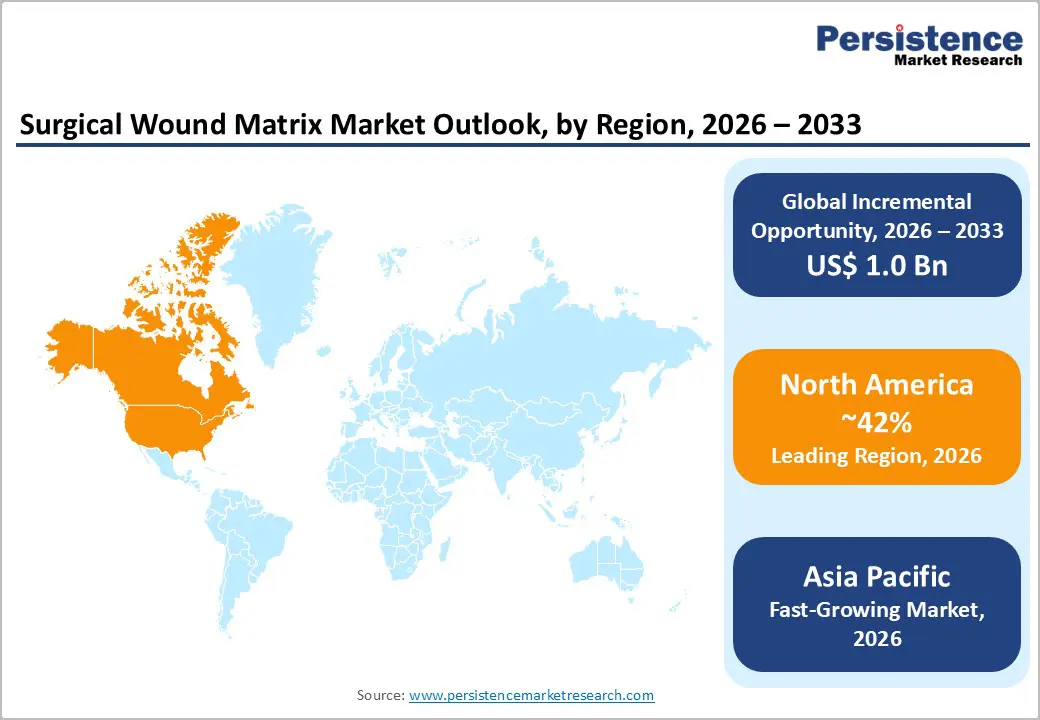

- Leading Region: North America, anticipated to account for a 42% market share in 2026, driven by high chronic wound prevalence, advanced reimbursement policies, and strong demand in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by rising diabetes incidence, increasing surgical volumes, and expanding advanced wound care access in India and China.

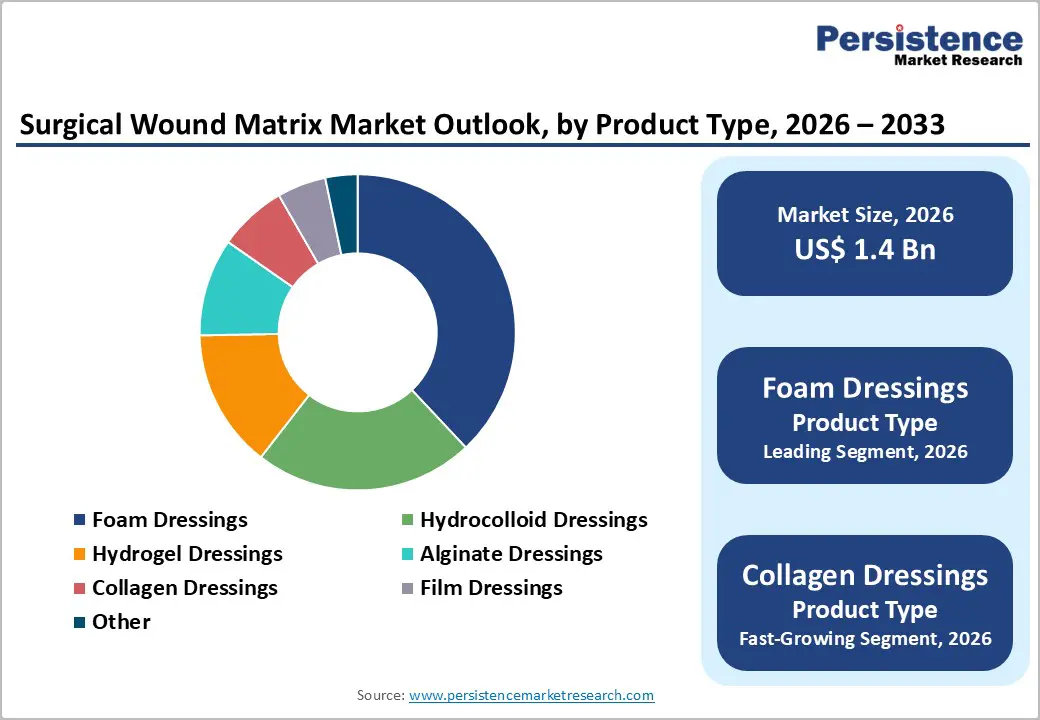

- Dominant Product: Foam dressings, to hold approximately 38% of the market share, as they remain the most widely used advanced dressing category.

- Leading Application: Diabetic foot ulcers, contributing nearly 35% of the market revenue, due to the highest chronic wound burden.

| Key Insights | Details |

|---|---|

|

Surgical Wound Matrix Market Size (2026E) |

US$1.4 Bn |

|

Market Value Forecast (2033F) |

US$2.4 Bn |

|

Projected Growth CAGR (2026-2033) |

8.0% |

|

Historical Market Growth (2020-2025) |

7.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis – Rising Chronic Wound Burden and Advanced Dressing Adoption

Chronic wound care is a substantial public-health issue that has been steadily increasing in recent years. In the U.S., about one in six Medicare beneficiaries, roughly 10.5 million people, are affected by chronic non-healing wounds, with prevalence rising from 14.5% in 2014 to 16.3% by 2019, as reported in a U.S. federal health compendium on wound burden. These wounds have significant health care implications, costing Medicare an estimated $22.5 billion annually and impacting quality of life across age groups. Chronic wounds often result from underlying conditions such as diabetes, peripheral artery disease, and pressure injuries, contributing to high rates of hospitalization and ongoing care needs. This growing patient population increases clinical demand for effective management approaches that go beyond standard dressings, underscoring the scale of the problem and the need for more advanced solutions.

Advanced dressings play a critical role in addressing complex and slow-healing wounds that do not respond to traditional wound care. Clinicians and health systems increasingly adopt technologies such as moisture-balancing foam dressings, hydrocolloids, antimicrobial materials, and bioengineered skin substitutes to improve healing outcomes, reduce infection rates, and lower the risk of complications such as amputations. These products are particularly relevant for chronic and post-surgical wounds where standard treatments fail to achieve timely closure, encouraging uptake across hospital, outpatient, and home settings. While comprehensive government adoption statistics are limited, the trend towards advanced wound care reflects a clinical emphasis on evidence-based interventions that optimize healing and reduce long-term costs within public health systems.

Outpatient and Home Healthcare Wound Management

Outpatient and home healthcare settings have become essential components of contemporary wound management as patients are discharged earlier from acute care facilities and require ongoing support outside of hospitals. In the outpatient setting, specialized wound clinics and ambulatory care units provide structured assessment, treatment planning, and follow-up care for both chronic and post-surgical wounds in patients who do not need overnight admission. These clinics employ licensed healthcare professionals to perform wound evaluations, provide dressing changes, and administer advanced therapies, tailoring treatment plans to the patient’s wound type and healing progress. In the home healthcare setting, skilled registered nurses and licensed practical nurses visit patients at home to provide wound care services, including wound cleaning, dressing changes, infection monitoring, and caregiver education on proper wound care techniques. Both settings emphasize individualized plans of care created and reviewed by attending physicians, with weekly documentation and measurable healing progress required for continued care eligibility under government health programs.

Outpatient and home management of wounds supports continuity of care and helps reduce demand on inpatient resources by enabling patients to heal outside the hospital environment, lowering the risk of readmission, and improving comfort for individuals with complex wounds. Home and outpatient care are particularly important for patients with chronic ulcers, pressure injuries, or non-healing surgical wounds that need frequent monitoring and dressing changes over time. Government-defined medical necessity criteria for these services include licensed supervision and individualized care plans, ensuring that wound care delivered in these settings maintains quality and effectiveness.

Barrier Analysis – High Cost of Advanced Wound Matrices

High cost remains a significant factor in the adoption and utilization of advanced wound matrices compared with traditional wound care products. These advanced matrices, including bioengineered skin substitutes and specialized extracellular matrices, are priced considerably higher due to the complex manufacturing processes and regulatory compliance required, which increases acquisition costs for healthcare providers. Clinical evidence shows that incremental treatment costs per additional successfully treated patient using certain advanced matrices can range substantially, with some products approaching US$29,952 per successful healing episode in venous leg ulcers, highlighting wide cost variance among options used in practice.

Government healthcare reimbursement frameworks influence the economic landscape for these products in markets such as the U.S. For instance, the Centers for Medicare & Medicaid Services (CMS) has implemented standardized reimbursement rates for skin substitutes (advanced wound matrices) that may not fully align with actual acquisition costs, potentially limiting provider willingness to adopt higher-priced innovations under fixed payment structures. These pricing and reimbursement pressures contribute to slower uptake in settings with constrained budgets, affecting how widely advanced matrices are used in clinical wound care.

Reimbursement Challenges and Regulatory Complexity

Reimbursement for advanced wound matrices, particularly skin substitutes and cellular/tissue-based products (CTPs) under government programs such as Medicare in the U.S., has become more complex and challenging for both providers and manufacturers. The Centers for Medicare & Medicaid Services (CMS) has restructured how these products are paid for under the 2026 Physician Fee Schedule, moving from varied product-specific pricing to a flat national payment rate (about US$127.28 per cm²) that applies regardless of product brand, composition, or regulatory pathway. This shift means providers must bill these products as incident-to supplies tied to a covered wound application procedure, raising the administrative burden around accurate coding and documentation for reimbursement eligibility.

Regulatory complexity further amplifies reimbursement challenges. CMS groups skin substitutes by FDA regulatory pathways (such as 361 HCT/P, 510(k), and PMA classifications) and plans to differentiate payment rates in future years, requiring clinicians and manufacturers to align coding precisely with regulatory status to avoid denials or audits. Practices now face increased audit activity focused on medical necessity and proper billing, and the uniform flat rate may not fully cover acquisition costs for higher-priced or advanced matrices, potentially limiting access and dampening incentives for innovation.

Opportunity Analysis – Expansion in Antimicrobial and Bioactive Wound Matrices

The growing focus on infection control and enhanced healing environments is encouraging wider use of antimicrobial and bioactive wound matrices in surgical and complex wound care. Chronic wounds affect an estimated 10.5 million U.S. Medicare beneficiaries, and this public-health burden underscores the need for solutions that address both prolonged healing and microbial challenges in wounds. Advanced matrices that embed antimicrobial agents, such as ionic silver or peptides, can help limit infection and biofilm formation, a key complication in which bacterial biofilms are present in up to 80% of infected chronic wounds, impairing healing and increasing the need for repeat interventions. Government-backed research, such as Small Business Innovation Research (SBIR) awards, highlights initiatives to develop antimicrobial matrix technologies that combine bacterial elimination with tissue regeneration, targeting hard-to-heal and drug-resistant infections in wound care. These developments align with broader public-health efforts to combat antimicrobial resistance and improve wound outcomes, as emphasized by national antimicrobial resistance programs aiming to reduce resistant infections across healthcare settings.

Clinicians increasingly recognize that integrating bioactive components into wound matrices can improve clinical outcomes by maintaining a controlled healing environment while mitigating infection risks that lead to prolonged treatment and higher healthcare utilization. Antimicrobial matrices that sustain ≥99.99% microbial reduction for extended periods have been cleared for use in surgical, burn, donor-site, and trauma wounds, offering practical options that align with regulatory approvals and safety standards. Enhanced healing profiles and infection control are key drivers for adoption in hospital and post-acute care pathways, supporting reduced complications, shorter healing times, and improved quality of life for patients with complex and surgical wounds.

Growing Elderly Population and Technology Innovation

The global demographic transition toward older populations is creating a larger patient pool with complex healthcare needs, which presents a significant opportunity for surgical wound matrix markets. According to World Health Organization (WHO) data, people aged 60 years and older are projected to nearly double their share of the world’s population, from 12% in 2015 to 22% by 2050, with 1.4 billion older adults expected by 2030. In India, according to government reports, seniors (60 +) already comprise around 9.7% of the population, up from 8.6% in 2011, and this share is rising steadily as fertility declines and life expectancy increases. Older adults are statistically more prone to surgical procedures and complications such as impaired healing, pressure injuries, and chronic ulcers, all of which heighten demand for advanced wound healing solutions such as surgical wound matrices. Growth in the elderly demographic thus directly expands the addressable patient base for these specialized biomaterials and regenerative products.

Innovations in technology are rapidly reshaping wound care and creating new avenues for market growth. Advances in smart biomaterials, biosensors, and AI-enhanced wound monitoring systems enable real-time assessment of wound conditions, tracking moisture, temperature, and biomarkers that are critical to timely and effective healing. Integration of digital health tools and wearable technologies with wound matrices improves clinical decision-making and can reduce healing time and complication rates. Such technological progress also supports telemedicine and remote patient management, which are increasingly relevant for elderly patients and home-based care pathways.

Category-wise Analysis

Product Type Insights

Foam dressings are anticipated to dominate the market, accounting for approximately 38% of the market share in 2026. Their popularity stems from a combination of excellent exudate management, cushioning protection, and patient comfort across a wide range of surgical and chronic wounds. These dressings maintain a moist healing environment that supports tissue regeneration while minimizing maceration of surrounding skin, making them suitable for moderate-to-heavily exuding wounds. ALLEVYN® foam dressings from Smith & Nephew. These polyurethane-based foam dressings are designed to absorb and retain wound exudate while maintaining a moist healing environment, making them suitable for surgical wounds, pressure injuries, and chronic ulcers that require effective fluid management and protection from bacterial contamination.

Collagen dressings are the fastest-growing product category, due to their biocompatible and bioactive properties that support natural tissue repair. These dressings supply structural proteins that are fundamental to the body’s healing process, helping to stimulate new tissue formation, attract fibroblasts, and promote wound closure. They are especially valuable in challenging wounds with poor healing capacity, such as diabetic foot ulcers or surgical sites with high tissue stress. BIOSTEP Collagen Matrix from Smith & Nephew, Inc. This product is a collagen-based wound dressing designed to support tissue regeneration and enhance wound closure by targeting and deactivating excess matrix metalloproteinases (MMPs) in the wound bed, which are often elevated in chronic and surgical wounds.

Application Insights

Diabetic foot ulcers are expected to dominate the market, contributing nearly 35% of revenue in 2026, driven by the high clinical burden of diabetes-related wounds and their complex healing needs. These ulcers often involve poor blood flow, neuropathy, and an elevated risk of infection, which slows closure and increases recurrence. Advanced wound matrices help manage exudate, support granulation, and create a controlled healing environment, reducing complications. Diabetic foot ulcer management is the OASIS® Ultra Tri-Layer Matrix from Smith & Nephew, Inc. This bioengineered, acellular extracellular matrix device is cleared for healing partial- and full-thickness wounds, including diabetic foot ulcers, by providing a scaffold that supports cellular infiltration and tissue repair, thereby promoting more rapid wound closure compared with standard care alone.

Surgical & traumatic wounds represent the fastest-growing application, fueled by rising rates of surgical procedures and trauma-related injuries worldwide. These wounds often involve tissue loss, high exudate levels, and increased infection risk, making standard dressings insufficient for optimal healing. Advanced matrices provide structural support, enhance cellular migration, and help maintain a moist, controlled healing environment, thereby accelerating tissue regeneration. Surgical and traumatic wounds are treated with Integra® Wound Matrix from Integra LifeSciences Corp. This collagen-glycosaminoglycan matrix is FDA-cleared and indicated for managing a range of wound types, including surgical wounds (donor sites, post-surgical closures) and trauma wounds such as abrasions, lacerations, and second-degree burns, providing a scaffold that supports cellular invasion and capillary growth to aid healing.

Regional Insights

North America Surgical Wound Matrix Market Trends

North America is projected to dominate, accounting for nearly 42% of the share in 2026, driven by the region’s high chronic wound prevalence, advanced reimbursement policies, and high public awareness of advanced dressing benefits. Distribution systems in the U.S. and Canada provide extensive support for surgical wound matrix programs, ensuring wide accessibility across foam dressings, diabetic foot ulcers, and hospital populations. Increasing demand for bioactive, convenient, and easy-to-apply forms is further accelerating adoption, as these formats improve healing and reduce barriers associated with traditional gauze.

Innovation in surgical wound matrix technology, including stable antimicrobial foams, improved collagen delivery, and targeted home-care enhancement, is attracting significant investment from both public and private sectors. Government initiatives and CMS campaigns continue to promote use against infection risks, readmission concerns, and emerging chronic threats, creating sustained market demand. The growing focus on collagen grades and specialty uses, particularly for diabetic foot ulcers and others, is expanding the target applications for surgical wound matrix.

Europe Surgical Wound Matrix Market Trends

Europe is propelled by increasing awareness of the benefits of advanced wound care, strong regulatory systems, and government-led chronic disease programs. Countries such as Germany, the U.K., France, and Italy have well-established wound management frameworks that support routine surgical wound matrix use and encourage adoption of innovative foam and collagen delivery methods. These high-performance formulations are particularly appealing for diabetic foot ulcer populations, regulation-conscious hospitals, and home-care users, improving closure rates and coverage rates.

Technological advancements in surgical wound matrix development, such as enhanced silver-impregnated foams, application-targeted delivery, and improved hydrogel grades, are further boosting market potential. European authorities are increasingly supporting research and trials for matrices against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, cost-effective options is aligned with the region’s focus on preventive amputation reduction and outpatient care. Public awareness campaigns and promotional drives are expanding reach across both hospital and home healthcare segments, while suppliers are investing in bioactive materials and novel variants to enhance efficacy.

Asia Pacific Surgical Wound Matrix Market Trends

Asia Pacific is likely to be the fastest-growing market for surgical wound matrix in 2026, driven by rising awareness of diabetes and surgical volume, increasing government initiatives, and expanding application programs across the region. Countries such as India, China, Indonesia, and Thailand are actively promoting matrix campaigns to address chronic wound growth and emerging post-surgical needs. Surgical wound matrices are particularly attractive in these regions due to their scalable administration, ease of adoption, and suitability for large-scale diabetic foot ulcer and hospital drives in both urban and semi-urban populations.

Technological advancements are supporting the development of stable, effective, and easy-to-apply surgical wound matrices that can withstand challenging patient profiles and minimize dependence on infection. These innovations are critical for reaching domestic facilities and improving overall wound coverage. Growing demand for foam dressings, diabetic foot ulcers, and hospital applications is contributing to market expansion. Public-private partnerships, increased healthcare expenditure, and rising investment in matrix research and distribution capacity are further accelerating growth. The convenience of matrix delivery, combined with improved healing and reduced risk of complications, positions it as a preferred choice.

Competitive Landscape

The global surgical wound matrix market is shaped by active competition between established wound-care leaders and fast-moving bioactive specialists. In North America and Europe, Mölnlycke Health Care and 3M maintain leadership through sustained R&D investments, deep hospital relationships, and strong positions in chronic wound management. Their innovation pipelines in foam and collagen formats support broad clinical adoption across surgical, trauma, and complex wound settings. In Asia Pacific, regional manufacturers advance cost-competitive alternatives that improve access for public and private facilities, accelerating volume uptake.

Foam dressing delivery strengthens exudate control, improves patient comfort, and lowers infection risk, enabling standardized deployment across high-throughput care environments. Strategic partnerships, collaborations, and acquisitions consolidate expertise, widen product portfolios, and shorten time to commercialization in regulated markets. Collagen formulations address stalled healing by supporting granulation and tissue regeneration, driving deeper penetration in chronic and post-surgical wound segments while reinforcing clinician confidence and repeat use.

Key Industry Developments

- In August 2025, Imbed Biosciences Inc. launched SAM™ PainGuard™ with Lidocaine, a fully synthetic, antimicrobial, and biocompatible wound matrix for acute care. The company introduced two new product brands, Surgaflex™ PainGuard™ for surgical wounds and Pelashield™ PainGuard™ for burn and trauma wounds, enhancing its advanced wound care portfolio.

- In May 2025, Summit Products Group officially launched and partnered with NovaBone Products to offer new surgical and regenerative solutions. The collaboration advanced Summit's goal of transforming surgical and regenerative care with innovative biomaterials.

- In March 2024, Integra LifeSciences launched MicroMatrix® Flex in the U.S., featuring a dual-syringe system for precise mixing and delivery. The system improved access to difficult wound areas and enabled controlled application during wound management.

Companies Covered in Surgical Wound Matrix Market

- Mölnlycke Health Care Ab

- 3M

- Convatec Group Plc

- Baxter

- Coloplast Corp.

- Medtronic

- Derma Sciences Inc.

- Medline Industries Inc.

- Smith & Nephew Plc.

Frequently Asked Questions

The global surgical wound matrix market is projected to reach US$1.4 billion in 2026.

Higher volumes of surgeries, diabetes-related wounds, and trauma cases increase demand for matrices that support faster closure and tissue regeneration.

The surgical wound matrix market is poised to witness a CAGR of 8.0% from 2026 to 2033.

Products that control bioburden while promoting regeneration unlock new use cases in contaminated and high-risk surgical wounds.

Mölnlycke Health Care, 3M, Convatec Group Plc, Smith & Nephew Plc, and Coloplast Corp. are the key players.