Comprehensive Snapshot of Ship Spares and Equipment Market Including Regional and Country Analysis in Brief.

Industry: Automotive & Transportation

Published Date: April-2025

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 180

Report ID: PMRREP19408

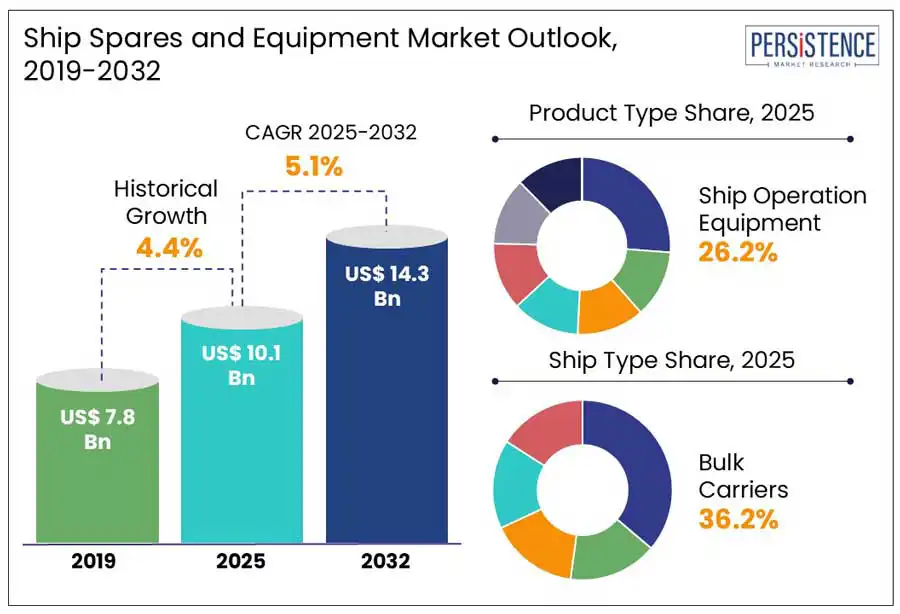

The global ship spares and equipment market size is projected to rise from US$ 10.1 Bn in 2025 to US$ 14.3 Bn by 2032. It is anticipated to witness a CAGR of 5.1% during the forecast period from 2025 to 2032.

Rising maritime trade worldwide is estimated to propel the global market through 2032. Commercial ships are witnessing high demand as international trade continues to surge and likely propel the requirement for ship spares and equipment to ensure these vessels remain efficient and operational. In addition, increasing procurement of naval ships due to high naval defense budgets in various countries is expected to be another market driver.

Key Industry Highlights

|

Global Market Attribute |

Key Insights |

|

Ship Spares and Equipment Market Size (2025E) |

US$ 10.1 Bn |

|

Market Value Forecast (2032F) |

US$ 14.3 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.1% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.4% |

A key driver of the global market is regulatory compliance, specifically regarding safety and environmental standards implemented by government bodies such as the International Maritime Organization (IMO). For instance, retrofitting activities increased after the implementation of IMO 2020 regulation, which limited the amount of sulfur in marine fuels to 0.5%.

Fleet owners hence installed modified engines and exhaust gas cleaning systems to comply with this norm. It accelerated demand for associated spare parts such as sensor units, nozzles, and scrubber pumps. The Ballast Water Management Convention has also created a rising demand for UV control units, filters, and lamps required for ballast treatment systems.

The issue of substandard and counterfeit spare parts is a significant concern in the market. These parts usually replicate the appearance of original components. However, these fail to meet the safety or technical standards required for maritime operations, especially in propulsion, navigation, and engines.

IMO, for instance, stated that majority of marine equipment failures worldwide occur due to the use of counterfeit parts. The easy availability of counterfeit spares and equipment not only surges the risks of accidents but also jeopardizes ship performance.

Defense and military modernization programs are estimated to open new doors to opportunities through 2032. Governments are emphasizing the expansion and upgradation of naval capabilities, especially in Eastern Europe, Middle East, and Indo-Pacific, due to rising geopolitical tensions. It is projected to create an increasing demand for mission-critical and high-performance ship parts and equipment to comply with endurance and reliability standards.

In Australia, the Naval Shipbuilding Enterprise is currently undergoing transformations under the AUD 100 Bn investment plans for developing a sovereign naval fleet. Similarly, the FY2024 defense budget in the U.S. allocated more than US$ 32.8 Bn to the Navy’s conversion and shipbuilding accounts. Such investments are poised to create lucrative growth opportunities in the future.

The emergence of 3D-printed and modular ship components is expected to be a key trend propelling the market forward. Increasing demand for enhanced operational flexibility, cost savings, and quick turnaround times in time-sensitive or remote maritime operations is predicted to bolster this trend.

Conventional ship spares often involve long lead times due to geographic constraints, customs delays, and complex supply chains. Hence, 3D-printed and modular parts are likely to emerge as ideal solutions to mitigate these issues.

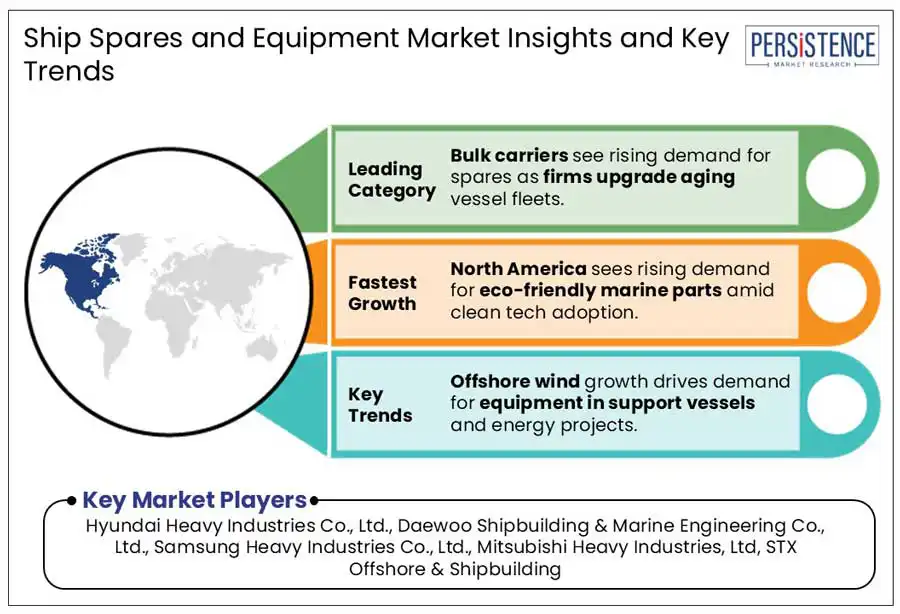

By ship type, the market is divided into containers, bulk carriers, transportation and general cargo, and cruise. Among these, bulk carriers are projected to dominate with around 36.2% ship spares and equipment market share in 2025, says Persistence Market Research. It is attributed to increasing use of these carriers in maritime trade for transporting essential raw materials such as fertilizers, grains, iron ore, and coal.

Components including engine machinery, ballast systems, and hatch covers of bulk carriers require frequent maintenance as these are designed with minimal onboard systems and large cargo holds. High demand for these vessels, especially from energy and construction sectors, is estimated to propel the requirement for efficient spare parts and equipment.

Cruises, on the other hand, are predicted to exhibit considerable growth in the foreseeable future. Cruise ships have become immensely popular due to the rapid growth of the cruise tourism industry worldwide. Cruise operators are investing in upgrading their fleets to meet rising environmental, health, and safety standards. It is poised to increase demand for a wide range of spare parts and equipment to ensure uninterrupted operations during long voyages.

Based on product type, the market is segregated into ship fittings and equipment, shipbuilding and shipyard industrial equipment and spare parts, main propulsion systems and equipment, auxiliary propulsion systems and equipment, ship operation equipment, rigging and lifting equipment, and electrical and electronic equipment. Out of these, ship operation equipment is expected to hold about 26.2% share in 2025.

Growth is attributed to increasing emphasis on environmental compliance and rising complexity of maritime operations. As ships become high-tech, demand for innovative equipment such as communication and navigation systems and onboard automation tools will likely skyrocket.

Rigging and lifting equipment is estimated to show decent growth through 2032 with ongoing expansion of offshore energy projects, especially oil and gas. Increasing number of floating wind farms in Asia Pacific and North Sea is also projected to bolster demand for specialized rigging gear.

In 2025, North America is predicted to account for a share of nearly 31.8%. It is attributed to aging commercial fleets and naval modernization in the region. The U.S. ship spares and equipment market is expected to generate the lion’s share in the region due to rising shipbuilding programs such as Arleigh Burke-class destroyers and Virginia-class submarines.

Need for frequent maintenance is also increasing in the U.S. commercial maritime sector owing to the presence of an aging fleet. More than 60% of active U.S. flag vessels have already crossed 20 years, found the U.S. Department of Transportation. This is anticipated to result in a high demand for spare parts such as auxiliary engines, hydraulic systems, gaskets, and valves.

In Asia Pacific, India’s naval modernization drive is predicted to propel the market forward. The Indian Navy was allocated a budget of around US$ 6.5 Bn for 2024 to 2025. A significant portion of this budget is dedicated to fleet modernization. It includes the retrofitting of existing platforms such as submarines, destroyers, and frigates as well as the commissioning of new vessels.

South Korea is also anticipated to showcase steady growth as it is home to several shipbuilding giants including Daewoo Shipbuilding & Marine Engineering and Hyundai Heavy Industries. These companies are focusing on developing green ship technology to enhance sustainability.

Norway in Europe is predicted to spearhead Germany. The country is considered a key hub of sustainable maritime technology. More than 80 electric and hybrid vessels are already under operation in the country’s waters as of 2024. Retrofitting activities are likely to skyrocket in Norway with the government’s ban on emissions in UNESCO World Heritage Fjords by 2026.

Germany is focusing on sophisticated naval procurement and ship automation. The country’s Navy is seeking custom-built spare parts such as advanced hydraulics, electronic warfare equipment, and acoustic signature control systems. It is due to ongoing expansion of its fleet with 212CD submarines and F126 frigates.

The global ship spares and equipment market for ship spares and equipment is intensely competitive with several companies striving to gain a high share. Established companies are focusing on collaborating with private or government-backed agencies to provide them with parts and equipment for their new vessels. A few companies are engaging in research and development activities to launch sustainable spares and equipment so that the maritime industry can comply with strict environmental norms.

|

Report Attributes |

Details |

|

Historical Data/Actuals |

2019 - 2024 |

|

Forecast Period |

2025 - 2032 |

|

Market Analysis Units |

Value: US$ Bn/Mn, Volume: As Applicable |

|

Geographical Coverage |

|

|

Segmental Coverage |

|

|

Competitive Analysis |

|

|

Report Highlights |

|

|

Customization and Pricing |

Available upon request |

By Ship Type

By Product Type

By End-user

By Region

To know more about delivery timeline for this report Contact Sales

The global market is projected to be valued at US$ 10.1 Bn in 2025.

Increasing government investment in retrofitting projects and stringent safety regulations are the key market drivers.

The market is poised to witness a CAGR of 5.1% from 2025 to 2032.

Launch of 3D-printed components and rising military modernization budgets are the key market opportunities.

Hyundai Heavy Industries Co., Ltd., Daewoo Shipbuilding & Marine Engineering Co., Ltd., and Samsung Heavy Industries Co., Ltd. are a few key players.