- Marine

- Ship Hull Inspection Services Market

Ship Hull Inspection Services Market Size, Share, and Growth Forecast 2026 - 2033

Ship Hull Inspection Services Market by Service Type (Contract-based, One Time Service), by Vessel Type (Oil and Chemical Tankers, Bulk Carriers, Container Ships, Gas Carriers, Offshore Support Vessels, Naval & Defense Vessels, Ferries & Passenger Ships), Technology (Diver-Based Inspection, ROV-Based Inspection, AUV-Based Inspection, Dry Dock Inspection, NDT-Based Inspection), End-user (Shipping Companies, Shipyards, Defense/Naval Authorities, Port Authorities, Others), by Regional Analysis, 2026 - 2033

Ship Hull Inspection Services Market Size and Trend Analysis

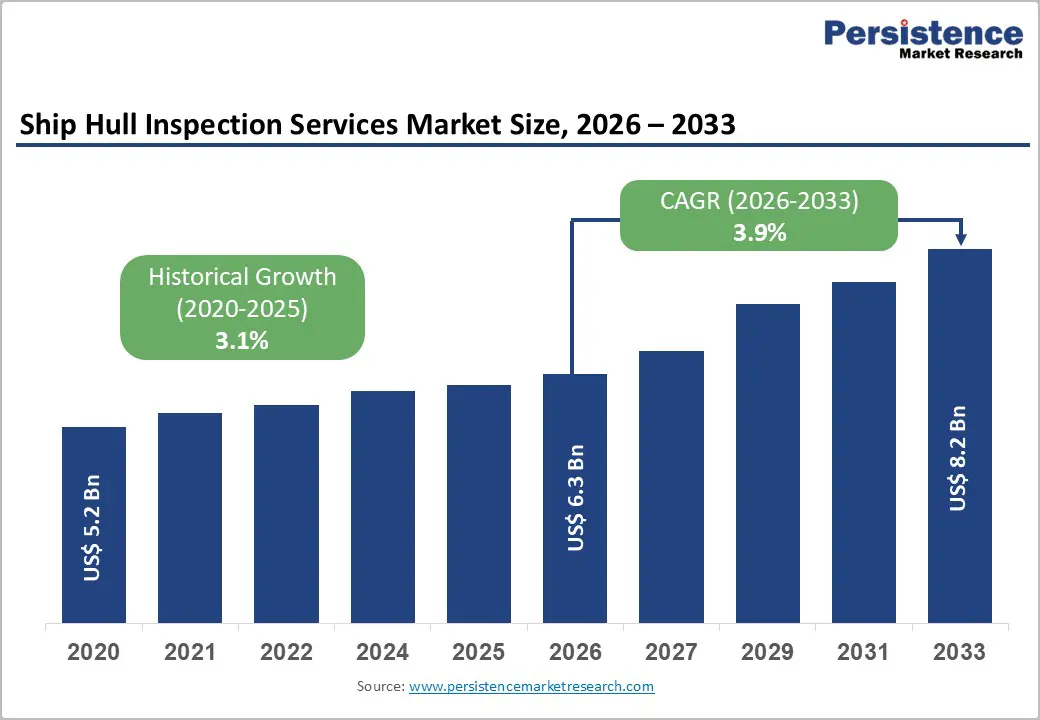

The global ship hull inspection services market size is expected to be valued at US$ 6.3 billion in 2026 and projected to reach US$ 8.2 billion by 2033, growing at a CAGR of 3.9% between 2026 and 2033.

Steady market growth is underpinned by tightening international maritime safety and environmental regulations, expansion of the global commercial fleet, and accelerating adoption of autonomous and remotely operated inspection technologies. The International Maritime Organization (IMO)'s Enhanced Survey Programme (ESP) and Port State Control (PSC) inspection regimes compel shipowners to maintain rigorous hull maintenance schedules, sustaining consistent service demand across all vessel classes globally.

Key Industry Highlights

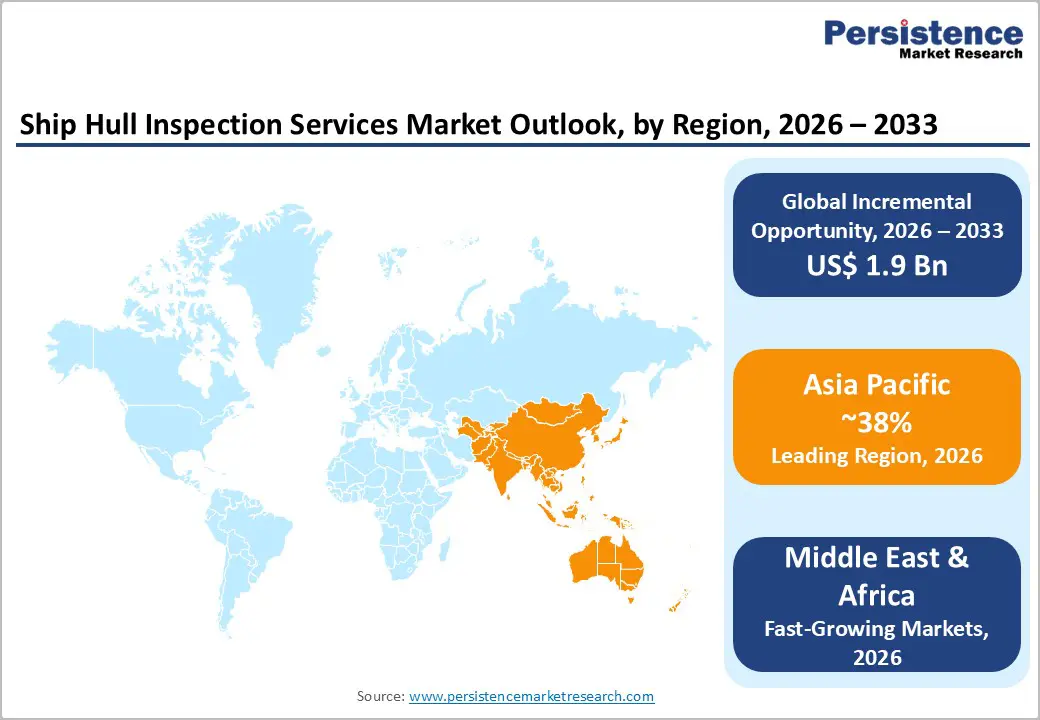

- Leading Region: Asia Pacific leads the global ship hull inspection services market with approximately 38% share in 2025, anchored by China's dominance in global shipbuilding order book tonnage and the region's large commercial and naval fleet operations.

- Fastest Growing Region: The Middle East & Africa region is the fastest-growing market, driven by expanding offshore energy infrastructure, growing naval fleet investments by GCC nations, and increasing maritime trade activity through key Red Sea and Gulf shipping corridors.

- Dominant Service Type: Contract-based services dominate with approximately 68% market share in 2025, as large shipping companies and classification societies prefer long-term inspection frameworks aligned with IMO Enhanced Survey Programme class renewal cycles for compliance assurance.

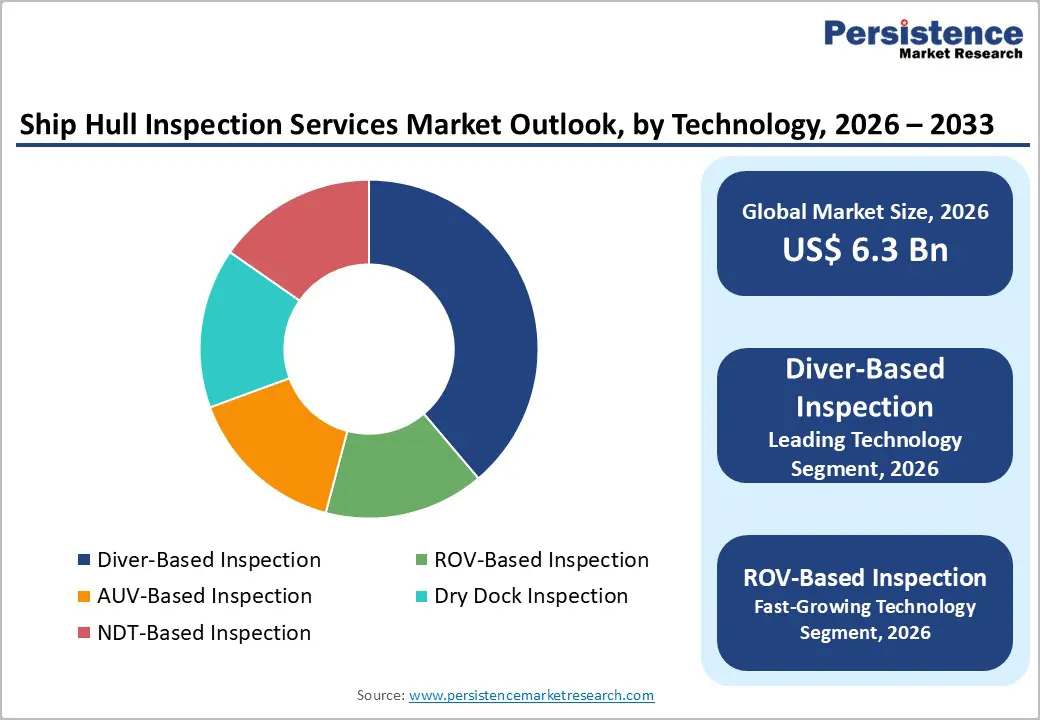

- Fastest Growing Technology: AUV and ROV-based autonomous inspection is the fastest-growing technology segment, reducing inspection time by up to 60% versus diver methods, eliminating safety risks, and gaining IMO recognition as an acceptable alternative to traditional dry-dock surveys.

- Key Opportunity: Defense and naval fleet modernization programs, supported by NATO's 2% GDP defense spending mandate and expanding Asia Pacific naval procurement, represent a high-value, premium-priced growth opportunity for specialized hull inspection service providers globally.

Market Dynamics

Drivers - Stringent International Maritime Safety Regulations and Compliance Mandates

Intensifying regulatory oversight by the International Maritime Organization (IMO) and flag state authorities is a primary driver of sustained demand for ship hull inspection services. The IMO's SOLAS (Safety of Life at Sea) convention and the Enhanced Survey Programme (ESP) require mandatory periodic hull and structural surveys for vessels above specified ages and tonnage thresholds. Port State Control (PSC) inspections, conducted under regional regimes such as the Paris MOU and Tokyo MOU, result in vessel detentions for hull condition deficiencies, creating powerful economic incentives for proactive inspection. In 2023, the Paris MOU detained over 1,400 vessels globally, reinforcing the commercial necessity of regular hull maintenance and inspection services for shipowners and operators.

Growth of Global Commercial Fleet and Offshore Energy Sector Expansion

The sustained expansion of the global commercial shipping fleet, driven by rising seaborne trade volumes and energy sector investments, is directly expanding the addressable market for hull inspection services. The United Nations Conference on Trade and Development (UNCTAD) reported that the world merchant fleet reached over 105,500 vessels of 100 GT and above by 2023, with fleet growth projected to continue. Concurrently, the expansion of offshore oil and gas infrastructure and the rapid development of offshore wind energy installations are generating new demand for hull and underwater structural inspection services for floating production units, jack-up rigs, and offshore support vessels, broadening the service provider's customer base beyond traditional commercial shipping.

Restraints - High Capital Investment and Operational Costs for Advanced Inspection Technologies

The deployment of advanced hull inspection technologies, including autonomous underwater vehicles (AUVs), remotely operated vehicles (ROVs), and phased array ultrasonic testing (PAUT) systems, requires substantial capital investment, specialized technical expertise, and ongoing maintenance. Procurement costs for survey-grade ROV systems range from US$ 50,000 to over US$ 500,000, placing advanced capabilities beyond the reach of smaller regional inspection companies. This cost barrier concentrates advanced inspection capacity among large, well-capitalized service providers, limits competition, and constrains adoption rates in cost-sensitive emerging market shipping segments, particularly among smaller fleet operators in Southeast Asia and Latin America.

Shortage of Certified Marine Inspection Personnel and Skilled Divers

Skills shortage in the maritime inspection sector is pertinent, particularly for certified commercial divers and NDT (non-destructive testing) specialists with IMO-recognized qualifications, constraining service delivery capacity globally. The International Marine Contractors Association (IMCA) has documented growing recruitment challenges for qualified saturation and air diving personnel. An aging workforce and limited training pipeline across developed maritime nations are exacerbating this constraint. As inspection volumes grow with fleet expansion, the qualified personnel gap risks creating service bottlenecks, extending inspection turnaround times, and increasing labor cost inflation for hull inspection service providers.

Opportunities - Rapid Adoption of ROV and AUV-Based Autonomous Inspection Platforms

The transition from diver-based to remotely operated and autonomous underwater vehicle (AUV) inspection represents the most technologically transformative opportunity in the ship hull inspection services market. AUV-based systems eliminate diver safety risks, reduce inspection time by up to 60% compared to conventional methods, and enable in-water surveys without dry-docking, generating significant cost savings for shipowners. The IMO has recognized in-water surveys as acceptable equivalents to dry-dock surveys under certain conditions, further validating technology adoption.

Companies such as Blueye Robotics and Inuktun Services are actively developing compact, AI-integrated inspection drones capable of real-time defect detection and 3D hull mapping, capabilities that are rapidly becoming the new industry standard for proactive fleet management.

Defense and Naval Fleet Modernization Programs Driving Inspection Demand

Escalating global defense budgets and naval fleet expansion programs are creating a significant and underserved demand pool for specialized ship hull inspection services. The NATO has mandated that member states increase defense spending to 2% of GDP, with naval procurement and maintenance forming a significant expenditure component. The U.S. Navy operates the world's largest naval fleet and has an annual ship maintenance, repair, and overhaul (MRO) budget exceeding US$ 8 billion, a substantial portion of which covers hull inspection and underwater survey activities.

Naval vessel hulls demand higher inspection frequency and more stringent NDT protocols than commercial vessels, commanding premium service pricing. Growing naval procurement across Asia Pacific nations, including India, South Korea, and Australia, is further expanding this high-value end-user segment.

Category-wise Insights

Service Type Analysis

Contract-based services dominate the Service Type category, accounting for approximately 68% of the ship hull inspection services market share in 2025. Long-term inspection and maintenance contracts are preferred by large shipping companies and fleet operators seeking predictable cost structures, guaranteed service availability, and compliance assurance across multiple vessels and international ports.

Classification societies including Lloyd's Register, Bureau Veritas, and DNV typically structure their survey obligations on multi-year frameworks aligned with IMO class renewal cycles. The economic efficiency of bundled inspection, reporting, and certification services under long-term contracts incentivizes fleet operators to consolidate vendor relationships, reinforcing the contract-based segment's market dominance.

Vessel Type Insights

Oil and Chemical Tankers lead the Vessel Type category, representing approximately 30% of total market share in 2025. Tankers are subject to the most stringent hull inspection requirements under the IMO's MARPOL convention and the Enhanced Survey Programme (ESP), due to the catastrophic environmental and safety consequences of hull failure.

The global tanker fleet numbers over 11,000 vessels according to UNCTAD data, and tankers require both internal and external hull inspections at defined intervals, generating high per-vessel inspection revenue. Additionally, the post-2020 IMO sulphur cap and alternative fuel transitions are prompting tanker retrofits that necessitate complementary structural surveys.

Technology Insights

Diver-Based Inspection currently leads the Technology category, representing approximately 40% of total market share in 2025. Despite the emergence of ROV and AUV technologies, diver-based inspection retains dominance due to its established acceptance by classification societies, flexibility in accessing complex hull geometries, and the extensive global network of certified commercial diving service providers.

The IMCA estimates that commercial diving operations, including underwater hull surveys, are conducted across all major ports globally, supported by a large pool of certified divers. However, ROV and AUV-based inspection is the fastest-growing sub-segment, gradually displacing diver-based methods in deepwater, high-risk, and efficiency-critical inspection scenarios.

End-user Insights

Shipping companies represent the dominant end-user segment, accounting for approximately 52% of total market share in 2025. Commercial fleet operators bear direct regulatory and commercial responsibility for hull condition, making them the primary purchasers of inspection services across all vessel classes and inspection technologies.

Leading global shipping conglomerates, including A.P. Moller-Maersk, MSC, and CMA CGM, manage large fleets requiring coordinated inspection programs across multiple international ports. The commercial pressure to minimize off-hire time and avoid PSC detentions drives shipping companies to invest proactively in regular hull surveys, underpinning this segment's market leadership.

Regional Insights

North America Ship Hull Inspection Services Market Trends and Insights

North America holds an estimated 26% share of the global ship hull inspection services market in 2025, driven by the presence of major naval installations, active Gulf of Mexico offshore energy infrastructure, and the regulatory framework of the U.S. Coast Guard (USCG) and American Bureau of Shipping (ABS). Demand for advanced ROV and AUV-based inspection technologies is high, supported by technology-focused shipowners and naval defense contractors operating in the region.

U.S. Ship Hull Inspection Services Market Size

The United States accounts for approximately 80% of the North American market. The U.S. Navy's multi-billion-dollar MRO budget, active Gulf of Mexico offshore vessel fleet, and USCG-mandated inspection regimes for commercial vessels entering U.S. ports sustain consistent and high-value demand for certified hull inspection services.

Europe Ship Hull Inspection Services Market Trends and Insights

Europe is a mature and highly regulated ship hull inspection market, anchored by the Paris MOU Port State Control regime and the classification mandates of Lloyd's Register, Bureau Veritas, and DNV. The region benefits from a high concentration of major shipyards, offshore energy infrastructure in the North Sea, and strong maritime heritage driving consistent inspection service demand.

Germany Ship Hull Inspection Services Market Size

Germany accounts for approximately 18% of the European market, supported by its significant shipbuilding and repair industry centered in Hamburg and Bremen, high offshore wind installation density in the North Sea, and the operational presence of DNV's European inspection networks.

U.K. Ship Hull Inspection Services Market Size

The United Kingdom represents approximately 15% of the European ship hull inspection market. The UK's extensive North Sea offshore infrastructure, major commercial ports including Felixstowe and Southampton, and the global headquarters of Lloyd's Register position it as a key hub for inspection service activity and technological innovation.

France Ship Hull Inspection Services Market Size

France accounts for approximately 11% of the European market. Major ports including Marseille and Le Havre, France's significant naval fleet operated by the Marine Nationale, and Bureau Veritas's global headquarters in Paris contribute to active demand for classification-aligned hull inspection and survey services.

Asia Pacific Ship Hull Inspection Services Market Trends and Insights

Asia Pacific is the largest regional market, holding approximately 38% of global share in 2025, driven by China's world-leading shipbuilding and ship repair capacity, large commercial fleet operations, and the region's dominance in global maritime trade. China alone hosts over 40% of global shipbuilding order book tonnage, sustaining intensive hull inspection activity across its major shipyards in Shanghai, Guangzhou, and Dalian.

India Ship Hull Inspection Services Market Size

India contributes approximately 8% of the Asia Pacific market, supported by its growing shipbuilding capacity at Cochin Shipyard and L&T Shipbuilding, expanding naval procurement under India's Maritime India Vision 2030, and increasing fleet registration under the Directorate General of Shipping.

Japan Ship Hull Inspection Services Market Size

Japan accounts for approximately 14% of the Asia Pacific market. Japan's advanced shipbuilding industry, operated by companies such as Japan Marine United Corporation and Imabari Shipbuilding, combined with a large domestic fleet and the presence of Nippon Kaiji Kyokai (ClassNK) headquarters, sustains high-value inspection service demand.

Southeast Asia Ship Hull Inspection Services Market Size

Southeast Asia contributes approximately 12% of the Asia Pacific market. Singapore's position as the world's busiest bunkering port and a major ship repair hub, home to Sembcorp Marine and Keppel Offshore & Marine, drives significant hull inspection activity, alongside growing offshore energy service vessel demand in Malaysia and Indonesia.

Competitive Landscape

The global ship hull inspection services market is highly fragmented, characterized by the presence of numerous regional service providers, marine survey firms, and specialized inspection companies operating alongside established classification societies and technology vendors. Competition is largely driven by accreditation credentials, breadth of inspection capabilities across diver, ROV, AUV, and non-destructive testing methods, and the ability to offer services across a wide network of ports and offshore locations.

From a strategic standpoint, providers are increasingly adopting technology-led differentiation through robotic inspection systems, AI-enabled defect detection, and digital reporting platforms to enhance efficiency and accuracy. Business models are evolving toward technology-as-a-service offerings, enabling scalable and repeatable inspection solutions. Additionally, companies are integrating inspection with maintenance and coating services to provide end-to-end hull lifecycle management. This bundled approach strengthens customer retention, increases switching costs, and supports long-term contractual relationships, positioning incumbents to capture recurring revenue in a regulation-driven market.

Key Developments:

- April 2026: Maritime and Port Authority of Singapore selected six companies including robotics and inspection specialists for co-funded in-water hull cleaning and inspection solutions, accelerating adoption of automated, sustainable hull maintenance technologies across port operations.

- January 2026: Black Sesame Technologies partnered with a COSCO Shipping unit to develop intelligent vessel inspection robots, leveraging embodied AI and prior robotics deployments to automate hazardous maritime tasks such as hull inspection and cleaning, improving efficiency and safety.

- October 2025: Inhaca Sub Diving Services launched its AI-powered Smart Hull Sight platform, enabling digital underwater hull inspections using 3D photogrammetry, corrosion detection, and digital twin visualization to enhance inspection accuracy and support predictive maintenance.

- March 2025: Blueye launched its next-generation underwater inspection drone featuring integrated AI defect recognition and real-time 3D hull mapping, targeting commercial shipping and offshore energy hull survey applications globally.

Ship Hull Inspection Services Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 5.2 Billion |

| Current Market Value (2026) | US$ 6.3 Billion |

| Projected Market Value (2033) | US$ 8.2 Billion |

| CAGR (2026 - 2033) | 3.9% |

| Leading Region | Asia Pacific, 38% market share (2025) |

| Dominant Service Type | Contract-based, 68% market share (2025) |

| Top-ranking Vessel Type | Oil and Chemical Tankers, 30% market share (2025) |

| Incremental Opportunity (2026 - 2033) | US$ 1.9 Billion |

Companies Covered in Ship Hull Inspection Services Market

- Royal Marine Management Pte Ltd

- Carisbrooke Shipping Limited

- IMF Technical Services Ltd

- Inuktun Services Ltd.

- Marine Inspection Services Ltd

- Nippon Kaiji Kentei Kyokai (NKKT)

- Norwegian Marine & Cargo Survey

- Overseas Merchandise Inspection Co., Ltd.

- SolidTech

- TechKnowServ

- TECHNOS MIHARA Co., Ltd.

- Ultramag

- AIM Control Group

- Blueye

- Commercial Diving Services Pty Ltd

- Bureau Veritas (Marine & Offshore)

- DNV (Det Norske Veritas)

- Lloyd's Register

Frequently Asked Questions

The ship hull inspection services market is estimated at US$ 6.3 billion in 2026.

Demand is driven by regulatory compliance, fleet expansion, and offshore infrastructure growth.

Asia Pacific leads, accounting for around 38% of the market share.

The key opportunity lies in AUV/ROV-based autonomous inspection with AI analytics.

Key players include Inuktun Services Ltd., Blueye, AIM Control Group, Marine Inspection Services Ltd, Nippon Kaiji Kentei Kyokai, and Ultramag, along with classification societies such as Bureau Veritas, DNV, and Lloyd's Register.