- Transportation & Logistics

- Chemical Tanker Shipping Market

Chemical Tanker Shipping Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Chemical Tanker Shipping Market by Shipping Route (Inland, Coastal, Deep-sea), Fleet Type (IMO 1, IMO 2, IMO 3), Fleet Material (Stainless Steel, Coated Steel), Application (Organic Chemicals, Inorganic Chemicals, Vegetable Oils & Fats, Liquefied Gases), and Region Analysis for 2026 to 2033

Chemical Tanker Shipping Market Trends & Analysis

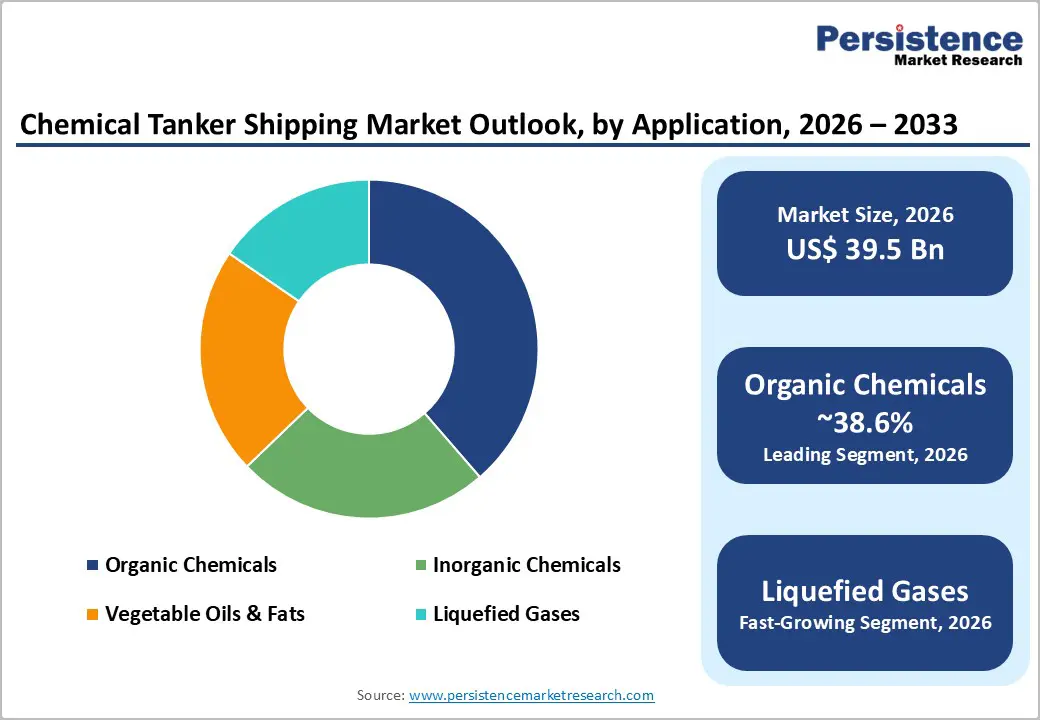

The global chemical tanker shipping market size is anticipated at US$ 39.5 billion in 2026 and is projected to reach US$ 53.8 billion by 2033, growing at a CAGR of 4.5% between 2026 and 2033. Global seaborne chemical trade exceeded 1.1 billion DWT-miles in 2024; Asia Pacific petrochemical capacity expanded 8.3% YoY; IMO CII and EEXI regulations drove 62% of fleet operators to initiate vessel compliance upgrades; and stainless steel tanker charter rates rose 15% above coated vessel equivalents on IMO 2-compliant configurations through 2024.

Rising global specialty chemical trade volumes, IMO-mandated fleet compliance upgrading, and Asia Pacific petrochemical industry capacity expansion are primary structural growth drivers. The historical 3.9% CAGR from 2020 to 2026 confirms steady trade volume-driven expansion, while tightening IMO 1 and IMO 2 fleet standards and fleet modernization investment sustain forward momentum.

Key Industry Highlights:

- Leading Fleet Type: IMO 2 leads at 51.5% share; IMO 1 grows fastest at 5.2% CAGR, driven by specialty chemical and pharmaceutical cargo purity requirements and IMO safety upgrade enforcement at port state control inspections globally.

- Leading Application: Organic Chemicals leads at 38.6% share; Liquefied Gases grow fastest at 4.8% CAGR, driven by green ammonia carrier demand and IEA's US$ 150 Bn green hydrogen production investment projection through 2030.

- Leading Fleet Material: Stainless Steel leads and grows fastest at 58.9% share; and 4.6% CAGR, with Odfjell's US$ 500-900 Mn supersegregator newbuild program sustaining stainless steel segment dual leadership.

- Regional Leader: Asia Pacific leads at 38.5% share (China US$ 7.2 Bn, India US$ 2.5 Bn) at 4.9% CAGR in the forecast timeline.

- Strategic Milestone: MOL's US$ 400 Mn Fairfield acquisition (March 2024) creating Asia Pacific's largest 117-vessel fleet and Odfjell's US$ 500-900 Mn stainless steel supersegregator program (2024) signal fleet consolidation and green-aligned vessel procurement as defining competitive themes through 2033.

Market Dynamics Analysis

Drivers - IMO Environmental Compliance Mandates, CII, EEXI, and Sulfur Cap, Accelerating Chemical Tanker Fleet Modernization and Replacement Procurement

The IMO Carbon Intensity Indicator (CII) and Energy Efficiency Existing Ship Index (EEXI) regulations, effective from January 2023 and enforceable across all chemical tankers above 5,000 GT, require fleet operators to reduce carbon intensity annually or face restricted trading permissions and port state control detentions, directly compelling operators to replace aging epoxy-coated vessel fleets with modern stainless steel, dual-fuel IMO 1 and IMO 2 compliant tankers.

BIMCO confirmed that over 22% of the global chemical tanker fleet operating in 2024 was built before 2005, comprising approximately 1,200 vessels approaching mandatory phase-out under CII rating degradation schedules, generating a structured newbuild and fleet replacement procurement pipeline concentrated at Stolt-Nielsen, Odfjell, and MOL Chemical Tankers' capital allocation programs through 2033.

The IMO 2020 sulfur emission cap, mandating maximum 0.5% sulfur fuel oil content globally and 0.1% in Emission Control Areas (ECAs), has driven scrubber retrofitting and LNG dual-fuel conversion investment across European and North American trading chemical tanker fleets, with scrubber-fitted IMO 2 vessels commanding US$ 3,000-5,000 per day higher charter rates versus non-compliant equivalents at spot market pricing as of Q1 2025. Vessels built post-2015 command up to 15% higher charter rates due to environmental compliance and operational efficiency advantages, creating a clear incentive structure for fleet renewal investment across the global chemical tanker operator community through 2033.

Asia Pacific Petrochemical Industry Expansion and Specialty Chemical Trade Volume Growth Driving Deep-Sea Chemical Tanker Demand

Asia Pacific's petrochemical production capacity expanded 8.3% YoY in 2024, with China's annual chemical production exceeding US$ 1.65 Tn in 2024 (China Petroleum and Chemical Industry Federation, CPCIF), generating the world's largest seaborne chemical export volumes requiring deep-sea IMO 2 and IMO 3 chemical tanker transportation services across intra-Asia, Asia-to-Europe, and Asia-to-Americas trade routes.

India's petrochemical capacity was valued at US$ 300 Bn by 2025 under the National Chemical Policy framework, supported by ONGC Petro additions' Dahej complex and Reliance Industries' Jamnagar integrated complex expansions, generating structured incremental chemical tanker demand across Indian Ocean and Persian Gulf trade corridors.

Global specialty chemical market growth, valued at US$ 700 Bn in 2024 at 5.1% CAGR (ICCA, Global Chemical Industry Report), is expanding demand for high-specification IMO 1 stainless steel tankers capable of transporting pharmaceutical-grade solvents, electronic chemicals, and high-purity specialty chemical cargoes requiring contamination-free, nitrogen-blanketed stainless steel tank environments unavailable in coated steel or IMO 3 general chemical carrier configurations. The specialty chemical trade expansion is generating a US$ 8-12 Bn addressable fleet investment opportunity for IMO 1 stainless steel newbuilds through 2033, concentrated at Japanese, Korean, and European chemical shipping operators specializing in pharmaceutical and electronic chemical value chains globally.

Restraints - Geopolitical Trade Route Disruptions Constraining Chemical Tanker Voyage Efficiency and Scheduling Reliability

The Red Sea crisis, with Houthi maritime attacks diverting over 85% of Asia-Europe chemical tanker traffic away from the Suez Canal to the Cape of Good Hope route from January 2024 onwards, extended average Asia-to-Europe voyage distances by 3,800 nautical miles, increasing per-voyage transit times by 12-15 days and reducing effective fleet capacity utilization from scheduled 88% to actual 74% at peak diversion intensity across IMO 2 and IMO 3 chemical tanker fleets. Russian petrochemical export restrictions and U.S.-China trade tariff escalation, affecting US$ 14 Bn in bilateral chemical trade flows in 2024, create structural route uncertainty that complicates multi-year time charter contract pricing for fleet operators.

Port Infrastructure Deficiency and Chemical Cargo Handling Capacity Constraints Limiting Inland and Coastal Segment Expansion

Inland waterway chemical terminal infrastructure across Southeast Asia, South Asia, and Sub-Saharan Africa lacks the dedicated chemical unloading berths, vapor recovery systems, and chemical storage tank farms required for safe handling of IMO 1 and IMO 2 cargo categories, with UNCTAD's 2024 Review of Maritime Transport estimating that fewer than 28% of developing-nation port facilities can accommodate the specialized chemical tanker cargo handling standards required for hazardous chemical categories.

Port congestion at Rotterdam, Singapore, and Shanghai, the three largest global chemical tanker ports, creates average waiting times of 4.8 days per vessel arrival during peak chemical trade seasons, reducing effective annual chemical tanker cargo cycle efficiency and constraining market volume growth rates.

Opportunities - Liquefied Gas and Ammonia Carrier Conversion Opportunity as Green Hydrogen Economy Shipping Infrastructure Expands

The global green hydrogen economy, with the IEA projecting US$ 150 Bn in green ammonia production investment by 2030, is creating demand for specialized dual-purpose chemical/liquefied gas tankers capable of transporting anhydrous ammonia, methanol, and liquid organic hydrogen carriers (LOHC) as zero-carbon fuel feedstocks across emerging green energy trade routes between Middle East producers and European and East Asian consuming markets.

Kawasaki Heavy Industries' liquid hydrogen carrier program, MAN Energy Solutions' ammonia-compatible IMO 1 tank design certification, and Yara's ammonia shipping expansion program, each representing US$ 200-450 Mn in vessel investment per program, exemplify the emerging liquefied gas and green energy carrier hybrid market opportunity at the intersection of chemical tanker and gas carrier market segments through 2033.

The green ammonia shipping opportunity alone, with the Hydrogen Council projecting 100 million metric tons of green hydrogen traded annually by 2050 primarily through ammonia carriers, represents a US$ 3.5-5.0 Bn addressable new chemical tanker vessel investment opportunity by 2033 for operators establishing early positioning in green ammonia and methanol carrier fleet configurations compatible with the global energy transition trade route evolution.

Middle East Integrated Petrochemical Complex Expansion Generating New Chemical Tanker Trade Route and Fleet Demand

Saudi Aramco's US$ 110 Bn integrated downstream and petrochemical expansion program, including the Jizan Economic City complex, Jazan refinery, and SABIC Jubail complex expansions, is generating new deep-sea IMO 2 and IMO 3 chemical tanker demand on Middle East-to-Asia and Middle East-to-Europe trade routes, with SABIC projecting 12 million metric tons of additional annual chemical export volume by 2028 requiring dedicated chemical tanker fleet capacity.

UAE's Ruwais Industrial City expansion and Abu Dhabi National Chemicals Company (ChemCorp) greenfield investment, targeting US$ 45 Bn in UAE petrochemical output by 2031, are creating a new Gulf chemical tanker trade route triangle linking Middle East supply with Asian downstream processing and European specialty chemical distribution. Combined, Saudi Arabia, UAE, Kuwait, and Qatar Middle East petrochemical expansion programs are estimated to generate US$ 3.6 billion in incremental annual chemical tanker freight revenue by 2030, representing one of the highest-concentration geographic growth opportunities for deep-sea IMO 2 chemical tanker fleet investment and long-term time charter contract procurement through 2033.

Category-wise Analysis

Shipping Route Insights

Deep-sea leads the product type segment with a 54.7% market share in 2026, estimated at approximately US$ 21.61 Bn, anchored by the dominant Asia-to-Europe, Middle East-to-Asia, and Americas-to-Asia international chemical trade corridors requiring long-haul IMO 2 and IMO 3 tankers operating on voyages of 5,000-14,000 nautical miles that generate the highest freight revenue per voyage per vessel compared to coastal or inland route configurations.

Deep-sea market leadership reflects the fundamental structure of global chemical trade, with petrochemical production centers concentrated in the Middle East, Asia, and North America while consumption centers span Europe, Southeast Asia, and South America, making intercontinental chemical tanker voyages the dominant revenue-generating product type. Coastal and inland segments are growing, but deep-sea's absolute freight volume and per-voyage revenue scale sustain product type segment leadership.

Expanding China Yangtze River chemical trade, European Rhine-Scheldt-Meuse inland waterway chemical cargo network growth, and India's National Waterways Authority chemical freight expansion investment collectively drive inland chemical tanker adoption acceleration at regional distribution and last-mile chemical logistics program levels globally through 2033.

Fleet Type Insights

IMO 2 leads the fleet type segment with a 51.5% market share in 2026, estimated at approximately US$ 20.34 Bn, comprising 5,838 active vessels operating the optimal balance between versatility and economics, capable of transporting moderately hazardous chemicals including alcohols, aromatics, and agrochemicals at 20-30% lower unit transportation costs than IMO 1 specialist vessels through multi-cargo flexibility and port-routing efficiency advantages. IMO 2's fleet type leadership reflects the commercial sweet spot at the moderate-hazard chemical cargo tier, where the broadest range of industrial chemical trade flows intersect with optimal vessel size efficiency at the 5,000-80,000 DWT range. No structural dominance shift is anticipated through 2033, as IMO 2 vessels' multi-cargo flexibility and CII compliance retrofit compatibility sustain procurement preference.

IMO 1 is the fastest-growing fleet type at 5.2% CAGR through 2033. Rising demand for highly hazardous specialty chemical transport, including concentrated acids, organochlorine compounds, and high-purity pharmaceutical solvents, combined with stricter IMO safety upgrade enforcement at port state control inspections, is driving IMO 1 newbuild procurement and fleet expansion at specialty chemical shipping operators globally through 2033.

Fleet Material Analysis

Stainless Steel leads the fleet material segment with a 58.9% market share in 2026, estimated at approximately US$ 23.27 Bn, driven by its superior cargo versatility, contamination resistance, non-porous surface hygiene performance, and multi-cargo cycling capability across pharmaceutical, specialty chemical, and food-grade vegetable oil cargoes without tank coating reconditioning downtime between cargo changes. Stainless steel's dominance reflects IMO 1 and premium IMO 2 fleet specifications where cargo purity requirements and multi-chemical cycling flexibility deliver higher charter rate premiums than coated steel alternatives. Stainless steel tankers' US$ 3,000-5,000 per day charter rate premium versus coated alternatives sustains operator investment preference for stainless steel newbuild procurement at high-specification fleet expansion programs through 2033.

Stainless Steel is also the fastest-growing fleet material at 4.6% CAGR through 2033. Growing specialty chemical, pharmaceutical, and electronic chemical trade requiring contamination-free stainless tank environments, IMO fleet modernization phasing out aging epoxy-coated vessels, and Odfjell's US$ 500-900 Mn stainless steel supersegregator newbuild program collectively sustain stainless steel's simultaneous leadership and growth position through 2033.

Application Analysis

Organic Chemicals lead the application segment with a 38.6% market share in 2026, estimated at approximately US$ 15.25 Bn, reflecting the dominant position of organic chemical trade flows, including methanol, ethanol, benzene, xylene, styrene, and organic acids, within global seaborne chemical cargo volumes, where Asia Pacific petrochemical production expansion generates the largest export volumes at commodity-scale freight rates supporting high-volume IMO 2 and IMO 3 tanker utilization. Organic chemicals' application leadership is sustained by the sheer volume scale of commodity organic chemical trade, with global methanol sea trade alone exceeding 40 million metric tons annually (Methanol Institute, 2024), maintaining application segment revenue dominance against specialty chemical, vegetable oil, and gas cargo categories. No dominance reversal is anticipated through 2033.

Liquefied Gases are the fastest-growing application at 4.8% CAGR through 2033. Green ammonia as hydrogen carrier, LPG trade expansion across South Asian import markets, and dual-purpose chemical/gas carrier configurations gaining regulatory approval, driven by IEA's US$ 150 Bn green hydrogen investment projection, collectively sustain liquefied gases application segment's accelerating growth trajectory within the chemical tanker market through 2033 globally.

Regional Market Insights

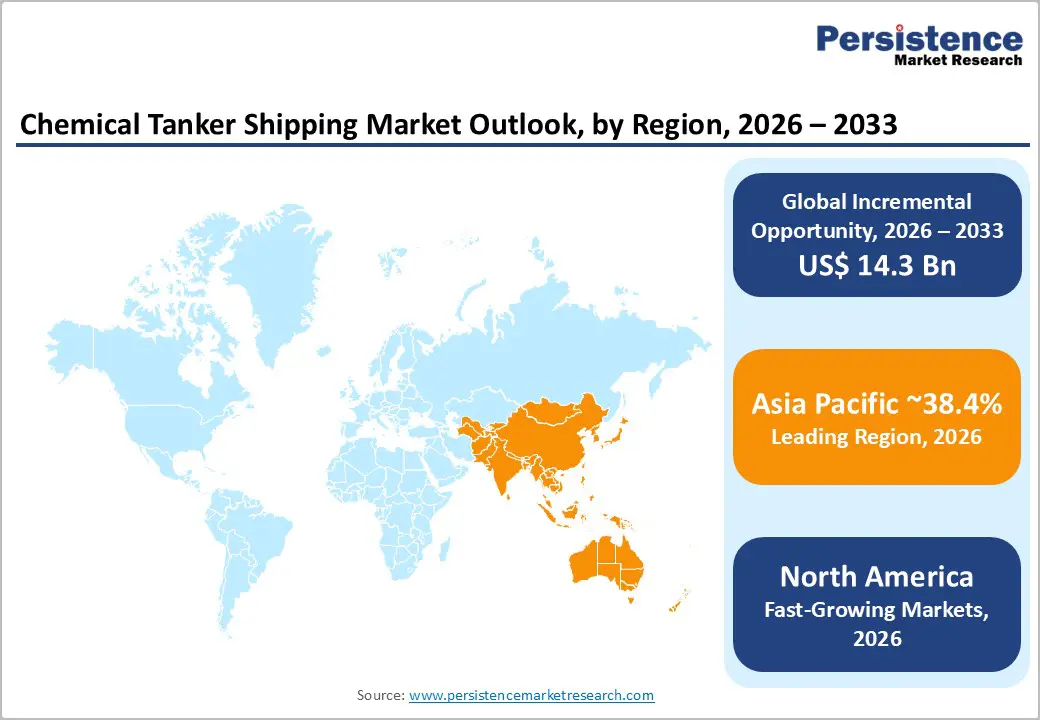

Asia Pacific leads the region at approximately 38.5% share in 2025, while Asia Pacific also grows fastest at 4.9% CAGR.

North America

North America is growing at a prominent 4.1% CAGR through 2033, holding approximately 19.4% of global Chemical Tanker Shipping Market share in 2026, estimated at approximately US$ 7.66 Bn, anchored by U.S. Gulf Coast petrochemical export capacity, Jones Act chemical tanker fleet serving U.S. coastal routes, and expanding U.S.-to-Asia and U.S.-to-Europe deep-sea chemical tanker freight volumes generated by U.S. LNG-advantaged chemical production cost competitiveness improvements from 2020 onwards.

U.S. Chemical Tanker Shipping Market: Gulf Coast Petrochemical Export Leadership and Jones Act Coastal Tanker Demand

The United States holds approximately US$ 7.0 Bn in 2026, driven by U.S. Gulf Coast ethylene, methanol, and specialty chemical export fleet demand, EPA Chemical Facility Anti-Terrorism Standards compliance-driven vessel security investment, and USGC/CBP chemical import documentation digitalization. Jones Act-compliant chemical tankers, with over 50 qualified vessels serving U.S. coastal chemical trade, represent a structural domestic procurement segment. Canada contributes through Trans-Mountain expansion-linked petrochemical feedstock export growth from British Columbia Pacific gateway terminals to Asian chemical markets.

North America's growth is sustained by U.S. Gulf Coast petrochemical export expansion, EPA maritime emissions compliance investment, and Jones Act fleet modernization as aging U.S.-flag coastal chemical tankers require CII-compliant replacement procurement through 2033.

Europe

Europe holds a 25.7% share of the global Chemical Tanker Shipping Market in 2026, estimated at approximately US$ 10.15 Bn, driven by European Union's chemical trade leadership (EU Chemical Industry generating €670 Bn in annual output, Cefic 2024), Rotterdam's position as the world's largest chemical tanker port by throughput, and IMO CII and EU ETS compliance regulatory pressure driving fleet modernization investment at European-headquartered Stolt-Nielsen, Odfjell, and Navig8 operations.

Germany Chemical Tanker Shipping Market: Chemical Export Leadership and IMO Fleet Compliance Investment

Germany holds approximately US$ 2.8 Bn in 2026, anchored by BASF, Bayer, and Evonik chemical export volumes through Rotterdam and Hamburg ports requiring dedicated IMO 2 chemical tanker freight capacity. The U.K. sustains INEOS chemical tanker operations and Thames Estuary coastal chemical fleet. France contributes through TotalEnergies petrochemical export volumes and Dunkerque LNG-chemical terminal integration. Spain expands through Repsol's Tarragona complex and Mediterranean coastal chemical distribution fleet growth. EU Fit for 55 maritime framework drives European fleet decarbonization investment.

Europe's EU Cefic chemical industry export volume leadership, IMO compliance-driven fleet renewal at Rotterdam and Hamburg hubs, and Stolt-Nielsen/Odfjell European operator capital investment programs sustain structured chemical tanker market procurement through 2033.

Asia Pacific

Asia Pacific is the leading and fastest-growing region at 4.9% CAGR through 2033, commanding approximately 38.5% of global Chemical Tanker Shipping Market share in 2025, driven by China's world-largest petrochemical production base, India's National Chemical Policy-linked capacity expansion, South Korean and Japanese shipbuilding IMO 2 newbuild delivery dominance, and ASEAN inter-regional chemical trade route development expanding intra-regional chemical tanker freight volumes.

China Chemical Tanker Shipping Market: Petrochemical Scale, Newbuild Capacity, and Green Chemical Trade

China holds US$ 7.2 Bn in 2026, driven by CPCIF-confirmed US$ 1.65 Tn annual chemical production, COSCO Shipping Chemical Tankers fleet expansion, and CCS classification society newbuild IMO compliance integration. India at US$ 2.5 Bn expands through ONGC/Reliance chemical export growth and Sagarmala chemical port infrastructure investment. Japan sustains MOL Chemical Tankers' 117-vessel post-Fairfield acquisition fleet as the largest Asia Pacific chemical tanker operator. South Korea drives Hyundai HI and Samsung HI IMO 2 newbuild delivery pipeline.

Asia Pacific's China petrochemical export volume leadership, MOL Chemical Tankers' Asia Pacific fleet dominance, and South Korean shipyard IMO 2 stainless steel newbuild delivery capacity sustain the region's combined market leadership and growth momentum through 2033.

Competitive Landscape

The global Chemical Tanker Shipping Market is moderately consolidated at the top tier, with Stolt-Nielsen, Odfjell, MOL Chemical Tankers, Navig8, and Marida Tankers collectively commanding approximately 30-40% of global chemical tanker DWT capacity, while hundreds of regional and single-segment operators compete across coastal, inland, and specialized commodity chemical freight niches globally. Fleet age advantage, stainless steel tank versatility, CII compliance certification, and multi-port operational network breadth are the primary competitive moats.

IMO 1 stainless steel fleet expansion through newbuild and acquisition programs, green ammonia dual-purpose carrier positioning, digital fleet management platform integration, and Asia Pacific trade route capacity expansion define the dominant competitive strategic investment themes across global chemical tanker market participants by 2033.

Strategic Developments

- In March 2024, MOL Chemical Tankers completed its acquisition of Fairfield Chemical Carriers, adding 27 IMO 2 stainless steel vessels and expanding MOL's fleet to 117 vessels for a total investment of approximately US$ 400 Mn, establishing MOL as Asia Pacific's largest chemical tanker operator by DWT capacity.

- In October 2024, Christiania Shipping acquired France-based Navquim, adding 13 stainless steel chemical tankers to its fleet, strengthening European IMO 1 and IMO 2 stainless steel chemical tanker operations and expanding Christiania's geographic reach into French and Mediterranean coastal chemical trade routes.

- In March 2025, Hyundai Heavy Industries launched a new series of eco-friendly stainless steel chemical tankers integrating lightweight alloys and IoT monitoring systems, targeting 15% emissions reduction per voyage and aligning with IMO CII compliance requirements, with vessels targeting European and Asian operators requiring next-generation stainless steel fleet configurations.

Companies Covered in Chemical Tanker Shipping Market

- Stolt-Nielsen Limited

- Odfjell SE

- MOL Chemical Tankers Pte. Ltd.

- Navig8 Chemical Tankers Inc.

- Marida Tankers Management

- Nordic Tankers A/S

- Team Tankers International Ltd.

- Bahri (National Shipping Company of Saudi Arabia)

- MISC Berhad (AET Chemical Tankers)

- Iino Kaiun Kaisha Ltd.

- Maersk Tankers A/S

- Chemikalien Seetransport GmbH (CST)

- Odfjell Tankers (China)

- Hyundai Heavy Industries (Shipbuilding)

- Kawasaki Kisen Kaisha ("K" Line)

Frequently Asked Questions

The chemical tanker shipping market is likely to be valued at US$ 39.5 Bn in 2026, projected to reach US$ 53.8 Bn by 2033, delivering an incremental opportunity of US$ 14.5 Bn through 2033.

IMO CII and EEXI compliance mandating fleet modernization with post-2015 vessels commanding 15% charter rate premiums, Asia Pacific petrochemical capacity expanding 8.3% YoY, and global specialty chemical trade at US$ 700 Bn growing at 5.1% CAGR are the primary growth drivers.

The chemical tanker shipping markeymarket grows at a CAGR of 4.5% from 2026 to 2033, building on a historical CAGR of 3.9% from 2020 to 2026.

Green ammonia and hydrogen carrier fleet development (US$ 3.5-5.0 Bn opportunity by 2033) and Middle East petrochemical expansion generating US$ 2.8-3.6 Bn in incremental annual chemical tanker freight revenue by 2030 represent the highest-value actionable growth opportunities.

Stolt-Nielsen, Odfjell, MOL Chemical Tankers, Navig8, Marida Tankers, Nordic Tankers, Team Tankers, Bahri, MISC (AET), Iino Kaiun, Maersk Tankers, CST, Hyundai HI, and K Line are the leading global Chemical Tanker Shipping market participants.