- Home Care & Utilities

- Pet Furniture Market

Pet Furniture Market Size, Share, and Growth Forecast 2026 - 2033

Pet Furniture Market by Product Type (Pet Sofas & Beds, Pet Houses, Pet Trees, Others), Pet Type (Dogs, Cats, Others), Price Segment (Economy, Mid-Range, Premium), Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Online), and Regional Analysis, 2026 - 2033

Pet Furniture Market Size and Trend Analysis

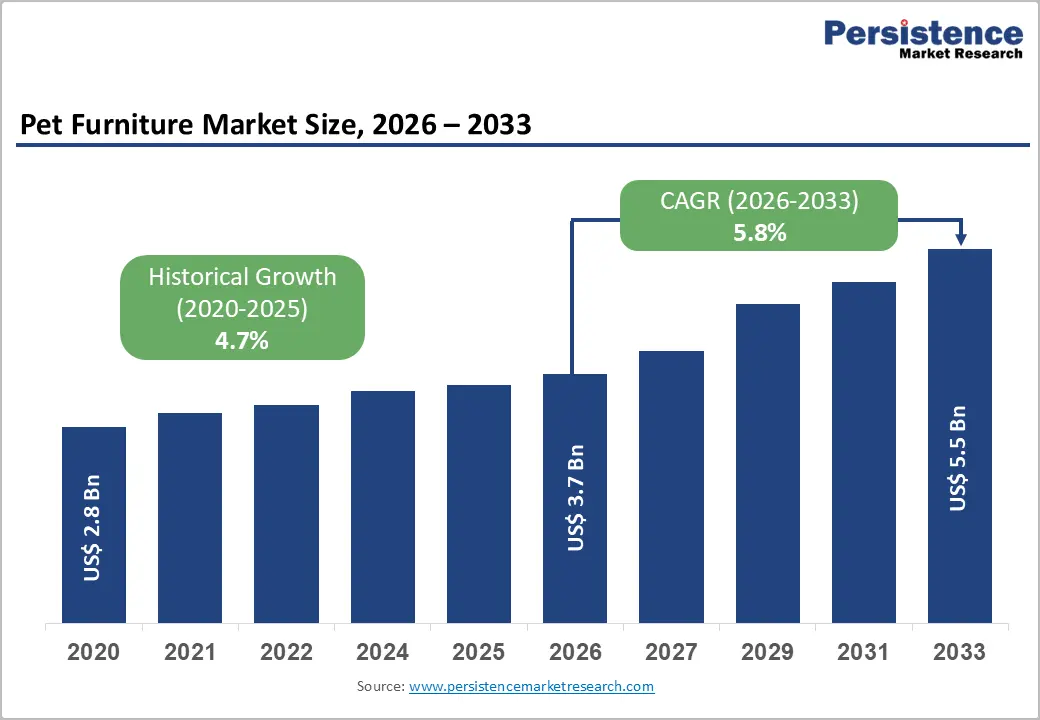

The global pet furniture market size is expected to be valued at US$ 3.7 billion in 2026 and projected to reach US$ 5.5 billion by 2033, growing at a CAGR of 5.8% between 2026 and 2033. This consistent acceleration is driven by the intensifying global pet humanization trend, where pet owners increasingly treat companion animals as family members and invest in high-quality, aesthetically coordinated furniture, combined with surging pet ownership rates globally and the rapid expansion of online pet specialty retail.

The market grew from US$ 2.8 billion in 2020 at a historical CAGR of 4.7%, supported by the COVID-19 pandemic's dramatic acceleration of pet adoptions, growing millennial and Gen Z pet owner demographics prioritizing premium pet lifestyle products, and expanding product innovation in design-forward, sustainable pet furniture that blurs the line between pet accessories and home interior design.

Key Industry Highlights

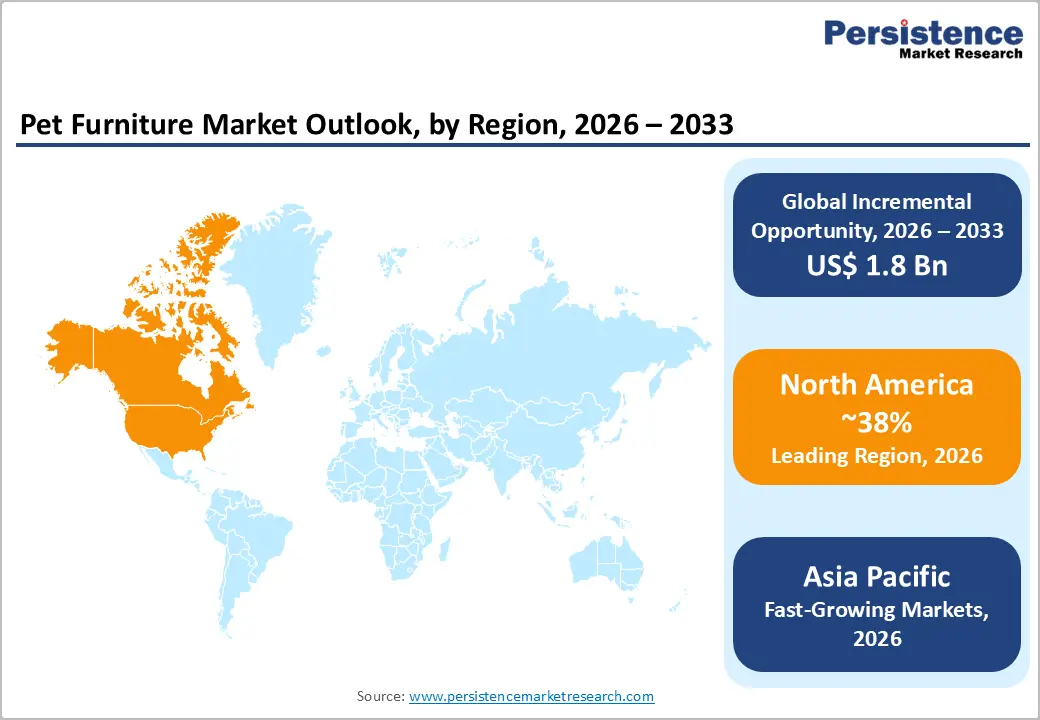

- Leading Region: North America commands 38% global pet furniture market share in 2025, driven by US$ 147 billion total pet industry spending per APPA, 69 million U.S. dog-owning households, and a mature premium pet lifestyle culture among millennial and Gen Z consumers.

- Fastest Growing Region: Asia Pacific is the fastest growing region at 7.5% CAGR through 2033, driven by China's 120 million registered pets, India's expanding urban middle-class pet ownership, and e-commerce platforms including JD.com, Flipkart, and Shopee enabling rapid market penetration.

- Dominant Product Type: Pet Sofas & Beds hold 52% market share in 2025, driven by universal ownership necessity, highest-frequency replacement cycles, and growing orthopedic memory foam bed premiumization targeting the expanding senior dog care market across North America and Europe.

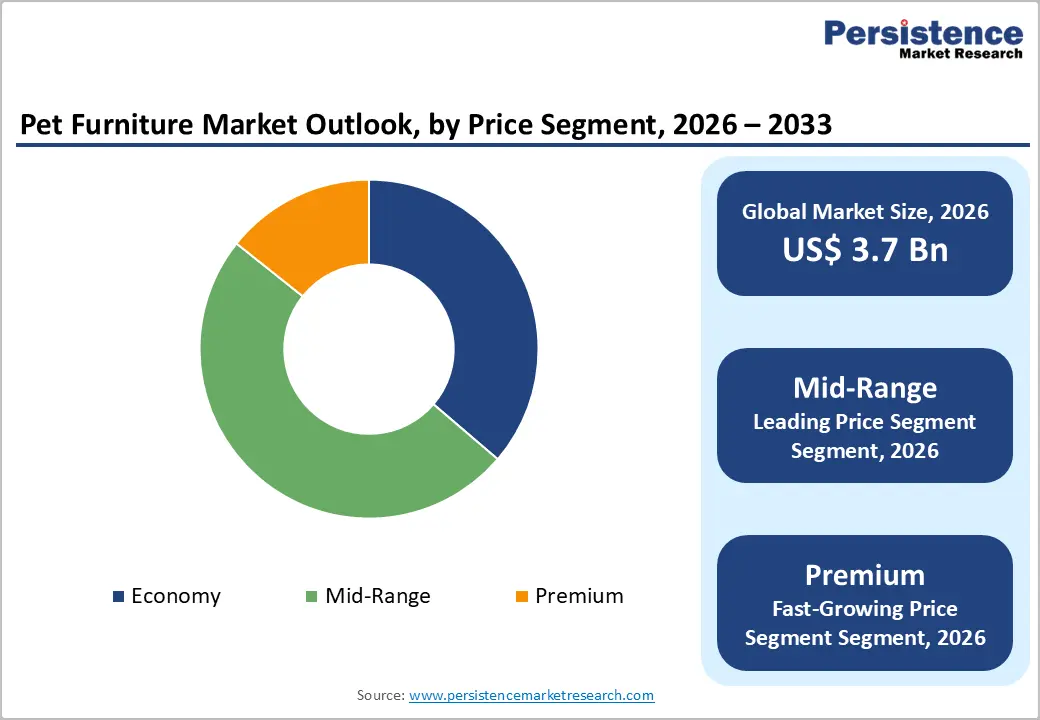

- Fastest Growing Price Segment: The Premium pet furniture segment is the fastest growing price tier, with design-led brands including MiaCara and Fable Pets demonstrating strong DTC growth among affluent millennials and Gen Z pet owners prioritizing sustainable materials and Scandinavian-inspired home-coordinated aesthetics.

- Key Opportunity: Design-forward, sustainable premium pet furniture sold through social commerce and direct-to-consumer channels represents the highest-margin growth opportunity, with FSC-certified wood, recycled PET fill, and certified organic fabric products commanding US$ 200-800+ price points among growing eco-conscious pet owner demographics.

Market Dynamics

Drivers - Pet Humanization Trend and Rising Pet Ownership Rates Globally

The humanization of pets, treating companion animals as family members and investing accordingly in their comfort, health, and quality of life, drives pet furniture market demand worldwide. The American Pet Products Association (APPA) reports that total U.S. pet industry expenditure reached over US$ 147 billion in 2023, with pet owners increasingly allocating spending toward lifestyle-oriented products, including premium beds, sofas, and houses.

Globally, pet ownership rates have risen substantially: the European Pet Food Industry Federation (FEDIAF) estimates that approximately 90 million European households own at least one pet. The pandemic-driven surge in pet adoptions, with the ASPCA reporting that approximately 23 million U.S. households acquired a new pet during COVID-19, created a large new cohort of first-time owners who have since advanced to higher-spend engagement with premium pet lifestyle categories, including designer pet furniture.

E-commerce Expansion and Social Media-Driven Premium Product Discovery

The rapid growth of e-commerce and social media platforms is fundamentally reshaping pet furniture distribution and consumer discovery, enabling small and mid-sized premium brands to reach global audiences without traditional retail infrastructure. Platforms including Instagram, Pinterest, and TikTok have become primary channels for pet furniture discovery, with aesthetically designed products earning significant organic reach among pet owner communities.

APPA 2026 reports that online pet product sales have grown at significantly above-average rates within the broader pet category, with specialty online retailers including Chewy.com and Amazon providing frictionless access to an increasingly diverse range of pet furniture brands. Direct-to-consumer brands like Fable Pets and MiaCara GmbH & Co. KG have demonstrated that premium, design-led pet furniture can achieve rapid growth through social commerce and content-driven marketing strategies independent of traditional physical retail channels.

Market Restraints

Price Sensitivity and Discretionary Spending Exposure in Economic Downturns

Pet furniture is a discretionary consumer product, and despite the humanization trend, purchasing decisions remain subject to macroeconomic conditions and household income pressures. During inflationary periods, such as the 2021-2023 cost-of-living crisis affecting North America and Europe, consumers demonstrably traded down from premium to economy pet furniture or deferred purchases altogether.

The APPA's periodic consumer surveys document spending prioritization toward pet food, veterinary care, and medicines well above discretionary lifestyle categories, including furniture and accessories, indicating that pet furniture growth is more economically sensitive than the broader pet care sector.

Product Safety Concerns and Lack of Standardized Testing Requirements

Unlike human furniture, pet furniture products, particularly cat trees, pet houses, and elevated beds, are not subject to uniform mandatory safety standards in most markets, creating consumer uncertainty about material safety, structural durability, and chemical content compliance. Reports of product failures, toxic fabric treatments, and formaldehyde off-gassing from lower-cost imported pet furniture items have periodically generated negative media coverage and consumer concern. The absence of standardized ASTM or ISO safety certification frameworks for pet furniture creates both consumer confidence challenges and potential liability risk for retailers, which can restrict premium placement and slow category growth in health-conscious consumer segments.

Opportunities - Premium and Design-Forward Pet Furniture: Fastest Growing Price Segment

The premium pet furniture segment is the fastest growing price tier globally, driven by a growing demographic of affluent, design-conscious pet owners who view pet furniture as an extension of their home interior aesthetic rather than a purely functional accessory. Brands including MiaCara GmbH & Co. KG (Germany) and Fable Pets (USA) have demonstrated strong commercial success with minimalist, Scandinavian-inspired pet furniture collections priced at US$ 200-US$ 800+ per piece.

APPA reports that premium pet product categories are growing at above-average rates within the overall pet market, with millennial and Gen Z pet owners, who collectively represent the fastest-growing buyer cohort, over-indexing on premium and sustainable product purchases. Sustainable materials, including certified organic fabrics, recycled PET fill, and FSC-certified wood, are commanding specification premiums from environmentally conscious buyers.

Asia Pacific Pet Furniture Market: Fastest Growing Region with Emerging Middle-Class Pet Ownership

Asia Pacific is the fastest growing regional market for pet furniture, driven by rapidly expanding pet ownership among emerging middle-class households in China, India, South Korea, and Southeast Asian urban centers. The China Pet Industry White Paper (Goumin.com) reports that China's pet population exceeded 120 million registered pets, with urban pet ownership growing at double-digit annual rates. South Korea's pet-owning households number over 3 million per Korea Animal Welfare Association data, reflecting the rapid cultural adoption of pet companionship.

The region's rapidly expanding online retail infrastructure, with platforms including JD.com, Tmall, and Flipkart, is providing pet furniture brands with accessible, high-reach distribution channels in markets where specialist pet retail chains remain underdeveloped, creating a significant first-mover advantage for brands establishing early regional presence.

Category-wise Analysis

Product Type Insights

Pet sofas & beds are dominant and likely to account for approximately 52% share in 2026. This leadership position reflects the universal requirement for comfortable, dedicated sleeping and resting spaces for companion animals across all demographics, geographies, and price points. Pet beds and sofas are the highest-volume, highest-repurchase-frequency pet furniture category, they wear out, get soiled, and are replaced more frequently than pet houses or cat trees, generating recurring demand.

Product innovation in orthopedic memory foam beds for older dogs, addressing the growing pet longevity care market, and self-heating thermal beds for cats are driving premiumization within the segment, expanding both unit values and total category revenue across North America and Europe.

Pet Type Insights

Dogs represent the leading Pet Type segment, accounting for approximately 58% share in 2025. Dogs are the world's most widely owned companion animal. The American Veterinary Medical Association (AVMA) reports approximately 69 million U.S. households owning dogs, compared to 45 million owning cats, and dogs require a broader and higher-value furniture assortment including beds, crates, sofas, and outdoor furniture than cats.

Larger dog breeds require higher-priced, structurally robust furniture items, elevating average transaction values in dog-focused pet furniture. The premium orthopedic and therapeutic pet bed segment is predominantly dog-oriented, given dogs' higher incidence of joint conditions in aging populations. Brands including Furhaven Pet Products and Midwest Homes for Pets derive the majority of their pet furniture revenue from dog-category products, reinforcing segment dominance.

Price Segment Insights

The mid-range price segment is the dominant pice tier, accounting for approximately 50% market share in 2025. Mid-range pet furniture, typically priced between US$ 30 and US$ 150, occupies the broadest commercial sweet spot, balancing acceptable quality and durability with price accessibility for the majority of pet-owning households across North America, Europe, and urban Asia Pacific. The segment serves the core mass-market consumer base that increasingly demands above-economy quality, durable fabrics, adequate fill, decent aesthetics, without the premium price commitment.

Major retailers including Petco, PetSmart, and Chewy.com, generate the majority of their pet furniture revenue from mid-range SKUs. While premium is the fastest growing tier by CAGR, mid-range's broad consumer base ensures its revenue dominance through the forecast period, particularly in price-sensitive emerging markets where middle-class pet ownership is expanding rapidly.

Distribution Channel Insights

Online channels represent the leading distribution channel for pet furniture, accounting for approximately 46% share in 2026 and continuing to gain share from physical retail. Pet furniture's characteristics, bulky shipping dimensions, broad product variety, and high consumer research intensity, make it ideally suited to the online purchasing journey. Platforms including Chewy.com, Amazon, and brand direct-to-consumer websites enable detailed product exploration, customer review consultation, and convenient home delivery that physical stores cannot match for large-format items.

Online-native brands including Fable Pets and Go Pet Club have built significant market positions exclusively through digital channels, demonstrating the viability of online-first pet furniture business models.

Regional Insights

North America leads the global pet furniture market with approximately 38% market share in 2025, while Asia Pacific is the fastest growing region, projected to record the highest CAGR of approximately 7.5% through 2026 - 2033.

North America Pet Furniture Market Trends and Insights

North America is the world's largest and most mature pet furniture market, sustained by deeply embedded pet humanization culture, the world's highest per-capita pet spending per APPA data, and a well-developed specialty pet retail and e-commerce ecosystem. Premium and sustainable pet furniture segments are growing fastest, driven by affluent millennial and Gen Z pet owners who prioritize design aesthetics and material safety in purchasing decisions.

U.S. Pet Furniture Market Size

The United States accounts for approximately 84% of North American pet furniture market revenue in 2025, reflecting the country's US$ 147 billion, with approximately 69 million dog-owning and 45 million cat-owning households providing an enormous addressable base. Premium and orthopedic pet bed adoption is growing fastest, with major e-commerce channels including Chewy.com sustaining consistent double-digit pet furniture sales growth.

Europe Pet Furniture Market Trends and Insights

Europe is the second-largest pet furniture market globally, driven by approximately 90 million pet-owning households per FEDIAF data and growing premium pet lifestyle culture across Western European markets. Design-forward, sustainable pet furniture, particularly Scandinavian-inspired minimalist collections, is the fastest growing product tier, with European brand MiaCara GmbH & Co. KG pioneering the high-design luxury pet furniture segment that commands premiums of US$ 300-800+ per piece.

Germany Pet Furniture Market Size

Germany holds approximately 22% of European pet furniture market revenue in 2025. With over 34 million pets per Industrieverband Heimtierbedarf (IVH) data and a strong culture of premium pet care investment, Germany is home to leading European pet furniture brand MiaCara GmbH & Co. KG. German consumers are particularly receptive to design-led, sustainable pet furniture made from FSC-certified wood and certified organic fabrics, driving premium segment growth above European averages.

U.K. Pet Furniture Market Size

The United Kingdom represents approximately 17% of European pet furniture market revenue in 2025. The Pet Food Manufacturers' Association (PFMA) reports over 13 million cats and 12 million dogs in UK households, providing a substantial addressable market. The UK's strong online retail culture, with Amazon UK and specialty pet e-tailers capturing growing pet furniture share, and increasing consumer interest in design-forward pet accessories drive consistent market expansion.

France Pet Furniture Market Size

France accounts for approximately 12% of the European pet furniture market revenue in 2025. France has approximately 14 million cats and 8 million dogs per FACCO (French pet industry association) data, with a growing premium lifestyle pet culture among urban French consumers. French pet owners increasingly specify aesthetically coordinated pet furniture that complements interior design, driving demand for premium and mid-range cat furniture and dog beds.

Asia Pacific Pet Furniture Market Trends and Insights

Asia Pacific is the fastest growing pet furniture region, with China's rapidly maturing urban pet ownership culture, and over 120 million registered pets per Goumin.com data, driving the largest incremental demand. South Korea and Japan also maintain highly developed pet care cultures with strong premium product adoption. The region's rapidly expanding e-commerce infrastructure provides pet furniture brands accessible, low-barrier distribution at scale, supporting rapid market penetration by both local and international brands.

India Pet Furniture Market Size

India represents approximately 8% of Asia Pacific pet furniture market revenue in 2025 and is growing rapidly. India's pet ownership is expanding rapidly among urban middle-class households, with the Indian Pet Industry Federation documenting consistent double-digit growth in domestic pet care spending. E-commerce platforms including Amazon India and Flipkart are the primary pet furniture distribution channels, with affordable mid-range products driving volume growth as the category matures.

Japan Pet Furniture Market Size

Japan contributes approximately 16% of Asia Pacific pet furniture market revenue in 2025. Japan has one of Asia's most developed pet care cultures, with cats being the most popular companion animal and commanding high per-unit furniture spend. The Japan Pet Food Association reports consistent growth in premium pet lifestyle product adoption. Japanese consumers' preference for compact, space-efficient pet furniture designs, suited to smaller urban living spaces, drives demand for innovative, multi-functional cat trees and pet houses.

Southeast Asia Pet Furniture Market Size

Southeast Asia collectively represents approximately 12% of Asia Pacific pet furniture market revenue in 2025. Urban pet ownership is expanding rapidly across Thailand, Indonesia, Malaysia, and Vietnam, driven by growing middle-class affluence and cultural acceptance of indoor companion animals. The ASEAN pet industry is at an early growth stage, with e-commerce platforms including Lazada and Shopee providing primary pet furniture distribution channels and enabling rapid market development at minimal infrastructure cost.

Competitive Landscape

The global pet furniture market is highly fragmented, characterized by the presence of numerous small and mid-sized brands alongside a limited number of established players, with no dominant company holding significant global share. The market’s diversity in product offerings, pricing tiers, and regional preferences creates low entry barriers and intensifies competition, particularly in online retail channels and design-focused segments.

From a strategic standpoint, companies are focusing on product differentiation through aesthetic design, comfort features, and the use of sustainable and high-quality materials to align with evolving consumer preferences. Strong digital presence and direct-to-consumer models are becoming critical, with brands leveraging social media and e-commerce platforms for visibility and engagement. Emerging business models such as subscription-based furniture solutions and collaborations with interior design brands are gaining traction. Additionally, premiumization trends driven by pet humanization are encouraging innovation in multifunctional and space-efficient furniture, enabling companies to capture higher-margin segments.

Key Developments

- April 2026: HEAPETS launched a global pet cleaning ecosystem designed to combat airborne pet hair using integrated air purification and vacuum solutions, aiming to improve home air quality and deliver comprehensive cleaning for modern pet households.

- November 2025: ROOOF launched a debut collection of modern, design-focused dog beds featuring handcrafted materials, sculptural forms, and customizable finishes, targeting design-conscious pet owners seeking luxury pet furniture that integrates seamlessly with contemporary home interiors.

- April 2024: SVAG Pet introduced “Barkitecture” design solutions including villas, pods, and furniture for dogs under its Barkkey brand, focusing on premium pet living spaces that integrate functionality with modern architectural aesthetics.

- March 2024: IKEA launched its first pet furniture range, UTSÅDD, designed for cats and dogs with products focused on eating, sleeping, playing, and hiding, aiming to combine functionality, comfort, and home-friendly aesthetics.

Pet Furniture Market - Key Insights

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 2.8 Billion |

| Current Market Value (2026) | US$ 3.7 Billion |

| Projected Market Value (2033) | US$ 5.5 Billion |

| CAGR (2026 - 2033) | 5.8% |

| Leading Region | North America, 38% market share (2025) |

| Dominant Product Type | Pet Sofas & Beds, 52% market share (2025) |

| Top-Ranking Pet Type | Dogs, 58% market share (2025) |

| Incremental Opportunity (2026 - 2033) | US$ 1.8 Billion |

Companies Covered in Pet Furniture Market

- Go Pet Club

- Inter IKEA Systems B.V.

- Ware Pet Products

- Petpals Group

- Aosom LLC

- Fable Pets

- Midwest Homes for Pets

- North American Pet Products

- MiaCara GmbH & Co. KG

- Furhaven Pet Products

- Critter Crouch Company

- K&H Pet Products

- Pet Zone Products Ltd.

- Trixie Heimtierbedarf GmbH & Co. KG

Frequently Asked Questions

The global pet furniture market is projected at US$ 3.7 billion in 2026, supported by rising pet ownership and premium pet care spending.

Key drivers include growing pet humanization, high pet ownership rates, and rapid expansion of online retail channels.

North America leads with about 38% share, driven by strong pet ownership and high spending on premium pet products.

Major opportunities lie in premium sustainable furniture and fast-growing demand in Asia Pacific urban markets.

Key players include Go Pet Club, Inter IKEA Systems B.V., MiaCara GmbH & Co. KG, Furhaven Pet Products, Fable Pets, Midwest Homes for Pets, Petpals Group, Aosom LLC, Ware Pet Products, Critter Crouch Company, and Trixie Heimtierbedarf GmbH & Co. KG.