- Executive Summary

- Global Pet Oral Care Market Snapshot, 2025 and 2033

- Market Opportunity Assessment, 2025 – 2033, US$ Bn

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Key Trends

- Macro-economic Factors

- Global Sectoral Outlook

- Global GDP Growth Outlook

- COVID-19 Impact Analysis

- Forecast Factors – Relevance and Impact

- Value Added Insights

- Tool Adoption Analysis

- Regulatory Landscape

- Value Chain Analysis

- PESTLE Analysis

- Porter’s Five Force Analysis

- Price Analysis, 2025A

- Key Highlights

- Key Factors Impacting Deployment Costs

- Pricing Analysis, By Product Type

- Global Pet Oral Care Market Outlook

- Key Highlights

- Market Volume (Units) Projections

- Market Size (US$ Bn) and Y-o-Y Growth

- Absolute $ Opportunity

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast

- Historical Market Size (US$ Bn) Analysis, 2025-2025

- Market Size (US$ Bn) Analysis and Forecast, 2025 – 2033

- Global Pet Oral Care Market Outlook: Product Type

- Introduction / Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis, By Product Type, 2025 – 2025

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2025 – 2033

- Toothbrushes

- Toothpaste

- Chews & Treats

- Oral Rinses

- Dental Sprays

- Dental Wipes

- Others

- Market Attractiveness Analysis: Product Type

- Global Pet Oral Care Market Outlook: Pet Type

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Pet Type, 2025 – 2025

- Market Size (US$ Bn) Analysis and Forecast, By Pet Type, 2025 – 2033

- Dogs

- Cats

- Others

- Market Attractiveness Analysis: Pet Type

- Global Pet Oral Care Market Outlook: Distribution Channel

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Distribution Channel, 2025 – 2025

- Market Size (US$ Bn) Analysis and Forecast, By Distribution Channel, 2025 – 2033

- Veterinary Clinics

- Pet Specialty Stores

- Supermarkets

- Pharmacies

- Online

- Market Attractiveness Analysis: Distribution Channel

- Key Highlights

- Global Pet Oral Care Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Units) Analysis, By Region, 2025 – 2025

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Region, 2025 – 2033

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Pet Oral Care Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2025 – 2025

- By Country

- By Product Type

- By Pet Type

- By Distribution Channel

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 – 2033

- U.S.

- Canada

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2025 – 2033

- Toothbrushes

- Toothpaste

- Chews & Treats

- Oral Rinses

- Dental Sprays

- Dental Wipes

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Pet Type, 2025 – 2033

- Dogs

- Cats

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Distribution Channel, 2025-2033

- Veterinary Clinics

- Pet Specialty Stores

- Supermarkets

- Pharmacies

- Online

- Market Attractiveness Analysis

- Europe Pet Oral Care Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2025 – 2025

- By Country

- By Product Type

- By Pet Type

- Distribution Channel

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 – 2033

- Germany

- France

- U.K.

- Italy

- Spain

- Russia

- Türkiye

- Rest of Europe

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2025 – 2033

- Toothbrushes

- Toothpaste

- Chews & Treats

- Oral Rinses

- Dental Sprays

- Dental Wipes

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Pet Type, 2025 – 2033

- Dogs

- Cats

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Distribution Channel, 2025-2033

- Veterinary Clinics

- Pet Specialty Stores

- Supermarkets

- Pharmacies

- Online

- Market Attractiveness Analysis

- East Asia Pet Oral Care Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2025 – 2025

- By Country

- By Product Type

- By Pet Type

- By Distribution Channel

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 – 2033

- China

- Japan

- South Korea

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2025 – 2033

- Toothbrushes

- Toothpaste

- Chews & Treats

- Oral Rinses

- Dental Sprays

- Dental Wipes

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Pet Type, 2025 – 2033

- Dogs

- Cats

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Distribution Channel, 2025-2033

- Veterinary Clinics

- Pet Specialty Stores

- Supermarkets

- Pharmacies

- Online

- Market Attractiveness Analysis

- South Asia & Oceania Pet Oral Care Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2025 – 2025

- By Country

- By Product Type

- By Pet Type

- By Distribution Channel

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 – 2033

- India

- Southeast Asia

- ANZ

- Rest of South Asia & Oceania

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2025 – 2033

- Toothbrushes

- Toothpaste

- Chews & Treats

- Oral Rinses

- Dental Sprays

- Dental Wipes

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Pet Type, 2025 – 2033

- Dogs

- Cats

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Distribution Channel, 2025-2033

- Veterinary Clinics

- Pet Specialty Stores

- Supermarkets

- Pharmacies

- Online

- Market Attractiveness Analysis

- Latin America Pet Oral Care Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2025 – 2025

- By Country

- By Product Type

- By Pet Type

- By Distribution Channel

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 – 2033

- Brazil

- Mexico

- Rest of Latin America

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2025 – 2033

- Toothbrushes

- Toothpaste

- Chews & Treats

- Oral Rinses

- Dental Sprays

- Dental Wipes

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Pet Type, 2025 – 2033

- Dogs

- Cats

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Distribution Channel, 2025-2033

- Veterinary Clinics

- Pet Specialty Stores

- Supermarkets

- Pharmacies

- Online

- Market Attractiveness Analysis

- Middle East & Africa Pet Oral Care Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2025 – 2025

- By Country

- By Product Type

- By Pet Type

- By Distribution Channel

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 – 2033

- GCC Countries

- Egypt

- South Africa

- Northern Africa

- Rest of Middle East & Africa

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product Type, 2025 – 2033

- Toothbrushes

- Toothpaste

- Chews & Treats

- Oral Rinses

- Dental Sprays

- Dental Wipes

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Pet Type, 2025 – 2033

- Dogs

- Cats

- Others

- Market Size (US$ Bn) Analysis and Forecast, By Distribution Channel, 2025-2033

- Veterinary Clinics

- Pet Specialty Stores

- Supermarkets

- Pharmacies

- Online

- Market Attractiveness Analysis

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping By Market

- Competition Dashboard

- Company Profiles (Details – Overview, Financials, Strategy, Recent Developments)

- Mars Petcare

- Overview

- Segments and Deployments

- Key Financials

- Market Developments

- Market Strategy

- Nestlé Purina PetCare

- Colgate-Palmolive

- Virbac

- Vetoquinol

- Dechra Pharmaceuticals

- PetzLife

- TropiClean

- ImRex Inc.

- Ceva Santé Animale

- Hill’s Pet Nutrition

- Beaphar

- Mars Petcare

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Animal Health

- Pet Oral Care Market

Pet Oral Care Market Size, Share, and Growth Forecast 2026-2033

Pet Oral Care Market by Product Type (Toothbrushes, Toothpaste, Chews & Treats, Oral Rinses, Dental Sprays, Dental Wipes, Others), Pet Type (Dogs, Cats, Others), Distribution Channel (Veterinary Clinics, Pet Specialty Stores, Supermarkets, Pharmacies, Online), and Regional Analysis for 2026-2033

Key Industry Highlights

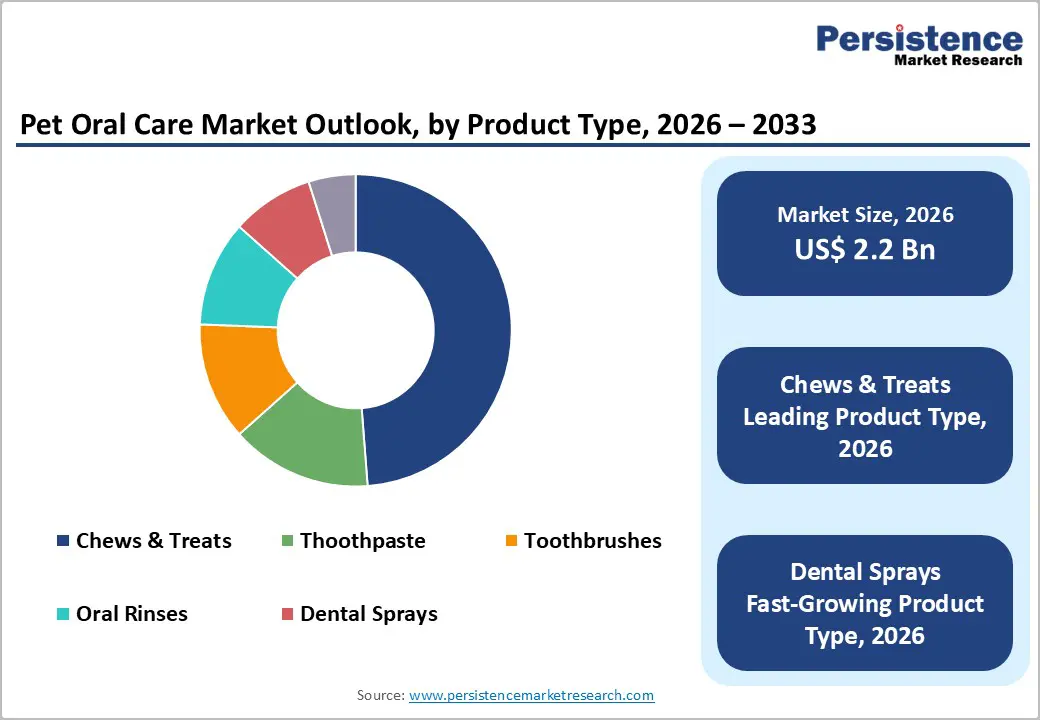

- Dominant Product Type: Chews & treats are set to command approximately 40% revenue share in 2026, while dental sprays are likely to grow the fastest through 2033, driven by increasing preference for non-brushing solutions.

- Leading Pet Type: Dogs are projected to account for over 60% revenue share in 2026, whereas cats are expected to register the fastest growth over 2026-2033, supported by species-specific product innovation.

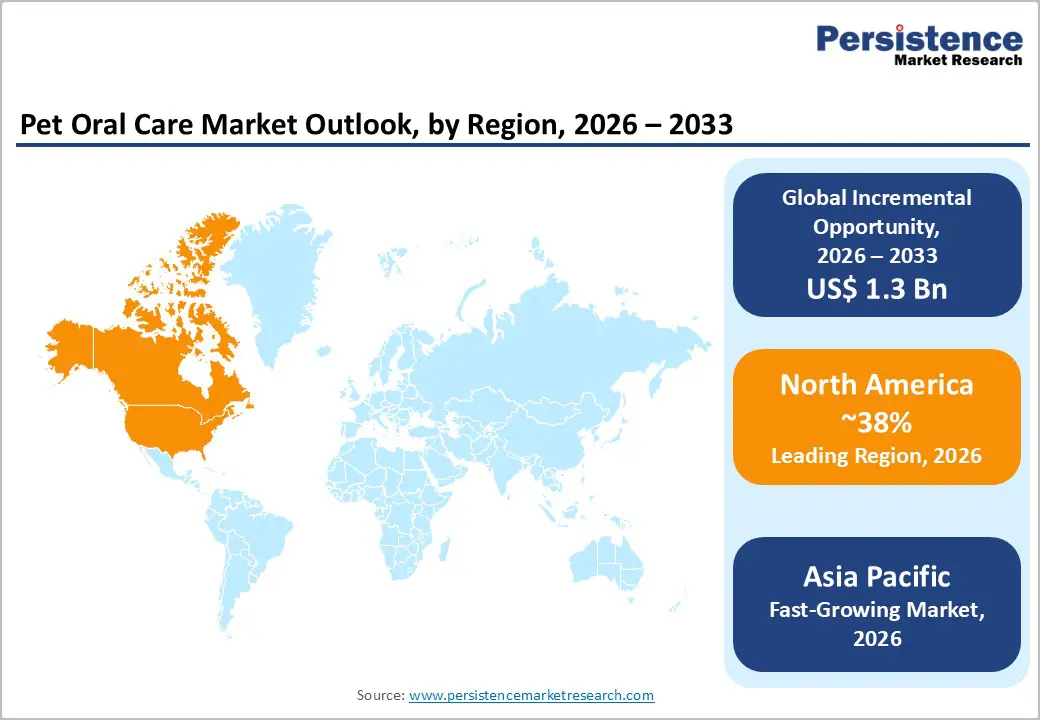

- Regional Leadership: North America is expected to account for around 38% of global revenue in 2026, while Asia Pacific is projected to be the fastest-growing market through 2033, reflecting income growth and expanding veterinary access.

- Competitive Environment: Strategic priorities include expanding subscription-based distribution, sustaining R&D in functional formulations, and strengthening veterinary partnerships to enhance brand credibility and visibility into recurring revenue.

- April 2025: Pooch & Mutt unveiled a 100% natural, kelp-based dental powder for dogs designed to reduce plaque and tartar buildup, freshen breath, and support healthy gums through an easy-to-mix daily supplement format.

|

Key Insights |

Details |

|---|---|

|

Pet Oral Care Market Size (2026E) |

US$ 2.2 Bn |

|

Market Value Forecast (2033F) |

US$ 3.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Pet Ownership and Institutionalization of Preventive Dental Care

Pet ownership has expanded consistently across developed and emerging economies. According to the APPA, over 66% of U.S. households own pets, with dogs and cats representing the majority, while the European Pet Food Industry Federation (FEDIAF) reports over 340 million pets across Europe. This structural rise in pet population has directly increased expenditure on preventive healthcare, including oral hygiene solutions. As companion animals are increasingly regarded as family members, owners are prioritizing long-term wellness over episodic treatment, strengthening demand for routine dental care products.

Periodontal disease affects approximately 70–80% of dogs over the age of three, according to the AVMA, positioning oral hygiene as a clinical necessity rather than a discretionary expense. In 2025, Chubb expanded its pet insurance coverage offerings in North America to improve access to preventive services, including dental evaluations, helping reduce out-of-pocket cost barriers. Airvet, a U.S.-based telehealth veterinary platform, reported continued expansion of its digital consultation services in 2025, enabling more frequent preventive care guidance. These developments, combined with regulatory oversight by the U.S. FDA and the European Medicines Agency (EMA), reinforce consumer trust and encourage consistent adoption of oral care.

Premiumization, Product Innovation, and Retail Transformation

Manufacturers are increasingly introducing enzymatic toothpastes, Veterinary Oral Health Council (VOHC)-approved dental chews, and veterinary-grade sprays aligned with evolving consumer preferences for clinically validated and natural formulations. Premium oral care offerings are gaining traction as pet owners seek scientifically supported preventive solutions. This shift toward value-added products enhances average selling prices and strengthens category profitability. The emphasis on convenience, including sprays and wipes for pets resistant to brushing, further expands addressable demand.

Retail and digital transformation are accelerating this momentum. In 2025, Mars Petcare expanded its direct-to-consumer and subscription capabilities across selected brands to improve the capture of recurring revenue. Similarly, Nestlé Purina PetCare strengthened its e-commerce partnerships and auto-replenishment offerings, enhancing purchase consistency for consumable categories such as dental chews. Sustained acquisition activity across the broader pet wellness sector also reflects strong investor confidence in preventive pet healthcare segments. These developments demonstrate how innovation, insurance expansion, and digital retail integration are structurally supporting growth in the pet oral care market.

Limited Awareness and Veterinary Infrastructure Gaps in Emerging Economies

Despite strong growth in North America and Europe, awareness of pet oral hygiene remains limited in parts of Asia, Latin America, and Africa. Veterinary infrastructure gaps and lower discretionary income constrain adoption. In 2025, several emerging markets reported that routine dental cleaning rates remained below 25% of pet-owning households. This reflects the limited prioritization of preventive dental care relative to vaccinations and essential treatments. Spending patterns in developing regions remain largely reactive rather than preventive, restricting demand for daily-use oral hygiene products.

Infrastructure limitations remain evident in 2025–2026. For example, Indian state authorities in Nagpur announced plans to modernize multiple government veterinary hospitals to improve diagnostic capacity and access to treatment, highlighting existing service gaps in semi-urban and rural areas. Such public upgrades underscore that veterinary accessibility remains uneven across emerging markets. Without structured outreach programs and widespread preventive education, awareness of periodontal risks remains low. Consequently, product penetration is concentrated in metropolitan areas, limiting broader market expansion and delaying category maturity in high-population regions.

Price Sensitivity and Increasing Regulatory Oversight

Premium oral care products carry higher price points compared to general pet grooming items. Enzymatic formulations and functional chews can cost 20–40% more than standard variants. In price-sensitive markets, consumers often substitute basic treats for specialized dental products. Even in developed economies, consumer spending on non-essential pet products has shown moderation under inflationary pressure. In 2025, U.K.-based retailer Pets at Home reported stronger growth in veterinary services compared to discretionary retail categories, reflecting cautious consumer behavior toward premium add-on products such as dental care items.

Regulatory oversight is also intensifying across key markets. In early 2026, the UK government proposed comprehensive reforms to the veterinary sector, including mandatory pricing transparency and enhanced regulatory supervision to address rising treatment costs. While aimed at consumer protection, such reforms increase compliance requirements and administrative burdens across the pet healthcare ecosystem. Additionally, regulatory frameworks such as the U.S. FDA, EFSA in Europe, and national authorities in Asia require strict ingredient validation and labeling standards. Approval delays can extend product launch timelines by 6–12 months, adding operational complexity and moderating innovation speed in the pet oral care category.

Digital Veterinary Platforms and Telehealth Integration

The rapid expansion of digital veterinary consultation platforms offers a scalable growth avenue for oral care education and product recommendations. In 2025, U.S.-based telehealth provider Airvet reported continued growth in remote consultation services, increasing access to licensed veterinarians across underserved regions. Digital consultations reduce geographic barriers and allow pet owners to seek guidance on preventive oral hygiene without requiring in-clinic visits. This increased accessibility strengthens awareness of periodontal risks and promotes consistent use of the product.

Telehealth integration also creates cross-selling opportunities for oral care brands. Many digital platforms now provide treatment follow-up reminders and preventive care guidance, which can be paired with subscription-based purchasing models. Automated reminders for dental checkups or plaque management reinforce routine consumption patterns. As younger, digitally native pet owners become the dominant demographic segment, online veterinary ecosystems are expected to play a larger role in influencing purchasing decisions. This convergence of digital health and consumer commerce enhances customer lifetime value and supports sustained category expansion.

Emerging Market Urbanization and Veterinary Infrastructure Investment

Rapid urbanization across Asia and parts of Latin America is reshaping pet ownership patterns and healthcare expectations. In 2025, several regional governments, including state authorities in India, announced modernization initiatives for public veterinary hospitals to improve diagnostics and treatment capacity. Such public investment signals increasing institutional recognition of companion animal healthcare needs. As veterinary infrastructure expands, access to preventive dentistry services is likely to improve, creating downstream demand for maintenance-oriented oral hygiene products.

Urban middle-class expansion is further supporting premium pet care adoption. Rising disposable incomes and exposure to global pet wellness standards are influencing purchasing decisions in metropolitan centers across China, India, and Southeast Asia. Organized retail penetration and e-commerce growth in these regions improve distribution efficiency and product availability. While awareness gaps persist in rural areas, concentrated urban adoption can significantly accelerate regional revenue contribution. Over time, infrastructure upgrades combined with rising income levels present one of the most scalable long-term opportunities for the global pet oral care market.

Category-wise Analysis

Product Type Insights

Chews & treats are estimated to account for approximately 40% of the pet oral care market's revenue share in 2026, maintaining their leadership position due to convenience, palatability, and strong repeat-purchase behavior. Their dual positioning as both reward-based treats and functional dental solutions strengthens consumer preference, particularly among first-time pet parents. The segment benefits from high visibility in organized retail and veterinary clinics, where impulse and recommendation-based purchases are common. Premiumization trends, including those driven by natural ingredients and grain-free variants, continue to support pricing power. In 2025, leading pet care manufacturer Mars Petcare expanded its GREENIES dental treats portfolio in Asia-Pacific markets, strengthening distribution through veterinary and specialty retail partnerships. Similarly, Nestlé Purina PetCare highlighted dental chew innovations under its DentaLife line during its 2025 global product showcases, emphasizing clinically tested plaque-reduction benefits.

Dental sprays and rinses are projected to be the fastest-growing product segment, with an estimated CAGR of 9.5% through 2033, driven by rising demand for non-invasive and brushing-free alternatives. Ease of application, portability, and alcohol-free formulations enhance usability. Urban pet owners, particularly in apartment-based households, show a stronger inclination toward low-effort oral hygiene solutions. Increasing online product discovery and subscription-based sales further accelerate adoption. Innovation in enzymatic and herbal-based formulations also strengthens consumer appeal. In 2026, TropiClean introduced an upgraded oral care spray line featuring naturally derived ingredients and vet-reviewed safety validation, expanding its e-commerce footprint. The AVMA reiterated its emphasis on preventive dental care awareness in its 2025 pet health campaigns, indirectly supporting alternative oral hygiene formats beyond traditional brushing. These developments align with shifting consumer behavior toward convenience-driven products.

Pet Type Insights

Dogs are anticipated to capture nearly 60% of the pet oral care market share in 2026, supported by higher ownership rates and greater clinical intervention frequency. The prevalence of canine dental disease contributes to stronger veterinary recommendations for routine oral hygiene maintenance. Larger body size and treat compatibility further enhance product utilization rates compared to other pets. Premium dog-specific dental chews and enzymatic toothpastes continue to occupy significant shelf space across specialty and veterinary channels. American Veterinary Dental College reinforced National Pet Dental Health Month initiatives, emphasizing preventive dental routines for dogs and increasing consumer engagement. Meanwhile, Colgate-Palmolive expanded its Hill’s Pet Nutrition oral care portfolio in select international markets during 2026, targeting clinically backed canine dental solutions. These strategic moves highlight continued industry alignment around preventive dog dental care.

Cats are likely represent a smaller share, but are nonetheless projected to register the fastest growth among pets, with a CAGR of approximately 10.1% through 2033. Rising urbanization and apartment living trends have accelerated feline adoption, particularly among younger demographics. Historically, product compatibility challenges limited growth; however, tailored flavor profiles and smaller-format dental solutions are improving acceptance. Increasing awareness of feline periodontal disease is gradually shifting owner behavior toward preventive care. Retailers are dedicating more shelf space to cat-specific oral hygiene SKUs. Digital education campaigns further contribute to incremental demand expansion. In 2026, Virbac expanded distribution of feline enzymatic toothpaste variants across European veterinary networks, focusing specifically on cat-friendly formulations. Additionally, public guidance updates from the British Veterinary Association in 2025 emphasized early dental screenings for cats and encouraged routine at-home maintenance. These developments support a gradual but meaningful behavioral shift among cat owners.

Regional Market Insights

North America Pet Oral Care Insights

North America is estimated to remain the largest regional market in 2026, accounting for approximately 38% of global revenue, supported by advanced veterinary infrastructure and high per-pet healthcare spending. The United States drives the majority of regional demand, reflecting strong awareness of preventive dental care and premium product adoption. According to data published by the American Pet Products Association, overall U.S. pet industry expenditure continues to exceed US$ 140 billion, with healthcare representing a significant share. Robust distribution through specialty retail chains, veterinary clinics, and expanding e-commerce platforms strengthens product accessibility. Regulatory oversight by the U.S. Food and Drug Administration ensures ingredient safety and transparency in labeling, reinforcing consumer confidence. Innovation pipelines remain active, particularly in enzymatic and natural formulations.

Canada complements regional performance through rising urban pet adoption and premiumization trends. High frequency of veterinary visits supports recurring purchases of oral hygiene products, especially chews and clinically endorsed solutions. Preventive healthcare campaigns continue to improve compliance among pet owners. Strong brand competition fosters product differentiation, particularly in natural and grain-free dental care variants. Subscription-based online sales channels are further enhancing repeat purchase behavior. Investment in sustainable packaging and clean-label positioning also resonates strongly with environmentally conscious consumers. These structural advantages are expected to sustain North America’s leadership over the forecast period.

Europe Pet Oral Care Insights

In Europe, the market for pet oral care products is spearheaded by Germany, the United Kingdom, France, and Spain, where demand is being fuelled by high pet ownership density and organized retail networks. Population data published by the FEDIAF confirms a substantial companion animal base across Western Europe, supporting steady product consumption. Harmonized regulatory frameworks overseen by the European Food Safety Authority ensure ingredient traceability and safety compliance. Consumer preference for scientifically validated formulations enhances trust in veterinary-recommended products. Growth remains consistent across specialty pet stores and clinic-based channels.

Sustainability trends are increasingly shaping purchasing decisions across the region. In 2025, several manufacturers introduced recyclable packaging and responsibly sourced ingredient lines, aligning with broader European environmental standards. Premium dental sticks and plant-based oral care solutions are gaining shelf visibility. E-commerce penetration continues to rise, particularly in the U.K. and Germany, supporting omnichannel retail strategies. Educational initiatives promoting preventive pet healthcare are also strengthening consumer engagement. While growth is not as rapid as in emerging economies, strong regulatory credibility and brand transparency sustain long-term stability. Europe is therefore expected to maintain its solid contribution within the global landscape.

Asia Pacific Pet Oral Care Insights

Asia Pacific is projected to be the fastest-growing market for pet oral care, with an estimated CAGR of approximately 8.2% through 2033, reflecting accelerating pet humanization trends. China and Japan represent the largest revenue contributors. Rapid urbanization and expanding middle-class incomes are increasing discretionary spending on companion animal health. Government-supported livestock and veterinary infrastructure programs in several countries are improving professional care access. Rising awareness of preventive dental maintenance is gradually shifting consumer purchasing patterns. Domestic manufacturing capabilities enhance cost competitiveness and product availability. These structural factors position the Asia Pacific as the primary growth engine for the global market.

Emerging markets such as India and ASEAN countries demonstrate strong untapped potential due to rising first-time pet ownership. Retail modernization and digital commerce platforms are accelerating product penetration beyond metropolitan centers. Regulatory frameworks continue to evolve, improving product standardization and import compliance across the region. Educational outreach from veterinary associations is gradually increasing awareness of periodontal disease prevention. International brands are expanding distribution partnerships to capture high-growth urban clusters. At the same time, local manufacturers are introducing competitively priced dental solutions tailored to regional preferences. As income levels and pet care sophistication advance, Asia Pacific is expected to consistently outpace other regions in overall growth momentum.

Competitive Landscape

The global pet oral care market structure is moderately consolidated, with leading players such as Mars Petcare Inc., Nestlé Purina PetCare, Colgate-Palmolive Company, and Virbac S.A. accounting for a substantial share of global revenue. These companies leverage strong brand portfolios, veterinary partnerships, and wide retail penetration to sustain market leadership. Their competitive strength lies in science-backed formulations and clinically supported dental solutions. Continuous R&D investment enables innovation in enzymatic toothpaste and functional chews. Established supply chains and omnichannel strategies further reinforce their market position.

Regional manufacturers and emerging direct-to-consumer brands are intensifying competition through niche positioning and premium natural formulations. Subscription-based models and e-commerce expansion are reshaping customer engagement and repeat purchases. Regulatory compliance and veterinary endorsement requirements create entry barriers for new players. However, digital marketing and online platforms are enabling smaller brands to scale rapidly. Gradual consolidation is expected as major companies pursue acquisitions and strategic partnerships to strengthen global presence.

Key Industry Developments

- In January 2026, pet health brand OMNI launched Dual-Texture Dental Sticks featuring a firm grooved outer shell for mechanical plaque removal and a soft core containing Ascophyllum nodosum seaweed to combat tartar buildup, offering a low-fat, hypoallergenic daily oral care solution for dogs.

- In October 2025, Phibro Animal Health Corporation introduced Restoris™, a piezoelectric dental gel for dogs with periodontal disease that uses microcurrent-generating particles to stimulate bone growth, reduce periodontal pocket depth, and support long-term oral health restoration.

- In July 2025, Pet Honesty expanded its feline oral care portfolio with Fresh Breath Dental Bites, a clean-label, dual-texture supplement formulated with ingredients such as kelp, postbiotics, parsley, and green tea to support gum health, reduce plaque and tartar, and improve breath without brushing.

Pet Oral Care Market Scope Report

| Report Attribute | Details |

|---|---|

| Historical Data/Actuals | 2020 – 2025 |

| Forecast Period | 2026 – 2033 |

| Market Analysis Units | Value: US$ Bn/Mn, Volume: As Applicable |

| Geographical Coverage |

|

| Segmental Coverage |

|

| Competitive Analysis |

|

| Report Highlights |

|

Companies Covered in Pet Oral Care Market

- Mars Petcare

- Nestlé Purina PetCare

- Colgate-Palmolive

- Virbac

- Vetoquinol

- Dechra Pharmaceuticals

- PetzLife

- TropiClean

- ImRex Inc.

- Ceva Santé Animale

- Hill’s Pet Nutrition

- Beaphar

Frequently Asked Questions

The global pet oral care market is projected to reach US$ 2.3 billion in 2026.

Rising pet humanization, increasing veterinary recommendations for preventive dentistry, and expanding premium product adoption are driving the market.

The market is poised to witness a CAGR of 7.5% from 2026 to 2033.

Manufacturers can capitalize on premium formulations, subscription-based e-commerce models, and emerging market penetration to unlock new growth opportunities.

Mars Petcare Inc., Colgate-Palmolive Company, Nestlé Purina PetCare, and Virbac S.A. are some of the leading global market players.